SHI 3.9.22 – The Problem with Forecasting

SHI 3.2.22 – Rising Uncertainty … Uncharted Waters

March 2, 2022

SHI 3.16.22 – It Will be Tough from Here

March 16, 2022

The headline reads: “Miami’s condo bubble is up against a monster.”

Condo bubble? In Miami?

That’s right. According to the article, “condos are getting crushed” in Miami. Massive supply growth, the article continued, is overwhelming demand. In fact, during the next 24 months the article reported, 40 large projects will be completed, adding another 11,000 units to an already overcrowded market. According to StatFunding, based on current sales trends, ballooning supply will give Miami a 674-months’ supply — a glut that could take 56 years to absorb. Prices and values, the author opined, will soon plummet! Look out below!

“

Who want’s a Miami condo?”

“Who want’s a Miami condo?”

No, as I suspect you already figured out, this is not a current news report. The article appeared in August of 2016, a time when condo demand was moderate and supply was growing fast. New high-rise condo construction did explode, delivering a very, very large number of beautiful, brand-new units to the market in a very short period of time. At that time, almost every local real estate expert predicted two things: Values were certain to decline double digits and it would take decades to clear the inventory.

Neither happened. Once again, the experts were wrong.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Significantly. During 2021, nominal growth clocked in at $2.1 trillion. The US annual economic output was just under $23 trillion for the full year. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

This is why predicting the future is really a fools errand. Experts may have a reasonable grasp of the applicable variables, the “if” and “then’s” if you will, but they never know them all. In fact, by my observation, many forecasters make predictions using a woefully inadequate data set. Sometimes this happens because the data is in flux, changing quickly as circumstances moderate; others, it’s because the forecaster is simply incompetent.

Like the bozo who forecasted it would take more than 50 years to clear the Miami condo inventory in 2017.

But that’s the risk one takes when making a public forecast. I’m sure at least one or two of my 6 blog-readers thinks I’m a bozo, too. 🙂

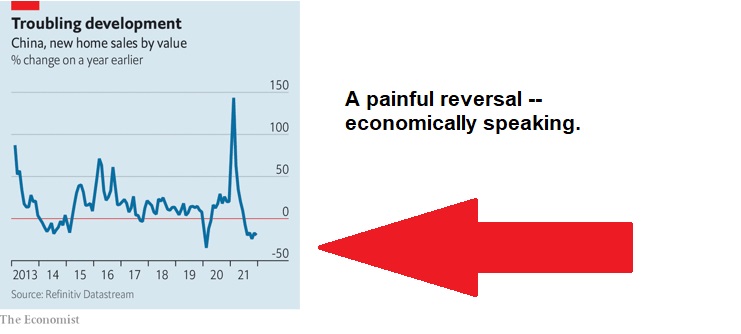

Years ago, I predicted the Chinese housing market would eventually crash. The oceans of “see-thru,” high-rise condos in Beijing and other mega-cities are legendary. Many of these completed projects remain unoccupied even today. Few were ever intended to lived in. Most were purchased in speculation. A fact that ultimately, eventually, drove the Chinese president, Xi Jinping, to do something unexpected: Like shutting off the water to a garden hose, he turned off the tap of easy credit. Within a few months, the first of a dozen of major Chinese developers, Evergrande, defaulted on their bonds. Now, almost a full year later, construction remains stalled in many projects; many developers have ceased land purchases pushing residential land values down 72% year-over-year. Home prices have begun falling in many cities, turning off the tap for many speculators. According to one consultant, the annual supply of urban homes is now 3-times forecasted future household formation. Said another way, many cities in China now have a 3-year supply of condos on the market.

The really fascinating part of this story is not the massive decline in home sales. To me, its the fact that free-market forces did not cause this reversal. No, this outcome is 100% the result of the decision by one man to change the future. Housing speculation was out of control, making a home unaffordable for many … flying in the face of Xi’s well-documented policy of “common prosperity.” So he decided it was time for a change.

Perhaps, not unlike Putin’s decision to invade Ukraine. Once again, the guy in charge decided it was time for change.

In both cases, it’s awfully hard to predict the outcomes of their choices. In China, the choice to crush speculation seems to be in-line with the Communists’ longer-term plan. In a country where the government already controls education and health care, having a hand on the tiller of housing might be all Xi and the communist party needs to promote their common prosperity doctrine — of course, this can only happen after China crushes all the housing entrepreneurs and takes over their businesses. Which seems to be happening now.

And then the world watched the the Chinese winter Olympics spectacle … or debacle … you pick the adjective … and once Putin left the games, and returned to Russia from Beijing, he decided to invade Ukraine. Any connection? Who knows. Hard to say. Just as it’s hard to gauge China’s feelings on Putin’s war. They’ve been awfully quiet since the invasion.

But the Chinese economy is reeling from Xi’s war against Chinese housing speculation. Home sales have fueled hyper-GDP growth for almost a decade. The luminary economist and Harvard professor Kenneth Rogoff estimates almost 30% of China’s GDP growth is driven by real estate development. That’s right … almost 30%. But that’s all changed now. Probably permanently. And so China’s economy will shed the annual growth that was tied to housing. China has “targeted” a 5.5% GDP growth rate in 2022. I doubt they will hit it…but as they lie to the outside world about most financial statistics, we may not know the true impact until much later. For China, in the aggregate, this will be painful at best, making this a very difficult time for Xi to vocally support Putin against the rest of the world. Perhaps that’s why China has been awfully quiet since the invasion. Again, it’s hard to say.

Regardless, no amount of government intervention will fix the massive glut of empty homes all over China. New births and household formation are simply inadequate to quickly absorb all the existing supply of homes…let alone newly build homes.

Allen Feng and Logan Wright at Rhodium have done a bit of forecasting themselves: In an admittedly highly-optimistic scenario in which 65% of China’s roughly 170m people currently aged 16-25 eventually live in cities, and 90% of those enter the housing market, that still only creates demand for about 50 million homes over the next decade. Even if each of those new households bought two homes, at the current rate of building, China’s home market has a 5.5-year supply. Hmmm.

Right or wrong, China has a self-imposed mess on their hands. As does Russia, after the Ukrainian invasion. Downstream, so does the US as $7 per-gallon gasoline is probably on the horizon. But who knows? Its a tough time to be in the prediction business. 🙂

So, instead of making a prediction now, I’ll offer some common-sense advise: Work hard to treat “expert” forecasts with a dose of skepticism and a grain of salt. Most are well-intentioned, some are self-serving, but in all cases, you should work hard to maintain objectivity and consider the alternatives.

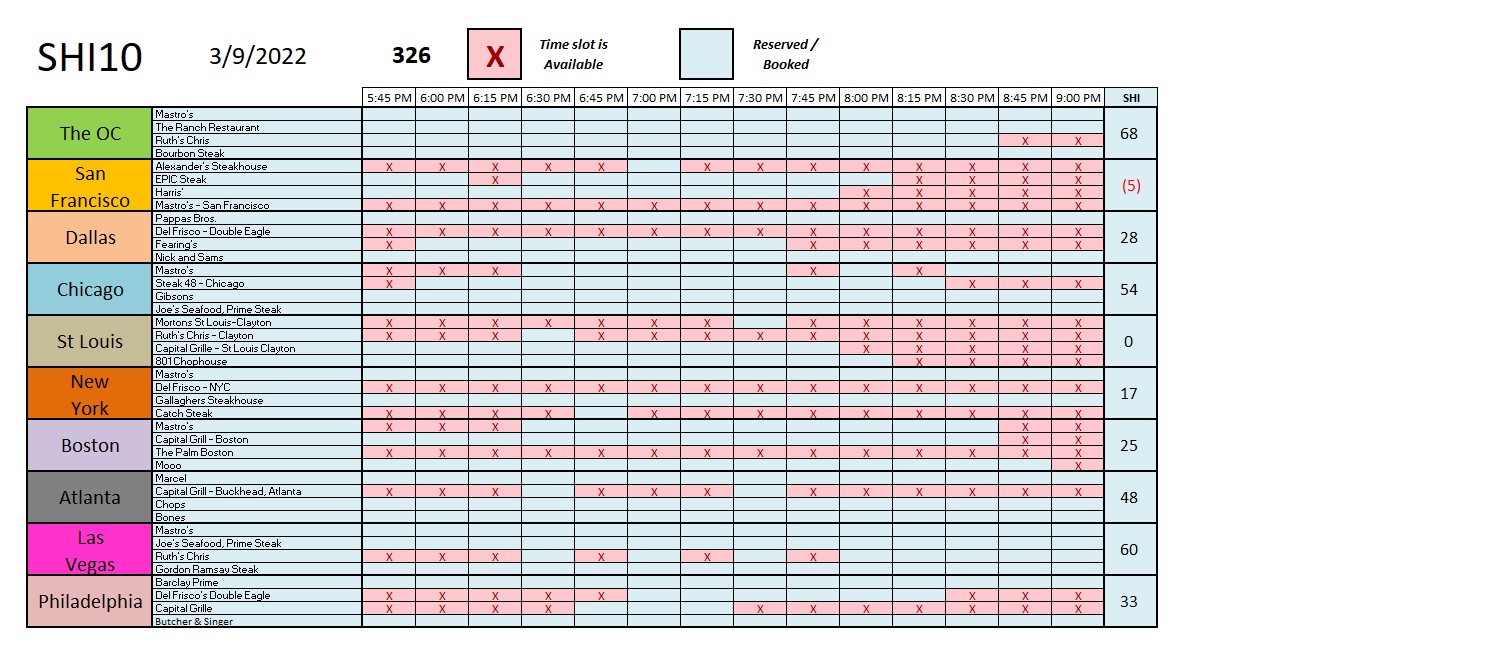

But, hey! This is the Steak House Index, by-gosh! It’s what we do here! So let’s grab a sharp knife and carve into reservation data at our 40-expensive-eateries for this coming Saturday across this great land of ours and see if 700-degree T-bones are flying off the grill, or if those slabs of beer are still still chillin‘ in the ‘fridge. First, the trend report:

Interesting. Not much change from last week. Reservation in ‘Vegas spiked this week … I’ve heard anecdotal reports that the city is packed these days. And our affluent eaters here in the OC continue to reserve tables and order steaks at inflation-spiked prices. As before, it’s a bit of a mixed bag in other SHI10 markets. The weakest demand city is still San Francisco, closely followed by St Louis. Here is the weekly report:

With all the excitement in the east, you may have forgotten the FED meets next week, and precisely one week from today, I predict we will learn that the FED raised interest rates by 25 basis points. That’s right: I’m making a prediction! And this one, I’m confident, you can take to the bank!

At least I think I’m confident. My fingers are crossed — I hope I don’t feel like a bozo after the actual outcome is known. 🙂

<:> Terry Liebman