SHI 6.10.2020 – Goodbye Old Friend

SHI 6.3.20 – Disasters: Natural and Unnatural

June 3, 2020

SHI 6.17.20 – The Beef Index

June 17, 2020

It’s official. It was bound to happen eventually, but I’m sure, like me, you hoped it would be many years hence. In light of recent events, we can’t be surprised.

According to the respected expert, the National Bureau of Economic Analysis, also known as the NBER, we have entered a recession.

” The longest-ever US economic expansion officially ended in February of 2020. “

Goodbye old friend. You will be missed.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Before COVID-19, the world’s annual GDP was about $85 trillion today. No longer. It has shrunk sizable during ‘The Great Lockdown.’ I did not coin this phrase — the IMF did. The same folks who track global GDP. Until recently, annual US GDP exceeded $21.7 trillion. Together, the U.S., the EU and China still generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Here is what the NBER had to say: “The Business Cycle Dating Committee of the National Bureau of Economic Research, which maintains a chronology of the peaks and troughs in economic activity in the United States, has determined that a peak in monthly economic activity occurred in the US economy in February 2020. The peak marks the end of the expansion that began in June 2009 and the beginning of a recession. The expansion lasted 128 months.”

OK. So. We’re now in a recession. Got it. Like me, you’re probably wondering how long the effects of this downturn might last.

Would you believe 40 years?

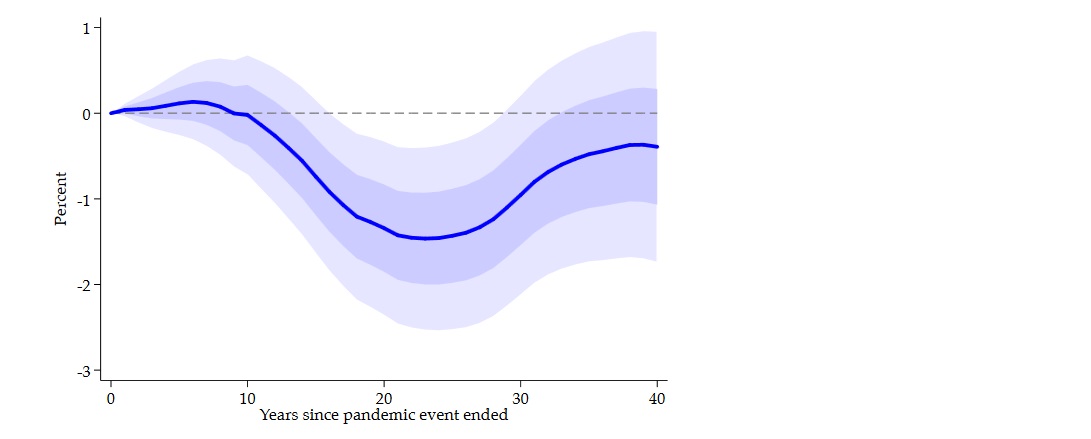

Neither would I. However, in March, a well-known economist at the San Francisco FED, Oscar Jorda, and a few of his friends released a paper entitled, “Longer-run economic consequences of pandemics” and came to this conclusion:

“At about four decades later, the natural (interest) rate returns to the level it would be expected to have had the pandemic not taken place.”

Amazing. Here’s a bit more detail:

“We study rates of return on assets using a data-set stretching back to the 14th century, focusing on 15 major pandemics where more than 100,000 people died. In addition, we include major armed conflicts resulting in a similarly large death toll. Significant macroeconomic after-effects of the pandemics persist for about 40 years, with real rates of return substantially depressed. In contrast, we find that wars have no such effect, indeed the opposite. This is consistent with the destruction of capital that happens in wars, but not in pandemics. Using more sparse data, we find real wages somewhat elevated following pandemics. The findings are consistent with pandemics inducing labor scarcity and/or a shift to greater precautionary savings.”

I find the “war vs. pandemic” comparison is interesting. It makes sense that a wide-spread pandemic “induces labor scarcity” … when viewed thru an economist’s lens.

But apparently historic pandemics did not trigger “capital scarcity.” And thus, “real” interest rates, and other rates of return, have historically been depressed for 40 years following a pandemic! Per the authors:

“These results are staggering and speak of the disproportionate effects on the labor force relative to land (and later capital) that pandemics had throughout centuries. It is well known that after major recessions cased by financial crises, history shows that real safe rate scan be depressed for 5 to 10 years, but the responses here display even more pronounced persistence.“

Look at the chart below: 20 years after the pandemic, rates remained more than 2% below their prior levels.

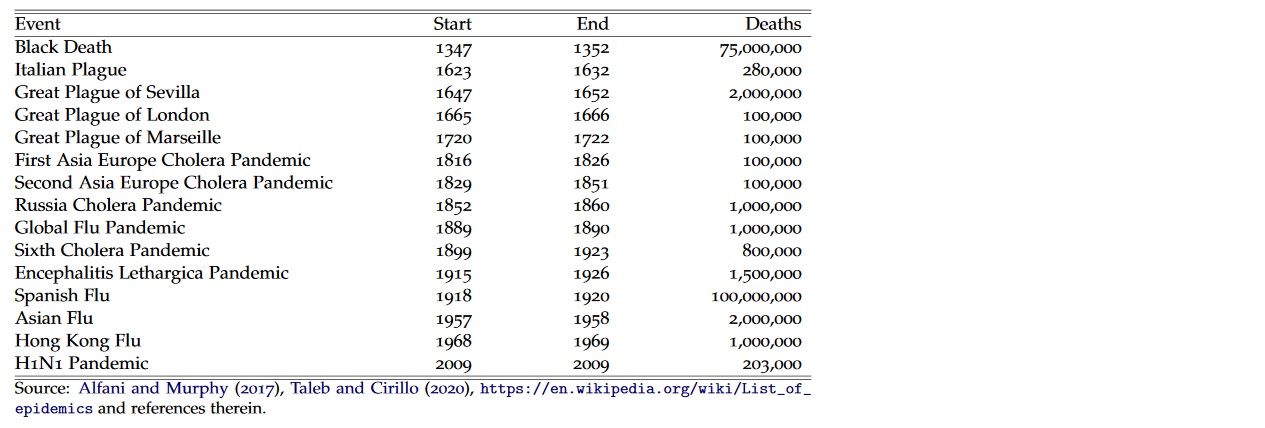

To be frank, I was surprised by the number of global pandemics in the past 600 years, as you can see in the chart below. At the time “The Black Death” began, world population was estimated at 475 million. Staggering.

Will this pandemic cause the same, protracted long-term effect on yields? No, I don’t think we’ll see a similar duration … but I feel we will see the yield decline. I don’t believe we will have a 40-year “tail” from this event. But I think the world will experience a protracted reduction in real rates of return. A decline that could last for 2 or more years.

In fact, the FED just finished their meeting and concluded:

“The coronavirus outbreak is causing tremendous human and economic hardship across the United States and around the world. The virus and the measures taken to protect public health have induced sharp declines in economic activity and a surge in job losses. Weaker demand and significantly lower oil prices are holding down consumer price inflation. Financial conditions have improved, in part reflecting policy measures to support the economy and the flow of credit to U.S. households and businesses.

The ongoing public health crisis will weigh heavily on economic activity, employment, and inflation in the near term, and poses considerable risks to the economic outlook over the medium term. In light of these developments, the Committee decided to maintain the target range for the federal funds rate at 0 to 1/4 percent. The Committee expects to maintain this target range until it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals.”

Interest rates will remain low. The FED expects their short-term ‘federal funds’ rate to remain at 0.1% thru the end of 2021, at the minimum, and probably thru 2022. This is effectively zero. For the rest of 2020, 2021 and probably 2022. Wow.

And while the FED is forecasting a 6.5% GDP reduction in 2020, they expect a bounce-back to a 5% growth rate in 2021. This outcome would be a victory, in my eyes, if achieved.

Here are the FED forecasts, if you’re interested in seeing more:

https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20200610.pdf

– Terry Liebman

{kind=link}