SHI 02.04.26 – A Shifting Tide

February 3, 2026SHI 2.18.26 — Only The Paranoid Survive

February 18, 2026

It’s been said, “Be careful what you wish for….”

Because your wish may come true. Our world has been running flat out to embrace AI and the future that it promises, only to discover all that the hype, promise, hopes and dreams of AI may not be all rainbows and unicorns.

Undeterred, Amazon, Meta, Google, and Microsoft — four of what have been termed “The Magnificent 7” or MAG7 for short — have announced 2026 plans to spend, collectively, roughly $650 billion on data centers and related technology. Shall we call them the “Money Four” or M4? Sure. And remember: This is on top of about $400 billion in the prior year. That’s more than a trillion dollars, collectively, folks.

Over-one-trillion-dollars. In just two years. From just the M4. Staggering.

Clearly, they are hoping and wishing for rainbows and unicorns. Of course, no one knows, with any precision, what those will look like when the future finally unfolds. Never before in history has so much been risked where the outcome is so uncertain, so unclear, so undefined.

“

Rainbows and Unicorns.”

Of course, the M4 would disagree with my characterization. They would likely argue demand for their cloud infrastructure far exceeds current and near future supply. And they would probably say that global AI compute demand, again, far exceeds available supply.

Businesses seem to be on board. For the first time since AI dreams covered the landscape, economic output and labor seem to be decoupling. Measured productivity might now be growing at a 5% (and increasing) rate, while labor costs remain close to flat.

This is the essential promise of AI integration, right. Massive productivity gains seem to be the goal — for the betterment of society, of course. But if this comes true … and we’ve discussed before … what’s the collateral damage?

Welcome to this week’s Steak House Index update.

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding.

The ‘real’ growth rate — the number most often touted in the mainstream media — was 4.4% in the 3rd quarter of 2025. That is a HUGE growth rate. In “current dollar” terms, US annual economic output rose to $31.098 trillion. Even more staggering: The current dollar annualized GDP growth rate was 8.3% !!!!

According to the World Bank, the world’s annual GDP expanded to over $111 trillion in 2024. Further, IMF expects global GDP to reach almost $132 trillion by 2030. The US? Various forecasts project about $37 trillion for American GDP in 2030 — I believe it could be even higher.

America’s GDP remains around 28% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

So what is the collateral damage? Who knows, right? I certainly don’t. Frankly, no one does. Some opine AI is the beginning of the end of humanity. Others believe this technology will usher in the best of times, a veritable nirvana for us all. Who knows.

But one thing I believe is this: Change is not the problem today.

The problem is the speed of change.

Think of this idea in this way. Prior generations of humans spent an entire lifetime without any real change in their lives. From birth to death, the world remained fairly constant. Probably the single largest change, which was measured over centuries, was the human move from nomad to farmer. But then came the industrial revolution and with it, change. A lot of change. Over a fairly short time, historically speaking. But even this new world after a while, seemed fairly stable, fairly consistent. Sure the carriage gave way to the car over a couple of decades, the telegraph to the telephone, electricity became a thing. But all these changes took years or even decades before they were fully embraced by society.

Then came the internet. And now AI. And things are changing fast. Too fast, frankly, for anyone to grasp the implications.

“Disruption Dislocation” could be Joseph Schumpeter’s next book — well, if he wasn’t dead. You’ll remember Schumpeter is the father of “Creative Destruction” — the economic theory that capitalism only advances thru waves of innovation, each of which destroys the prior and replaces it with the new. Schumpeter believed the cycle of innovation leading to disequilibrium leading to temporary monopolies and finally societal diffusion, repeats relentlessly.

Sure. But never at the speed we’re experiencing today. Disruption seems to be happening daily. Existing patterns — technological, economic, demographic, or institutional — seem to shatter continuously. And the dislocation follows. People, capital, and systems get rocked, without the time to adapt or adjust. “Disruption dislocation” describes the gap between a shock and the system’s ability to absorb it.

What’s my point here? Just this: Be careful out there. When making important decisions, consider rethinking certainly with a dose of uncertainty. Whatever you were sure of yesterday, you cannot be sure about tomorrow. When measuring future risk, figure whatever risk levels you perceive are incorrect: The risks are probably higher in the coming months or years. Volatility will only increase in coming days. Question your decisions carefully. The ground under our feet is far less stable today.

We don’t know the impacts AI will have on each of us or society as a whole. Hopefully it will be more utopian than dystopian. Regardless, however, we’re all on the roller coaster. So hold on tight.

Ready for a glass of wine and a beautifully grilled steak?

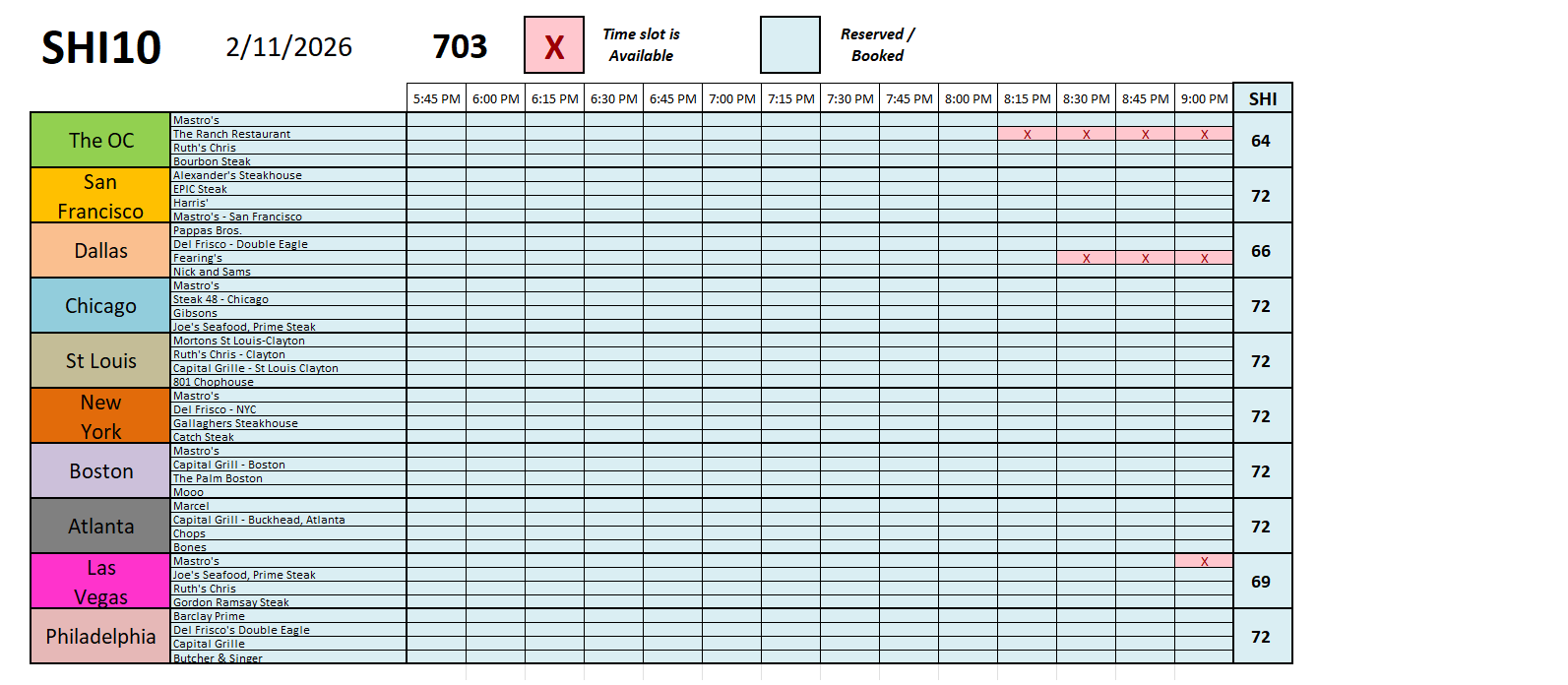

Great. However, you won’t get either at most of our 40 opulent steakhouses across the nation. They’re almost fully booked this weekend. Check this out.

Damn. Is this accurate? Yep. I double checked it. There were 8 remaining time slots when I ran the SHI40 this morning at 11AM. That’s right: Only 8. This has never happened before.

What’s going on? Is this an AI thing? Are AI robots taking all our reservations?

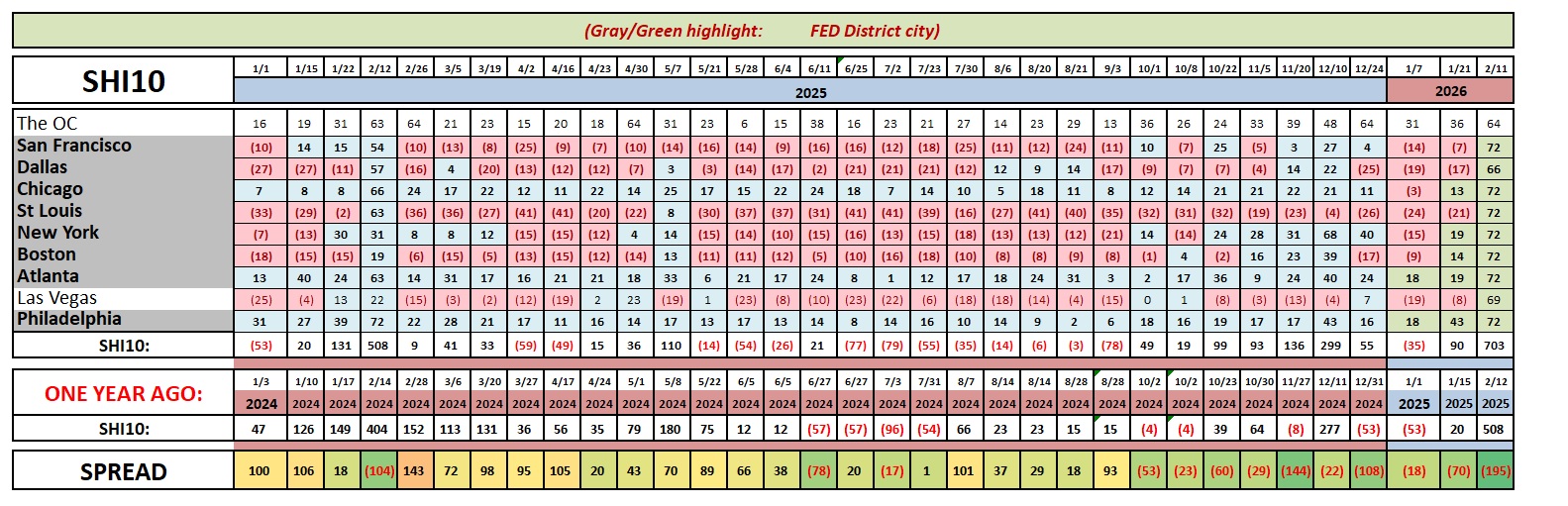

Nope. It turns out that this Saturday is February 14th — Valentines Day. It’s the day of love, folks. And all those lovers, country wide, are opening their hearts and wallets to spend big bucks and profess their love this weekend. Beautifully, this is about un-AI as it gets. Here’s the longer term chart:

We haven’t seen a week where each of the 10 SHI cities were “in the black” in quite a while. Unsurprising, the last time was the SHI40 on 2/12/25. On that day, the SHI40 clocked in at 508 — a super high reading. But this year, our young lovers have gone over the top. The steakhouses are booked. Can I suggest Costco? They have both excellent wines and beautiful steaks. Yes, it’s a do-it-your-self kind of thing, but I think that’s as good as you’ll do this weekend. Unless you have already booked your expensive eatery. 🙂

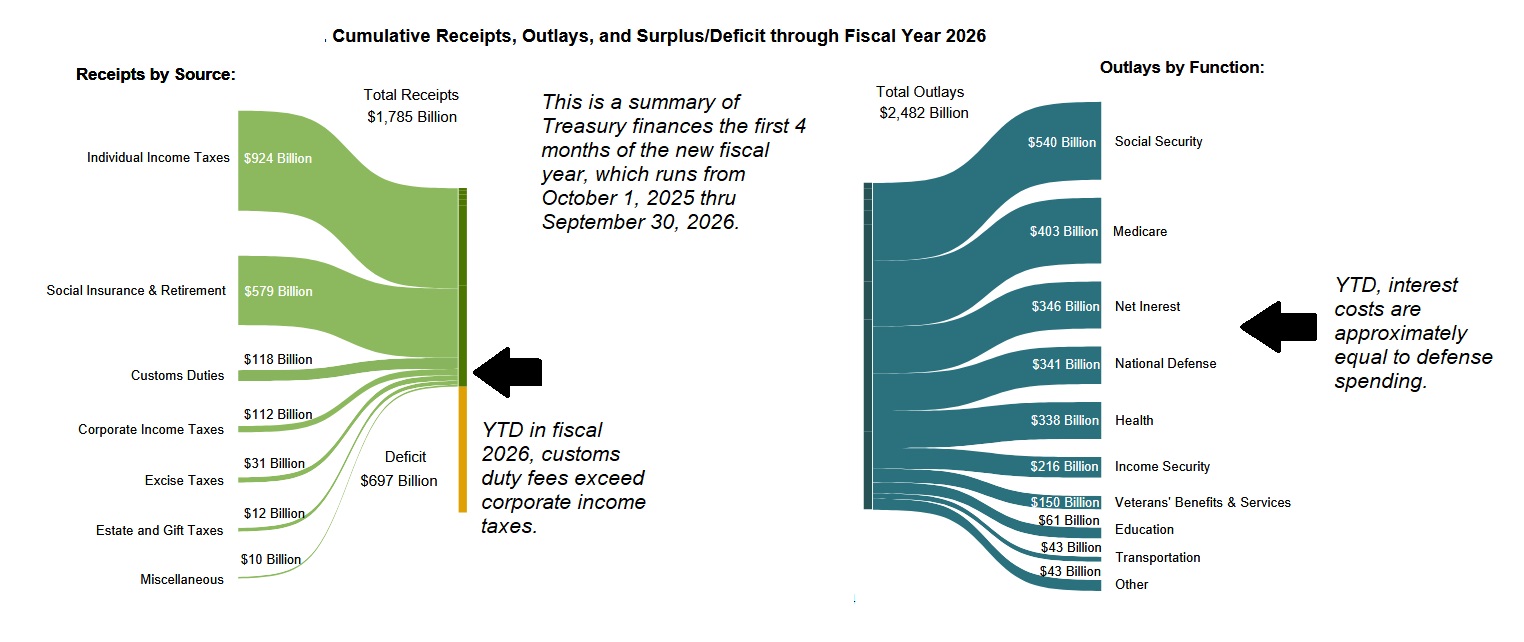

I’ll finish with this: Every month, the US Treasury publishes the “Monthly Treasury Statement,” a 30- or 40-page document that both summarizes the details the financial goings-on over at the Treasury Department. The most recent report was published this morning, covering exactly 1/3 of the current fiscal year. In other words, this data covers a four month period, beginning on October 1, 2025 and ending on January 31, 2026.

As always, setting politics aside since this is an economic blog, I wanted to point out a couple of items I personally found interesting. Before I do, however, you might notice that the “deficit” for these first 4-months was $697 billion. How does this compare to the first 4-months of the prior fiscal year? Better. This same time frame last fiscal year, $838 billion — $141 billion higher.

Interesing Item #1: Tariffs collections are way up. They are trending near $30 billion a month. YTD in fiscal 2026 they have totaled $118 billion. That’s interesting … but even more interesting, to my eyes anyway, is the fact that customs duties year to date exceed corporate income tax collections. Wow.

Interesing Item #2: Interest payments on Treasury debt remains elevated. Net interest expense YTD was $346 billion. And that number exceeded spending on our national defense by $5 billion. Wow.

Happy Valentines Day all! Enjoy.

< Terry Liebman >