SHI 3.24.26 – Unknown Unknowns

SHI 3.11.26 — A Financial Neutron Bomb?

March 11, 2026

Mark Twain famously said:

“It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.”

Bad information will get you in trouble. So we have a problem: As ubiquitous and instantaneous our data feeds are today, they are wildly inconsistent. I attribute that to a simple fact: Most data we get in our inbox, from a mainstream media source, or social media feed is typically incomplete at best, and completely inaccurate at worst.

“

Data check everything.‘“

“

Data check everything.‘“

That’s why I data check everything. Often times, more than once. Because data accuracy is critical when making important decisions.

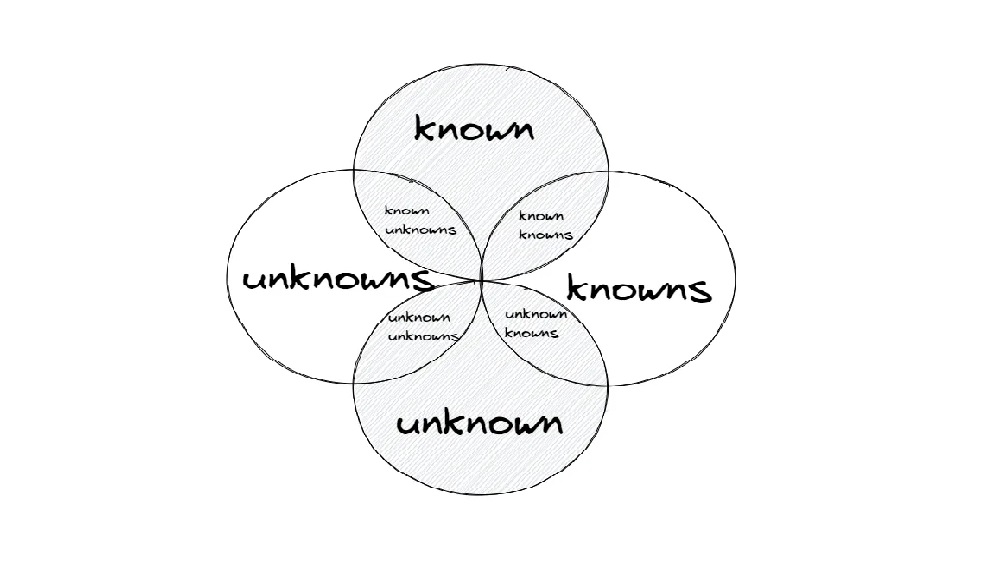

Donald Rumsfeld, the US Defense Secretary under Ford, once suggested, “There are known-knowns… there are known-unknowns; that is to say we know there are some things we do not know. But there are also unknown-unknowns—the ones we don’t know we don’t know.”

“Unknown-unknowns.” Yeah, that’s bad. What a great way to frame the issue. Rumsfeld felt real danger lies in the things we don’t know we’re missing. When an unknown-unknown pops up, we are completely surprised as the issue wasn’t even on our radar. I completely agree: Whether we’re talking war or economics, it’s a serious problem.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. But is the US economy expanding or contracting?

Expanding … according the ‘advanced’ reading just released by the BEA, Q4, 2025 GDP grew — in ‘current-dollar‘ terms — at the annual rate of 5.1%.

The ‘real’ growth rate — the number most often touted in the mainstream media — was 1.40%. In current dollar terms, 2025 US annual economic output reached almost $31.50 trillion.

According to the IMF, the world’s annual GDP expanded to over $115 trillion in 2024. Further, IMF expects global GDP to reach almost $135 trillion by 2028 — an increase of more than 28% in just 5 years.

America’s GDP remains around 25% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

I do my best to “keep a finger on the pulse” of global goings-on. I want to assess how current events may or may not impact economic conditions. And lately, we all know, there have been plenty of current events to keep track of. But as turbulent as conditions feel today … a couple of things have really surprised me in the past few days. For me, they fit Rumfeld’s definition of “unknown unknowns.” Face it: It’s impossible for me to keep that proverbial finger on that proverbial pulse if I can’t even find the pulse.

So I dug in deeper to figure it out.

For example, did you know that the Secretary General of NATO spoke on ‘Meet the Press’ on Sunday morning. That’s right, Mark Rutte himself was interviewed on Meet the Press. On that show, he announced that a coalition led by the UAE, Bahrain, and the UK, 22 nations in total had been established to focus on reopening the Straight of Hormuz. Wow. Until I personally saw him speak, I had no idea this was happening. Further, on that same Sunday, the United Nations Secretary-General delivered an address and confirmed there exists a coordinated international effort to break the blockade of Hormuz. Collectively, they declared they are aligned and ready to “secure maritime navigation” in the Straight of Hormuz by any means required.

I have seen nothing on this topic in the mainstream media. Have you?

Interestingly enough, seemingly in response to the UN and NATO 22-nation coalition, this morning Iran has “formally notified” the UN and the International Maritime Organization that Iran will allow “non-hostile” vessels to pass. Of course, there are numerous conditions and vague definitions; and, of course, even with this formal notification in hand, and even if ships are allowed to pass, Iran remains in violation of Maritime law. But – hey – it’s a start! 🙂

Here’s my hope: This is the “off-ramp” for the heated US/Israeli military campaign in Iran. This international coalition will take on the task of opening the Straight. Alternatively, the ‘threat’ of the 22-nation flotilla moving into the region motivates Iran to come to the negotiating table with demands considered reasonable under international standards. Fingers crossed.

Here’s another of my unknown-unknowns: Did you know that China has built an operational GPS system that is functionally superior to the US GPS system? I certainly didn’t. Called “Beidou-3”, the Chinese system uses a satellite constellation of 56, versus the US system of 31. Its accuracy is down to 10cm – about 4 inches. I had no idea.

Did you know that in 2025 Iran learned they could no longer rely on the US GPS system to guide their missiles? Their missile attacks on Israel were ineffective due to jamming and “spoofing” within the US GPS system. So in March of 2026 – meaning this month – Iran switched. Iranian missile guidance now uses the Chinese system. Apparently, their missile guidance on Beidou-3 cannot be jammed or “spoofed” by the US or Israel. I had no idea.

My point is this: Unknown-unknowns are very, very problematic. Whether in war, economics and finance, facts and knowledge are important.

A couple weeks ago, I addressed the unknown-unknowns within the private credit space. By my efforts, I believe some of those unknown-unknowns moved closer to known-knowns. That outcome was important to me. I hope you found the write-up valuable. That’s the essential purpose of this blog and why I do the research in support. Yes, admittedly I’m a control freak. I don’t like unknowns. I never have. So I investigate and, hopefully, uncover facts where only ‘unknowns’ existed before.

As this Iran conflict began, the number of unknown unknowns grew. In this environment, fear and anxiety is difficult to constrain. Oil prices shot straight up. Brent Crude temporarily reached an intra-day peak just under $120 per barrel. Of course, stock prices fell. A lot. And Treasuries sold off, and interest rates increased, as spiking oil prices triggered growing inflation fears.

And recession fears grew greater, too.

Higher oil prices can trigger a recession. Economists look at the “recession risk of oil” when they discuss a thing called the “Energy Expenditure Share of GDP.” At or above this percentage, theory has it, the US economy can tip into recession.

That number is a tipping point. Experts today believe that percentage is 5%. Of course, the per-barrel price would have to stay there for a protracted period of time. When the amount spent on oil exceeds 5% of US GDP, which today is about $30 trillion, experts believe a recession will begin within a quarter or two.

The US consumes 20 million barrels of oil daily. Today, that 5% threshold would be crossed at just above $200 per barrel. Were the price to lift that high, the longer the barrel price stayed there, the greater the adverse economic impact.

That number seems quite high, right? It is. Fortunately.

Consider this: ‘Oil intensity’ is a term defined as the amount of oil needed to create or generate $1,000 of GDP. In 1973, that number was about $1 of oil per each $1,000 of GDP. Today, for many reasons including significant efficiency gains, it’s closer to 32 cents – about a 60% reduction. That’s why the US economy can tolerate a much higher price today without tipping into recession.

Of course, we all know skyrocketing oil prices can tip our economy into recession. This was a known. What was unknown to me was how high and how long. Now I know: the barrel price would have to rise above $200 per barrel and for more than 4 months to trigger a recession. That’s worth knowning, right?

The good news, in my opinion, is the UN and NATO 22-nation coalition. Hopefully, they will get started early next week and global oil will flow smoothly again.

Steakhouses?

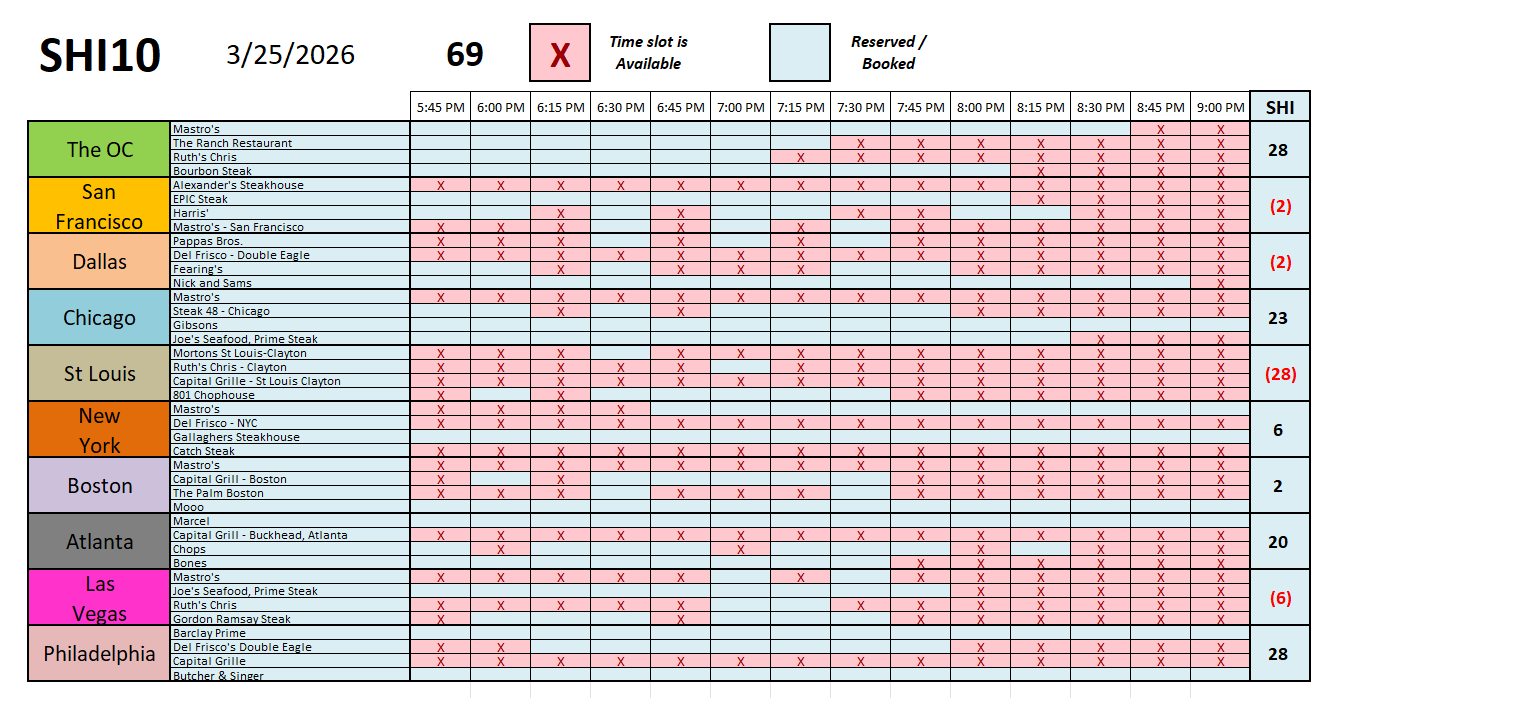

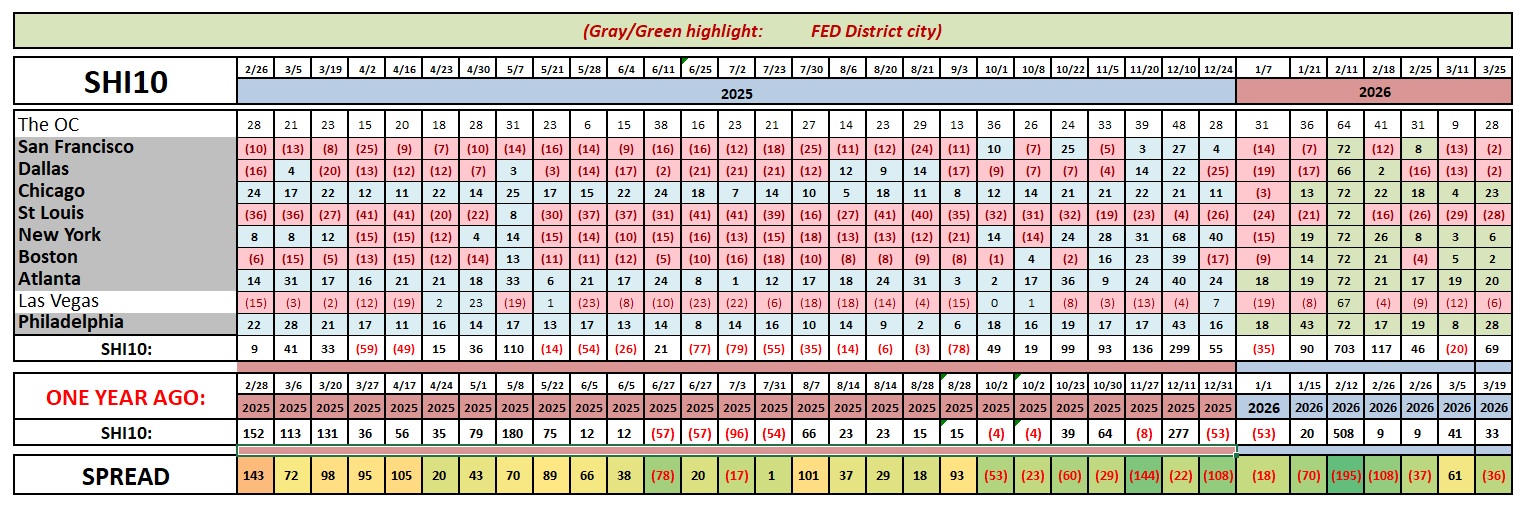

I was pleasantly surprised by today’s SHI10 numbers. With all the economic, financial and “war” uncertainty out there, I thought the numbers would be weak. Nope, demand for expensive eateries remains strong for this coming Saturday. Almost every one of our 10 SHI cities saw demand increases this week. Surprising. Take a look.

My take-away: The SHI is telling us the US economy remains robust.

Permit me to move away from the ‘2X-unknowns’ to a few known-unknowns that had me a bit puzzled. I’ll finish today’s diatribe with some brief comments on Private Credit, the corporate bond market, the most recent ‘Productivity’ numbers, and Q4 GDP.

Private Credit: On his ‘Money Stuff’ podcast, Matt Levine also did a deep dive into private credit. His podcast is worth a listen. Anyway, he comes at the issue from a different angle. His macro is that the debt assets owned by entire industry, in the aggregate, are worth less than before this current “confidence crisis”. At the minimum, he believes the loans to SaaS software companies aren’t worth what they were before.

Summarizing his take, he believes that this entire loan segment is under stress. His belief: The market stress has created an imbalance which would instantly show up in a traditional, liquid market fund as an immediate reduction in the value of these assets. But this has not happened since many private credit funds are not liquid. Further, he believes that as a private credit fund’s value is reflected in a thing called the ‘Net Asset Value’ or NAV, these large institutional, private, non-liquid funds should reflect a loss of value as a reduction to NAV carried on their books. So if the NAV was $1.00 per share before the crisis, it is something less today. Maybe 90 cents or 85 cents, or something like that. It’s an interesting take, but I don’t agree. I could say more, but I’ll leave it there. Listen to his podcast if you want to learn more and get another perspective. It’s worth your time.

Corporate Bonds: According to the NY FED “Corporate Bond Market Distress Index” for March, 2026, the BEST quality bonds – known as ‘Investment Grade’ or IG – are under increased stress! Are they at risk too? IG bonds are theoretically the safest corporate bonds you can buy. Yet right now, they are under more “stress” than the junk segment known as ‘high yield’ bonds. This surprised me. So I dug in a bit more.

It turns out that the stress is not due to anxiety over repayment but amount. Recent estimates from Apollo suggest that IG bond issuance during 2026 will be nearly $14 trillion!

Before you get too excited, know that $12 trillion of that is US Treasury issuance. But about $2 trillion is new corporate issuance. And that’s a big number. Again, quality is not the concern. Quantity is. The sheer amount of investment grade bonds seeking buyers is the source of the concern.

Productivity: Q4 productivity was only 1.8%. Again, this surprised me. In Q3, productivity in the US economy increased by 5.2%. What happened? Great question. See my next bullet point.

Q4 GDP: In the ‘second estimate,’ Q4 GDP was downgraded to just 0.7%. That reduction, in fact, was the primary driver behind the productivity decline. But in an economy that is (well, was, before the US decided to bomb Iran back to the Stone Age) booming, why did Q4 GDP come in so weak? One word: Shutdown. The 43-day US government shutdown in Q4, 2025, as it turns out, was exceptionally bad for GDP. No true surprise here. And keep in mind that this is the ‘real’ GDP number. Even with the shutdown, ‘nominal’ or current-dollar GDP still grew at the staggering annualized rate of 4.5%. That’s still red-hot, my friends.

I’ll end here. Thanks.

< Terry Liebman >