SHI 8.28.24 – Tennis Millionaires

August 28, 2024SHI 10.2.24 – Sweating the Labor Market

October 2, 2024

I just returned from London.

Which, as you know, is the home of Shakespeare and his infamous plays. We walked past the Globe Theater — the latest one — which was originally built on the Thames in 1599, and burned down (the first time) in 1613. Such amazing history.

London capped off an almost 3-week trip that took me from Reykjavik, Iceland down thru the North Sea to Scotland, Ireland, the Isle of Man, and finally to the capital of the UK itself. As this remains an economic blog, I’ll refrain from travel commentary except only to say this: London was busy! The streets were packed with locals and tourists, the pubs were filled to the gills, and the city looked great.

Of course, these are really economic observations.

Because a vibrant city is a place where people are spending money. And at its core, every city and country economy is heavily reliant on consumer spending. This is far more true in the West … but across the globe, economies depend on consumer spending and activity for their financial success. As you all know, while I was away, the FED decided to “super-size” their rate cut. I was confident they would toss out a 25 basis point bone at this time — primarily as we find ourselves so close to a highly contested presidential election. But apparently throwing caution to the proverbial wind, they went with a 50 basis point cut.

“

The FED cut rates by 1/2%.“

I was surprised by the size of the cut. I really expected a 1/4 percent cut in the FEDs ‘Federal Funds Rate’ (FFR).

Many financial experts were were surprised by the larger-than-expected move. And immediately the hand-wringing began. Many media reports featured financial experts claiming the 1/2% cut — double in size what was generally expected — suggests the FED is worried about a recession in the near future. I have no doubt you’ve read numerous expert commentary on this issue. Financial and economic experts paint the move as a nod to impending economic weakness. They seem to all agree that the ‘super-sized’ cut is indicative of degeneration in the economic picture, vis-à-vis the employment market.

But I disagree. I feel the angst is misplaced and wrong. To quote the Bard himself, it is truly much ado about nothing. Not only is our economy expanding, it is growing at a rate significantly higher than even the FED expected for 2024!

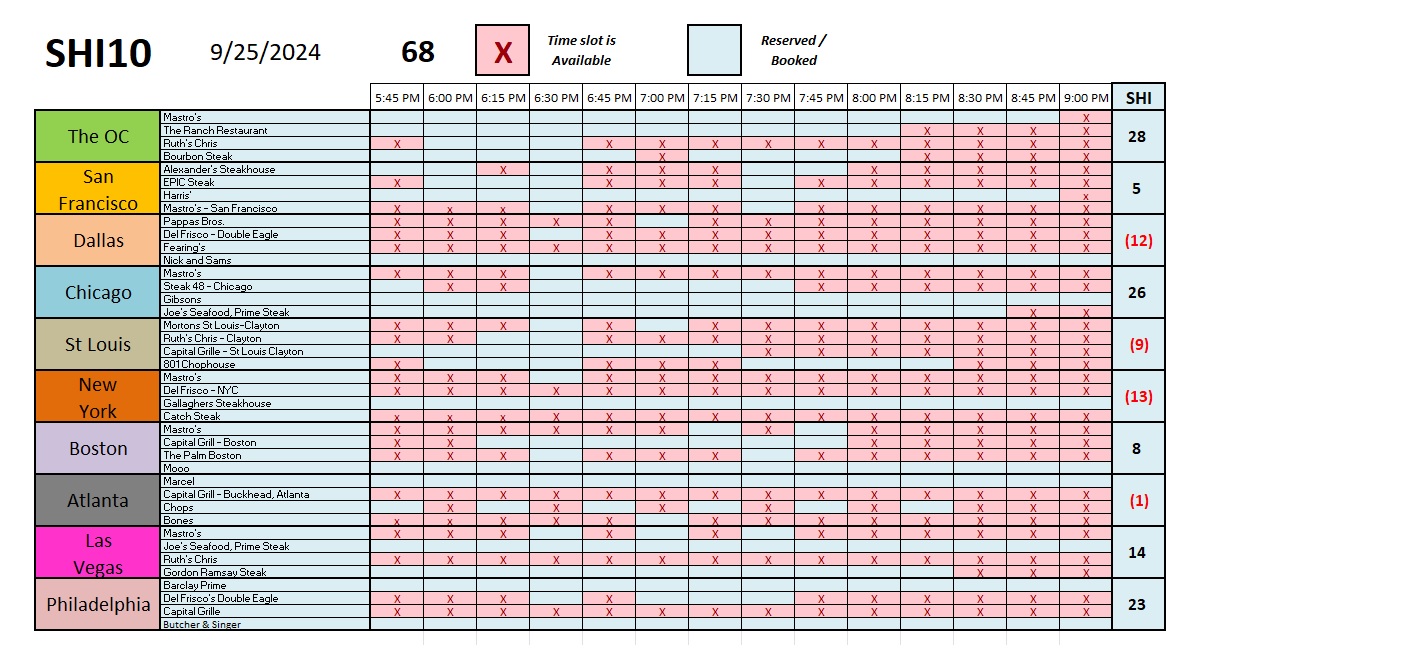

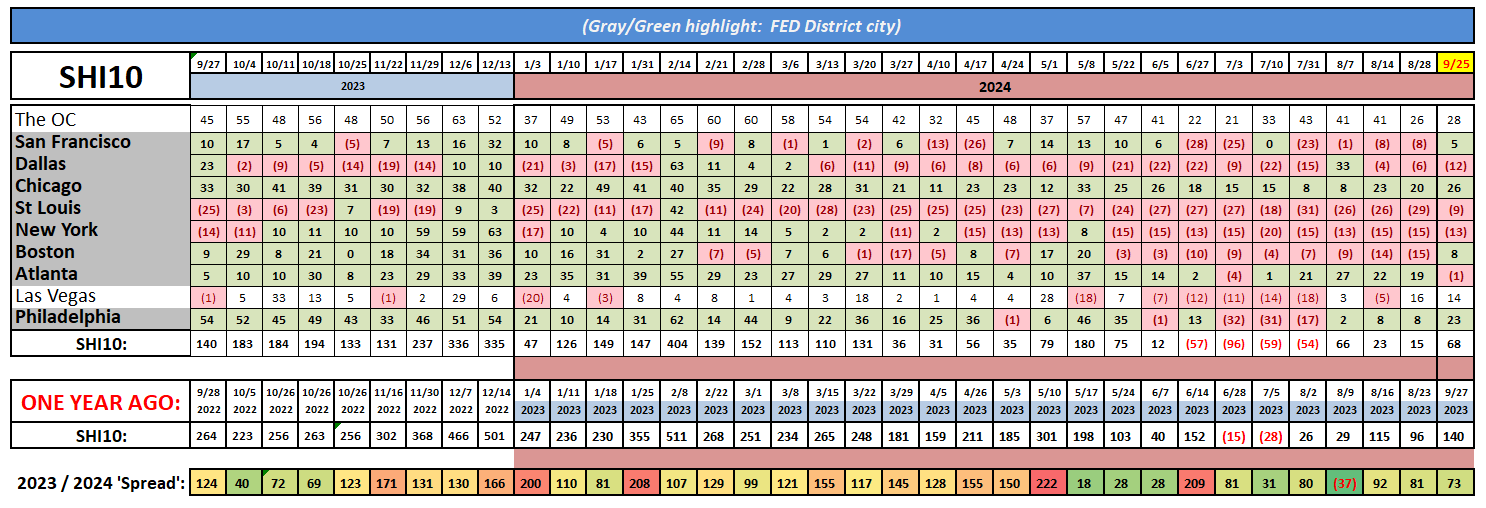

Welcome to this week’s Steak House Index update.

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding …. By the end of Q2, 2024, in ‘current-dollar‘ terms, US annual economic output rose to an annualized rate of $28.63 trillion. After enduring the fastest FED rate hike in over 40 years, America’s current-dollar GDP still increased at an annualized rate of 4.8% during the fourth quarter of 2023. Even the ‘real’ GDP growth rate was strong … clocking in at the annual rate of 3.3% during Q4.

According to the IMF, the world’s annual GDP expanded to over $105 trillion in 2023. Further, IMF expects global GDP to reach almost $135 trillion by 2028 — an increase of more than 28% in just 5 years.

America’s GDP remains around 25% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Sure, the cut in the FFR was larger than I expected.

Double in size, in fact. But I don’t believe recession fears on the part of the FED was the basis for the large cut. Many experts have expressed this concern. I don’t share it.

I believe the 50 basis point move tells us two things: First, half the rate cut was to begin reversing the tight monetary conditions imposed by the FED beginning in March of 2022. That’s right: The FED began their tightening cycle almost 2.5 years ago. Time does fly. And now, feeling they have (generally) defeated the inflation monster, they began a cut cycle. Fnancial conditions are easing. The 1/2 percent rate cut should quickly reduce short-term variable consumer loan rates, credit card interest rates, and home loan rates.

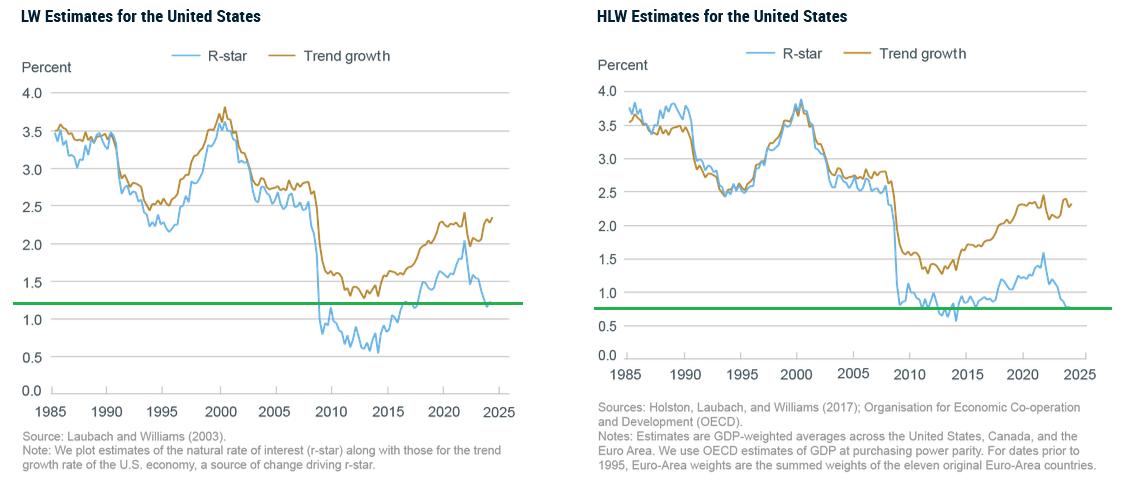

I believe the additional or “extra” 1/4% cut was targeted at moving more rapidly toward what we call the”natural” or “neutral” rate of interest. Essentially the neutral rate of interest is an “equilibrium” rate. It is a rate of interest that rate which is neither restrictive nor stimulative to the economy. Of course, that’s a moving target. The rate is always fluctuating up and down, but in any case that equilibrium or neutral rate is most assuredly far below the current federal funds rate of about 5%.

Here’s a NY FED link if you’re interested in a deeper-dive than my comments below (right click, ‘open in a new tab’)

You see, the current FFR is quite economically restrictive thru this lens. The natural or neutral rate — also known as ‘r-star’ in economic circles — is far lower than the current FFR. In fact, depending on which forecast model one uses, as you can see in the graph below, the neutral rate is probably much closer to 1.25% — and maybe as low as 0.75%.

Clearly, even after the 50 basis point cut, the FFR is still far above this theoretical neutral rate. The FFR remains way too high. Which is ironic, as the economy continues to prove its resilience. Earlier this morning, the Bureau of Economic Analysis (BEA) released its final GDP estimate for Q2 of 2024. They confirmed that:

The US economy grew by 3.0% during the second quarter on a “real” basis and by 5.6% on a “current dollar basis.”

For the first time in history, per the BEA, the US economy eclipsed $29 TRILLION on an annualized basis:

Current‑dollar GDP increased 5.6% at an annual rate, or $392.6 billion, in the second quarter to a level of $29.02 trillion, a $9.5 billion larger increase than the previous estimate.

Even with the interest rate headwind, GDP still grew substantially above the trend rate. After this first FFR rate cut of 0.5%, economic growth will surely have another tailwind. No, recession fears just diminished somewhat. What’s more, the Atlanta FED and NY FED are now forecasting 2.9% and 3.01%, respectively, for Q3 GDP ‘real’ growth. These are impressive numbers, folks. No recession here.

So ignore all the hand-wringing and whining from the economic experts telling you the 1/2 point rate cut is evidence the FED expects a recession soon. These comments are total hogwash. The US economy remains solid, expansionary, and growing above trend. These naysayers? Much ado about nothing, I say. Ignore them.

It is worth noting that the FED did express some concern about the labor market. For good reason. Job growth has been decelerating and the number of unfilled jobs has returned to historic trend levels. The FEDs “duel mandate” requires they focus on both ‘economic growth’ and ‘full employment.’ So their concern is noted. But I contend the slow-down in job growth is more cyclical and mean reversion than indicative. Time will tell … but I’m not concerned. Yet. 🙂

To the steakhouses! It’s been almost a month since we visited … let’s see how they’re doing.

Quite nicely, it appears. Expensive eatery reservations remain in high demand across the US. As you will see below, San Francisco and Boston both jumped from the ‘red‘ into the black this week. Even St Louis saw a significant increase in reservation demand. The steakhouses are looking flush.

Forecasters will always disagree on the future. As Yogi Berra said, “It’s tough to make predictions, especially about the future.” 🙂

But I strongly disagree with the experts who paint this FED rate cut as indicative of their fear the economy will soon tilt negative. This cut is a good thing. Our economic foundation is strong and this 1/2% rate cut will provide an even greater tailwind. Consider these closing evidentiary facts:

<> Economic growth, as evidenced by both the GDP and the GDI, has been revised UP from prior periods. Q1 GDI was revised up from 1.3% to 3.0%!

<> The technical ‘recession’ the US experienced in the first half of 2022 has just been revised away.

<> Most of the GDI revision can be attributed to wage compensation — it was revised UP from a 1% increase to 2.4% in Q1.

<> The compensation revision resulted in upward revisions in the personal savings rate.

<> Corporate profits was also revised upward in Q2. Pre-tax profit is now more than 13% of GDP — something that hasn’t happened since the 1950s.

<> Unemployment claims fell again last week. Open jobs may have fallen, but people are employed and working.

In closing, I did want to mention this. All the countries we visited in Europe charged a VAT — what is called a ‘value added tax,‘ or sales tax. In England the VAT amounted to 20% on whatever we purchased. My observation, accurate or otherwise, is this tax was charged on everything, including food. I mention this because I found it interesting. Even more interesting is the fact that after all the income and other taxes the UK already collects, this 20% VAT doesn’t appear to solve their deficit spending problems. Even after accounting for the VAT, their deficit is running above 4% per year.

Can a government ever spend less than it collects in revenue? What a great question? 🙂

I’ll leave that one to you.

<> Terry Liebman

{kind=link}