SHI 2.18.26 — Only The Paranoid Survive

SHI 2.11.26 — Disruption Dislocation

February 11, 2026

SHI 2.25.25 – Horseshoes and Hand Grenades

February 26, 2026

In 1996, Intel CEO, Andy Grove published a manifesto for the digital age.

The book was titled “Only the Paranoid Survive.” In the book, Grove argued that in the life of a business, there is a moment-in-time when the underlying fundamentals of that business change forever. If the business fails to recognize that strategic moment, or fails to “act” at the right time, Grove would argue that moment-in-time is the beginning of the end of that business.

“

The ‘Valley of Death.’“

“

The ‘Valley of Death.’“

Grove told us that if the company acts too early, they waste resources. Too late? You’re dead — out of business, or, at the minimum, severely financially compromised. And the “Valley of Death” is the turbulent and chaotic period between transitioning from the “old way” to the new. Hmmm … this sounds a lot like that guy Joseph Schumpeter again, right?

Remember creative destruction? 🙂

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. But is the US economy expanding or contracting?

Expanding … according the ‘advanced’ reading just released by the BEA, Q3, 2024 GDP grew — in ‘current-dollar‘ terms — at the annual rate of 4.7%.

The ‘real’ growth rate — the number most often touted in the mainstream media — was 2.8%. In current dollar terms, US annual economic output rose to $29.35 trillion.

According to the IMF, the world’s annual GDP expanded to over $105 trillion in 2023. Further, IMF expects global GDP to reach almost $135 trillion by 2028 — an increase of more than 28% in just 5 years.

America’s GDP remains around 25% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Recently, I’ve been trying to wrap my mind around a few financial and economic puzzles floating around my brain.

My first puzzle: Why, seemingly all of a sudden, are the “big tech” companies spending trillions on the AI infrastructure build-out? Perhaps “all of a sudden” is a bit hyperbolic — after all, this is a several-years-long trend — but it feels that way to me. It feels a bit panicky. The financial markets — essentially a collection of millions of very smart investors and algorithms around the world — are telling the leaders of these companies “NO! Stop spending!” These millions of investors seem to believe those companies are torching money without a discernible purpose. But the mega-tech spending continues unabated.

The Second: ‘Operating efficiency’ — and ultimately, a lower operating cost framework — seems to be the intended goal and result of AI implementation in the myriad of S&P500 businesses employing those tools today. Thru this lens, many have forecasted tectonic-level layoffs across all industries — some industries, many opine, are ripe for extinction.

Focusing locally for a moment, the US labor force measures about 170 million folks, more or less. Davron, an executive search and placement firm, forecasts that 10 million jobs could be lost due to full automation by 2030. And up to 30% of U.S. jobs may have substantial portions of their tasks automated. Globally, they opine roughly 85 million jobs may be displaced. Forecasts by Goldman Saks and McKinsey are similar.

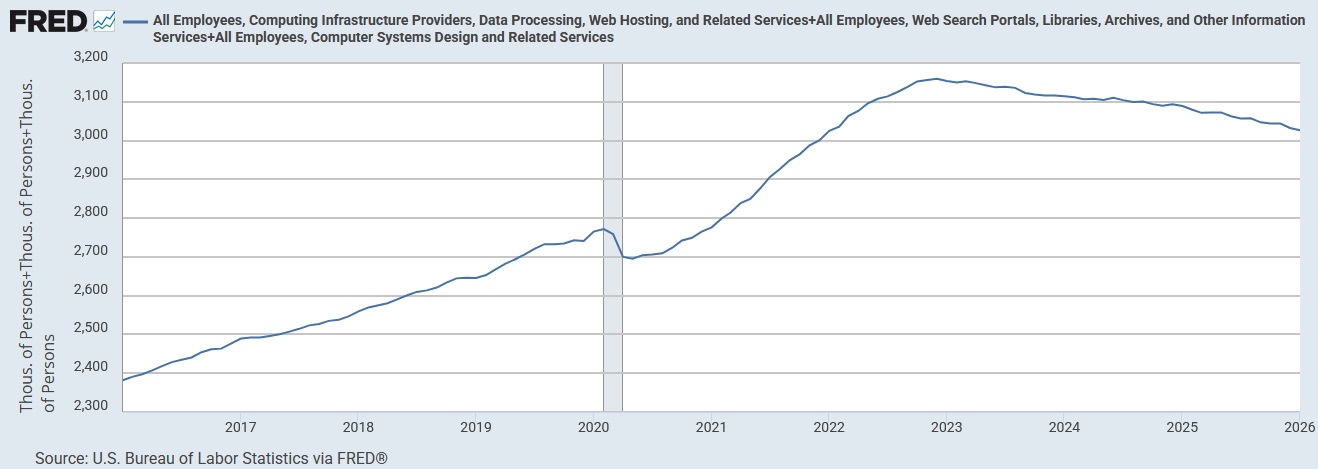

Perhaps the proverbial canary in the coal mine, the data center at FRED, the St Louis Federal Reserve, reports employment is already meaningfully lower in:

Computing Infrastructure Providers, Data Processing, Web Hosting, and Related Services+All Employees, Web Search Portals, Libraries, Archives, and Other Information Services+All Employees, Computer Systems Design and Related Services

After peaking in December of 2022, this employment segment has shrunk ever since. Here’s the graph of employment changes in this space during the past 10-years:

The decline near the beginning of 2023 is apparent. For context, recall that total employment in the US continues to move up and to the right. Clearly, within this technical space, fewer people are employed today than just a few years ago. Is this change the result of AI, or just improving efficiency? On its face it’s hard to tell. Clearly, jobs are more scarce, but the cause is harder to pinpoint.

Widening the lens a bit, the mental gymnastics of reconciling both of my “puzzles” with Andy Grove’s foundational premise — adapt or die — makes me wonder what’s really happening here today? Is AI an existential threat to the existing human labor force across the globe? Are the biggest, most successful companies in the history of capitalism simply torching capital at an unprecedented rate? Or is something else at work here in both cases? Many today seem to believe that AI is going to “eat everything” in its path. In my first puzzle above, AI is eating money. Voraciously. Seemingly without end. In the second, AI is eating jobs in the name of operating efficiency.

For the moment, let’s step out of the anxiety filled narratives above and consider another possible explanation for both, simultaneously.

Could the “truth” be more nuanced than that? What if this precise moment is that moment in time to act according to Grove? What if now is the time when the tech companies, collectively, must increase AI spending or face extinction? What if all this spending actually does end up generating a massive ROI? And what if AI doesn’t actually eat jobs but preserves them, to a great extent, and results in increased employee compensation? Is there a world where this might actually be the outcome?

Perhaps. Consider this.

Last week, the Harvard Business Review published an article titled “AI Doesn’t Reduce Work — It Intensifies It.”

The two authors spent eight months studying a 200-person tech company to see how generative AI changed work habits. What they discovered might surprise you: AI doesn’t create “slack” or free time — it creates a feedback loop of job intensification. They claim AI use created “attention fragmentation” because workers began using multiple AI chats concurrently. Hmmm … yeah, I see that. I do that. And they highlight the loss of boundaries — they observed employees “chatting” with their AI buddies during lunch, at meetings and at home after work hours. Yeah, I can see that too. Guilty as charged. 🙂

Here’s where my mind begins to diverge from the findings of this paper: The simple fact is that the proliferation of AI chat-bots isn’t really what I’m talking about above. Sure, I agree that these friendly, helpful, and brilliant chat-bots are amazing as is, but this is not the end-goal. We all know this, so this isn’t what puzzles me. Nor do I think it explains why the big tech companies are spending money like they are in a race for digital supremacy.

So what is the end game? No one can possibly know yet. However, the “next chapter” — the move that explains the massive investment — is likely to be agents. This isn’t new, of course. The buzz around Agentic AI is everywhere. I won’t talk about that here. But I will talk about the economics. Perhaps like me, you’ve been thinking, “Wow, it will be really cool to have an AI agent book my next trip to NYC. With one click I can tell the agent when I want to go, how I want to get there, where I want to stay, do, experience, or consider when there; and, finally, when and how I want to get home.” Because that would be quite amazing.

Not for my travel agent, perhaps, but amazing for me. But hold on a minute, let’s think about the economics. Right now, I can call my travel agent and ask him or her to do this for me. And it doesn’t cost me one cent today — at least not directly.

But will an AI agent do this work for me at no cost? Will this, too, be “free” to me? Probably not. While chatting with an AI-bot is relatively “cheap” in terms of computing power — perhaps even free today — I understand that Agentic AI—where the AI doesn’t just talk, but actually acts on your behalf—is a massive leap in complexity and cost.

As the AI industry transforms from “Chatbots that talk” to “Agents that think and do” the equation begins to change. Today’s “free” experience is likely to become a “premium” experience as AI gains agency. Consider these thoughts.

When you ask your AI-bot a question, it runs a single “inference” (a one-shot calculation) to give you an answer. An Agentic AI, however, has to plan, act, observe, and correct. And make many iterations. My Gemini AI chatbot tells me that the ‘standard AI’ request costs roughly $0.001 to $0.02 per request. Contrast this with an Agentic AI request: One request involves dozens of internal loops, multiple API calls to other tools, and constant “reasoning” steps. This cost is far higher: $0.10 to $5.00 per workflow. Because the complexity of the agentic system causes it to run exponentially more compute cycles than a simple chat for a single “outcome”.

So as we shift from a conversation to an “outcome,” the pricing model will change dramatically. And as the complexity of agentic requests increases, so will the cost of that service. As it should, right? Today, I enjoy the “subsidized” era of AI chatting. And perhaps “free” AI will remain for basic search and chat. But “Agentic” AI—the kind that actually handles your errands or job tasks—will likely be billed as a professional utility or a “digital employee”.

I suggested to my Gemini chatbot this feels much like a drug dealer giving away “free samples” to get us hooked. It agreed with this assessment. He called it the “Freemium-to-Agentic” pipeline — a classic ‘hook-and-scale’ strategy. “Free chat” is expected to be used to embed AI into nearly 80% of workplace applications by 2026, making it a “must-have” for employees. At the same time, our human interactions help the models learn. So there’s a bit of quid pro quo here.

But Agentic AI is vastly different: A single agentic system can consume hundreds or thousands of times more compute than a human user because every decision triggers a chain of “reasoning” calls. It is clear to me: The industry is betting that once you “get hooked” on an agent handling your complex tasks, you’ll be willing to pay for it as a “digital co-worker” rather than a simple toy.

Let’s assume they are correct. We are all willing to pay for an agent to handle personal tasks for us. Like making dinner reservations. Or planning and booking my next New York City trip. These tasks are relatively simple. Over time, our requests are sure to become more complex. And as they do, the amount we are willing to pay will most assuredly increase, right? Whether the complex task is personal or business, the more important an accurate and expeditious outcome becomes, the greater the cost we’re willing to endure. And as the AI agent performs better and better, I’m likely to rely on it more an more. Instead of once or twice a day, the AI agent might actually become my digital assistant, executing task after task, all day long. Perhaps even all night long, too.

Thru this lens, I can envision a future time when I might be paying quite a bit to employ my digital assistant. And when that happens, when the cost becomes substantial, I will inevitably compare the cost of my digital assistant to that of a human assistant. Might there become a time when my AI agent costs even more than a human assistant or employee? Sure, that could happen. And it probably will. In this way, a competition will develop between a human armed with personal AI tools and skills vs. my AI agent. The “cost/benefit” analysis will become front and center. Sometimes the AI agent efficacy will outweigh that of a human. Sometimes the human will “win” and get the job.

Could this be the future? Again, perhaps. Gemini suggests that a “Business Operator” running a custom autonomous system that handles my emails, invoices and scheduling 24/7 could cost me as much as $3,000 a month today. Hmmm …. fascinating. This is a very different mindset and framework. Perhaps like me, you’ve been thinking its impossible for the mega-tech companies to realized an ROI on a trillion dollars of spend on AI compute facilities. Perhaps like me, this puzzle has been bouncing around in your brain, causing you to wonder if Meta and Google have lost their marbles. Clearly, this has been the conclusion of millions of investors in the stock markets. But there is a value case here.

Are we now Grove’s “Valley of Death?” Is this the precise moment in time when Andy Grove would suggest Google and Meta adapt or die? That’s their challenge, right? Deciding that this is the moment-in-time is far easier in retrospect. In the moment, it’s much harder. It’s not so easy when you are living in the valley. 🙂

As the AI companies roll out new tools and uses, we need to consider this alternative future, one where AI agents cost a lot of money. Andy Grove would probably suggest that an AI agent providing a 10X output improvement, costing $3,000 a month, is superior to its human counterpart. But does that calculation change as the AI agent cost increases appreciably? Of course it does. It’s not hard to imagine a future where an AI agent demands more high-cost inputs and resources like “high-frequency AI models”, a multi-modality framework, more high-frequency systems, more memory, etc. As these costs escalate, a human alternative might start looking pretty good. Especially when you consider that even now, humans often achieve higher “success rates” because they can handle nuance that AI agents often miss or “hallucinate”. Yes, that’s a thing. Hallucinations happen.

In the final analysis, the future is probably far more nuanced than you, me or the financial markets are considering today. Back in the “Dot-Com” era, the greatest fear was that everything was going to move to the internet. It was generally believed that retail “bricks and mortar” would completely disappear, as everyone shopped on-line. Many expected that shopping centers and Walmart would become ghost towns as consumers stayed home and ordered everything they needed on-line.

Well, that didn’t happen. The internet touched and changed everything, but shopping centers remain and many are thriving. And Walmart’s stock price has never been higher. It’s entirely possible that instead of a “mass replacement” of human labor, we are seeing a shift where AI agents will become more and more expensive to use; and, if this becomes the future reality, they might be more cost effective as instruments rather than co-workers.

At present, the most profitable companies aren’t the ones that fired everyone to use robots; they are the ones using AI to make their existing humans 10x more productive at a fraction of the cost of full autonomy. This dynamic will continue to evolve as we discover just how much Google, Meta, Amazon, et. al. plan to charge us all for the use of their AI agents and compute. The more productive these products prove to be, the more they can — and will — charge. And what comes after this next chapter? The evolution is swift. No one can possibly know today. All we can know for certain is that the future is likely very different than we expect it to be: As the complexity of an AI agent use increases, its cost could easily eventually hits a ceiling where it is cheaper to just have a human manage the AI.

This digital reality, of course, is precisely what Andy Grove tried to articulate in his book. And this entire episode is precisely what Joseph Schlumpeter postulated in his creative destruction theories. Things change. The old gives way to the new. We all know that. And the rate of change is accelerating. We know that too. But what we don’t know is precisely how they WILL change in the months and years to come.

That is the true unknown. And that creates fear and anxiety — but also opportunity. Especially if you figure it out before your competitor. Good luck! 🙂

Let’s head to the steakhouses.

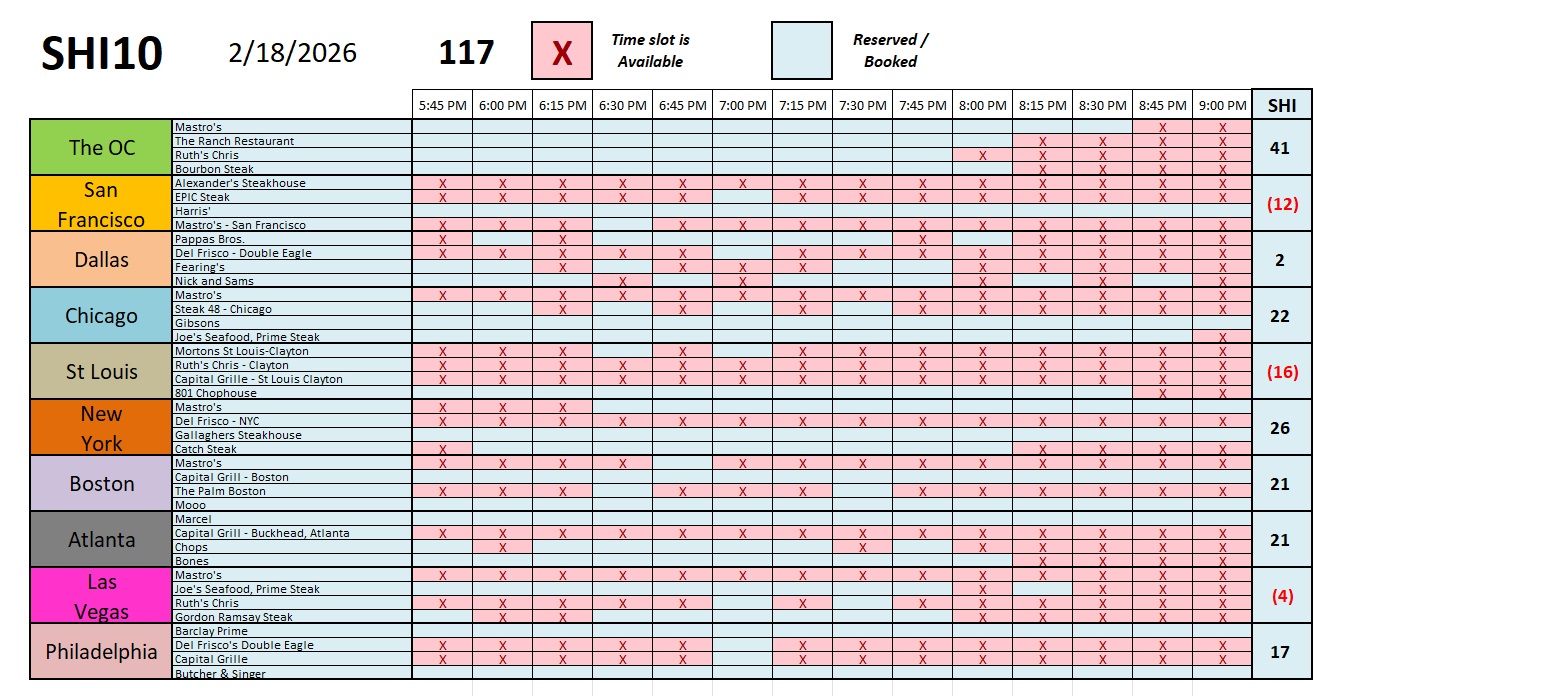

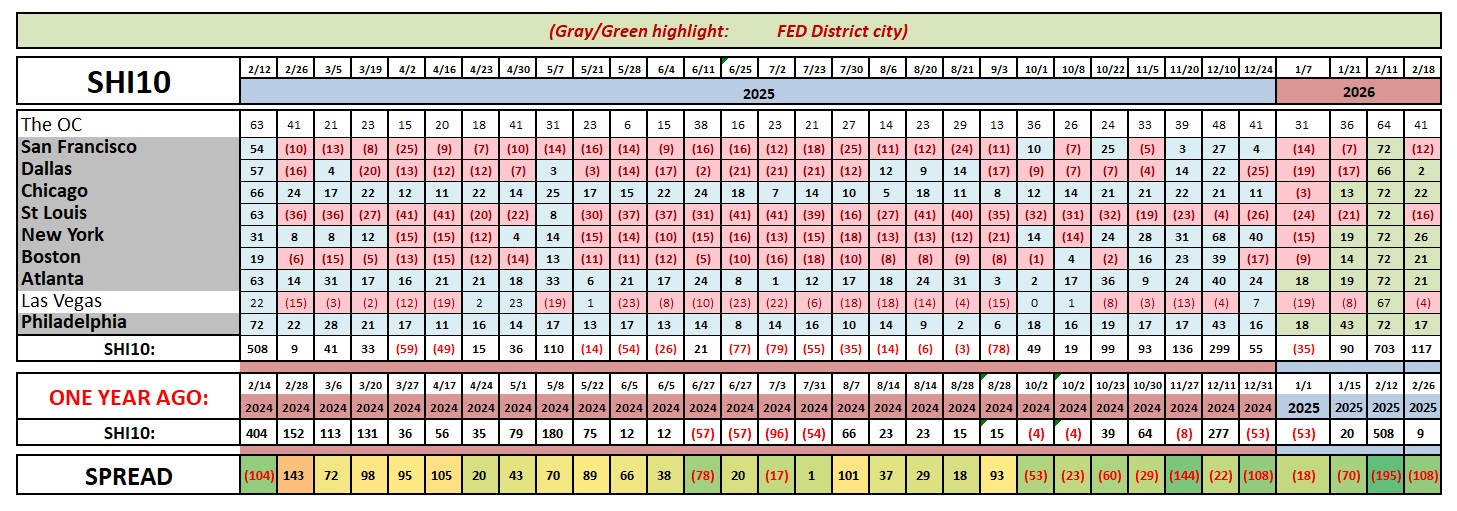

Well, one thing is clear: This Saturday is not Valentines Day! 🙂

No, it’s another “normal” Saturday, with an SHI40 reading that is very consistent with prior, non-holiday weekends. Take a look:

The SHI remains impressively consistent, suggesting our economy remains strong and resilient.

In two days, this Friday at 5:30 am California time, the Q4, 2025 GDP number will be released by the BEA. The Atlanta FED ‘GDPnow’ forecast still expects a 3.60% number as of today. And remember, a 3.60% ‘real’ growth rate translates to about a 6.00% ‘current dollar’ growth rate. Both would be impressive numbers as they follow a stellar 4.40% Q3 growth ‘real’ number. I’ll be watching … and of course, I’ll report back.

< Terry Liebman >

{kind=link}