4.8.26 — Another Look at Private Credit

SHI 4.1.26 – A Season For Mischief

April 1, 2026

SHI 5/13/2026 – AI or Die

May 13, 2026

I have been asked: Will “private credit” trigger a systemic financial crisis?

One reader went as far to ask if I believed the current slow-rolling private credit crush could take down the entire financial system, somewhat a-la-2008?

“

Will the “private credit crisis”

bring down the US financial system? “

“

Will the “private credit crisis”

bring down the US financial system? “

I answered “no, it will not.” But thinking further on my reply, I later decided this question was worth a more thoughtful answer. Here we go.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. But is the US economy expanding or contracting?

Expanding … according the ‘advanced’ reading just released by the BEA, Q4, 2025 GDP grew — in ‘current-dollar‘ terms — at the annual rate of 5.1%.

The ‘real’ growth rate — the number most often touted in the mainstream media — was 1.40%. In current dollar terms, 2025 US annual economic output reached almost $31.50 trillion.

According to the IMF, the world’s annual GDP expanded to over $115 trillion in 2024. Further, IMF expects global GDP to reach almost $135 trillion by 2028 — an increase of more than 28% in just 5 years.

America’s GDP remains around 25% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

First a quick review. What is private credit?

As I wrote in my blog on March 11th titled,

SHI 3.11.26 — A Financial Neutron Bomb?

… private credit is simply non-bank lending to primarily “middle-market” companies. “Non-bank lending” means the lender was not a commercial bank. In the blog post above, I discussed in detail why the loan was not made by a bank. Re-read it for more details.

Who are the borrowers? As I said in that blog:

These business development companies focus on lending to “middle-market” companies. In this instance, middle-market refers to a smaller company with an enterprise value of, say, $100 to $750 million and revenues from $10 million to $1 billion. These business might be very profitable, but they are deemed riskier due to their smaller size. Most of these companies do not have access to the public corporate bond market which usually requires a deal minimum of $500 million. Interestingly, there are about 200,000 middle market companies in the US; while they represent only about 1% of all businesses out there, they account for about one third of private US GDP and employ about 50 million people.

One third of GDP? That’s a very meaningful slice of the US economy. Ironically, after the Great Recession of 2008, many of these companies essentially became “un-banked” due to new federal (and international) banking regulations resulting from the 2008 financial collapse that almost ended the global financial system. And by un-banked, I mean banks would no longer lend to them.

Sort of. That statement employs some degree of hyperbole. Because at a conservative-enough level, banks will lend to just about anyone. Whether measured by “interest coverage ratio” or some multiple of EBITDA, post-2008 all commercial banks were essentially prohibited from making loans deemed risky by regulators. Which meant that the “risky” borrower’s loan request was often “too large” for a commercial bank to make either due to regulatory limits or profitability limitations.

Into this void moved the private credit sponsors. The private credit boom began. Growth accelerate quickly and today we’re up to almost $2 trillion in total private credit lending. I know this is somewhat vague, but let me leave it there for the moment.

The term “non-bank” is equally vague, right? After all, the term only means the lender is not a bank. So who are the lenders in the private credit space? Well, in some cases, as we know from all the headlines, the lender is a publicly traded “business development company” known as a BDC. Sometimes, that lender was a private BDC with names like Blackrock, Blackstone, and Blue Owl coming to mind.

But there are many other private credit lenders. For example, estimates suggest about 30% of private credit loans were made, and are owned by, pension funds. Both public and private. And this makes sense, right? Matching a long-term lender with a long-duration borrower is a good thing. Pension fund investments into private credit typically have no right of redemption.

Then we have the life insurance companies. Estimates suggest about 25% of private credit loans were made, and are owned by, the LICs. Again, they are a perfect lender for this type of product. They work hard to find long-term, higher-yield investments. Not only are LICs not looking for an exit from their private credit ownership, they continue to commit more capital to PC even today.

Coming in third are the global Sovereign Wealth Funds, at about 15% of all private credit lending.

So adding those three (3) sources up, you see that about 70% — or more than 2/3 of all private credit loans — are in the hands of pension funds, LICs and SWFs!

Another bunch — more than 10% — are estimated to be held by ‘family offices’ and high-net worth individuals.

My point? There is no monolithic private credit lender. These loans are disbursed far and wide to very large, very sophisticated investors.

But this fact alone won’t prevent a financial “black eye” as the crisis continues to unfold. I worry there are some shenanigans taking place within the LIC space — quite a few are now owned by private equity companies and many have been moved “off-shore.” Many of those PE owned LICs made private credit loans which are probably riskier than Look this up for more detail — I could go on for hours about this alone. The financial markets fear contagion as various systemically important players, like the life insurance companies, come under additional scrutiny. Reports suggest that about 10% – 20% of private credit loans are “distressed” or “subordinate” — making them far more risky than mainstream private credit loans. In theory, these loans were priced appropriately at these elevated levels of risk. But we don’t really know, since the industry is “private” and light on disclosure.

So, yes, there is cause for concern.

But beyond the wealthy, long-term profile of most PC lenders, I take comfort from the fact that the marketplace is really quite small. Yes, small. Consider this: 20 years ago — in 2006 — about 30% of all home mortgages were “subprime” and “Alt-A” loans. These were your problem loans. Further, many of these loans (and related assets) were owned by commercial banks with leverage ratios of 30 to 1. If — and as we all know, when — a loan goes bad, 30:1 leverage magnifies the problem 30X.

Compare this to the private credit market. Sure, $2 trillion sounds like a lot, but it represents only about 2.50% of the global financial system. It’s a small slice of a VERY big market. But more importantly leverage ratios within the private credit market are close to zero. To be clear, not zero but close. Private funds do us leverage of about 1 to 1. Meaning that for every dollar lent, they may borrow one more dollar. Generally, LICs and SWFs use no leverage in their investments.

They typically use only capital on hand. No leverage at all.

This set up is vastly different than the 2008 negative feedback loop. At 30:1 leverage, a 3 or 3.5% asset value decline could wipe out the entire equity of a bank. At 1:1 leverage, the same value decline adversely impacts the investor’s return, but the investment principal remains intact.

The bottom line: The private credit market has issues. They deserve some bad press. However, as most of these lenders essential “use their own cash” and leverage is close to zero, if a loan goes bad, some capital is lost. The stress and anxiety are real. But the existential fear the media is selling is not. A few, or even quite a few loans will go bad. They always do in all credit cycles. But bad loans within the PC space will not trigger margin calls that put the financial system at risk. No, the problem here is that even thought the loans are performing and borrowers are paying, the investors are looking to exit anyway.

It’s worth noting that earlier today, Moody’s — a credit rating agency — downgraded the credit rating of Blue Owl Capital’s “flagship fund” known as “Blue Owl Credit Income Corp” or OCIC, a fund that is not publicly traded. It is known as a “perpetual, non-traded Business Development Company.” The total portfolio size is $36 billion, holds loans in about 350 different companies in more than 30 different industries.

Ironically, Moody’s would agree that the credit quality of the portfolio is exceptionally good. Their default — or non-accrual — has historically hovered around 0.2%. Their historic loss rate is about 0.14% annualized. So why the downgrade? Liquidity concerns. In Q1 of 2026, they were hit with redemption requests totaling almost 22% of the fund. The 5% gate kept a lot of folks in the fund who, at that moment, wanted to leave. You may find this set of facts confusing. I understand. But there you are.

Fear is driving behavior. It’s not rational … but “bank run” mentality never is. In the final analysis, I believe this will blow over. Fingers crossed. 🙂

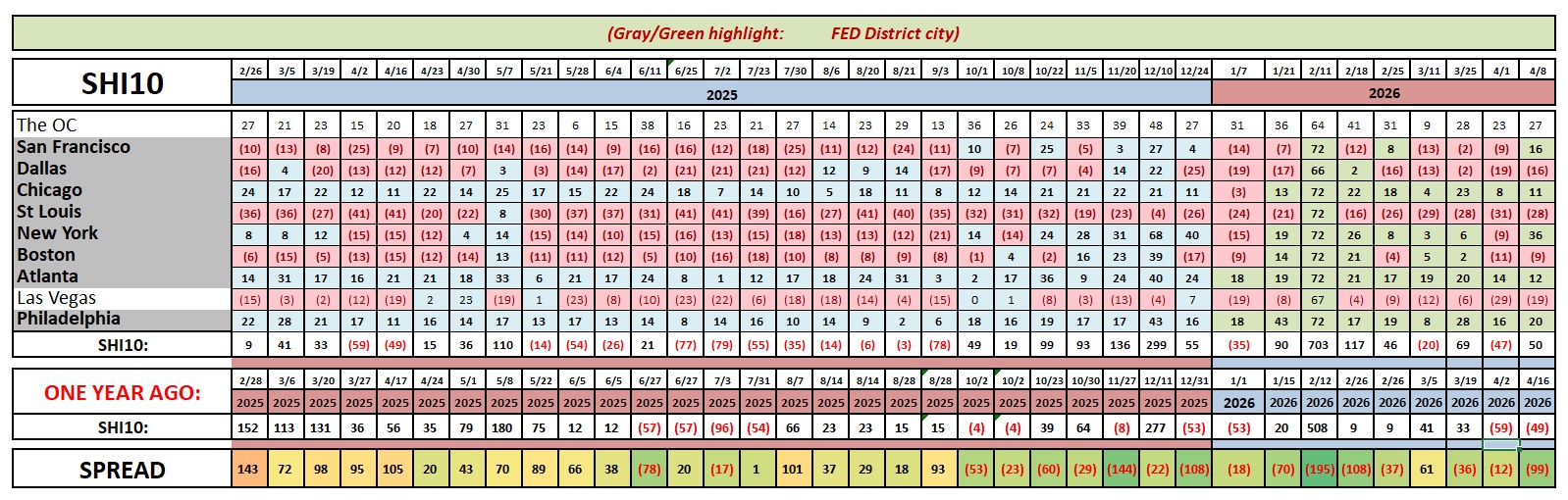

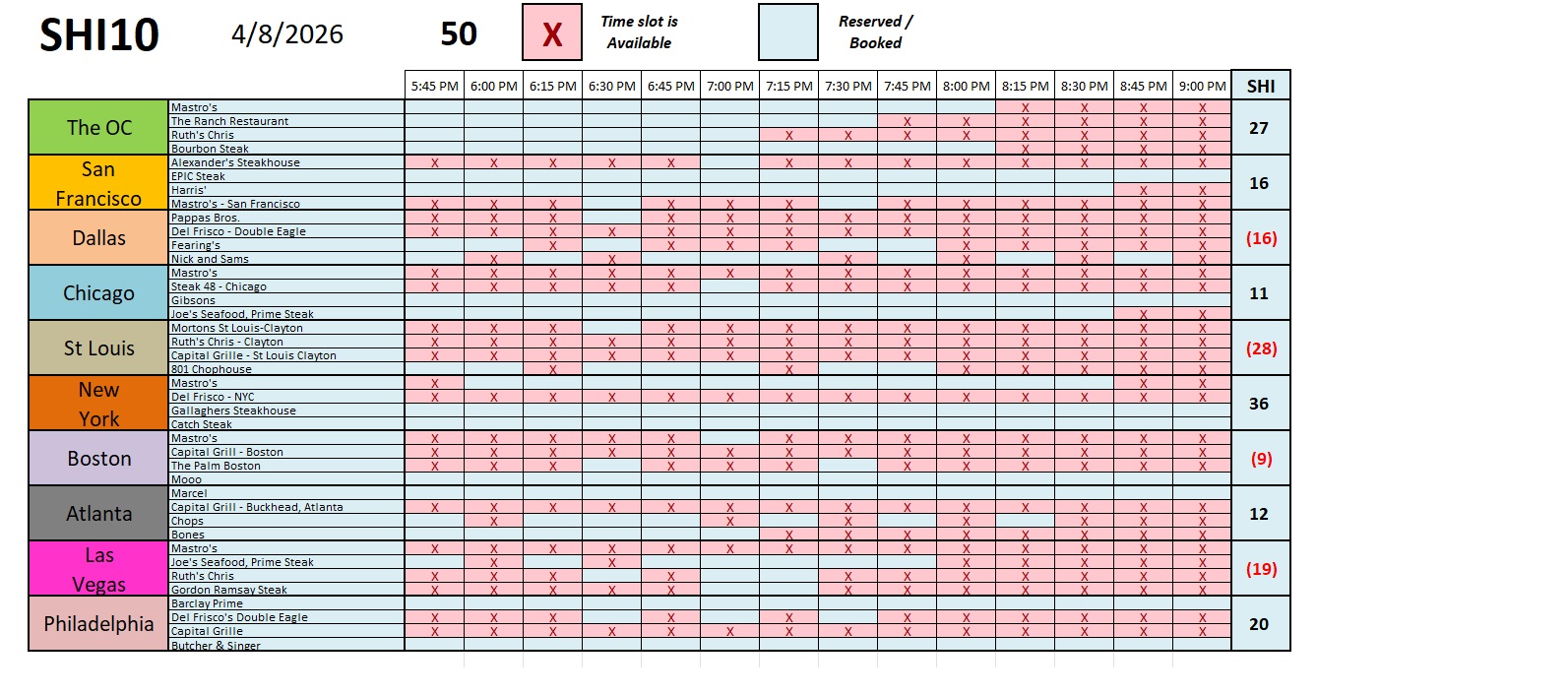

To the steakhouses?

Well, well, well, it looks like the demand for red meat picked up a bit this week. The SHI10, as you can see below, popped up to a positive 50. Frankly, that’s a pretty good showing given all the turbulence in the global financial markets.

That turbulence is showing up in Q1 GDP forecasts. The Atlanta FED ‘GDPnow’ forecast has tumbled down to 1.3%. This is a long way from earlier 3%+ forecasts. Why the drop? Reading the report more closely, a few of the subcomponents are flashing weakness. First, “net exports” is down markedly. This is probably related to a “front-running” import surge due to the Iran conflict. But even more concerning, consumer spending is looking tepid at best. Hmmm … this is not good if it becomes a longer term trend. We’ll keep our eye on it.

Here’s the long-term chart.