SHI 11/20/25 – The Swan and the Canary

SHI 11.5.25 – Miles and Miles of LARGE Debt Piles.

November 5, 2025

SHI 12.10.25 — Prediction Predilection

December 10, 2025

Today’s blog title might sound like a fable or proverb, but my writing skills fall short of any such creativity. And this is economic blog, clearly devoid of poetic artistry!

🙂

So let’s move on and let me contextualize these “bird” phrases and their relevance to current events.

“

Birds of a Feather: A “Swan Song” and

the “Canary in the Coal Mine”

“

Birds of a Feather: A “Swan Song” and

the “Canary in the Coal Mine”

Have you ever wondered how the term “swan song” came to be?

The phrase originates from an ancient Greek belief that swans, usually silent, would sing a beautiful, mournful song just before dying.

In reality, this is “fake news.” Swans do not sing before death; it’s a myth that has persisted over centuries. By the Middle Ages and Renaissance, “swan song” became a metaphor for a final performance or a person’s final public act before retirement or death. Today, it simply refers to a last appearance, effort, or performance before the end.

Could 2025 be Warren Buffett’s swan song?

Who knows, as he’s now 95 and seemingly going strong. Regardless, his 2025 “Thanksgiving Message” is a wonderful read, full of age and wisdom, and I recommend reading it in its entirety:

https://www.berkshirehathaway.com/news/nov1025.pdf

One observation from Mr. Buffett’s letter stands out to me:

“Those who reach old age need a huge dose of good luck, daily escaping banana peels, natural disasters, drunk or distracted drivers, lightning strikes, you name it. But Lady Luck is fickle and – no other term fits – wildly unfair. In many cases, our leaders and the rich have received far more than their share of luck – which, too often, the recipients prefer not to acknowledge. Dynastic inheritors have achieved lifetime financial independence the moment they emerged from the womb, while others have arrived, facing a hell-hole during their early life or, worse, disabling physical or mental infirmities that rob them of what I have taken for granted. In many heavily-populated parts of the world, I would likely have had a miserable life and my sisters would have had one even worse.”

This man’s writing skills far surpass mine. Thank you, Mr. Buffett.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. But is the US economy expanding or contracting?

Expanding.

The ‘real’ growth rate — the number most often touted in the mainstream media — was 3% in the last quarter. In “current dollar” terms, US annual economic output rose to $30.331 trillion.

According to the World Bank, the world’s annual GDP expanded to over $111 trillion in 2024. Further, IMF expects global GDP to reach almost $132 trillion by 2030. The US? Various forecasts project about $37 trillion for American GDP in 2030 — I believe it could be even higher.

America’s GDP remains around 28% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Let’s talk about the “Canary in the Coal Mine.”

In the early 1900s, coal miners would carry canaries as they traveled underground. These birds are much more sensitive to carbon monoxide and methane gas than humans. The miners watched the canaries closely; if a canary died, it signaled a dangerous gas buildup long before the miners themselves would notice symptoms. It was time to get out. Quickly.

Today, the expression lives on as an early warning sign of impending danger or disaster. With so much talk around an “AI bubble”, one has to wonder is there’s a modern-day equivalent we might use for early economic warning today?

Leverage might be that economic ‘canary.’

I’ve talked about margin debt in the past. Another window into debt and debt ratios is the amount of debt public companies carry on their balance sheets, measured against their earnings before taxes and depreciation. Historically, a debt-to-EBITDA ratio of 3.0x to 4.0x is considered the upper bound of “safe” leverage for public companies in most industries. Ratios above this range often signal elevated financial risk, especially if the company’s cash flows are volatile.

So when a company starts pushing against that upper limit, analysts and market experts become concerned. This is today’s case with Oracle.

As we all know, the hyperscalers have committed astronomical amounts of capital this year for AI infrastructure: Data centers, GPU farms, networking, power, cooling, etc. are all being furiously added all over the world. Historically, these companies funded their growth through free-cash-flow. But this source has its limits: The current pace and scale of the AI-buildout has pushed them into debt issuance (public bonds/debt, private credit, leases) and other non-traditional structures, including “off balance sheet” financing vehicles such as “power-purchase agreements, sale/lease-back agreements, and colocation leases. Each of these require large future repayments in exchange for immediate debt or investment by the counterparty. Microsoft, Meta and Amazon are each using these financing techniques this year. Many of these multi-billion dollar commitments don’t show up on their balance sheets, even though they behave as fixed debt. At best, they appear as a CPA audit note in their audited annual financial statements.

But, on the good news side of the equation, they can afford it. Remember, their annual, recurring revenue streams are massive. Their ‘free-cash-flow’ (FCF) for their last fiscal year was $74 billion, $52 billion, and $38 billion, respectively.

Finally, they each have a debt-to-EBITDA ratio of about ½ x. Far below that 4x limit we discussed above.

The bottom line: I’m not a fan of these off-balance sheet vehicles, but Microsoft, Meta and Amazon can easily afford them. The same cannot be said about Oracle.

Their “net debt” to EBITDA ratio – let’s call this a “debt burden” – is around 4x. Some estimate it closer to 5x. About a month ago, Oracle issued another $18 billion in debt to fund AI datacenter investment – yes, this amount is included in the current debt burden. They are near $100 billion in long-term debt at present.

However, banks are preparing another $38 billion debt offering for Oracle. And analysts have projected Oracle’s net debt could reach $290 billion by 2028, almost tripling from today’s already elevated levels.

Is this our canary? You decide.

But to be fair, the $38 billion debt and investment I mention above supports a commitment from OpenAI to spend $300 billion with Oracle over a 5-year period in exchange for Oracle’s investment in massive GPU data center expansion in Texas, New Mexico and Wisconsin. So perhaps the risk is warranted.

Regardless, estimates put Oracle’s current annual EBITDA at about $22 billion. Assuming it grows to $30 billion by 2028, that would put their debt burden at about 10x. That’s not good. In fact, it might be quite bad … and even dangerous. Oracle has experience carrying a debt burden of between 4-4.5x. But 10x, if it came to pass, would be concerning to me.

The hyperscalers can afford a mistake – even many mistakes – here. If their data-center dreams don’t come to fruition, they will be fine. The same, I fear, cannot be said about Oracle. One has to wonder why Larry Elison is betting the farm on this one?

It’s worth remembering Mr. Ellison has become one of the wealthiest people in history by making bold bets, so one has to believe the odds are in his favor, and Oracle will be fine. Still, again, the air is thin up there.

Fascinating, right? My take away here is this: Watch debt levels and debt accumulation as diligently as you can. Keep track of those “off balance sheet” deals, too, to the extent possible. Any of the popular AI engines can help. Use them.

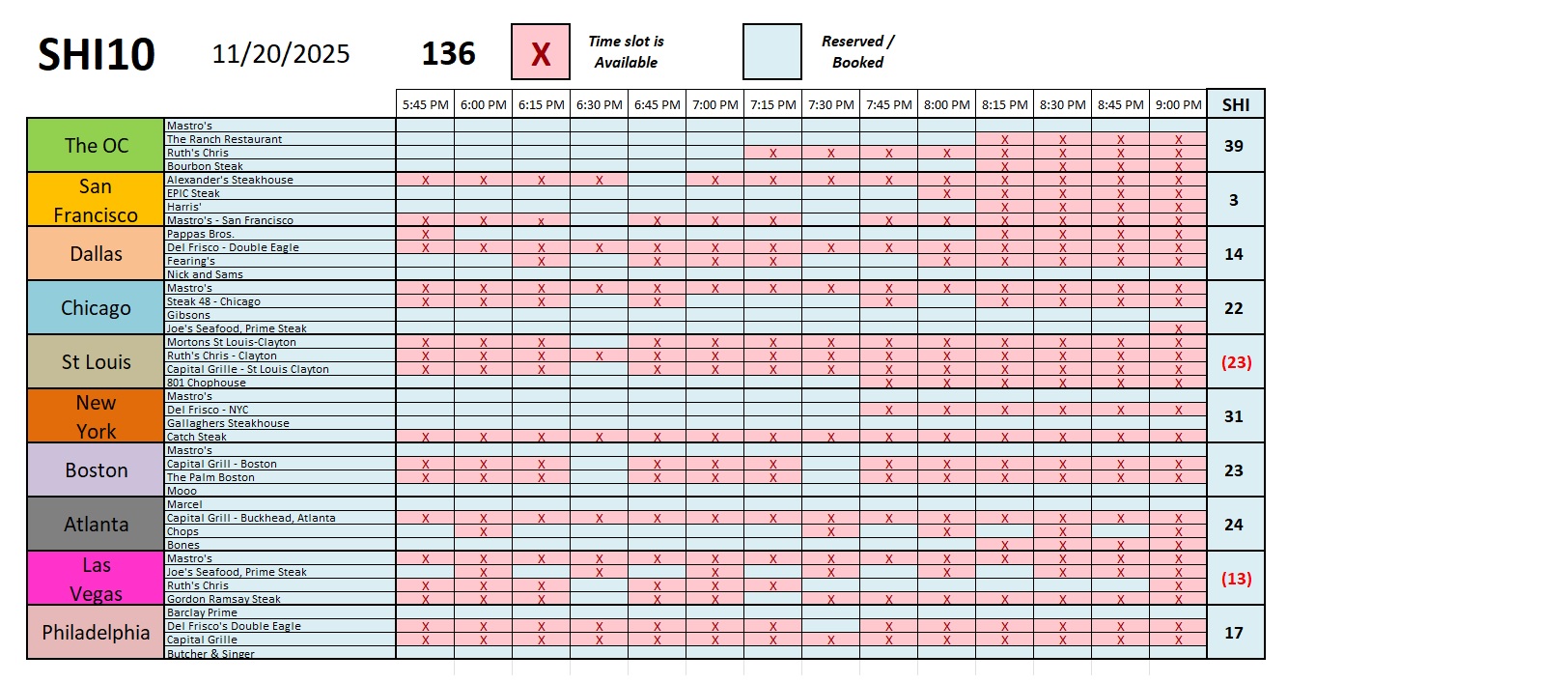

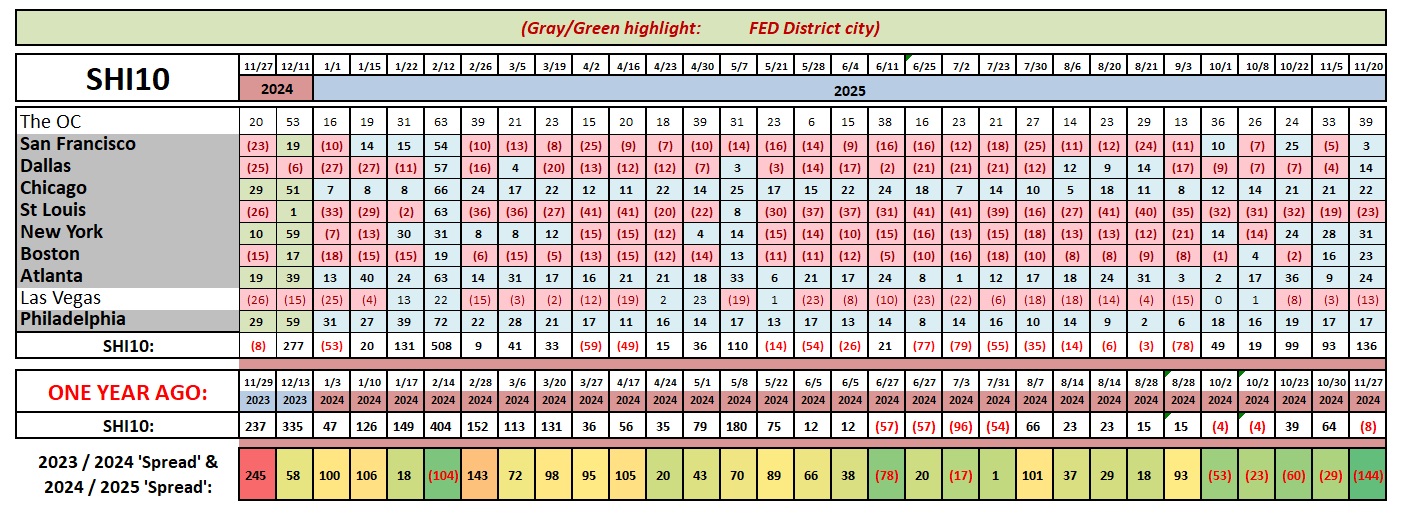

But at the end of the day, I do consider leverage and debt burdens to be key financial-health metrics. Watch them carefully. Shall we check in on the steak houses?

Interesting! We have an SHI40 firmly in the black. Only two of our 10 markets reflect negative demand numbers. This is quite a departure from the trend. Take a look:

I’m using the word ‘interesting’ a lot today. But, hey, it works. Here’s why I find this so interesting:

The US economy is clearly extremely large and complex in nature. I often focus on economic conditions — like GDP growth rates — in the macro. In doing so, I tend to ignore the nuance. Right now, my indicators suggest the US economy is growing at a solid rate. However, this doesn’t mean everyone of America’s almost 350 million residents are enjoying the same experience. As Mr. Buffet opined above, some folks have found America’s streets to be paved with gold … others have not.

The SHI40 focuses more on the upper strata of the population, and their propensity to buy an expensive, hot-off-the-grill, restaurant-served New York steak. This is how this alternative economic barometer was designed. That is its purpose. And today’s results seem to indicate that the SHI40 and US GDP growth rates are well aligned.

There is no doubt many Americans continue to experience challenging economic times — inflation and housing are serious headwinds for most Americans. Especially those at the bottom end of the ladder.

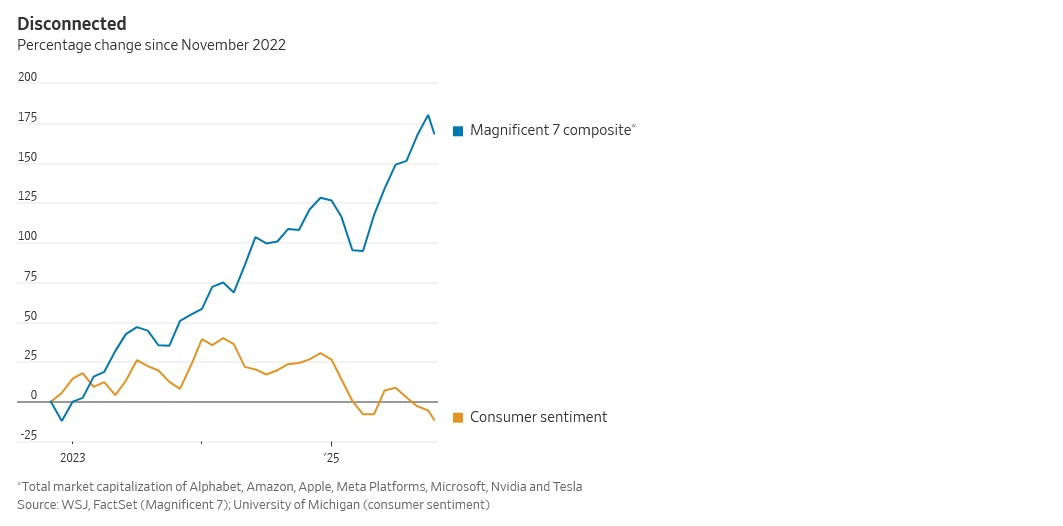

On that topic, Greg Ip, the senior economics writer over at the Wall Street Journal, wrote a piece titled, “The Most Joyless Tech Revolution Ever: AI is Making Us Rich and Unhappy,” sharing this image:

{kind=link}