SHI 1.7.26 — A World of Data

January 7, 2026SHI 02.04.26 – A Shifting Tide

February 3, 2026

“Take the hit.”

Essentially, this was the author’s message. At least, that’s how I took it. But more on that thought in the blog below.

We all know affordability is stretched thin today. Americans are struggling to make ends meet. Food and housing costs top the list. Everyone is talking about it – well, more precisely, those who frame it ‘academically’ are talking about it. People experiencing the challenge more viscerally, more personally, are doing more than talking. They are taking action, commenting in media, expressing anger in surveys, and filling the airwaves. And they are making their opinions known at voting booths. New York city’s mayor was just elected by voters looking for living solutions in the city. This topic is clearly the next political buzzword or galvanizing rallying-cry nationwide.

For good reason. It is a serious problem today, across the entire spectrum of consumer goods, but nowhere, perhaps, more notably than in the housing market.

“

Housing is unaffordable.”

For many Americans, this is nothing new — its just worse. Unlike rural Japan where homes are a dime a dozen, the opposite remains true here. Whether the desire is to rent or own, households are struggling under the cost. This is not a strictly American issue today. Consumers across the developed world face very similar issues. In fact, this problem is far worse in many other developed nations. But I’ll save that discussion for another day.

Today, once again, we will discuss American housing affordable. And more specifically, a “proposed” solution kicked around in a Wall Street Journal article I will share below. A solution, frankly, that I put in the “stupid” column. Yes, sorry, today I will be ranting a bit. I apologize in advance. 🙂

Welcome to this week’s Steak House Index update.

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding.

The ‘real’ growth rate — the number most often touted in the mainstream media — was 4.3% in the last quarter. That is a HUGE growth rate. In “current dollar” terms, US annual economic output rose to $31.095 trillion.

According to the World Bank, the world’s annual GDP expanded to over $111 trillion in 2024. Further, IMF expects global GDP to reach almost $132 trillion by 2030. The US? Various forecasts project about $37 trillion for American GDP in 2030 — I believe it could be even higher.

America’s GDP remains around 28% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

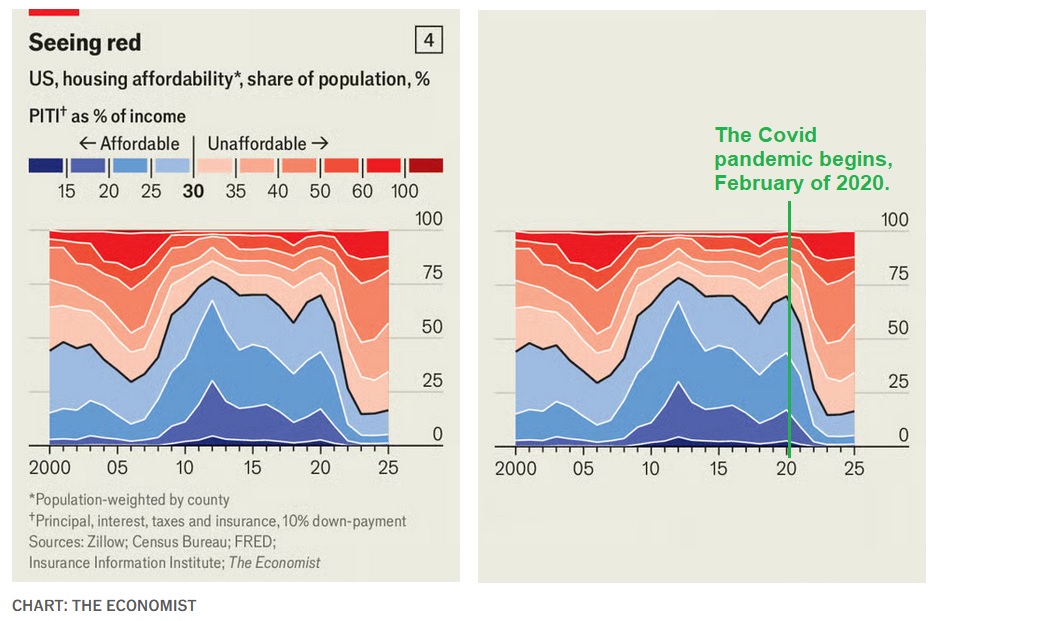

According to The Economist magazine, home affordability in America has never been worse:

The image on the left was provided by The Economist magazine. I modified the one on the right to identify the beginning date of the pandemic. Yes, your eyes do not deceive you: housing affordability plummeted soon after the pandemic began. No, its not because interest rates shot up – that didn’t begin for 2 more years, March of 2022. Clearly, when rates jump, mortgage payments do the same.

No, the opposite is true. After the pandemic hit, the FED dropped short term rates to about zero. Home loan rates fell shortly thereafter, reducing monthly payments. But this action triggered a buying frenzy. And because the pandemic also triggered the “remote work” movement, that buying frenzy wasn’t just in the big cities with large populations. No, the frenzy was nationwide. Simultaneously, the “for-sale” inventory collapsed as people everywhere were “sheltering at home” as instructed by health authorities. Sellers cancelled listings — people just stayed home. By later in 2020, existing home inventories fell by 24%.

These events, in concert, triggered the perfect storm for housing affordability. Low, low mortgage rates, tight and falling supply, with work-from-home now the latest thing, Covid really torched housing affordability. It plummeted as the chart shows. And it remains there today.

Affordability wasn’t good before; it was just better. As my long-time readers know, I’ve been complaining about the lack of new home supply for years – perhaps almost 2 decades! The housing affordability problem was here long before Covid. Covid simply dumped jet fuel on the fire.

So here we are. Fast forward to today, January of 2026, and the problem is not only much worse, but much more in focus. Everyone has an opinion; everyone is in the debate. Even President Trump has promised to “restore the American Dream of homeownership.” He’s even talking about declaring a “national housing emergency” – whatever that means. Regardless, this topic is definitely top of mind.

So what is the solution?

Well, like all complex problems, there are many moving parts and many obstacles to overcome. But the most “entertaining” solution I’ve come across lately is this one:

Young Americans need home prices to fall in order to make housing affordable.

Therefore, existing homeowners need to take the hit.

That’s right: Equity-rich homeowners, need to take one on the chin, bear the burden, eat the loss — you know: take the hit. So that younger folks can step in and realize their American Dream of home ownership.

Yep, that’s the pitch. You heard right. No — this isn’t MY idea. I’ve expressed stupid ideas before, but this one isn’t mine.

I’m pulling this one directly from the media. I’ve seen a number of articles suggesting precisely that. And here’s the latest, from the January 20th Wall Street Journal. Click here to read it (right click, open in new tab.)

The author’s message is right in the title: “To Make Homes Affordable Again, Someone Has To Lose Out.” The sub-text is: Young Americans need home prices to fall. Existing owners don’t want to take a hit.”

What? Existing homeowners don’t want to take a hit? Of course they don’t want to take a hit. Why would anyone want to take the hit? The suggestion — if that’s what it really is — that a homeowner with years of money, payments, and blood-sweat-and-tears invested in their home should sell their home at a loss is patently absurd. I define “at a loss” here as a price below current market value.

Is this really our best, bad idea? The best we can do is tell the American homeowner, all 83 million of them, that when they next sell their home they must sell it at a 10%, 20% or more discount to current market? Take the hit, homeowner, so the next buyer can afford to buy your home? That’s the best we have?

Well, it’s a stupid idea. If for-sale inventory fell to historic lows during Covid, this “proposal” or even worse, this (suggested? proposed?) regulation, would flash-freeze the market. I am confident every active listing would immediately cancel. No one would sell their house ever. Why would they? Instead of expanding the opportunity for home ownership for the next generation, this would slam the door closed.

Then, as an alternative, perhaps regulators can pass a law stating no one can own their home for more than 5 years before selling? Of course at a discount. The sale price would be mandated to be lower — the homeowner must take the hit. How about that solution? Yes, the legislators in Sacramento or Washington DC could pass a law that essentially declares “private property” is no longer private. That would solve the problem, right?

Oh, no, it wouldn’t. Because under these conditions, new homebuyers would vanish. Who in their right mind would buy a house knowing (1) they will not realize any value appreciation – in fact, they may have to sell at a discount, and, (2) they can only own their home for 5 years.

I don’t know the author, Carol Ryan. Her ‘bio’ in the WSJ states: “Carol Ryan is a Heard on the Street columnist based in London, where she covers European energy companies, property and the luxury-goods industry. She joined the Journal from Reuters Breakingviews, where she covered consumer-staples companies.”

It sounds like she covers business and economic issues. But, wow, her suggestion here is downright dumb.

Why stop with houses? Let’s make stocks and bonds cheaper again! And what about women’s purses! I mean, Chanel purse prices are ridiculous!

OK, ok, I made my point. Sorry Carol, but I’m afraid I disagree with your suggestion – and if suggestion is too strong, your implication – that existing homeowners must lose for new homeowners to win. Because, I am convinced, if one loses, both lose. The answer to this conundrum is finding a way for both to win. Existing homeowners cannot be forced to lose equity in any regulatory solution. That’s will not work.

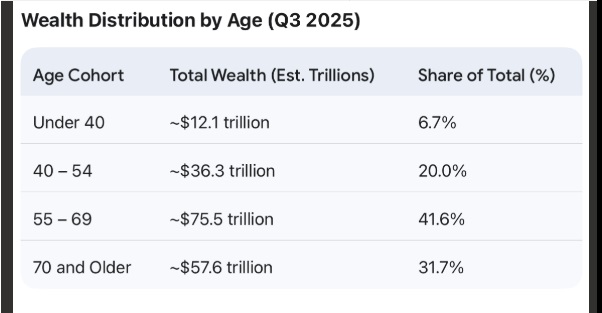

According to the latest FED z.1 report, the net worth of all American households, in the aggregate, is now more than $181 trillion. This is almost $100 trillion more than the collective number just 10 years ago. Almost $35 trillion of that is home equity. About $66 trillion is corporate equities. These are big numbers. America is rich. The problem, of course is not the aggregate net worth of all Americans. It’s how those assets spread across various age cohorts. Here is how that $181 trillion American “net worth” breaks down across age cohorts:

That’s the problem. First time home buyers — folks under 40 — only own 6.7% of American wealth. Perhaps there’s only one solution to that problem: The Great Wealth Transfer.

A private research and consulting firm, Cerulli Associates, believes a staggering sum — $124 trillion — will change hands by 2048. Much of that sum, $52 trillion, they expect, will “transfer” to “heirs” — meaning children. Of course, these are mostly children of rich people, but that’s a lot of wealth transfer. Gen X is the most immediate beneficiary over the next decade; Millennials are expected to be the largest beneficiaries over the longer term. This group is between 30 and 45 in 2026.

Is this the solution to the housing affordable problem? Probably not. But it’s better than what’s-her-name’s idea. 🙂

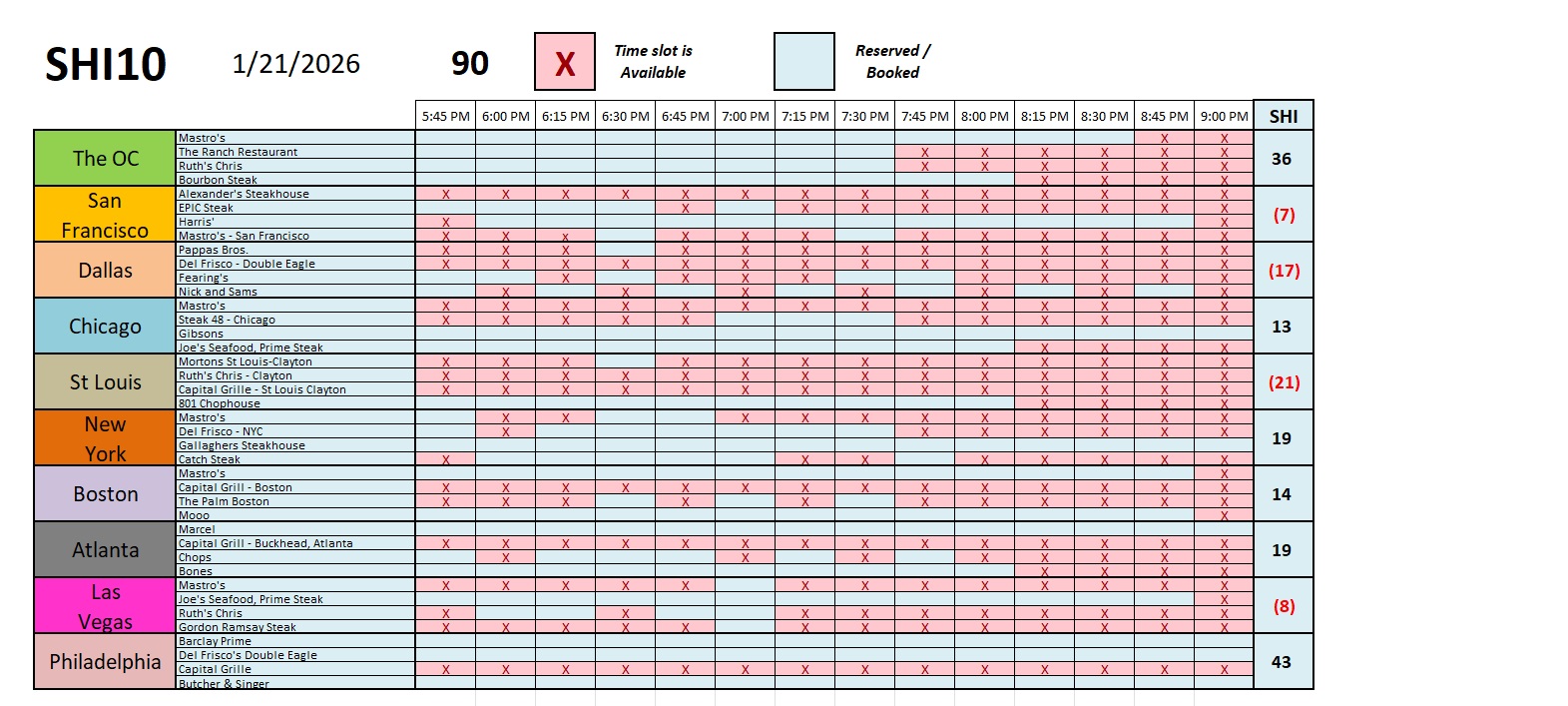

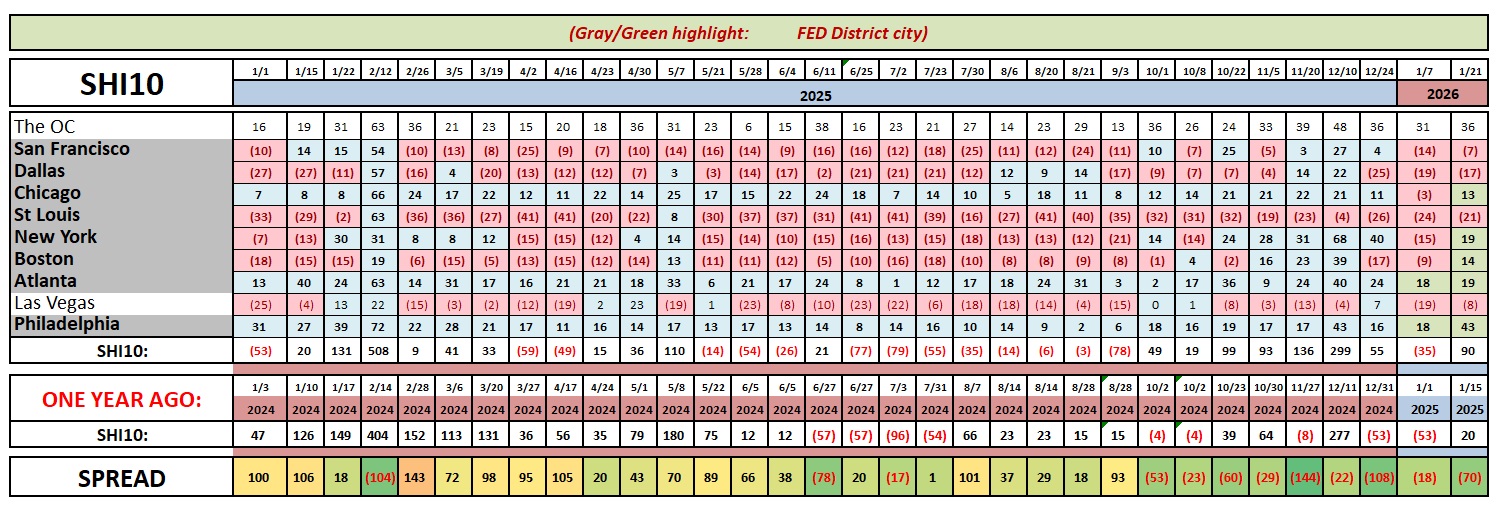

The SHI is looking solid today. Reservation demand for Saturday looks strong. Here’s the long term chart:

Literally, every single market improved this week. And the SHI40 increased from a negative <40> last week to a positive 90 this week. Our expensive eateries remain in strong demand. This suggests the US economy is cooking. So does the most recent Atlanta FED ‘GDPnow’ estimate: 5.4%. That’s right, the Atlanta FED now expects Q4 2025 GDP growth at an (annualized) rate of 5.4%. That is smoking hot!

Back to the housing affordability issue for a moment. It looks to me like President Trump is backing me up. Speaking today in Davos, President Trump reiterated that he wants to protect American homeowner equity. He said he is “very protective of people that already own a house.” Good. Someone should probably tell Carol.

<Terry Liebman>

{kind=link}