SHI 1.22.20 – When a House is a Bad Investment

SHI 1/15/2020 – The Roaring 20s Are Here Again. Not.

January 15, 2020

SHI 2/5/2020 – Sorry About That!

February 5, 2020

“When demand plummets, home values follow.”

Supply and demand are the most foundational of economic metrics, perpetually locked in a delicate ballet. If either changes meaningfully, value is impacted. Sometimes significantly … and sometimes irrevocably.

Homes all over the world have lost value at one time or another. Across the centuries, cyclical factors and economic conditions have impacted home values in every market at one time or another. Yet, in most cases, after a widespread value decline the market recovered and values rose again, often to a new and higher peak.

But not in Japan. And not in Greenwich, Connecticut. Homes in both locations have lost significant value, even as values in most other markets have increased significantly. But while the outcome is the same, the causes are very different. Both causes are quite interesting … and worth a discussion.

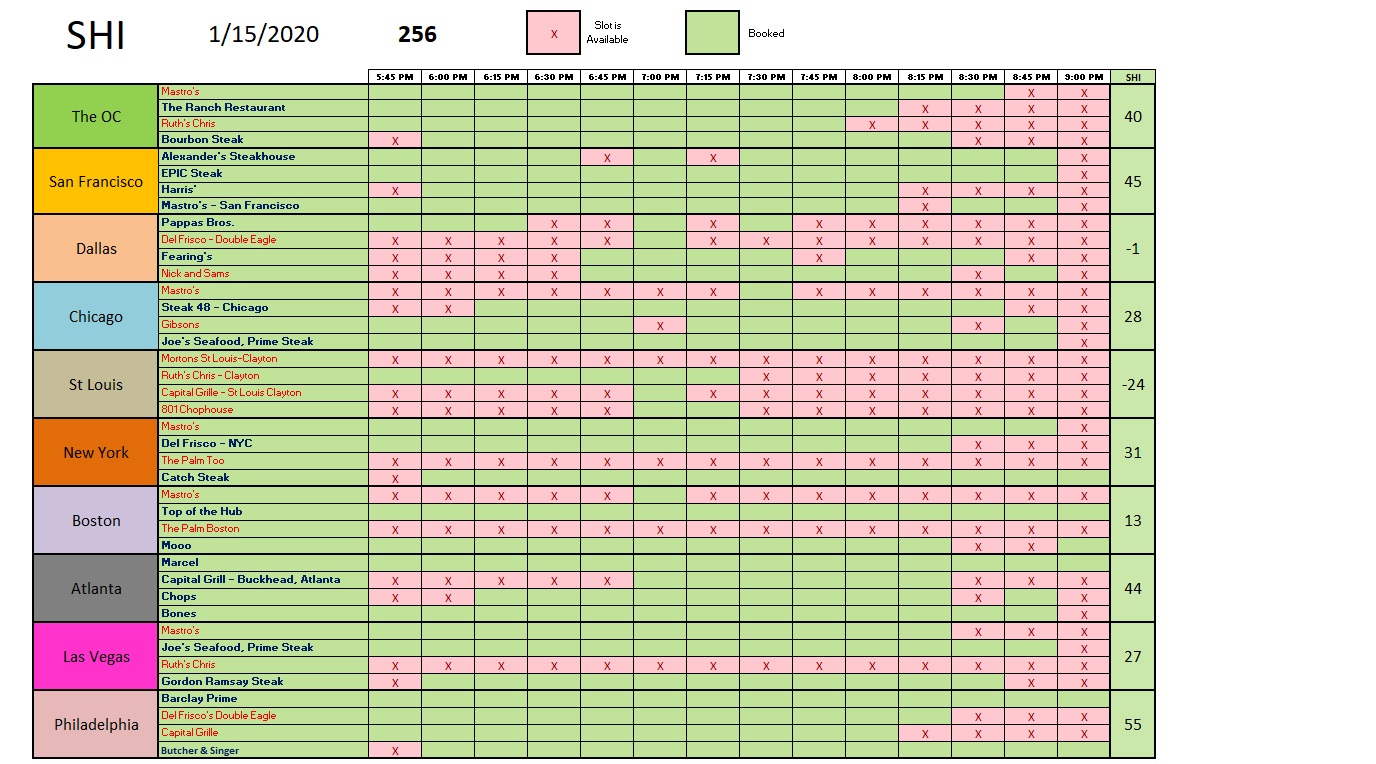

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will be true for years to come.

But is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $85 trillion today. According to the most recent estimate, US ‘current dollar’ GDP now exceeds $21.53 trillion. In Q3 of 2019, nominal GDP grew by 3.5%, following a 4.7% annualized growth rate in Q2. The US still produces about 25% of global GDP. Other than China — in a distant ‘second place’ at around $13 trillion — the GDP of no other country is close. The GDP output of the 28 countries of the European Union collectively approximates US GDP. So, together, the U.S., the EU and China generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

What do Star, Idaho and Greenwich, Connecticut have in common? Almost nothing.

Well, both cities have people, businesses and homes. But while home values in Star are rising like, well, a star, values in Greenwich are dropping like a stone. According the Wall Street Journal, the medial home price in Star has more than doubled to almost $400,000 since 2010.

Let’s get back to Greenwich. Because of it’s proximity to New York City, and the fact that in 1991 Connecticut reduced income tax rates on “investment” income from 13% down to only 4%, Greenwich become a veritable powerhouse of 20th-century finance. Numerous hedge-funds located in the town and their owners built or bought multi-million dollar homes. And they located their offices downtown. So, by the early 2000s, a third of its commercial property was occupied by hedge funds, and rents on Greenwich Avenue rivaled those on Park Avenue, New York.

Then the “Great Recession” came, crushing the fortunes of many fund managers and the state itself. Connecticut decided to increase state income taxes. By 2014, their ‘maximum’ income tax rate was now 6.7% — on income over $250,000. Many that were originally attracted by tax-free living decided it was time to go. And go they did: they left by the droves. Between 2015 and 2016 Connecticut lost more than 20,000 residents—including 2,050 earning more than $200,000 per year. Some experts believe the state is now collecting less tax than they did before the tax rate hikes. Oops.

Interestingly enough, leaving Greenwich often meant accepting a low offer. “You can’t give away a house in Greenwich,” said Barry Sternlicht of Starwood Capital when he moved to Florida in 2016. Poor Barry.

And poor Greenwich. But the good news for Connecticut is this: They can solve their problem. Fairly easily, in fact.

Japan, on the other hand, which has the same problem as Greenwich, probably cannot.

(Permit me a brief personal comment: I feel its worth mentioning that I feel bad highlighting “negative” news about Japan yet again. I’m actually a big fan of Japan! I have enjoyed traveling around the country, the people I’ve met there are wonderful … and I absolutely LOVE sushi! But, unfortunately, the country has some serious structural flaws. Much like we do here in the US. But unlike the ‘home value issue,’ the factors triggering financial and economic challenges in both the US and Japan are identical, in my opinion: Decades ago, a demographic shift began that is just now reaching a crescendo in the US … but, in Japan, it has been wreaking havoc and adversely impacting their economy for more than 2 decades. And the damage has just begun — it will get much worse.)

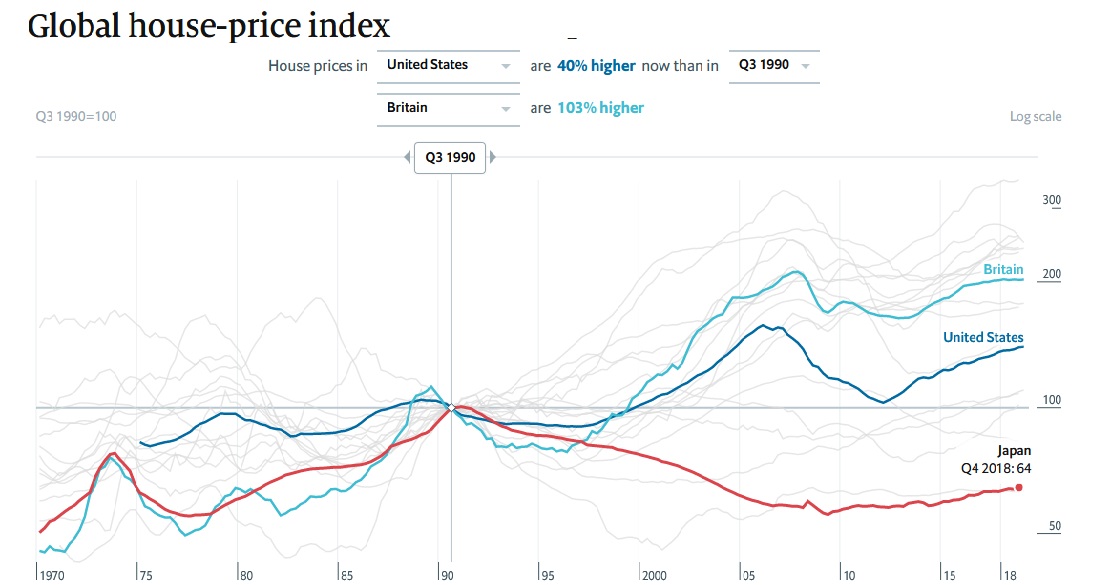

Take a look at the chart to the right, provided by the Economist magazine. It’s easy to see the cyclical patter for home values across the globe, from 1970 to the present. I’ve highlighted the US, England and Japan.

Take a look at the chart to the right, provided by the Economist magazine. It’s easy to see the cyclical patter for home values across the globe, from 1970 to the present. I’ve highlighted the US, England and Japan.

Here in the US, where home values were heavily impacted by the Great Recession, we see that values, in general, have recovered nicely — up 40% above values in 1990.

Home values in England were not hit as hard as they were here. We see that home values in England were recovering nicely until the ‘Brexit’ vote, when value increases started to cool a bit. Still, English home values are UP 103% since 1990.

But values are not higher in Japan. In fact, since “peaking” in 1990, home values across Japan have fallen precipitously. Compared to the 1990 ‘index value’ of 100, today’s reading is only 64. Which means values have fallen by 36% across Japan as a whole.

Why? In a word, demand. Japan has a serious demand problem. Again, why? Japan’s population peaked at about 128 million folks in 2008. Population has been declining since that time. Not by a huge amount, mind you, but as of the end of 2018, population had fallen to 126.5 million people. Not only is Japan’s population significantly older than it was 30 years ago, Japan’s population is now actually shrinking. This demographic condition creates a macro-economic problem: Underlying aggregate housing demand — due to population aging and shrinking — is falling across Japan.

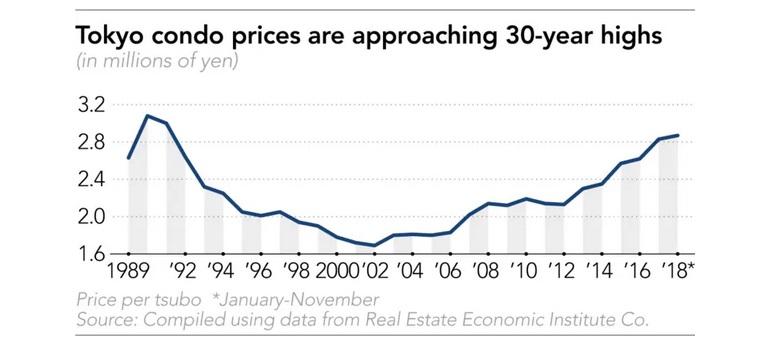

Of course, home values are not falling everywhere in the country. According to the Nikkei Asia Review, Tokyo condo prices are near a 30-year high. Per the graph below, values did decline from 1990 to around the year 2002, but values have been rising since then. Take a look:

If values in Tokyo — and other big cities across Japan — are up significantly, then the carnage across small towns, villages and in the countryside must be sizable. If values across ALL of Japan are down 34%, but they are UP in Tokyo, I can only imagine how much they have fallen outside the larger cities. Ouch.

Leadership in Japan caused this problem. The made two huge errors. First, the permitted the country’s fertility rate to fall below the absolute minimum of 2.1. Yes, they permitted it. Because they didn’t see the fertility problem when it began. So they made no attempt to solve the problem. They needed a robust child-care strategy to help working couples deal with day-care and the increased cost of child rearing when both parents were employed in the work-force. They didn’t recognize the problem as a problem when it began. And now, almost 2 generations later, their country is shrinking. Literally. Which is adversely impacting demand for homes and just about everything else.

The second error is their century’s-old aversion to immigration.

The rest of the developed world hasn’t done much better. They, too, seem to have failed to notice that increased participation of women in the work force is clearly associated with decreased fertility. And so, their populations too, will be shrinking soon in the not too distant future.

And the US is right behind them. We have the identical challenge. But I believe there is some good news for the United States:

It’s NOT too late!

We can fix this. But a fix will require serious focus from the House and Senate ASAP. In my opinion, this is the single most important long-term economic challenge our nation faces today! Bar none.

OK…it’s time for a steak. How are our extravagant, expensive eateries faring this week?

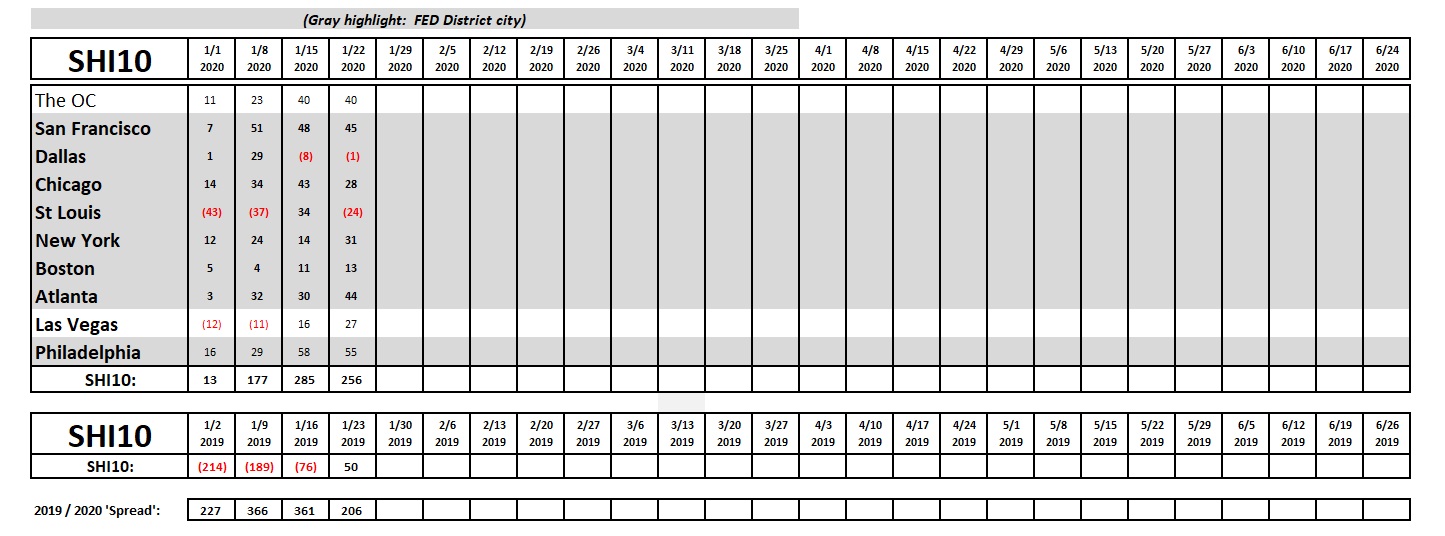

Pretty good. Reservation demand is fairly consistent with last week. Demand seems to have softened in St Louis … and firmed a bit in NYC. But, overall, pretty much the same as last week. Here’s our longer term trend chart:

The “old” SHI10 reading had a good showing this week last year — as you can see above. So the spread narrowed this week. This is interesting, but not overly meaningful.

Yesterday, speaking at Davos, Switzerland, President Trump commented, “I’m proud to declare that the United States is in the midst of an economic boom the likes of which the world has never seen before.” Hmmm….well…I hope our President is employing a bit of hyperbole here, because, unfortunately, I have to disagree. Sure, the economy is chugging along. But are we in the midst of an economic boom? Unlike any before? No. We are not.

But for the moment, things are just fine. Economically speaking.

– Terry Liebman