SHI 7.3.24 – Musical Chairs

SHI 6.26.24 – A Whole Lotta Red

June 27, 2024

SHI 7.10.24 – Greek Mythology

July 10, 2024

No matter how you measure it, by historic standards the US economy is huge today.

Consider the US labor force. According to the Bureau of Labor Statistics (BLS) employed Americans measured about 161 million in May of 2024. In 1951, that was the total population of the United States — today our population is over 330 million. 161 million employed people is a whole lot of people.

In January of 2023, the number of employed Americans was about 1 million folks lower — right at 160.15 million. But the number of unemployed people, measured by overall size, has grown recently, too. In May, ‘civilian unemployment’ totaled 6.65 million folks. In other words, 6.65 million people who sought full-time employment were unable to find jobs as of May. In January of 2023 — about 15 months earlier — that number was only about 5.7 million people.

So while the number of people employed has grown by almost 1 million since 2023 began, the number of people unemployed has also simultaneously grown by almost 1 million.

By the way, here is a great graphic generator from the BLS: https://www.bls.gov/charts/employment-situation/civilian-employment.htm

Using the pull-down menu, you can get a great visual on all kinds of data. Remember, “right click-open in a new tab.”

“

161 million is a large number.“

“161 million is a large number.“

Very large.

But even larger is the amount of dollars this 161 million people earn on an annualized basis. The ‘average hourly earnings’ in May of 2024 was about $35. Let’s do the math: $35 per hour X 2,080 work hours in a year X 161,000,000 = ………. drum roll ………

$11.72 trillion per year

At almost $12 trillion per year, employment income is a big part of our $28 trillion economy. No, labor itself is not measured within, nor directly contributes to, overall GDP figures, but employed people do spend money. Lots of money. And consumer spending is a big part of our GDP — as you know, is about 70% of all American economic activity. Thus, full, or at least high levels of, employment is critical for strong economic activity. But what does this have to do with ‘Musical Chairs‘ you ask?

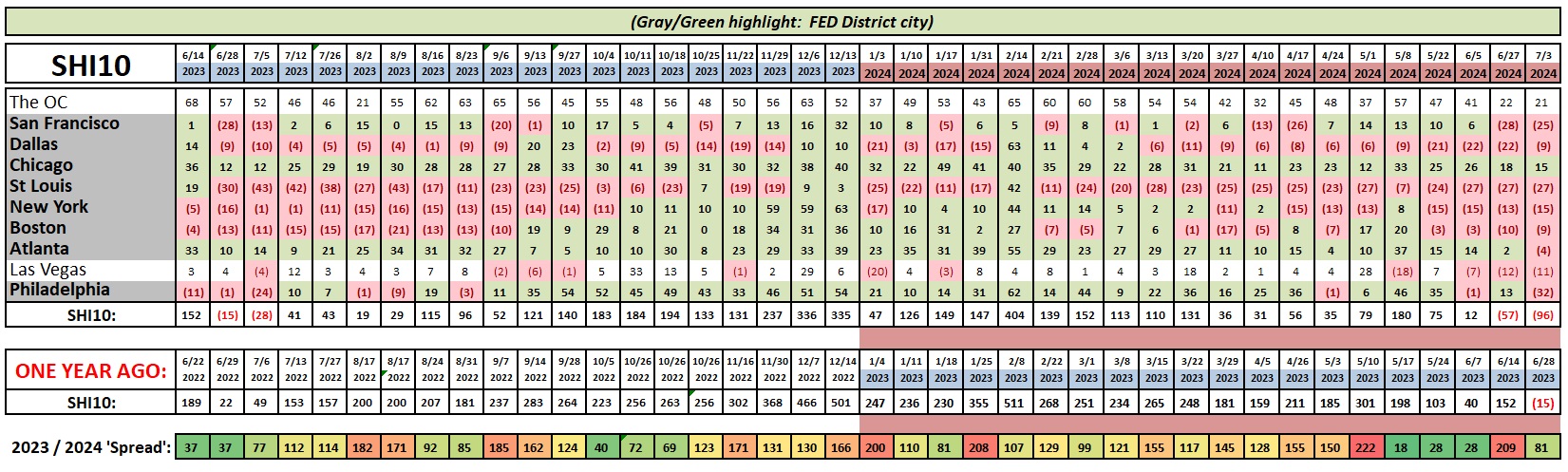

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. But is the US economy expanding or contracting? Expanding …. By the end 2023, in ‘current-dollar‘ terms, US annual economic output rose to an annualized rate of $27.94 trillion. After enduring the fastest FED rate hike in over 40 years, America’s current-dollar GDP still increased at an annualized rate of 4.8% during the fourth quarter of 2023. Even the ‘real’ GDP growth rate was strong … clocking in at the annual rate of 3.3% during Q4.

According to the IMF, the world’s annual GDP expanded to over $105 trillion in 2022. Further, IMF expects global GDP to reach almost $135 trillion by 2028 — an increase of more than 28% in just 5 years.

America’s GDP remains around 25% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

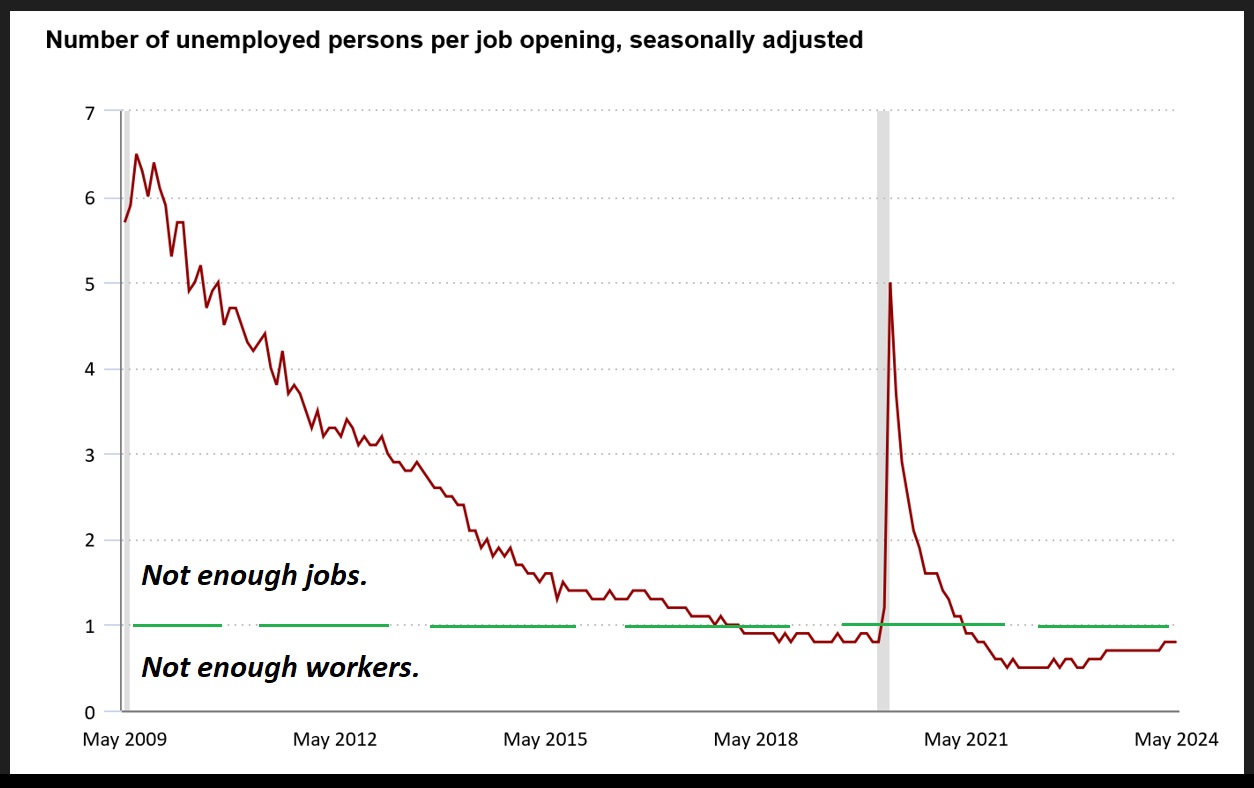

Let’s talk musical chairs. Right-click this image and select “Open Image in New Tab.”

With the image open in a separate tab, you can follow along easier.

First, note the title of the chart. It compares the number of unemployed folks, at any given time since May of 2009, to the number of job openings at precisely that same time. Following the “Great Financial Crisis of 2008” there were far more unemployed people than there were job opportunities. Simply stated, there were not enough jobs out there. America had a lot more workers than jobs.

Fast forward to 2018 when the ratio crossed below the green line. By late-2018, after crossing that line, the US economy had an insufficient number of workers. In fact, since that time, the American labor force was insufficient, in size, to fill all the available jobs. And we remain below that green line today. By this metric, there are not enough workers out there to fill the available jobs.

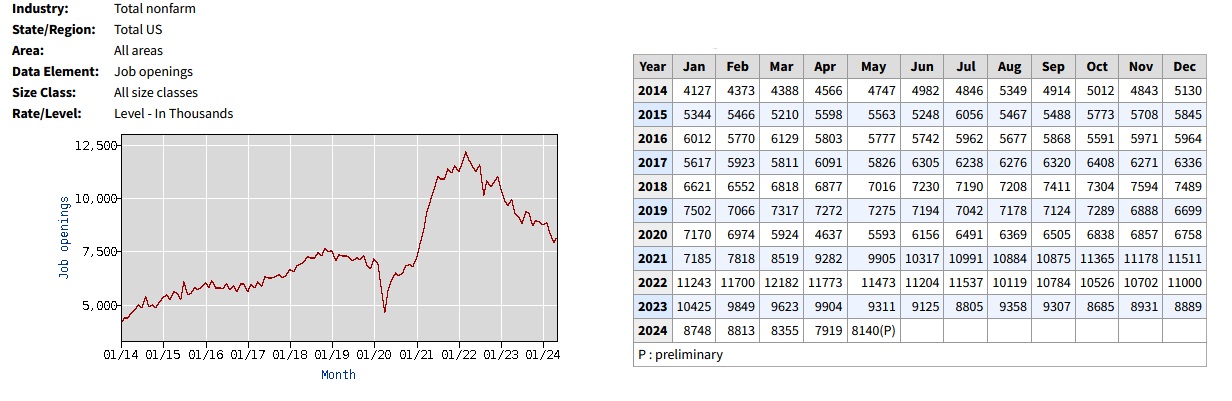

This labor size inadequacy has been one of largest hurdles for the FED. It is one of the primary reasons they have resisted lowering interest rates. But like many other post-Covid problems, this one, too, is resolving. Take a look at our next graphic:

These are the ‘JOLTs‘ number. Remember that JOLT is a government acronym for the ‘Job Openings, Labor Turnover‘ metric.

The graphic to the left — JOB OPENINGS — was created from the numbers on the right. This is a 10-year chart. Post pandemic, the number of job openings soared to unprecedented levels. In the number grid to the right, we see that JOB OPENINGS peaked in March of 2022 at 12,182 job openings. Back in 2000, this number was about 5 million … and it didn’t rise above 5 million until 2014, as we see in the graphic above.

So what does all this mean?

Essentially, the labor market is weaker than the numbers suggest.

Why? While new job formation is chugging along at a so-so rate, the number of job openings continues to trend downward while, and the number of job openings per unemployed laborer is heading back toward equilibrium. We are still in the “not enough workers” region on the graphic above, but we are trending back toward 1 to 1. Once we pass that figure, the labor market will, once again, have too many workers and not enough job openings.

Again, however, its important to keep this in perspective. For more than 5 years, we’ve been operating in an economy with an insufficient number of workers. We are heading back toward equilibrium at a very, very slow rate. It’s a trend worth watching … but not one worth worrying about.

Remember: We have 161 million people out there earning a paycheck. Collectively, they are earning close to $12 trillion. As long as the American labor force is employed, laboring and spending, the economy will remain sound.

On the other hand, I am getting a bit more worried about steak house reservation demand. It grows weaker by the week.

Back in December of 2023, every city in the SHI10 was green — every city had a positive SHI. Today? 8 of the 10 cities are flashing red. High-highfalutin steakhouse reservations are widely available for this coming Saturday evening. With a negative 96 reading today, it’s easy to see this trend is flashing red for the US economy.

It’s worth noting that the Atlanta FED ‘GDPNow‘ estimate, as of this morning, has also deteriorated. As of July 3rd, the latest estimate for ‘real’ Q2, 2023 GDP is running at 1.5%. You’ll recall the number was a fairly weak 1.7% just a few days ago.

Again, what’s it all mean? I’ll repeat my earlier admonition: The US economy is slowly slowing. The FED will have to begin reducing rates, in small but incremental steps, very soon.

<:> Terry Liebman

{kind=link}