SHI Update 7/19/17: Lend Me Money!

SHI Update 7/12/17: The Silent Giant

July 12, 2017

SHI 7/26/17: Food for Thought

July 26, 2017

Imagine this: You’re a lender — making student loans. Should default rates impact your decision to lend? If not the decision itself, how about the interest rate you charge?

If I was a “student loan” lender, I would certainly consider ‘default rates’ when making a lending decision. Wouldn’t you?

Unfortunately, our federal government does not. And this is REALLY unfortunate, since our federal government is the direct lender or guarantor of over $1.3 trillion in student debt. Let me add some context here: In the last fiscal year, 24% of the US Treasury budget was paid to Social Security recipients. Almost $925 billion was paid out, in total, during the year. The US student debt load is equal to about 1.5X annual social security payments. Wow.

Not only is the amount massive, but even more concerning, you and I are effectively offering student loans that are unlikely to ever be fully repaid.

Welcome to this week’s Steak House Index update.

As always, if you need a refresher on the SHI, or its objective and methodology, I suggest you open and read the original BLOG: https://terryliebman.wordpress.com/2016/03/02/move-over-big-mac-index-here-comes-the-steak-house-index/)

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. Is it expanding or contracting?

The world’s GDP is about $76 trillion. Our US GDP is almost $19 trillion — about 25% of the total. No other country is even close.

The objective of the SHI is simple: To help us predict US GDP movement ahead of official economic releases — important since BEA data is outdated the day they release it.

‘Personal consumption expenditures,’ or PCE, is the single largest component of US GDP. In fact, the majority of all US GDP increases (or declines) usually result from (increases or decreases in) consumer spending. Thus, this is clearly an important metric to track. The Steak House Index focuses right here … right on the “consumer spending” metric.

I intend the SHI is to be predictive, anticipating where the economy is going – not where it’s been. Thereby giving us the ability to take action early. Not when it’s too late.

Taking action: Keep up with this weekly BLOG update.

If the SHI index moves appreciably -– either showing massive improvement or significant declines –- indicating expanding economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

First, a quick apology. I’m on vacation and I’m writing my blog on my iPad. Which presents certain technical challenges that I’ll discuss later in the blog. Fortunately, I was able to write the introductory section before leaving town … so at least that portion is as “pretty” as usual. 🙂

You might find this interesting. I certainly did.

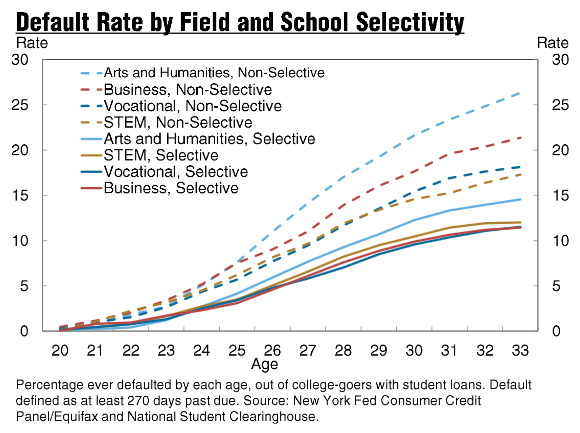

“For-profit” college students have the highest student loan default rates. 2-year college students have higher default rates than 4-year college students. In fact, the difference is staggering: Students from both these groups are TWICE AS LIKELY to default on their loan than their private, 4-year counterparts. Take a look at this image, courtesy of the NY FED Research and Statistics group:

Many colleges are ‘selective’ — meaning they accept only students exceeding specific admittance requirements and aptitude. Many others are ‘non-selective’: If you apply for admission, and can pay the tuition, you get in. Easy….

So, how about a ‘pop quiz’: Which has a higher default rate? Pretty obvious, right?

‘Non-Selective’ colleges have the highest default rates. No big shock there. Interestingly, once again, students from ‘non-selective’ colleges are almost TWICE AS LIKELY to default on their student loan than students who must surpass admission requirements.

Does our federal government charge ‘non-selective’ college students a higher rate? Nope. The same. It turns out, the interest rate charged for all federal student loan programs is the same.

Let me summarize the data. It appears that a student who attends a ‘non-selective,’ private, for-profit 2-year school is about FOUR TIMES MORE LIKELY to default than a student fortunate enough to qualify for admission to a private, “not-for-profit” 4-year college.

Let me repeat that: 4 times more likely to default. Yet, our benevolent federal government feels they should all be loan-approved and charged the identical interest rate. I wonder how long our banks would remain in business if they qualified their borrowers using a similar approach? 🙂

I have no issue with our federal government making or guaranteeing student loans. They should. I have an issue with bad lending practices, however, which by their basic nature tend to promote poor decisions from student borrowers. Cheap and easy-to-borrow money may cause a potential student to borrow money for an education not worth the cost of the debt. Saddling that student with a debt load which may haunt them for years to come.

Damn, it’s time for a steak. And a bottle of wine.

OK…here are those “technical difficulties” I mentioned earlier. As I’m working from my iPad, I’m unable to create my typical SHI images. Further, I’m unable to “preview” the blog before I post it. So I will apologize in advance for all the errors that I’m certain I’ve missed!

I’m sure it’s user error … but one I’ll have to modify when I return to my office next week. For now, let me say the SHI remains under pressure: This week’s reading is a negative 20. Only Mastros Ocean Club has booked time slots — from 5:45 to 8:30. (8:45 and 9:00 pm are open.) Our other three pricey eateries are wide open for you and your 3 guests this Saturday.

The SHI reading for 7/20/16 was a negative 7. Our spread, therefore, is 13. Not horrible…but still substantial. This week’s reading, once again, continues to support my belief that consumer spending remains sluggish.

And once again, I believe the SHI is suggesting we will see weak Q3 GDP growth. How weak, of course, is the question. Next week we will study some a few other related data sources and see if we can quantify the forecast.

- Terry Liebman

{kind=link}