SHI 12.10.25 — Prediction Predilection

SHI 11/20/25 – The Swan and the Canary

November 20, 2025

SHI 12.24.25 – A Toast, and goodbye, to 2025

December 24, 2025

Some people have a predilection for making predictions. They just can’t help themselves. I put myself in that camp.

Economists, generally, are also firmly in that camp. In fact, I would go as far as saying that making predictions is essentially their work product. That’s really what they produce after analyzing data. The FED has a larger collection of economic PhDs than any other group. And, of course, they put out a lot of predictions about our economy.

“

Predictions are essential

for economists and investors.”

“

Predictions are essential

for economists and investors.”

Speaking about the FED, its no surprise to anyone paying attention that President Trump is no longer a support of the current FED Chairman, Jerome Powell. Rumors about the name of the next FED chair are flying fast and furious.

And now, we have a new prediction tool: Polymarket. If you’re not yet familiar with Polymarket, you should check it out. I’ll talk more about it below, but right now, Polymarket puts the odds of Kevin Hassett winning the seat at 75%. Check out this graphic:

Kevin Hassett is clearly the front-runner. Right or wrong, Polymarket is certainly making economic forecasting more interesting – and, potentially, profitable!

Profitable? Yep, let me explain.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. But is the US economy expanding or contracting?

Expanding.

The ‘real’ growth rate — the number most often touted in the mainstream media — was 3% in the last quarter. In “current dollar” terms, US annual economic output rose to $30.331 trillion.

According to the World Bank, the world’s annual GDP expanded to over $111 trillion in 2024. Further, IMF expects global GDP to reach almost $132 trillion by 2030. The US? Various forecasts project about $37 trillion for American GDP in 2030 — I believe it could be even higher.

America’s GDP remains around 28% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

The year is 1999. You just turned 37 and are thrilled to be the co-author of a new book, “Dow 36,000,” officially published on October 1st of 1999, which lays the case for the DJIA reaching 36,000 in the not-distant future. Rest assured: This is a bold prediction. At the time of publication, the index was hovering near 10,000.

Of course, unknown by the co-author, Kevin Hassett, the infamous Dot-Com Bust would occur just 5 months in the future. The official date of the bubble burst was March 10, 2000.

Oops. The book’s timing was as catastrophic as the prediction itself. Just months after the book hit shelves, all markets crashed:

-

The S&P 500 fell about 49%

-

NASDAQ collapsed almost 78%

-

The Dow dropped near 38%

It’s no surprise that after the crash, Dow 36,000 quickly became the fodder for jokes, and the authors had to be quite embarrassed. Playing on Greenspan’s “irrational exuberance” comment from a few years before, many now attributed “irrational optimism” to Hassett and his co-author.

Fast forward to now. Hassett holds the position of “Director of the National Economic Council” (NEC) in the Trump Administration. He is also the front-runner for FED chair to replace Powell. As the president has the responsibility to appoint the FED chair, and as Chair Powell’s tenure expires early in 2026, Trump will need to appoint someone. Hassett seems the likely choice given the current rhetoric.

One likely reason is that he has publicly shared that like Trump, he is in favor of a larger interest rate cut. And as the FED Chair, he would use his influence to make that happen. On Tuesday, at the WSJ CEO Council Summit, when asked about rate cuts, Hassett commented

“If the data suggests that we could do it, then — like right now — I think there’s plenty of room to do it,” he said. Asked whether that meant more than 25 basis points, he said, “correct.”

Here are a couple of questions for you to consider, given the fact that many investors are already feeling great deal of anxiety: Is “FED independence” at risk with Hassett in the seat? And, given his tendency toward irrational exuberance, is he the right man for the job?

Let’s talk about FED independence first. There’s been a lot of hand-wringing over this one of late. If you, too, were worried about this, stop. Sure, Hassett or some other Trump appointee is likely to be influenced by Trump and other administration members. Every FED chair is influenced, to some extent, by the current administration. Independence is not maintained inside this relationship; independence is assured by the inherent design of the ‘rate setting committee’ called the Federal Open Market Committee, or FOMC for short. The FED chair – just like every other voting member of the FOMC – gets one vote. How many voting members are there on the committee? Twelve. So, sure, the President can influence the FED chair, and the FED chair can influence the other 11 voting members on the FOMC. But each member is a financial and economic luminary in and of him/herself, so rest assured they are not easy to influence.

How about Kevin’s tendency toward irrational exuberance? Is this a bad characteristic for a Federal Reserve chairman?

No. In fact, I personally find it endearing and entertaining. I like Kevin’s tendency toward optimism. I actually see it as a positive. However, I wouldn’t take investment advice from Kevin. 🙂

Betting on the Polymarket site is not investing. Have no doubt: It is a betting site. Consider this “question” trading on the Polymarket site: “What price will Bitcoin hit in 2025?”

Suppose you believe BTC will hit $200,000 next year. You could buy it now, somewhere around $93,000 and if you’re right, you can more than double your money. However on the Polymarket site, you can “bet” 3 cents against a $1 “return” if you are right. If BTC hits (or exceeds, I presume), $200,000 during 2026, your $300 “investment” would return $10,000 if BTC reached the metric. This is a 33X payout. Much better than that paltry doubling in value if you actually bought the thing!

Of course, alternatively, you will lose your entire $300 if BTC stays under $200K during 2026. So, I’ll repeat: This “prediction” site is actually a betting site. But here’s the twist: Some of the prediction events inspire exceptionally heavy betting. For example, the 2024 presidential election was such an event. Over $3.3 billion was wagered on the outcome of the elections.

Which is interesting. While the polls showed the election between Trump and Harris to be quite close, in late 2024, Polymarket reflected up to a 60% chance of a Trump victory. To paraphrase a proverb, people put their “money where their mouth was.”

So is Polymarket a type of crowd-sourcing forecasting platform? If hundreds of millions, or even billions are bet on the outcome of a forecast, does this suggest the likelihood of the outcome increases with the amount of money that is actually bet on that outcome?

It’s an interesting question.

You may have heard of Bayesian probability, and how it can be used in economic modeling as “observed data” becomes increasingly available. Said simply, the Bayesian model suggests that the probability of a certain outcome occurring is impacted by “new information” as that new information grows in quantity and frequency. Using that approach within the Polymarket model, Bayesian probability suggests that yes, in fact, the more money bet on a specific outcome suggests that increases the probability of that outcome. The presumption is that those people willing to risk their hard-earned-cash on the bet must have some reason for making the bet. Perhaps hunch, intuition, or maybe some exceptionally deep research was the catalyst for the bet. But regardless of the catalyst, each bet becomes “new information” that can be used to measure the ever-evolving probability.

Which is why the constantly evolving Polymarket probability inference for the next FED chairman is meaningful. If this is an outcome you find interesting, follow the Polymarket betting and see where it goes.

How about other Polymarket predictions? Here’s one I’m interested in: Will the FED cut interest rates in 2026?

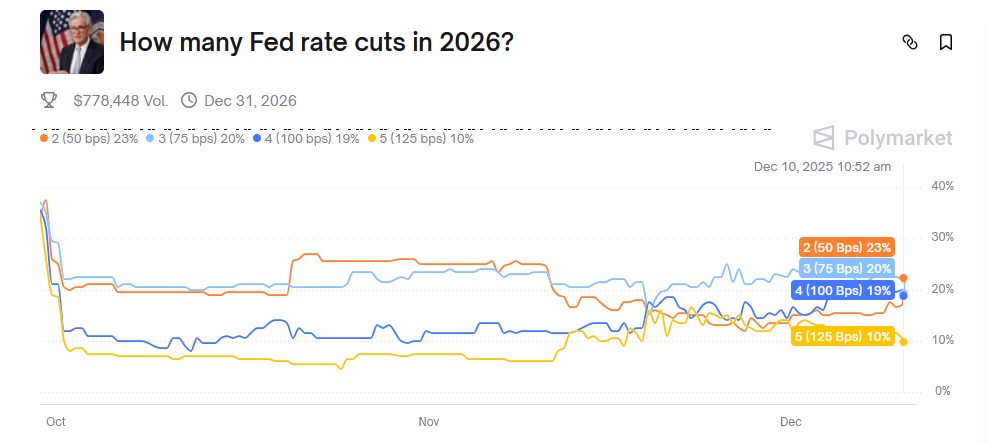

Let’s check Polymarket. A question in the mix right now is: “How many Fed rate cuts in 2026?”

Looks like a horse race! 2 cuts is the current favorite … but 3 and 4 are close behind. 🙂

The steakhouses are always a horse race. Today is no different.

Reservation demand for this Saturday, December 13th, is strong. One of the more fascinating transformations, at least to my eyes, is the San Francisco SHI. Take a look:

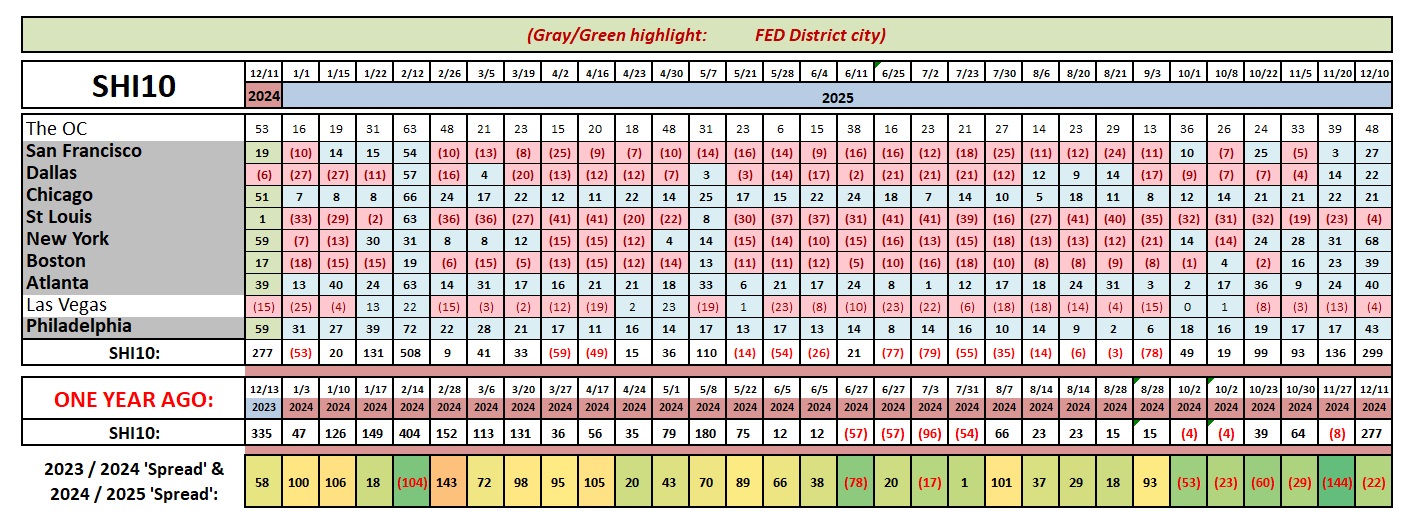

After spending much of the year in the ‘red‘ the SF market seems to be sizzling. As you probably know, SF is the heart and soul of the exploding AI movement. After spending a handful of years in the dog house, the city’s economic fortunes seem to be smiling. And the SHI reservation demand reflects the city’s budding optimism.

All in all, the SHI firmly supports the idea that America, in the macro, is firmly in the grips of a meaningful expansion.

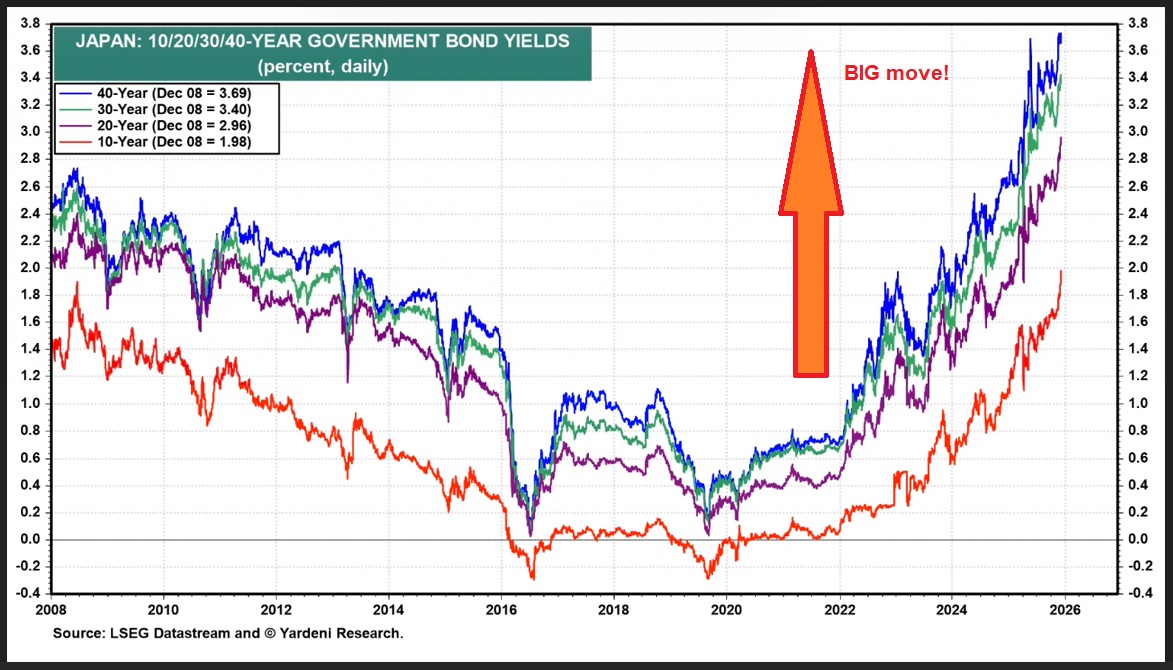

Shifting gears for a moment, take a look at this graph:

Interest rates in Japan are skyrocketing! Thru the lens of their prior levels, of course. For 2 or 3 decades, the rates on Japanese long-term debt was close to zero. No longer. The reasons are lengthy and complex, having to do with foreign exchange rates, inflation, maintaining the value of the yen, and a host of others — the least of which is the fact that Japan’s debt to GDP ratio has, for years, exceeded 200%.

But, interestingly enough, that ratio is now declining.

It may actually have dropped below 200%. Why? Have they been paying down debt?

Nope. They have been steadily increasing GDP, after decades of shrinking. They are demonstrating how a country might “grow their way our of their debt.” This is no small feat after their extended duration in their “balance sheet recession.” I’ll talk more about this in a future blog.

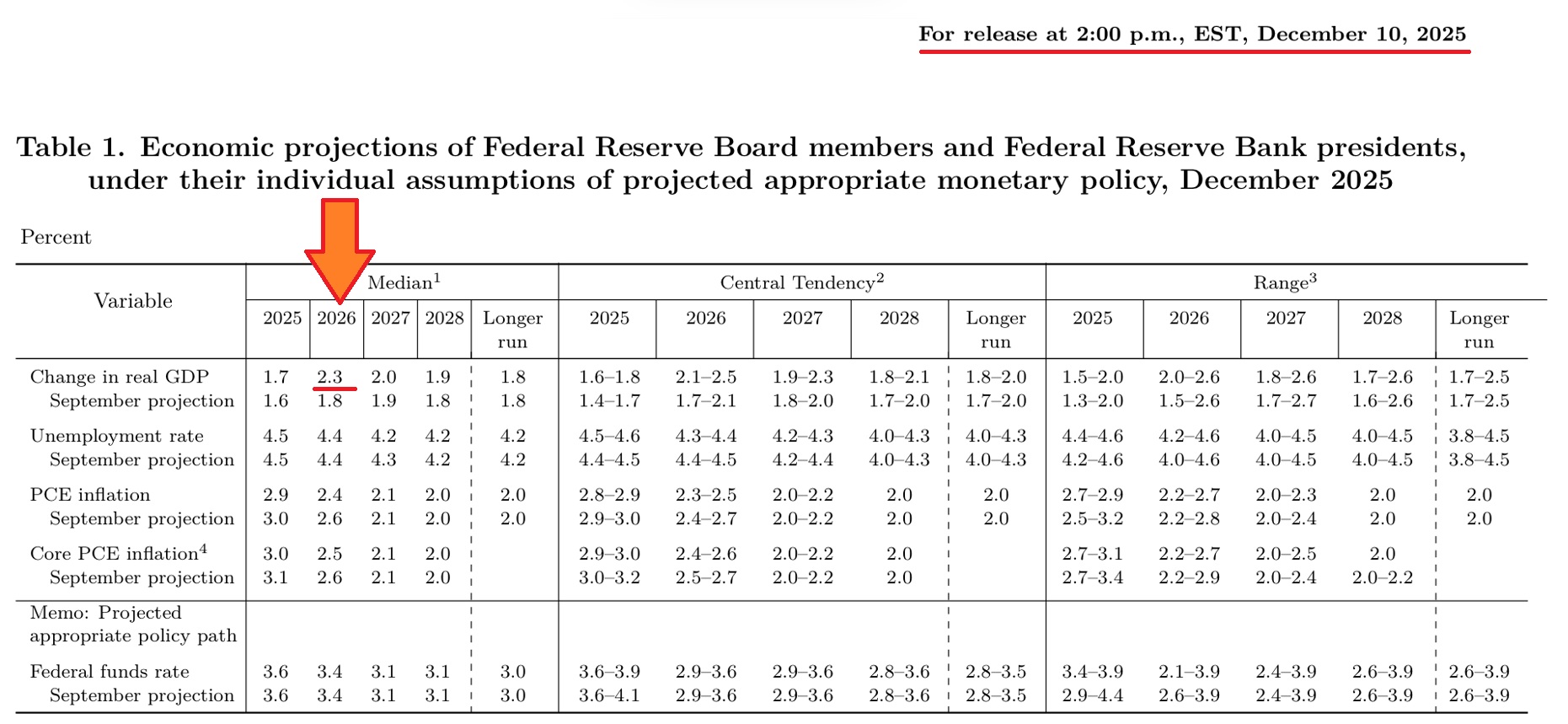

And so now we find ourselves full circle back to the topic of predictions, specifically those made by the FED. The FED lowered the ‘federal funds rate‘ — known as the FFR — earlier today. The shortest-term rate is now 3.50%. This is the lowest FFR we’ve seen in 3 years.

And yet, this cut came as the FED itself INCREASED its internal projection for 2026 GDP. See below:

Remember: The FED forecast is ‘real’ — meaning this is the growth rate after removing the effects of inflation. Thus, the ‘current dollar’ growth rate is likely well above 5.0% This is a far cry from the FED and market fears from earlier in the year.

The FED may be expecting 2.3% but I still believe GDP growth in Q4 and 2026 will be considerably stronger.

Folks, here’s your takeaway: Our economy is on a tear. AI datacenters and infrastructure growth is exploding. That spending finds its way into the greater economy, spending fuels new spending, and widespread growth is the result.

Even the FED is starting to sing from that hymnal. Believe. It’s happening.

<(| Terry Liebman |)>

{kind=link}