SHI 3.11.26 — A Financial Neutron Bomb?

SHI 2.25.25 – Horseshoes and Hand Grenades

February 26, 2026

SHI 3.24.26 – Unknown Unknowns

March 25, 2026

Late in the 1950s, the neutron bomb was built.

You may be unfamiliar with this type of nuclear weapon, but it’s the real deal. The “bomb eggheads” decided thermonuclear bombs were too destructive. The 1945 atomic blast in Hiroshima razed 70% of all buildings in the city. Everything within 1 mile of the blast was instantly turned to dust. Radioactive dust.

So the neutron bomb, termed an “enhanced-radiation weapon” was born. Essentially, the neutron bomb was designed to use radiation to kill all the people near the detonation without blowing up buildings. And believe it or not, the US successfully built this bomb.

It was never used in combat.

By now, you’re probably wondering why an economic/financial blog is talking about nuclear weapons. Understood. Here’s the thread.

The idea that a nuclear weapon that could “kill all the people but leave the buildings intact” reminded me of the economic devastation that peaked with the Great Recession of 2008. The sub-prime and negative-amortizing home loans, in my opinion, that were very common and widely used during the years leading up to 2008 acted much like a financial neutron bomb: Those home loans ultimately “killed all the people” but left their houses intact. Federal Reserve records say about 3.8 million homeowners lost their homes to foreclosure between 2007-2010, primarily due to subprime, ARM (adjustable rate), and negative–amortization mortgages. Over time, borrowers could no longer pay or refinance these loans. The homes they financed remained intact, but all the foreclosed homeowners were financially destroyed. This sounds like a financial neutron bomb to me.

So here’s todays question: Is “Private Credit” the latest financial neutron bomb?

“

What the heck is ‘private credit’?‘“

“

What the heck is ‘private credit’?‘“

Like that T-bone over at your favorite expensive steakhouse, private credit is getting grilled today. It’s all over the news. You’d have trouble today finding a financial publication or digital feed that isn’t trashing private credit or the companies that issue it. Of course, the detractors don’t explain precisely what private credit is.

It wasn’t that long ago that private credit was, well, private. It was obscure, very private and relatively unknown. Just as the neutron bomb really never made headlines, private credit was an obscure, not well publicized “alternative” investment vehicle. Until it wasn’t.

Today, everyone has heard of private credit. But not in a good way. No, because of all the hype and fear in the marketplace, today many believe private credit investments are downright radioactive. And as such, we are being told, they are very, very bad for your financial health.

Is this true?

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. But is the US economy expanding or contracting?

Expanding … according the ‘advanced’ reading just released by the BEA, Q4, 2025 GDP grew — in ‘current-dollar‘ terms — at the annual rate of 5.1%.

The ‘real’ growth rate — the number most often touted in the mainstream media — was 1.40%. In current dollar terms, 2025 US annual economic output reached almost $31.50 trillion.

According to the IMF, the world’s annual GDP expanded to over $115 trillion in 2024. Further, IMF expects global GDP to reach almost $135 trillion by 2028 — an increase of more than 28% in just 5 years.

America’s GDP remains around 25% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

No. It is not true. At least, not completely. In the macro, private credit is a great, systemically valuable financial tool. But like all tools, it must be used correctly and carefully. There is one aspect of private credit that I find very, very scary – it’s called PIK. This, my friends, is the financial neutron bomb hidden within private credit debt. It has the potential to “kill the investors” – speaking financially here – and leave the sponsors intact.

Of course, my reasons for these comments require that I explain precisely what private credit is, what private credit isn’t, what PIK is, and why private credit in the aggregate is on the grill in today’s financial news.

Immediately following the ‘SaaSpocalypse’ – the quickly evolving apocalyptic belief that new AI tools will replace existing software programs – the stock prices of the SaaS software companies began to plummet. These companies “rent seats” or software licenses as a business plan. For years, that business plan looked solid; but software tools unlocked by Anthropic cast doubt over the sustainability of this business plan.

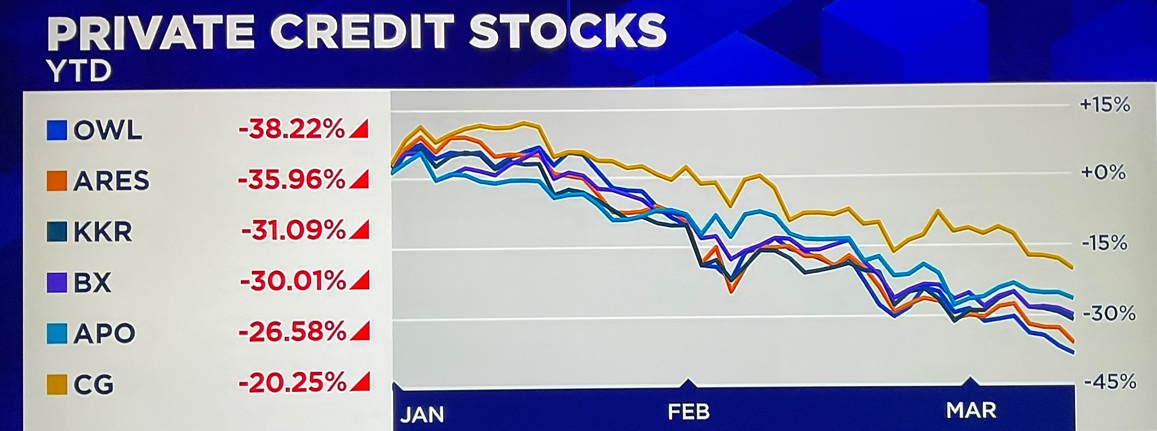

The publicly traded ‘business development companies,’ or BDC for short, soon sold off too. It turns out, many of these BDCs – essentially publicly listed and traded private credit funds – hold loans made to SaaS companies on their balance sheets. This knock-on effect continued, and soon thereafter the obscure cousins of the BDCs, the institutional private credit funds, which are not-traded, non-public, semi-liquid (really, if we’re being frank, almost fully illiquid) managed ‘private credit funds’ were maligned by the financial markets and media. The sponsors of this type of investment vehicle, names like ‘Blue Owl’ and Blackwood, were quickly tarnished as well. Their stock prices began to sell off as well, and the damage has yet to stop. Check out this image, from CNBC earlier today:

The image shows the distress in private credit. The fund sponsors listed here are all very large, very successful, “alternative investment” sponsors. And their public stock prices are getting killed. More on that later.

So, again, it turns out both exchange-listed and institutional private credit managers did lend significant amounts of capital to SaaS companies. Research suggests “software exposure” in some private credit funds is above 25% of their total loan book. This is a problem if the SaaS business plan, “renting seats” on a monthly basis for use of their software systems, has been disrupted or disintermediated by Anthropic today, and other AI systems tomorrow, right? A big problem. Because it suggests that what might have been a relatively safe, relatively conservative commercial loan before no longer is.

This is the catalyst for the current “bank run” on private credit and their sponsors. Yes, I used the term bank run – because that’s how it feels to me. Investor fear and anxiety are both amped up, and frightened investors are running for the exits. They are indiscriminately selling private credit, and related, assets as quickly as they can.

However, as I’ll discuss below, this is very different than a commercial bank run.

Today, private credit loans and managers, in the aggregate, without differentiation or distinction, are suspect. The financial talking-head experts seem to agree: The originator doesn’t matter. The borrower, irrelevant. And perhaps most disturbing: Within all funds, individual loan-level underwriting has become suspect at best and distrusted in the worst. If the software loans are bad, they seem to ask, what is the quality of rest of their portfolio? The investors and financial markets seem to have this conclusion: Private credit is BAD! Get out while you still can!

Seemingly overnight, every private credit company was suddenly radioactive. Clearly, the markets are telling us, leadership cannot be trusted. And private credit shares must be sold before the industry craters and investors lose even more money!

True?

No. It is not. The situation is far more nuanced than that.

As I mentioned above, to me, the public mania is reminiscent of a commercial bank run. Like with a bank run, there are catalyst. There is always a trigger or two. Something frightens the depositors. Some event, whether inside that bank or outside in the general economy, quickly changes depositor psyche and they want to grab their money and head to the exit as quickly as possible. The event, of course, is real. The event is usually a legitimate concern. But the fear of loss quickly spreads across a large group and mob mentality takes over. A bank run ensues. To me, today’s investor mania in the private credit markets reflects that same process.

But am I suggesting the “bank run” like fear gripping the private credit markets without merit? No, I’m not suggesting that either. Let me explain.

First, what is private credit?

Let’s start here. Financial advisors would probably describe private credit as an “alternative investment.” Meaning, in short, a private credit investment is an alternative to more traditional investments such as stocks, corporate bonds, treasury bonds, bank CDs, etc.

Until recently, I suspect most people had never heard of private credit. That’s because private credit flourished mostly in the quieter, more private segments of the financial markets. Some have referred to this area as a “shadow lending system.” This murky characterization might sound like a spy novel, but essentially private credit lenders do, in some respects, operate in the “shadows” of bank regulation.

Private credit owes its genesis to strict new traditional bank regulations implemented after the Great Recession of 2008. In a nutshell, bank regulators made it much more expensive for banks to hold riskier loans. Risky loans were no longer commercially profitable. So they stopped making most of them. Into that opportunistic void stepped companies like Blackstone, Apollo and Blue Owl as these companies were not commercial banks, and as a result, were not subject to the same regulations.

Unlike public corporate bond debt or a commercial bank’s balance sheet, private credit loans are private. There is no requirement that a private credit lender disclose loan-level detail. So calling this segment of the market a “shadow” banking segment rings true. Over time, this inherent opacity makes it hard for investors, the public, the FED, or the financial system at large to truly know how much systemic risk has built up.

In the years following 2008, private credit companies quickly stepped into the vacuum and grew by making commercial loans deemed risky by very strict post-financial crisis regulations. This lending niche was quite profitable because the private credit lenders could charge meaningfully higher interest rates since the commercial banks were unable to profitably compete. They attracted more investors by paying outsized returns. In turn, they grew larger and became a sizable alternative investment vehicle for investors seeking larger returns.

The investor’s tradeoff, however, was this: Early on, their investment in an institutional private credit fund was illiquid. Once invested, their capital was locked up. Over time, the funds became a bit more flexible and typically up to 5% of the fund’s total capital could be returned to requesting investors on a quarterly basis. But this feature notwithstanding, Institutional private credit investments remain highly illiquid.

The 2008 “bank retreat” truly opened the door for private credit. But the public financial markets solved the liquidity problem. By 2010, the appetite for this product exploded. About half of the public BDCs were formed between 2010 and 2014. They offered investors higher returns and daily liquidity. The aggregate market capitalization for all the BDCs is about $66 billion. The 44 largest and most liquid publicly traded BDCs in the US trade in the S&P BDC Index. Keep in mind, however, that these 44 companies are not all the same. The good news for you is that an AI chatbot can help you look under the hood.

These business development companies focus on lending to “middle-market” companies. In this instance, middle-market refers to a smaller company with an enterprise value of, say, $100 to $750 million and revenues from $10 million to $1 billion. These business might be very profitable, but they are deemed riskier due to their smaller size. Most of these companies do not have access to the public corporate bond market which usually requires a deal minimum of $500 million. Interestingly, there are about 200,000 middle market companies in the US; while they represent only about 1% of all businesses out there, they account for about one third of private US GDP and employ about 50 million people.

These public BDCs, however, are dwarfed by the big guys, like Blackrock.

At present, Blackrock’s “assets under management” – known as AUM – now exceed $14 trillion. Blackrock is a well-known “alternative investment asset” company. And Blackrock is publicly traded under the symbol BLK. BLK has many different types of assets under management. One is ‘Blackrock TCP Capital Corp’ which also trades in the public markets, under the ticker TCPC. You can buy or sell both BLK and TCPC every second of every day that the exchanges are open for business.

Another Blackrock company is a private credit company named “HPS.” As of March of this year, HPS has about $185 billion in assets. However, HPS is not publicly available. Their investment fund – called HLEND – is an investment grade non-traded private credit fund specifically designed for wealthy investors meeting mandatory suitability requirements. The only way an investor can buy into HLEND is thru a wealth managing institution like Morgan Stanley or JP Morgan.

Why? There are numerous reasons. But one is the fact that investor money is locked up. Illiquid. It’s hard to get into these non-traded, illiquid funds because it’s hard to get out. In theory, the fact that they are illiquid actually boosts long-term investment returns. But the tradeoff – and it’s a very real tradeoff – is the illiquidity. The fact that private credit funds are “locked up” is intentional – this is actually the primary feature of this type of investment. Because all the investors know their money is locked up, the sponsor can make long-term investments without fear that many or all its investors demand their money back in the short term. Essentially, this “model” is the diametric opposite of a bank: Banks make mid- and long-term loans using funds on deposit that can be withdrawn at any time. In past years, this feature has triggered a “run on the bank” sometimes ending in bank failure. Private credit funds, by design, don’t have this problem. There cannot be a run-on-the-bank because investors know they cannot demand their money back, except in precise, controlled conditions.

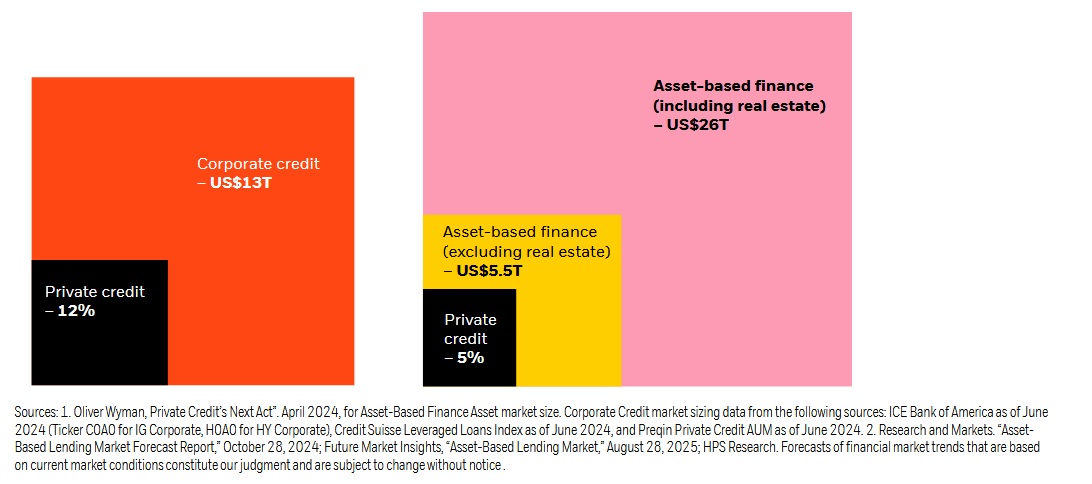

The private credit marketplace, in totality, sums to be about $2 trillion today. Here’s a great image from a Blackrock report called “2026 Private Markets Outlook.”

So let’s do a quick review. I know this might feel cumbersome and intertwined. Blackrock is an alternative asset company. They manage a ton of capital. BLK is a public stock. BLK also manages TCPC, a public-stock company in the private credit space, and, they manage HPS, an illiquid, private investment fund for accredited investors. Private credit is simply one segment of the total corporate credit market, measuring 12% of total corporate lending. And it’s about 5% of total asset-based lending.

Second, what precisely is wrong with private credit? Why is it so widely hated today? And finally, what is “right” with it?

Inevitably, a few private credit loans have gone bad. I say “inevitably” because some loan losses are a fact of life. All banks set money aside, called “loan loss reserves” for this reason. For example, late last year, a “used car retailer” company named Tricolor Holdings went bankrupt. The private credit industry was first blamed for their default; however, it soon became apparent that Tricolor was immersed in a massive systemic, multi-year fraud. This became clear over time, but private credit still got a black eye. Because opacity is one problem with private credit. Investors have limited visibility into the loans on the private credit balance sheet.

The AI chatbots can help here. If you plan to invest in this space, use them. Frankly, they offer much more visibility than you might think. For example, using Gemini+ I learned that Blue Owl was not the only lender impacted by the Tricolor Holdings failure. It turns out the mainstream commercial banks like JP Morgan, Fifth Third and Barclays banks all lost hundreds of millions in that deal.

When a loan or two within a private credit portfolio go bad, for any reason, fear grows that many more loans in the portfolio might be bad. The opacity inherent in private credit lending makes it an easy target for anxiety and fear.

Then, of course, the SaaSpocalypse struck. I’m sure you’ve followed this episode and its very negative impact on the public stock prices of the large SaaS companies. As private credit lenders have significant exposure to SaaS companies, they were quickly impacted. A crisis grew seemingly overnight. Many investors raced for the exits, dumping stocks like BLK and other large alternative asset managers and the publicly-traded private credit companies. Stock prices plummeted in response.

Now, let’s talk about the BIGGEST problem of all. Use your AI chatbot and ask this question about any of the 44 public companies in the BDC index or any of the institutional private credit names:

“Does ______ (fund name) use PIK?”

Put the name of the company or fund in the blank.

Yes, we’re looking for PIK. PIK is an acronym for “Payment-in-Kind.” In my opinion, my friends, this is the neutron bomb hiding in the loan portfolio. What is PIK?

PIK, in a nutshell, is interest accrual. When a private credit loan has a ‘Payment-in-Kind’ provision, some portion of the interest due on the loan accrues to the loan balance because, by agreement, some portion of the interest due the lender was permitted to accrue. A PIK agreement in the loan documents permits the lender to “book” a larger interest payment without actually receiving the cash from the borrower. In this instance, booked income looks higher and, at the same time, the borrower’s loan principal grows larger. In this way, a private credit loan can be much like the negative-amortizing mortgage loans that were common before the 2008 financial crisis.

The proliferation of PIK provisions in private credit loans, in my opinion, is THE problem. Let’s take this idea to the absurd for a moment: Suppose a private credit company made loans to borrowers willing to pay a 25% interest rate. But by agreement, all that interest simply accrued to the loan balance. The borrower could postpone the payment of interest almost indefinitely, while, at the same time the BDC could look extremely healthy on paper. Of course, in this instance, the opposite is true.

This hypothetical is not the reality. In reality, public BDCs receive about 8% to 9% of their investment income via PIK today. However, that percentage is about double the size it was pre-pandemic. It’s easier to “sell” a PIK provision to a borrow than demand all interest be paid when due. Especially when the BDC wants to realize a high income at a time when interest rates are declining and competition amongst BDCs is growing.

The growing use of PIK in private credit loan instruments is concerning to me. We don’t need another financial crisis triggered by “negative-amortizing” private credit loans. PIK provisions, if used excessively, are a financial neutron bomb. At excessive levels, they will kill all the people (investors) while leaving the buildings (investment banks) standing.

Hopefully, this latest “bank run” within the private credit space will help keep the use of this troubling feature under control. Fingers crossed. However, if you choose to invest here, be sure to clearly understand how much PIK your BDC is using.

So after those admonishments, what’s going right here?

It’s worth noting that the phrase “bank run” as used here is more of an emotional nod than a financial reality. The simple fact is that the money lent within private credit funds — whether public BDCs or private institutional funds — is lent for 5-10 years of more. Unlike demand deposits at a commercial bank, investors cannot demand for the return of their capital within private credit vehicles. So, in this specific respect, private credit companies might be safer than commercial banks. Private credit has other potential problems, but this is not one of them.

Finally, a well structured and well-operated BDC does pay a sizable return. The investment return can be significantly higher than the ROI from corporate or municipal bond markets. Of course, those investments are typically considered “safe.” As with all things involving “risk” and “return” the two are definitely highly correlated. Be warned. 🙂

Finally, is private credit going away?

Nope.

Like the mythical phoenix, the private credit loan rose from the ashes of the 2008 financial crisis. Before 2008, if a “middle market” company wanted to secure debt for a leveraged buyout, a big bank like Goldman or Citi would write the check, keep a small piece of the debt, and sell the rest. After the 2008 crash, federal banking regulation made that transaction impossible.

Until and unless commercial bank regulation changes, the private credit will continue to gain traction. They fill an important void in the marketplace. In fact, industry experts expect it will more than double in size, growing from its current approximately $2 trillion in size to as much as $4.5 trillion by 2030.

Private credit, whether in the form of the publicly traded BDCs or the large private, institutional funds, is probably with us for the long haul. I do expect the current maelstrom will usher in systemic improvements. Fingers crossed. But if you plan to wade into this pool, be sure to first do your homework.

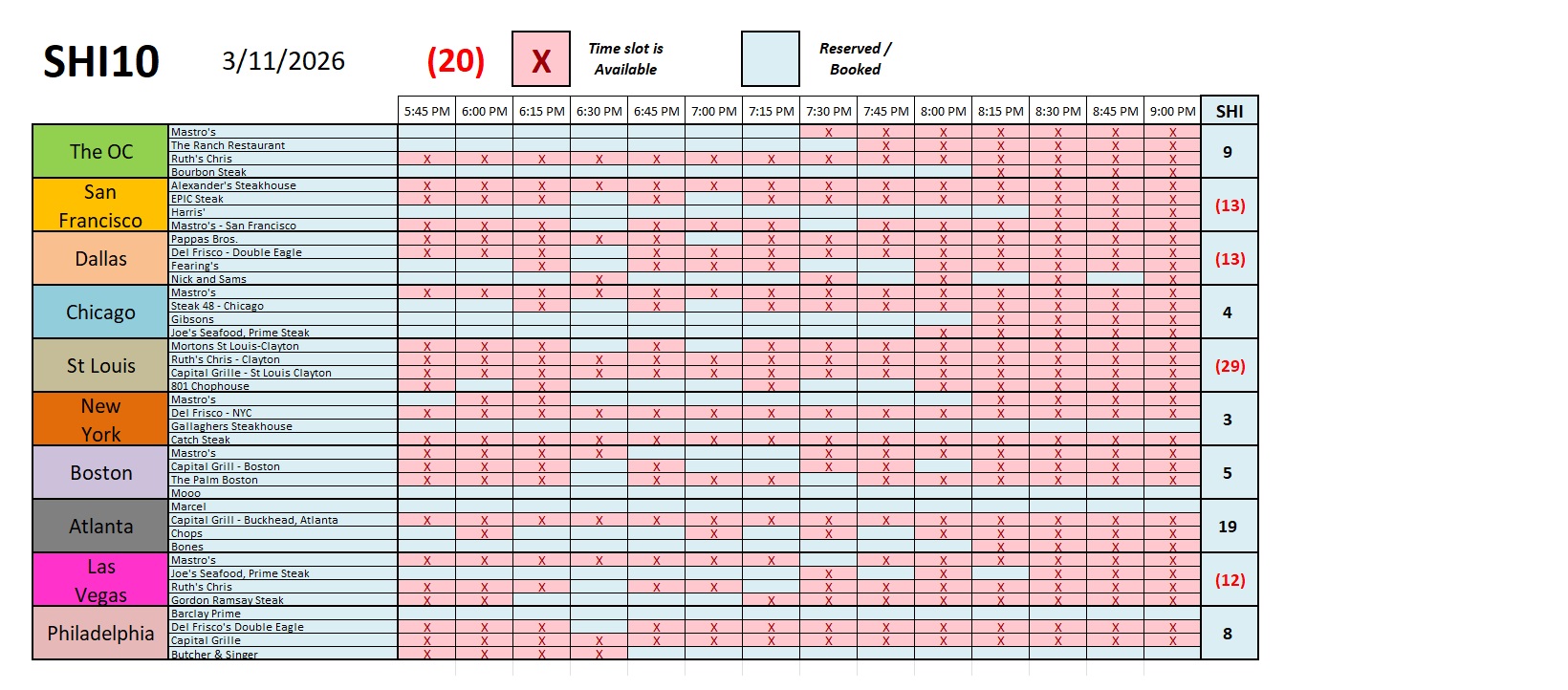

Let’s check in on the steakhouses.

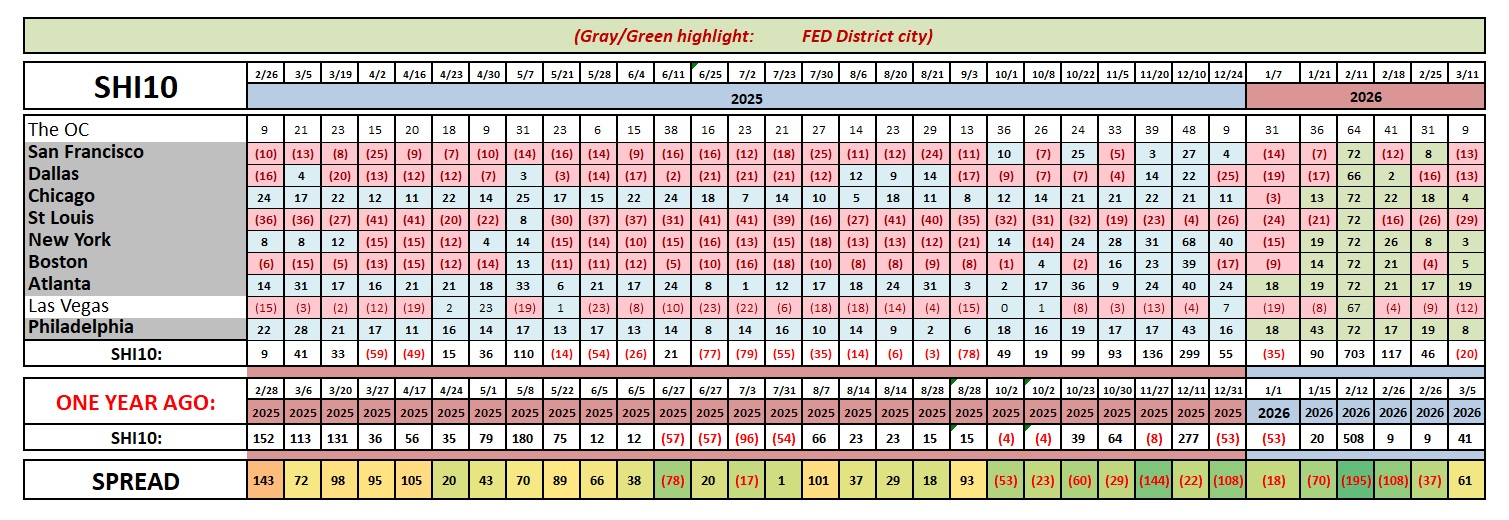

I hate to sound like a broken record, but there’s not much new going on here. This week the SHI10 is a little softer — quite a bit softer here in the OC. But overall, across the country, reservation demand remains consistent and fairly strong. Here’s the longer term trend chart:

I hope you enjoyed this weeks deep-dive into the world of private credit. I wrote this blog because I felt my personal understanding of private credit was deficient. Every day for months I been hearing financial “experts” talking trash about the sector and watch the stocks of the big sponsors continue to tank. I found it difficult to believe all the negative comments. So I did this deep-dive to educate myself. Writing this blog helped me crystalize and articulate my thoughts. And, trust me, those AI chatbots are fabulous research tools. I hope you find the same.

But I still wrote this blog. There’s no way a machine can replace me! 🙂