SHI 7.23.25 I’m Back!

SHI 7.2.25 – Washed Out?

July 3, 2025

SHI 7.30.25 – Betting the Balance Sheet

July 31, 2025

I’m back!

I apologize for my absence – summer vacations, you know! Those grandkids keep me hopping!

Unsurprisingly, there was no shortage of interesting news while I was gone. One of the more fascinating forecasts, from a demographic perspective, was the United Nations release of their report entitled WORLD POPULATION PROSPECTS 2024. Yes, this is a demographic piece, but it is chock full of economic and financial implications for the world. Consider the graphic below, courtesy of ‘Our World in Data’, using data sourced from the 2022 and 2024 UN reports.

The 2024 line is blue. Interestingly, in the bottom three (3) images above, just two years later the blue line has diverged significantly. Sure, 2080 is a long way off. But these forecasts are quite sobering.

In the near term, these demographic trends are not concerning – from an economic viewpoint. After all, populations continue to rise. A 25% population increase should keep consumer consumption strong in the US and the world for years to come. As consumer spending and consumption comprises about 70% of US GDP, this is an important point.

But our kids and grandkids should probably be a bit more concerned. A declining population may make the freeways and airports easier to navigate, but it won’t help American GDP growth, housing values, or economics overall. In fact, a declining population would be extremely detrimental to most economic outcomes.

Which is why I was puzzled by a recent Bloomberg article titled “US Tariffs Are Changing Europe’s Approach to Chinese Investment.” Does China even pay attention to demographic trends? Europe’s population is in clear decline. Why in the world would China be making long-term, “high-value” investments Europe? This seems like a bone-head moved to me:

Slovakia and Hungary are two countries where China plans to expand their investment footprint. Why? Again, this seems downright stupid. A falling population must adversely impact investment returns. This is not a complex concept. But clearly, no one in China asked me for my opinion.

Moving on. Bloomberg calls it “depopulation.” In fact, absence an increase in global birth rates, Bloomberg suggests that “simple math dictates that the population eventually falls to zero.” Zero? That’s quite a forecast.

My point is this: Things change. Constantly. Proving that point, consider this new development:

“

The GENIUS Act was signed into law.“

“

The GENIUS Act was signed into law.“

About 50 years ago, a Stanford biologist wrote and published a best-seller titled “The Population Bomb.” The book embraced Malthusian theories, warning of mass starvation and societal collapse due to overpopulation. To be clear, population certainly did explode when we compared today’s numbers to 1968: Population 3.5 billion. However, while about 1/3 of the world’s population was considered “undernourished” in 1968, only 9% of the world’s population faces hunger today. Clearly, the forecaster was wrong on this point. By comparison, that is a meaningful societal improvement.

A recently published book titled “After the Spike” by Spears and Geruso projects the diametric opposite – a population collapse – but with equally dire outcomes.

Will their forecast be equally inaccurate in the decades to come? Probably. Because things will change. Perhaps human lifespans will double. Or maybe Elon Musk will inspire others to have super-sized families? 🙂

Who knows.

But for today, let’s move on to something that is changing much quicker. The federal GENIUS Act was signed into law on July 18th. Just 15 years after Laszlo Hanyecz spent 10,000 bitcoin (BTC) to buy a $41 pizza in May of 2010, America now has a brand new, crypto-currency law entitled “Guiding and Establishing National Innovation for U.S. Stablecoins Act” which is designed to do precisely that: Wholly embrace change in the crypto-world and establish the United States as the center of that world. And that, my friends, is truly revolutionary.

But what does this mean for you and me? Ahhh yes, that’s the right question.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. But is the US economy expanding or contracting?

Expanding … according the ‘advanced’ reading just released by the BEA, Q3, 2024 GDP grew — in ‘current-dollar‘ terms — at the annual rate of 4.7%.

The ‘real’ growth rate — the number most often touted in the mainstream media — was 2.8%. In current dollar terms, US annual economic output rose to $29.35 trillion.

According to the IMF, the world’s annual GDP expanded to over $105 trillion in 2023. Further, IMF expects global GDP to reach almost $135 trillion by 2028 — an increase of more than 28% in just 5 years.

America’s GDP remains around 25% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

The total value of “cryptoassets” has now surpassed $4 trillion. Yes, this is a lot. For context, know that the US equities marketplace is worth about $60 trillion and the US bond markets are valued at about $55 trillion. So, in the aggregate, cryptoassets are “valued” today between 3 – 4% of these combined markets. BTC comprises 60% of that amount. But we’re not talking about this today.

Today we’re talking about stablecoins. What is a stablecoin, as defined by the GENIUS Act?

“A stablecoin is a digital asset that meets all the following criteria:

-

It is intended for use in payments or settlement – it is designed to function as money in transactions.

-

Issuer obligation – the issuer must be able and required to convert, redeem, or repurchase each coin for a fixed amount of monetary value.

-

Pegged to a stable value – the issuer represents that the coin will maintain a stable value relative to a fixed monetary amount.

-

Exclusions – it is not a national currency, a bank deposit, or a security.”

Permit me to summarize:

A stablecoin is a digital asset

used for payments, possessing a fixed monetary value,

and backed 1:1 by cash or US Treasuries.

By this Act, the US intends to launch America into the forefront of this rapidly developing digital frontier. And unlike BTC, this digital asset has a well supported use-case.

Does that comment seem odd coming from your blogger, a guy who agrees with Jamie Dimon that BTC is today’s equivalent of the Pet Rock? Or even worse, a Dutch tulip bulb? Rest assured, I have not changed my opinion on BTC. But I’ll save that discussion for another day.

A stablecoin is vastly different. The transactional use-case is quite strong. And for this reason, the stablecoin (SC) has now gone mainstream. The new rules also require all stablecoins to be federally regulated by the US government – even foreign-issued SC are covered under the Act if they are used or offered within the US. Foreign issuers doing business in the US must create a US entity that becomes licensed as a ‘Permitted Payment Stablecoin Issuer’ or PPSI.

Further, Congress passed the ‘Anti-CBDC Surveillance State Act’ which, effectively, bans the FED from issuing a digital currency without explicit authorization from Congress. Proponents of this bill point to China and their digital yuan, a use-case that many suggest is a thinly veiled “government-controlled” programmable currency. Which, of course, it is. Apparently, this concept has many detractors in Congress. “A CBDC would give the federal government access to and control over your personal financial information. It’s the kind of surveillance tool that has no place in a free society.” According to Rep. Tom Emmer, the co-sponsor of the bill. Agree or disagree, that seems to be the talk track in Congress at present.

Interestingly enough, this same prohibition does not apply to “open, permissionless, private” digital dollars – like bitcoin. So anyone — well, not the FED — can create their own currency or stablecoin! What can I say? Welcome to the Wild West.

OK, that’s enough updates. So, again, what does it all mean?

First and foremost, the FED will not be issuing a digital currency any time soon.

Second, plenty of others will. We will see an avalanche of new stablecoins in the near future.

The first US based SC is ‘Circle.’ Circle went public about a month ago. But it won’t be the last. All the big banks – JPM, BAC, Citi, Morgan Stanley – to name a few, have already thrown their hat into the ring. Across the “pond” Societe Generale, Revolut, BBVA and many others are planning to enter the space. They are joined by Fiserv, Paxos, Paypal and a host of other ‘fintech’ companies. Finally, VISA, Mastercard and AMEX have all said they are studying the space.

Why? What’s the attraction to the SC issuer? Well, in a word, money. It’s a money maker.

How? That’s easy: The SC issuer earns money holding the reserves that back the SC. Consider this: If an SC issuer holds $50 billion of reserves – comprised of short-term US Treasury securities yielding, say, 4% – they would yield revenue of $2 billion a year. And this is a likely case: Stablecoin issuers are required to hold cash or Treasuries to back the SC. Cash yields less than Treasuries, so clearly Treasuries will be the choice. Further, there will be transaction fees, licensing fees and float adding to the revenue pile.

Consider the business of American Express. They offer ‘financial services’ in over 110 countries and territories worldwide. Their cards are accepted in more than 160. Theoretically, the near-instant settlement from an AMEX stablecoin could significantly reduce their cross-border transaction expenses by reducing FX spreads and related bank fees. Further, research suggests real-time monitoring of their stablecoin could reduce fraud.

Why would a consumer use a stablecoin?

In the second quarter of 2025, American Express reported that their “billed business” broke up this way generationally:

<> 29% of the charges were from Baby Boomers

<> 36% from Gen X

<> 30% from Millennials

<> 5% from Gen Z

This is a huge generational shift away from those Boomers. Those other generations, all born after 1965, are much more likely to adopt newer technology – especially if it is cheaper.

In theory, with the Genius Act now in place, it will be a safe, fast, and inexpensive way to complete international transactions. The same will become true for credit and on-line merchants, as SC becomes deeply integrated into VISA and Mastercard rails. Remember: merchants pay a sizable credit card fee right now – might a stablecoin erode that cost? It’s quite likely.

Ever since Laszlo bought that 10,000 BTC pizza back in 2010, I’ve struggled to find a legitimate use-case for bitcoin. I have been unable to find one. Clearly spending $10 billion pizza is a bad idea. 🙂

But consider this: The global foreign exchange (FX) market handles an average of $7.5 trillion per day of overall volume. Every day! It is estimated that the ‘interbank spreads’ are about 0.01% of this amount – which is quite small, overall, but still translates to a $750-million-per-day transaction cost. Then consider intra-country remittances, which are estimated at several hundred-million-per-day. World Bank data suggests there is an “average” 6.6% fee on “global remittances.”

Finally, consider this:

More than 88% of daily FX is settled using the US dollar!

So the idea that the Genius Act essentially mandates that stablecoins are US domiciled and backed by US Treasuries is well supported.

It’s hard to estimate the size of a stablecoin market right now, but one thing is easy to forecast: Short-term US Treasury securities will be both the security backing most – if not all – stablecoins and US Treasury securities will be the largest benefactor from the adoption of stablecoins.

Benefactor? Yes. Absolutely. Remember, like all marketplaces, the Treasury marketplace is impacted by supply and demand. Lately, as we all know, supply has increased measurably. Which creates upward price pressure – in the form of higher interest rates – on those securities. What might happen to those interest rates if stablecoins significantly increase demand Treasuries? That one is easy. The opposite. Treasury rates could conceivably decline.

Is there an associated detriment? Possibly. Thru the lens of Paul Simon’s song, “One man’s ceiling is another man’s floor,’ a cost reduction always adversely impacts the entity previously receiving that income. Such is life in the capitalist’s jungle.

Combined, these facts clearly support a use-case for a stablecoin: It can conceivable reduce transaction frictions across the trillions of dollars of cross-border transactions, while at the same time reducing offering real-time monitoring of the transaction and accelerating settlement. In fact, VISA is already doing precisely this: Today, VISA settles SC payments in more than 25 countries and is running a number of cross-border stablecoin trials.

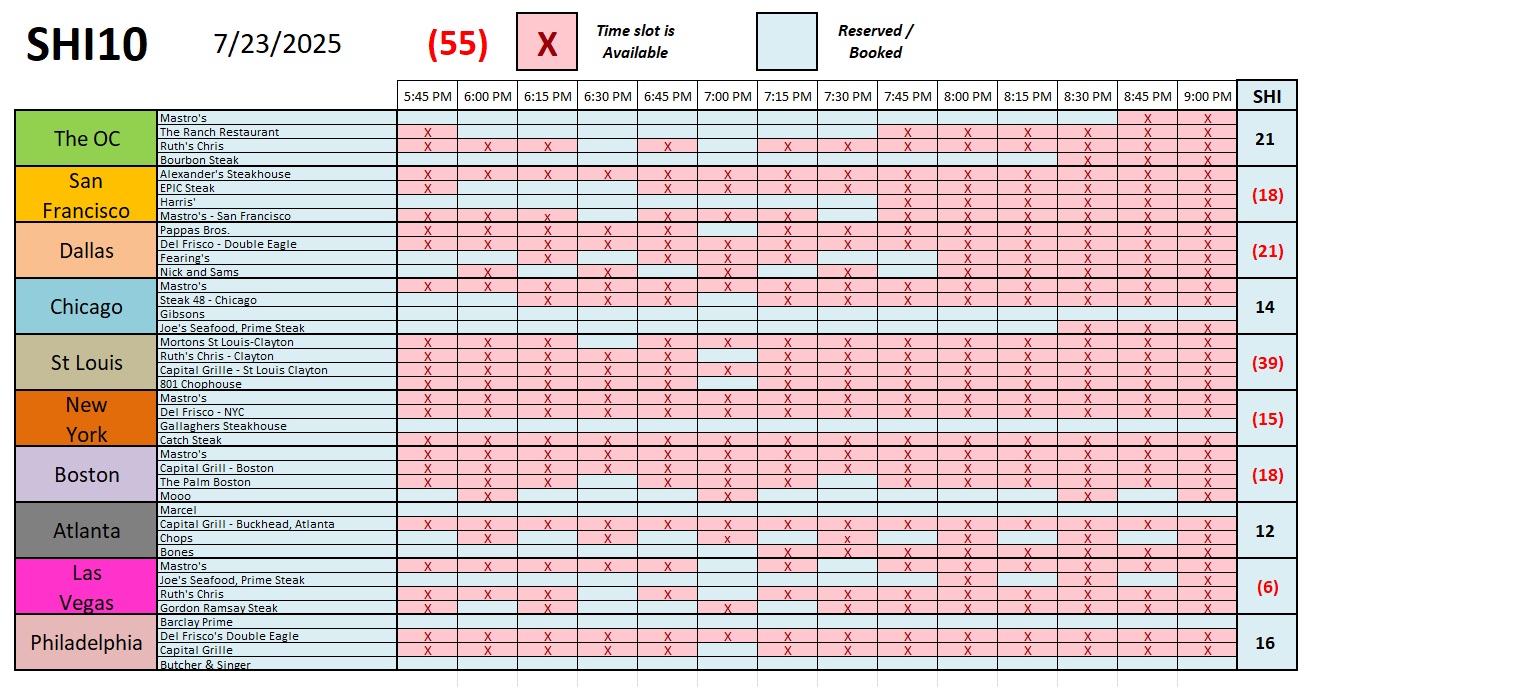

Let’s jump over to the steak houses and see what expensive eatery reservation demand is telling us today.

Not much is the answer. Clearly, that predominantly raw-steak red chart above is definitely telling us high-dollar steak house reservations are not in high demand right now. But that’s not new this week. As you’ll see in the long-term chart below, reservation demand has been weak for some time now. Even the Mooo steak house in Boston has numerous openings today for this coming Saturday!

Bottom line: Expensive steaks are sizzling on the grill, but the SHI10 continues to look cool.

As further proof of just how fast the “digital currency” picture is changing, consider this headline posted just a few hours ago:

BNY and Goldman Sachs Launch

Tokenized Money Market Funds Solution

{kind=link}