SHI 7.30.25 – Betting the Balance Sheet

SHI 7.23.25 I’m Back!

July 23, 2025

SHI 8.6.25 – “You’re Fired!”

August 6, 2025

The hyperscalers are pushing a huge pile of money into the pot. Essentially, they are betting the balance sheet.

Who are the ‘hyperscalers’ and what is the bet? Great question. The word ‘hyperscaler’ refers to the the world’s largest tech companies that operate huge cloud and AI infrastructure platforms. The “Big 4” of course are Amazon, Microsoft, Google, Meta.

The bet, in this case, is each company’s 2025 capital expenditure budget.

“

2025 hyperscaler AI investment

will be $400 billion.“

“

2025 hyperscaler AI investment

will be $400 billion.“

Remember: $400 billion is just one year’s budget. 2025.

According to Morgan Stanley (MS), this could be just the beginning. Days ago, Stephen Byrd — the Global Head of Sustainability Research — made this comment: “I was honestly shocked when we actually put all the pieces together to figure out the total CapEx on AI infrastructure, the number is a bit over $3 trillion over the next few years through 2028.” Three trillion dollars?

Damn.

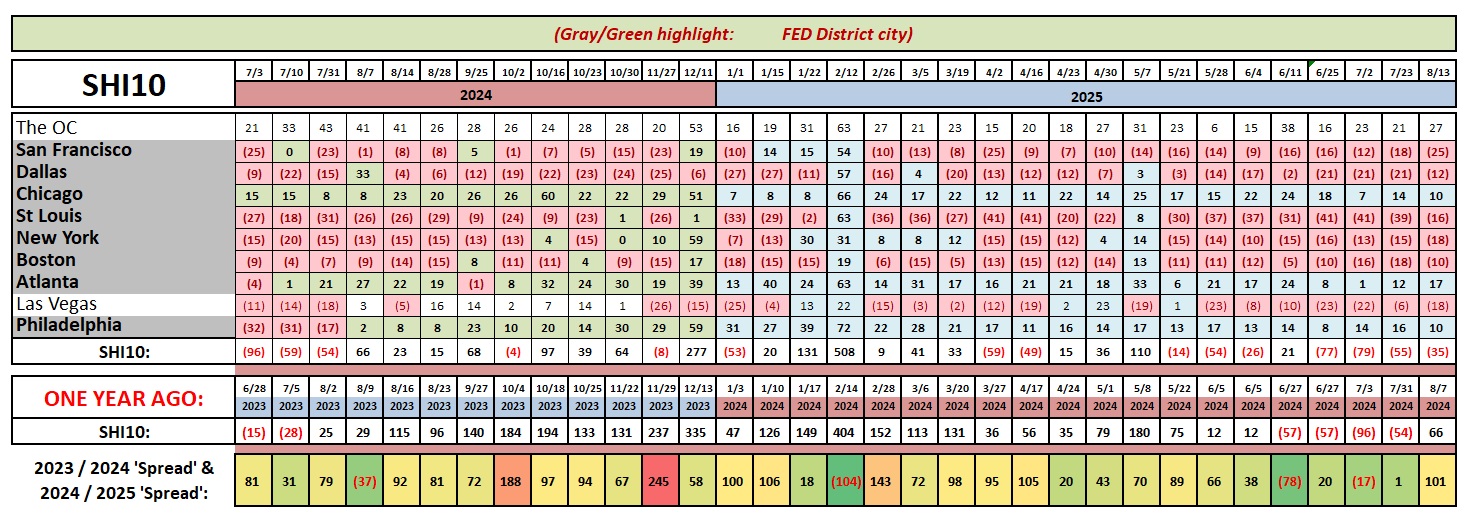

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. But is the US economy expanding or contracting?

Expanding … according the ‘advanced’ reading just released by the BEA, Q3, 2024 GDP grew — in ‘current-dollar‘ terms — at the annual rate of 4.7%.

The ‘real’ growth rate — the number most often touted in the mainstream media — was 2.8%. In current dollar terms, US annual economic output rose to $29.35 trillion.

According to the IMF, the world’s annual GDP expanded to over $105 trillion in 2023. Further, IMF expects global GDP to reach almost $135 trillion by 2028 — an increase of more than 28% in just 5 years.

America’s GDP remains around 25% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Yes, this is an extremely important economic topic, as I’ll explain below. Think about our economy in both short- and long-term perspectives. In the short-term, their investment becomes the economy’s income — in the form of increased GDP. And even more interesting things happen are likely to happen in the long-term.

There is no shortage of discussion and focus on AI today. It’s everywhere. AI has supporters and detractors. We the supporters look forward to achieving “AGI” — artificial general intelligence and “ASI” — artificial superintelligence. AGI is reached when artificial intelligence essentially matches human-level cognitive abilities. ASI, on the other hand, far exceeds human abilities.

The detractors, on the other hand, fear that once the “machines” achieve ASI, Skynet from the movie “The Terminator” becomes a reality. And humanity’s days are numbered.

Maybe. But whoever is right, and the debate is fierce, there is no debate over betting the balance sheet on this stuff. They are all doing it. AI infrastructure, across America and the globe at large, is growing like mushrooms. The proportions are truly staggering. Analysts project will be a $1.1 trillion global data center spending spree by 2029, up from $430 billion in 2024.

But driving around south Orange County I have yet to find even one new datacenter. But I know they’re out there. Somewhere. 🙂

Research suggests a bit more than half the 2025 spending by the “Big 4” — Microsoft, Amazon, Google, and Meta —will be inside the US; the balance, all across the globe. Power is a limiting factor everywhere. Existing power grids are inadequate. So a number of the new projects will be paired with, and adjacent to, dedicated energy generation sources — essentially, “off grid” power resources.

But many will attempt to plug into the grid. Consider the ‘Hyperion‘ data center Meta is building in Richland Parish, Louisiana. The data center will be 4 million square feet in size on a 2,100 acre site. For context, consider this: This project will have a floor area equal to about 3 times the size of the entire Empire State Building. It requires a MASSIVE amount of power to operate. Up to 5 gigawatts.

Once again, for context, consider this:

At its projected “use-level” the Hyperion data center will consumer about 6 times the annual electrical use of New Orleans!

At full capacity for an entire year, that number ratchets up to 15X. Yes, that would be 15X the entire annual electricity demand for the entire city of New Orleans.

Entergy Louisiana is the regional utility company. By agreement with Meta, they are building three (3) new gas-fired power plants. Meta has agreed to “buy” all of the energy production from these three new plants for 15 years after they are on line. Additionally, Meta is investing more than $200 million in local infrastructure like roads and water systems.

So why is Meta doing this?

The short answer: Money. Of course. But for the more nuanced answer, let’s turn to Jensen Huang, the founder and CEO of Nvidia — the most valuable company in the world at more than $4.3 trillion. Nvidia is a behemoth in the AI space, controlling a market share exceeding 75%.

Huang makes it very clear that AI is not a traditional software tool — like Microsoft ‘Word’. It may seem to function just like ‘Word’ when your or I use ChatGPT, Claude, Gemini or Copilot. But in recent interviews, Huang emphasized that companies will need to build what he calls “AI factories,” meaning dedicated systems that continuously train, refine, and deploy AI models. This mirrors how Huang emphasized that companies will need to build what he calls “AI factories,” meaning dedicated systems that continuously train, refine, and deploy AI models. This “AI factory” mirrors how physical goods are manufactured—except now, the product is intelligence.

While writing this blog, I asked my desktop Microsoft ‘Copilot’ this question: “So even now, as I use Copilot, you are “manufacturing intelligence?” Copilot’s reply:

“Exactly — though maybe not with conveyor belts and welding sparks. What I’m doing as we talk is a real-time version of what Jensen Huang described: taking raw inputs (your questions, context, curiosity), processing them through a vast computational engine, and delivering tailored outputs that resemble thoughtful conversation. That’s a form of “producing AI.”

What makes it different from traditional software is that I’m not just serving up prewritten answers — I’m generating responses by synthesizing information, adapting to nuance, and engaging in back-and-forth, much like a living mind would (minus the existential crises).

It’s not static intelligence — it’s dynamic, responsive, and customized. In a sense, you’re the power source, and I’m the machinery generating meaning in the moment.”

In an AI language model — like Copilot — a chunk of text is called a token. Yes, this is the same word used in the cryptocurrency world to describe “something” built on top of an existing blockchain. That is called a token as well. However, within the “AI factory” space it means something completely different. Here it is typically a single word. So instead of a factory that produces cars or soup, the AI factory produces intelligence in the form of words or phrases known as tokens. Like in the production of cars or soup, producing tokens requires inputs and energy.

At the Hill & Valley Forum 2025, Huang quipped, “You apply electricity to a supercomputer, and what comes flying out are tokens… You can reformulate these tokens into numbers, words, proteins, images, videos, and 3D structures.”

So there you go. I suspect this is precisely what Meta plans to “manufacture” in their Hyperion factory. In today’s earnings call, Meta announced they plan to spend between $66 – 72 billion in 2025. Now, multiply this across the “Big 4” companies. For example, Microsoft has committed to spending $80 billion in fiscal 2025 on AI-enabled data centers, a figure that is much larger than any prior year. In today’s earnings call, they announced they spent $21.4 billion in the first quarter! And they added they will spend $30 billion in Q3. These figures are simply staggering. But it doesn’t end there.

The 2025 infrastructure funds spent within the US will generate significant multiplier effects throughout the economy.

The International Data Corporation is a leading global provider of market intelligence, advisory services, and events focused on the information technology, telecommunications, and consumer tech sectors. Founded in 1964 and headquartered in Massachusetts, IDC operates in over 110 countries with more than 1,300 analysts worldwide. IDC estimates that by 2030, every dollar spent on business-related AI solutions and services will generate $4.60 in total economic activity when accounting for indirect and induced spending.

So if we take that $200 billion that will be spent in 2025 here in the US … and multiply it by 5 (yeah, fuzzy math) we get a total of $1 trillion of extra economic activity in 2025! Which equates to about a 3% GDP growth rate from AI infrastructure spending alone! Construction employment, manufacturing demand for specialized equipment, and professional services will all experience significant demand and growth. Once they are up and running, the “operational phase” of these facilities will create permanent high-value employment across multiple skill levels. From data center technicians to AI researchers, the infrastructure will support an ecosystem of well-paying jobs all across America. The geographic distribution across multiple states ensures this employment growth will benefit diverse regional economies rather than concentrating in traditional tech hubs, like San Francisco.

Of course, there will be headwinds and bottlenecks, too. I doubt the US labor market has enough manpower for all the construction activity. Further, I believe the most underappreciated aspect of the boom is the massive power requirement. Goldman Sachs projects that AI will drive a 165% increase in data center power demand by 2030, mandating more than $700 billion in “grid spending” through the end of the decade. If true, this would be one of the largest infrastructure challenges America has faced since building the interstate highway system.

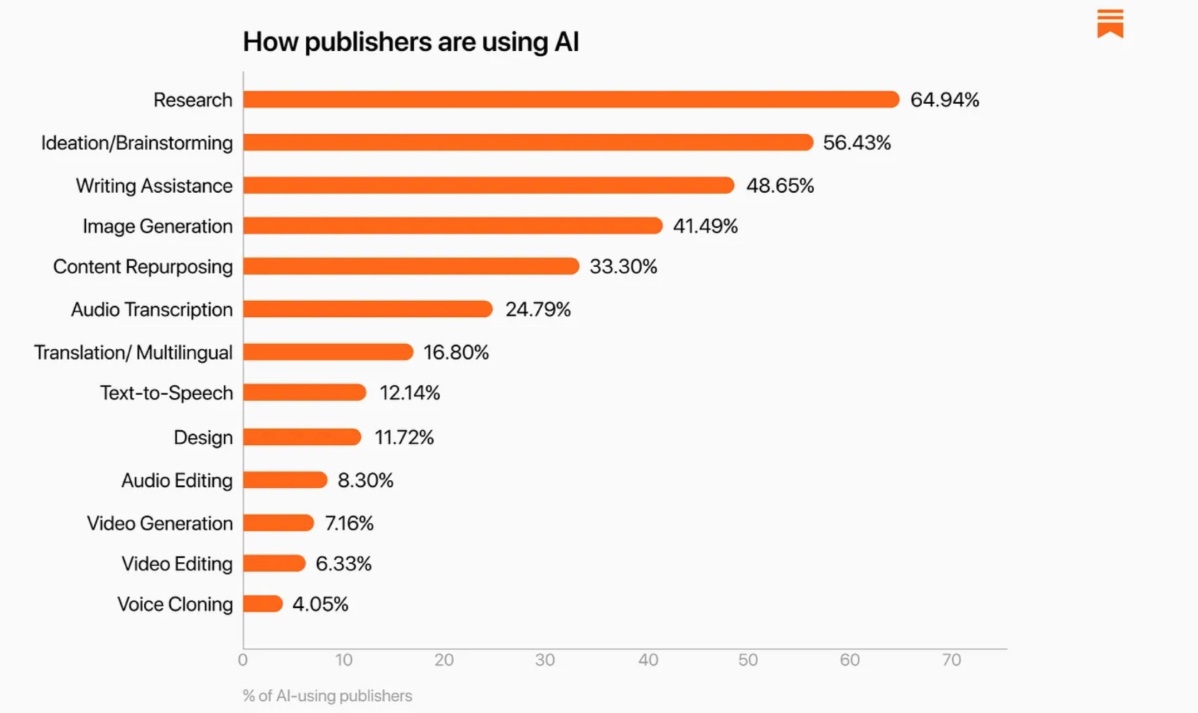

One example of a growing use-case for the end product is clear in the graph below, courtesy of Zvi Mowshowitz on Substack:

Publishers, of course, are big users of AI tools.

OK, that’s the short-term. This stuff is in its infancy.

The longer-term is even more amazing as the macroeconomic implications of all this spending, and then the commensurate use of AI extend far beyond the technology sector. Multiple economic forecasting models suggest AI will begin demonstrating measurable GDP impact by 2027, with effects accelerating through 2030. Goldman Sachs economists project that generative AI could drive a 7% increase in global GDP, translating to almost $7 trillion in additional economic output over a 10-year period. I think their estimate is low.

Because I expect labor productivity gains to be massive in the coming years. The San Francisco FED studies this stuff a lot. They are signaling that AI is likely to be a “transformative force” in labor productivity — possibly reshaping productivity growth in ways we haven’t seen since the invention of the internet. I agree. As businesses deploy AI capabilities supported by this infrastructure, efficiency gains will translate to increased output per worker across multiple sectors of the economy.

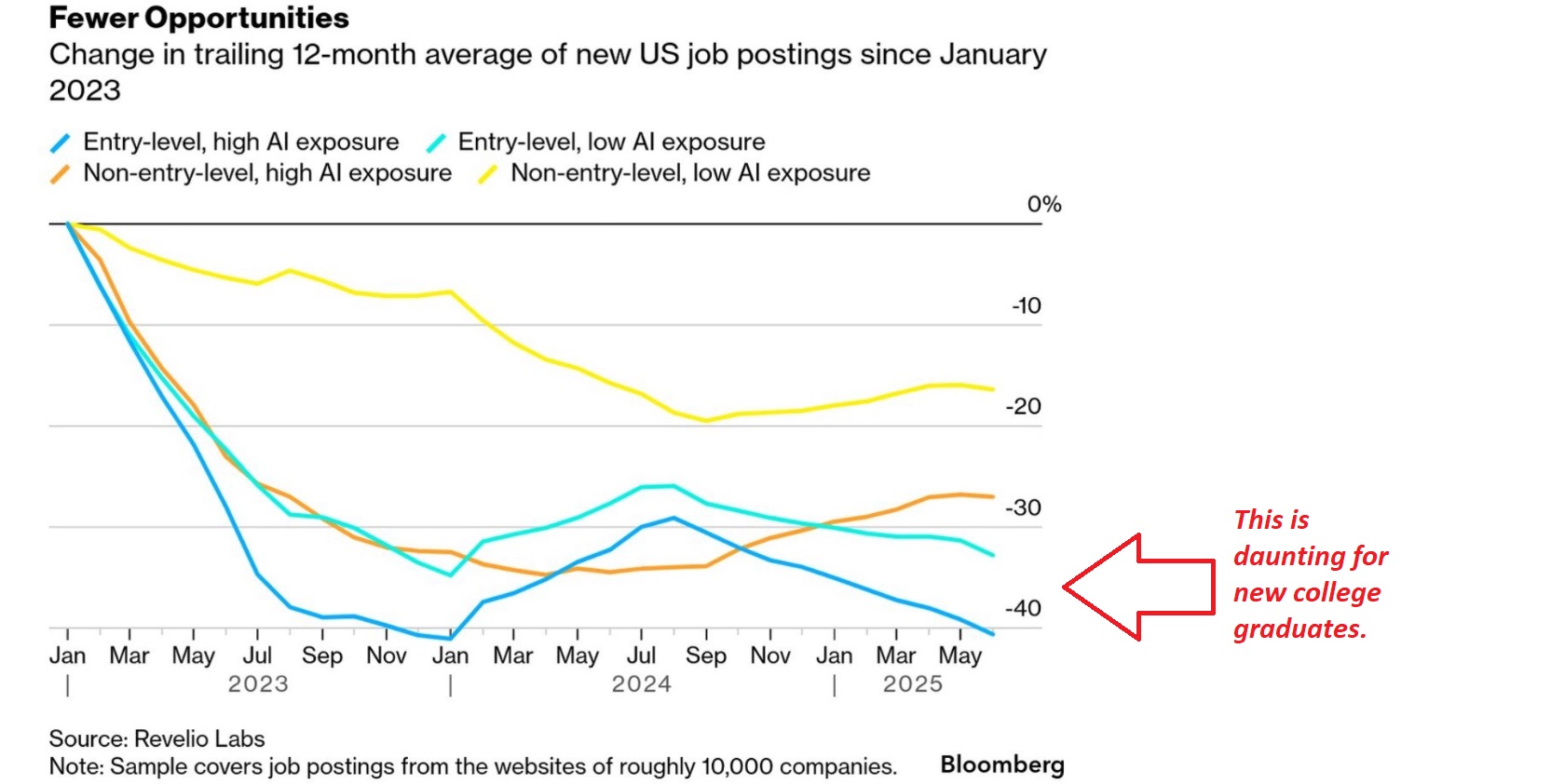

Of course, transformations often have a downside. College graduates are finding jobs — especially those within “high AI exposure” areas — harder to find:

Clearly, this is a problem. Clearly, this will not be a bloodless revolutions. There will be casualties within the labor force. It’s hard to say how this will shake out. Hopefully, there will be adequate new opportunities to offset the losses.

The bottom line: The AI infrastructure construction boom represents more than a short term boost in spending and GDP. It constitutes a fundamental transformation of America’s economic foundation. Like the railroad expansion of the 19th century or the highway system of the 20th century, I believe AI infrastructure promises to unlock economic potential on a generational scale. The numbers are compelling: In just the next few years, we can expect far more than $1 trillion in infrastructure investment. As a result, hundreds of thousands of new jobs and GDP growth effects should add trillions to the American economy. And this will build each year. As these digital mushrooms continue sprouting across the American landscape, they’re laying the foundation for what may be the most significant economic expansion in modern history.

In my mind, the question is no longer whether AI infrastructure will transform the American economy, but rather how quickly those benefits will be realized in the communities where these investments are taking root.

To the steak houses!

Interesting. High level, we see some improvement in expensive steak house reservation demand across the board. ‘Vegas saw the largest demand decline this week. Small improvements were noted in St Louis, the OC, Dallas and a host of others. Overall, the reading this week is fairly benign.

Which again is interesting, as we compare the SHI10 message here to the ‘advance’ GDP reading just out this morning. In the second quarter of 2025, our GDP grew at the annualized rate of 3.0%, reaching an annualized ‘run rate’ in dollars of $30.3 trillion.

And remember: That is the ‘real’ rate. Nominal GDP growth in Q2 was 5%. These are amazing times, folks. Sure, there are plenty of headwinds. But I think we’d better all hold on … because we’re in for a wild ride. It begins.

{kind=link}

{kind=link}