SHI 10.8.25 – Zero-Sum Game?

October 8, 2025SHI 10.22.25 – Bubble Talk, Epilogue

October 22, 2025

“Is this a bubble?”

This blog is the THIRD and final “bubble-talk” blog I will write on this amazing chapter in American history. Of course, I’m talking about artificial intelligence. And how quickly those two words have rapidly transformed the every-day dialog about our society, our lives, our economy — really, the entire world — in such a short time. The change has been so rapid, many people are asking the question, “Is this a bubble?” And as this is a financial and economics blog, today I will answer the question:

Is this a financial markets bubble?

My first blog framed the discussion. The second blog debated divergent facts and ideas.

Today? You will get answers. Well, at least my opinion on the answers. And what is my opinion worth? You decide.

If you missed my first blog, here’s a link (right click, open in a new tab):

And here’s the second blog:

So: Is this “AI thing” a bubble?

Welcome to this week’s Steak House Index update.

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding.

The ‘real’ growth rate — the number most often touted in the mainstream media — was 3% in the last quarter. In “current dollar” terms, US annual economic output rose to $30.331 trillion.

According to the World Bank, the world’s annual GDP expanded to over $111 trillion in 2024. Further, IMF expects global GDP to reach almost $132 trillion by 2030. The US? Various forecasts project about $37 trillion for American GDP in 2030 — I believe it could be even higher.

America’s GDP remains around 28% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

As of August 2025, margin debt in the stock markets reached $1.06 trillion, the highest it’s ever been.

I heard that fact when listening to an “Odd Lots” podcast. And I asked myself, “Wow, could that be true?”

It is. According to FINRA, a securities agency who publishes these figures monthly, this was a new ‘nominal’ record. At no time in history, according to FINRA, has margin debt been higher.

Andrew Ross Sorkin has published a new book titled, “1929: Inside the Greatest Crash in Wall Street History — and How It Shattered a Nation“. I’ve purchased it, but have not read it yet. But on that same podcast, Sorkin opined that his greatest fear in seeking a corollary with 1929, or for that matter the “dot-com” bust, is precisely this: LEVERAGE.

In other words, to the extent that today’s investors are borrowing ever-increasing amounts in order to increase their stock investments, that’s his greatest fear — and the potential cause of a popping bubble.

But here’s the thing about facts. Sometimes facts are factual, but they lack context. Yes, margin debt is at an all time high. However, as a percentage of market capitalization, the number is actually fairly tame. At it’s 2021 peak, margin debt was just under 4% of the total stock market capitalization. Today, that number is less than 2%. So, yes, the nominal number is UP, but the percentage of total stock market value is down — and down significantly.

Sorkin shared that in the 1920s, an “investor” could buy stocks with 90% leverage. In other words, with only 10% down, and a 90% loan, one could buy stocks. And after they appreciated, that same investor could “refinance” and buy even more stocks!

Wow.

In an opinion piece in today’s The Economist magazine, titled “Gita Gopinath on the crash that could torch $35 trillion of wealth,” Ms. Gopinath shared some alarming opinions:

“I calculate that a market correction of the same magnitude as the dotcom crash could wipe out over $20 trillion in wealth for American households.

This is several times larger than the losses incurred during the crash of the early 2000s. The implications for consumption would be grave. The global fallout would be similarly severe. Foreign investors could face wealth losses exceeding $15 trillion.

This stark increase in spillovers underscores how vulnerable global demand is to shocks originating in America.”

The article pointed out that should this crash occur, 70% of US GDP could vanish. And concurrently, another 20% could disappear from the rest of the world. Ms. Gopinath is worth listening to. She was a deputy Managing Director of the IMF – the International Monetary Fund – for about 3 years and is presently a professor of Economics at Harvard.

Ms. Gopinath, of course, correctly uses the word “could” in her opinion piece. But, at the end of the day, opinions are precisely that. Opinions.

Balance Ms. Gopinath’s opinion against that of Kathy Wood, the founder of a number of high-tech focused EFTs, including the ARK Innovation ETF with assets under management of almost $9 billion. Ms. Wood is of the opinion that artificial intelligence has a “once-in-a-generation” potential to double global GDP in the coming years.

Directionally, one of these two opinions will likely be spot-on. But which one?

It looks like it’s time for me to share my opinions. 🙂

IS THIS A FINANCIAL BUBBLE?

In my opinion: No. I don’t think so. At least, not yet. And at least not in total. Let me explain.

Some portions of today’s investment landscape is bubblish. There are companies and investors out there today who will lose massive amounts of money and likely go broke. Many are ill conceived and foolishly supported. But I don’t think the tech leaders are in bubble territory. Nor do I believe the majority of the S&P 500 are overpriced. Yes, they are all expensive, but I don’t believe outlandishly so. Why?

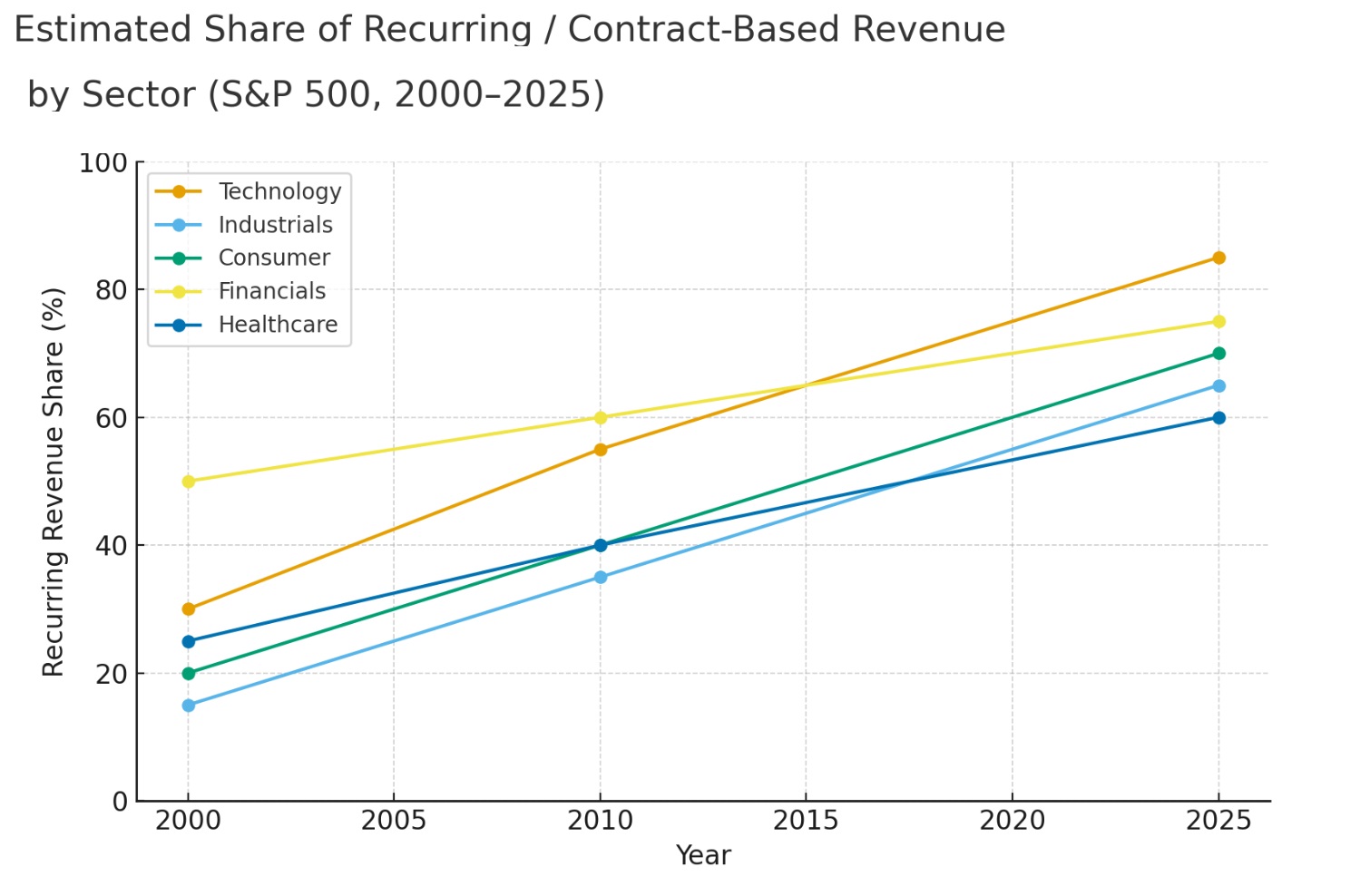

For many reasons. But primary because of corporate earnings. And because of the complexion of those earnings. Consider this image:

Since 2000, S&P500 earnings today are far more consistent due to the fact that they are recurring or contract based. The chart reflects these facts … but here’s the data:

<> Technology has surged from ~30 % to ~85 %, driven by the SaaS and cloud shift.

<> Industrials and Consumer sectors are now at about 65–70% recurring.

<> Even Financials and Healthcare have become progressively more fee- and plan-based.

So all this begs the question: Should today’s P/E multiple logically be higher than 25 years ago?

I suggest it should. And, of course it is. According to FactSet, the forward 12-month P/E ratio for the S&P 500 is now 22.8. This number is above the 5-year average of 19.9% and the 10-year average of 18.6%.

Further, corporate earnings continue to grow — and I believe this is just the beginning. Recently, FactSet published an opinion piece titled, “S&P 500 Will Likely Report Earnings Growth Above 13% for Q3.”

It’s worth noting, by the way, If we remove the top-8 companies by market cap from that calculation, the P/E ratio of the bottom 492 is currently around 18.5.

I believe corporate earnings will accelerate from here. Along with GDP. Which, in turn, will push P/E ratios down. And so on. I’ll be watching this trend closely. Further, I see no abusive leverage within the marketplace. At present. Again, we need to watch this.

We all know the hyperscalers are seemingly investing money into AI with reckless abandon. Everyone clearly wants to win the race.

But it’s generally money they have — again, for the most part, they are spending retained earnings. On the other hand, OpenAI is definitely highly leveraged. They are truly the outlier. And there’s no doubt that a meaningful problem at OpenAI could definitely destabilize the market. That is a personal concern. But one without reason or merit. Just a concern. Worth watching.

I could go on and on, but you get the point.

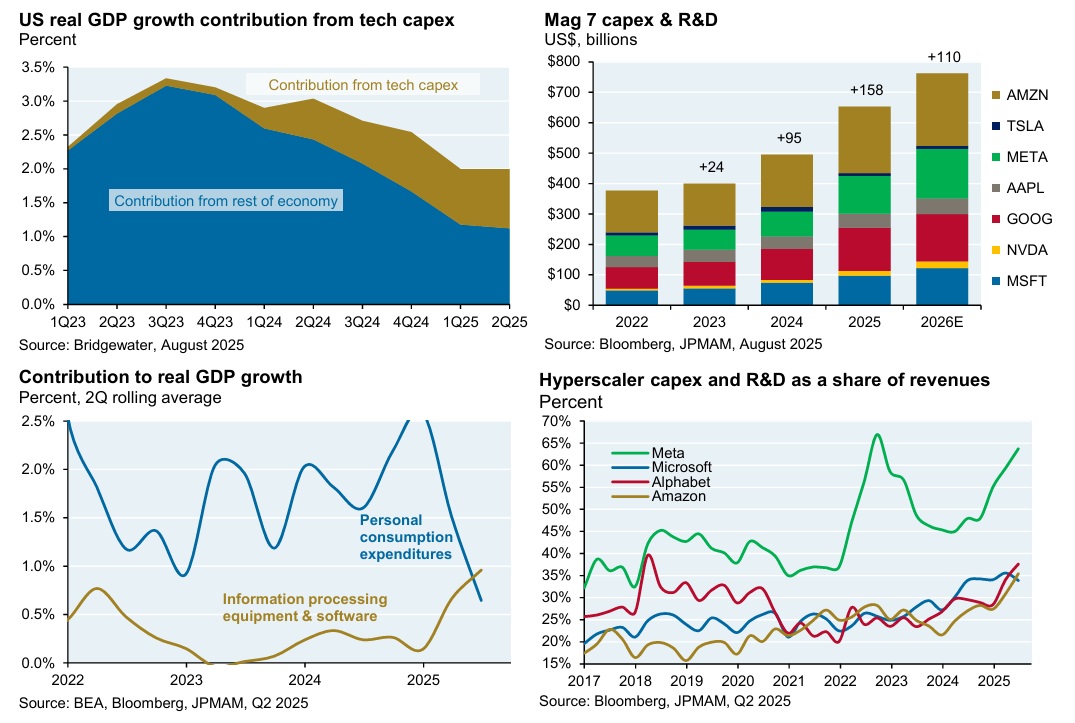

One of the best economic analysts I read is Michael Cembalest at JP Morgan Securities. The data is his weekly “Eye on the Markets” research is without equal.

The image below is one I clipped from his September 2nd publication.

Again, the capex levels are truly staggering. But so is the impact on GDP. This is real 2025 growth. And will likely also recur in 2026 and 2027. And by then, I expect the ROI on these investment will be significant. How significant?

When the Emirati Sheikh Tahnoon bin Zayed Al Nahyan built his new mansion, ChatGPT helped create the final design: Tahnoon prompted ChatGPT some 500 times while constructing his Japanese-style seaside home. And now, Tahnoon pledged to give a paid version of ChatGPT to every UAE schoolchild for free. And this is meaningful because Tahnoon is the ‘National Security Advisor’ and the driver of UAE’s push into AI. And he runs their $1.5 trillion investment fund.

Sure, the sheikh’s use of ChatGPT is probably not pushing much revenue toward OpenAI. Yet. But this is how it starts, right? Get everyone hooked? 🙂

Which brings me to my second point: In my opinion, this episode IS transformational. The world is changing right before our eyes. I can’t be certain it’s for the better, of course, but it is changing. I just hope we don’t discover the movie The Terminator was a documentary. 🙂

Finally, in my opinion, this transformation may also be existential for many members of our global society.

Since the beginning of time, mankind has worked to survive. Whether hunting, farming, sewing buttons, or completing an LBO, people have worked. If artificial intelligence ushers in a new era where rapid GDP growth is unrelated to work effort, what will we all do if society becomes so wealthy that work, essentially, becomes unnecessary? Could society get to a place where work is optional? And what will non-working people do with their time?

So, for now, I believe investment values are supported and justified by current conditions and near-term expectations. There is no generalized bubble. In my opinion.

What do you think? Shoot me an email.

< Terry Liebman >

{kind=link}