SHI 6.26.24 – A Whole Lotta Red

SHI 6.19.24 – Meaty Observations

June 20, 2024

SHI 7.3.24 – Musical Chairs

July 3, 2024

Last week, I opined that our US economy is slowing slowing.

I think the FED is getting the “soft landing” they have attempted to engineer.

This week, we have more evidence supporting my belief. Not only is the SHI40 quite low this week, but the GDP report, released today, also reflects this same weakness. However, on the other hand, that same GDP report also showed the continuing strength of the American economy.

“

Weak? Strong? Confused?.“

“Weak? Strong? Confused?.“

I get it. This is a bit confusing. Let me explain.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. But is the US economy expanding or contracting? Expanding …. By the end 2023, in ‘current-dollar‘ terms, US annual economic output rose to an annualized rate of $27.94 trillion. After enduring the fastest FED rate hike in over 40 years, America’s current-dollar GDP still increased at an annualized rate of 4.8% during the fourth quarter of 2023. Even the ‘real’ GDP growth rate was strong … clocking in at the annual rate of 3.3% during Q4.

According to the IMF, the world’s annual GDP expanded to over $105 trillion in 2022. Further, IMF expects global GDP to reach almost $135 trillion by 2028 — an increase of more than 28% in just 5 years.

America’s GDP remains around 25% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

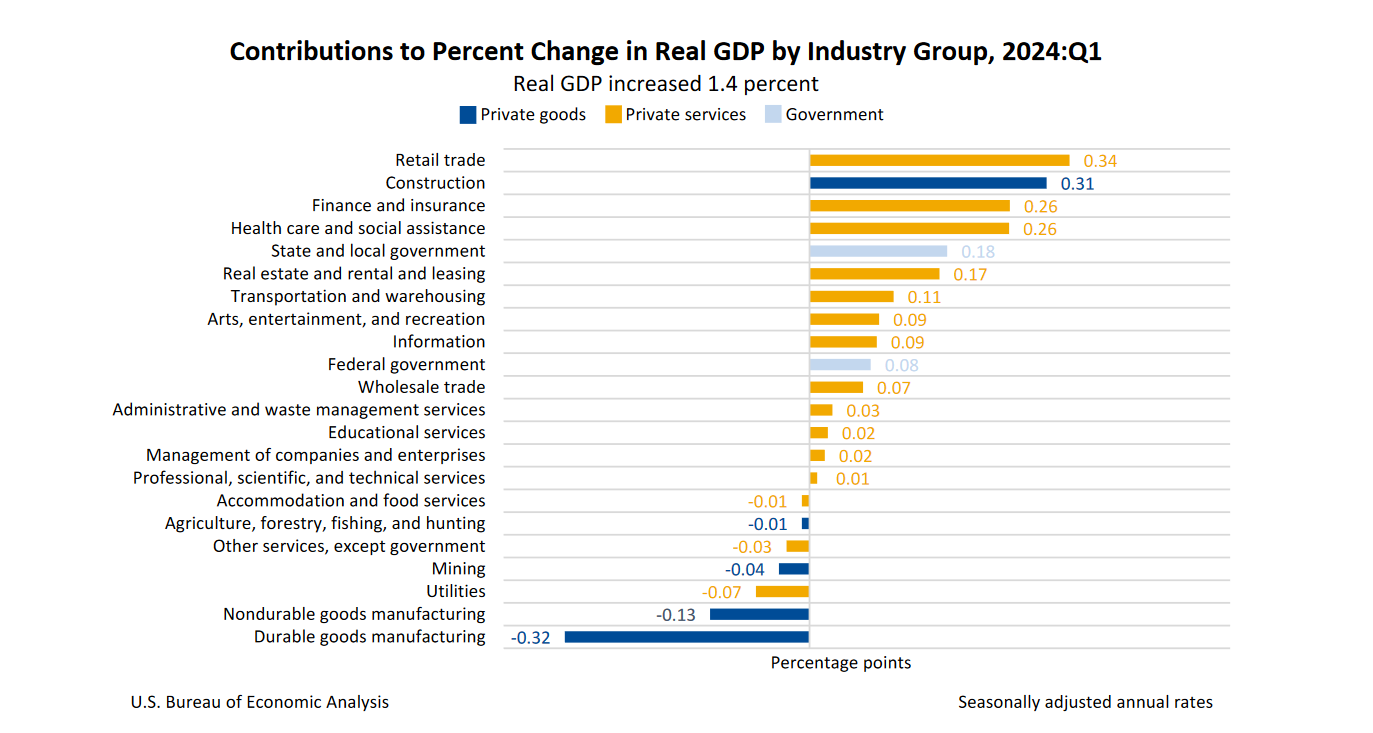

I’ll start with today’s GDP report, courtesy of the Bureau of Labor Statistics (BLS). According to that report, America’s GDP grew at the annual rate of 1.4% in the first quarter of 2024. For context, that same figure was 3.4% in the prior quarter. Clearly, GDP growth was lower in Q1. But, remember, this is the ‘real’ GDP figure. The ‘current dollar’ number was adjusted down, reduced by an inflation factor, to reach the 1.4% ‘real’ growth rate.

In current dollars, our economy grew at the annualized rate of 4.5% — a figure I consider to be quite robust.

Again, for context, while Q4 2023 reached a 3.4% ‘real’ growth rate, the ‘current dollar’ rate was 5.1% — almost equal to this quarter’s number. The difference, therefore, is the inflation factor adjustment.

Most assuredly, there were winners and losers in Q1. Take a look:

The biggest losers for the quarter, clearly, were in the manufacturing of goods. Our economy can be parsed many ways, but essentially it is made up of two components: Goods and Services. Services remain in high demand. Goods, on the other hand, are quite weak these days. Essentially …

… People are buying less stuff, while at the same time, enjoying more experiences.

There you have it.

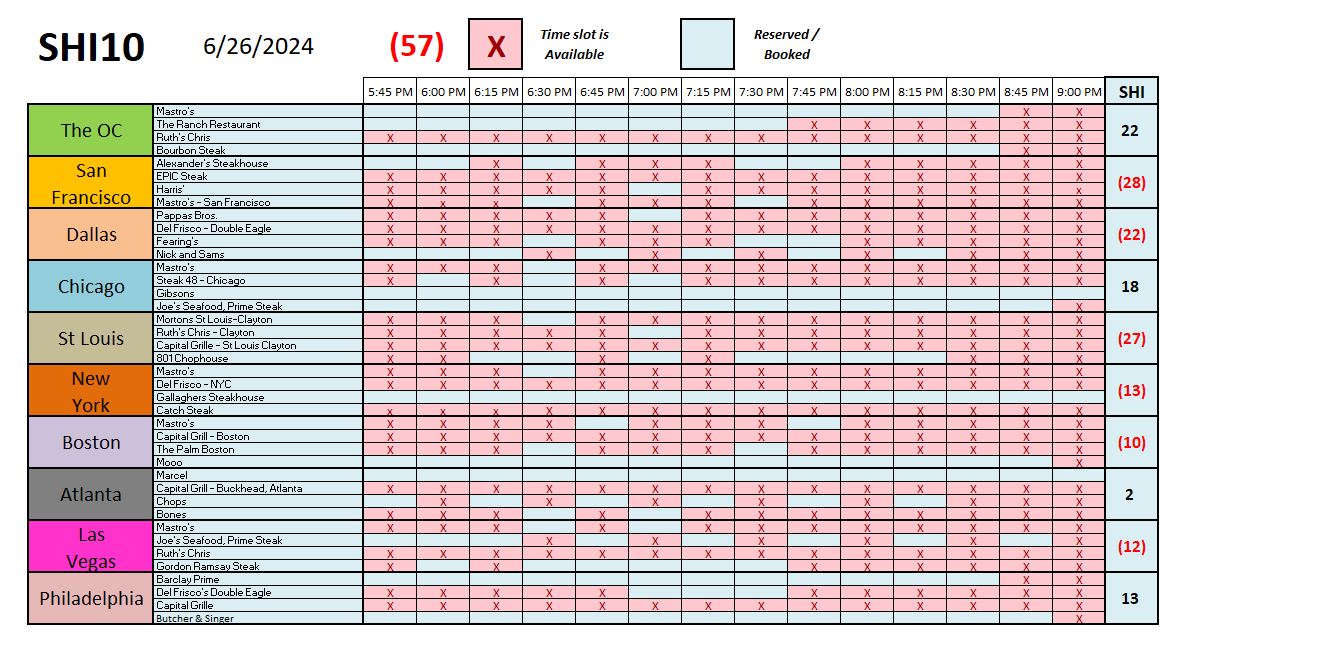

Then we have the steakhouses. Here’s the long-term chart:

This week we see a whole lotta red. And I’m not talking about rare beef. This weeks numbers are not good.

This trend has been building for months now. Other than the 180 SHI10 reading during the week of 5/8, every SHI10 reading since the beginning of Q2, 2024 has been in the double digits at best — and this week we’re firmly in the red.

Here is the 40-restaurant chart. Again, we see a whole lotta red where previously we had blue.

Both the GDP report and the SHI10 suggest a slowly slowing economy.

But, again, don’t panic. Seriously. This is a good thing. Our economy has been smoking-hot for too long now. Some slowing is a good thing. GDP growth remains quite robust in my book. And it looks like the Atlanta FED agrees with me.

The latest estimate from the Atlanta FED for Q2 GDP growth is 2.7%. And, of course, that’s a ‘real’ number.

So chill. Things are just fine. Go enjoy a beautiful steak, drink a nice glass of wine, or two, and relax.

<:> Terry Liebman