SHI 12.18.19 – Goodbye to an Exciting Year

SHI 12.11.19 – Folks are Working!

December 11, 2019

SHI 1/1/2020 – Retooling and Reflecting for a New Decade

January 1, 2020

“Say what you want about 2019, it was an exciting year.”

Lots happened. Whether viewed thru a political, economic, or financial lens, the year held something for everyone.

For a while there, it looked like the FED planned to push us right into a recession. Then came the pivot: The FED reversed course, reduced short-term rates, calming the fears of investors and forecasters alike. I believe the FEDs move, combined with the dominance of the US dollar and the resilience of our economic engine, will prevent our economy from contracting in the near term. But make no mistake: I believe whatever GDP growth we see in 2020 will be paltry and weak at best. Of course, forecasters are eying 2020 and offering widely divergent predictions. Let’s take a look at what some of the talking heads are saying … and as always, I’ll offer thoughts of my own for 2020 GDP growth, inflation rates and interest rates.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will be true for years to come.

But is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $85 trillion today. According to the most recent estimate, US ‘current dollar’ GDP now exceeds $21.53 trillion. In Q3 of 2019, nominal GDP grew by 3.5%, following a 4.7% annualized growth rate in Q2. The US still produces about 25% of global GDP. Other than China — in a distant ‘second place’ at around $13 trillion — the GDP of no other country is close. The GDP output of the 28 countries of the European Union collectively approximates US GDP. So, together, the U.S., the EU and China generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Viewed holistically, we end 2019 with the US economy in fairly good shape. Sure, we still face plenty of challenges, issues and detractors. But the US is now deep into the longest economic expansion on record, the unemployment rates is the lowest it’s been in 50 years, and it’s never been cheaper for folks to borrow money to purchase houses, cars, and other stuff. This all sounds pretty good to me!

So what will 2020 be like? What are the forecasters saying?

It depends on who you ask. For example, if you ask the FED and the economic eggheads in their Atlanta and NYC branches, you’ll get a significantly divergent forecast for Q4 GDP. The folks in Atlanta are forecasting a 2.3% growth rate for Q4; in NYC, they’re far more restrained. They feel Q4 will only crank out a 0.7% growth rate. Ouch. And the forecasters in the NY FED are presently forecasting a 0.82% growth rate for Q1, 2020. For the entire year of 2020, members of the Federal Reserve Board are targeting a GDP growth rate of 2.0%, down from an estimated 2.2% in 2019. And they expect it to shrink to 1.9% in 2021.

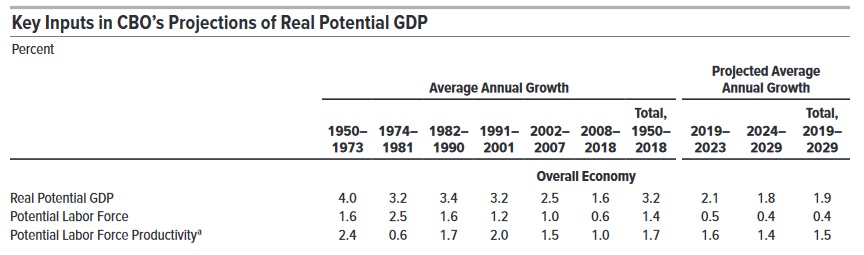

The Congressional Budget Office, known as the CBO, expects 2020 GDP to be a hair higher. And they are forecasting a deficit of just over $1 trillion for fiscal 2020. Why can’t the US economy grow faster than the FED and CBO forecast of around 2%? Frankly, we don’t have the horsepower. Take a look at the graphic below:

Between 1950 and 1973, GDP growth averaged 4.0%. Pretty amazing when compared to today’s growth rates, right? Well, look at the averages for labor force growth and productivity growth. And now, compare those to the forecasts for 2019 to 2029. There’s the loss in horsepower. The labor force growth forecast is more certain than the labor productivity forecast. Productivity can change significantly depending on technological advancement. So we’ll see how this shakes out. But after decades of falling fertility rates, the labor force is growing much slower than ever. This is a fact. And the more that labor force growth decelerates, the less horsepower we have to generate GDP growth.

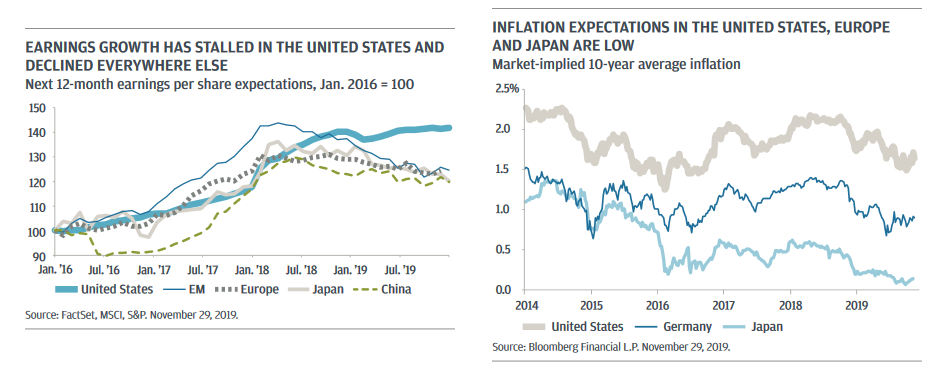

Demographics will continue to play an oversized role in this drama. Behavioral characteristics of our aging population, combined with the stunted growth of our labor force, will continue to put downward pressure on all aspects of economic and financial growth. I believe these factors are largely responsible for flat-lining corporate earnings growth here in the US and earnings declines in Europe and Japan.

The folks at Bank of America have similar opinions on GDP growth … but they feel corporate earnings will begin to improve:

“We believe a new cyclical upswing is already underway as a global economic pick-up is expected in 2020 with non-US economies bottoming out in Q1 and the U.S. economy stabilizing around trend at 1.7%–2%. Our expectations are for (corporate) earnings to trough soon and accelerate through 2020 as economic growth in the U.S. and globally start to stabilize.”

I don’t agree on their earnings call. I think the current trough will become the new normal.

The same demographic factors play a big role for inflation. The FED is forecasting a core inflation rate of 1.9% in 2020. I think they are overly optimistic. I don’t believe inflation will get that high. And the financial markets agree with me. Take a look at the graphic below, courtesy of JP Morgan:

As we roll into 2020, remember that our economy is enjoying the longest economic expansion — now well over 10 years — since the NBER began tracking economic cycles around the time of the Civil War. This expansion hasn’t been the fastest or showiest (is that even a word?); but, it’s been a real steady-eddie, continuing to defy forecasts and predictions of its demise. Earlier this year, I was one of the folks predicting 2020 would usher in a recession. No longer. The FED rate pivot helped … and recent changes in the level of vitriol in the US/China trade war give me hope for 2020. Of course, global trade and supply chains have taken some big hits during the war, and the damage is done. But not so much, I suspect, that if cooler heads continue to prevail we can’t expect a bit of growth in 2020.

And a bit is all I’m expecting as this year ends. I predict 2020 GDP growth will not exceed 2% … and will probably be closer to the 1% mark. But this is still better than a recession. Of course, the off-shoot from my GDP and corporate earnings forecasts is a prediction for a very flat stock market in 2020. More on this next year, but I don’t expect to see much more stock market value growth in 2020; frankly, I believe much of the growth we saw in 2019 had more to do with interest rate compression than improvements in corporate earnings.

Interestingly, I think the steak houses are telling us much the same thing.

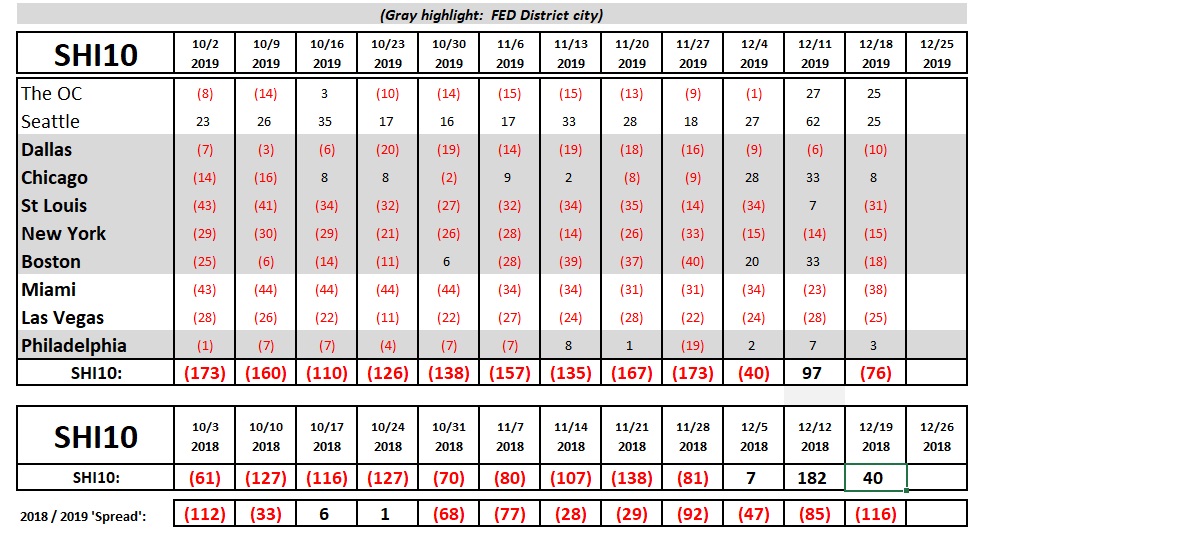

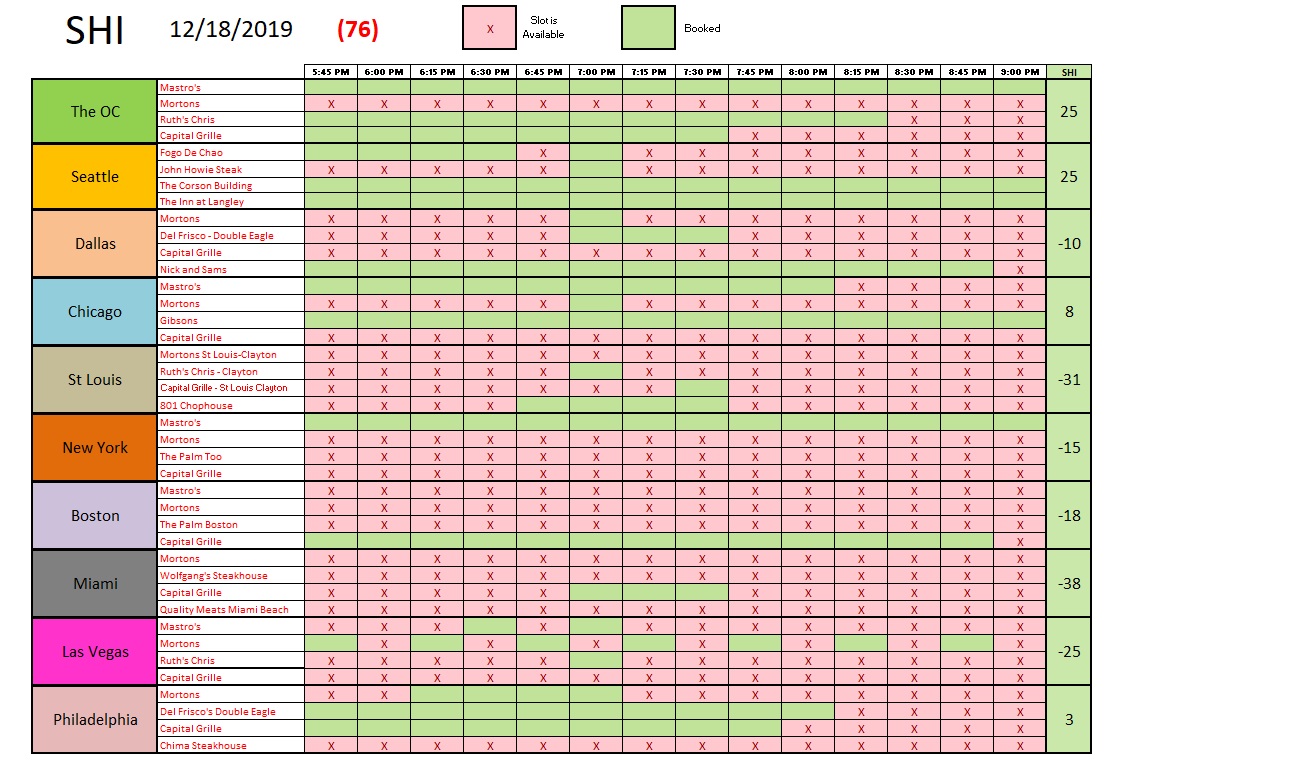

The SHI this week kinda fell off the cliff. This week in 2018, the SHI10 reading was a positive 40. Not this week. Not much positive here. Reservation demand in every market declined; only in the OC and Philly was the reading similar to last week. I was a surprised by the severity of the decline. I expected the Saturday before a Wednesday Christmas to show strong demand. Nope. Not this year. There will be no T-bones in Mastro’s stocking this year. Just a lump of coal.

On the good news side of the ledger, with enough time and pressure, coal becomes a diamond! 🙂

We see far less green this week. Most reservations slots are still available across most markets.

Using reservation demand for expensive steakhouses continues to be an interesting, somewhat tongue-in-cheek way to track the economy. We’ll continue to do so in 2020, but expect a few refinements. More on this in 2020.

As Christmas and New Years both fall on a Wednesday, this is my last blog for 2019. I’m signing off … and in doing so, I wish you JOY and PEAS in 2020! (See what I did there? Yep, I had to end the year with one more food reference.) 🙂

– Terry Liebman