SHI 3.16.22 – It Will be Tough from Here

SHI 3.9.22 – The Problem with Forecasting

March 9, 2022

SHI 3.23.22 – Is Recession Now Inevitable?

March 23, 2022

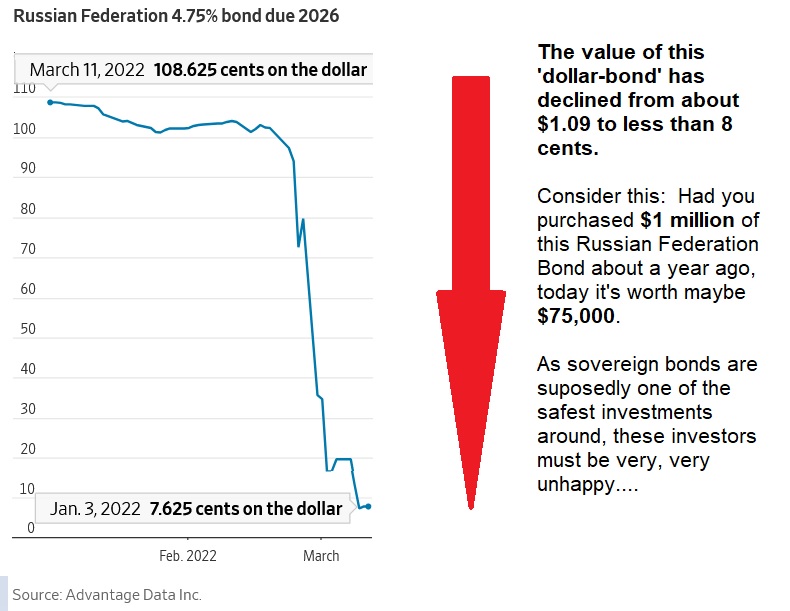

… said the CNBC commentator earlier this morning, when discussing Russia’s future, assuming they fail to pay $117 million of interest due today on ‘dollar-bonds.’ If they do, it will be the second Russian sovereign debt default since 1917.

According to Bloomberg, Russia’s failure to pay, or should they pay the interest due today in rubles as opposed to US dollars, will start “the clock ticking on a potential wave of defaults on about $150 billion in foreign-currency debt owed by both Russia and Russian-owned companies.

“

No, it will be tougher than tough.”

“No, it will be tougher than tough.”

Debt repayment requires two things: First a willingness to repay. I suspect Russia is willing to pay the interest due. The challenge is in the second: The ability to repay. Here’s where it gets complicated. In theory, Russia has the ability, and perhaps even the willingness, to repay. They have plenty of money. But they don’t have plenty of US dollars. And since the interest due today is due on ‘dollar-bonds’ — meaning the loan itself was originated in US dollars, and mandates interest and principal repayment must be in US dollars — Russia has a serious problem.

Apparently, viciously attacking and invading a peaceful neighboring country, an action denounced by almost every country in the free world, triggering punishing financial and economic sanctions, can cause financial difficulties for the aggressor country, making debt repayments difficult if not impossible. Apparently, one stupid war can ruin your entire credit rating! Who knew?

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Significantly. During 2021, nominal growth clocked in at $2.1 trillion. The US annual economic output was just under $23 trillion for the full year. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

It’s an interesting question, right? “Who knew?”

I’m guessing the answer is simple: Just about everyone with a brain except Vladimir Putin. Before attacking Ukraine, Putin must have assumed the EU and American response would be limited to histrionics only. He must have assumed Europe was so dependent on Russian oil and natural gas they would simply turn the other cheek. He must have assumed America’s political fractures, and Congressional gridlock, have neutered us, preventing any strong response beyond verbal condemnation.

Boy was he wrong. Whatever other outcomes we all experience from Russia’s invasion of Ukraine, one is almost an absolute certainty today: Russia is now a financial pariah. No one with a brain will lend Russia money now. If ever again.

Let me repeat that: Post-invasion, $1 million of ‘Russian Federation’ dollar-bonds are now worth about $75,000. And that assumes you can find a buyer.

When did Russia last default on a sovereign bond? In 1998. But that default was quickly forgiven, and Russia was able to re-enter the global capital markets a handful of years later. Not this time. This one is going to sting … for years, if not decades, and perhaps permanently. Why is this default different? Because more than 75 years of peaceful coexistence in Europe — the battleground for WW2 — was destroyed with Russia’s invasion of Ukraine. Further, human rights and human life have far greater value today. Putin’s invasion clearly broadcast the message that neither have much, if any, value to Putin or Russia’s leadership. Finally, this default will be the result of external aggression, not internal strife. Countries, like individual borrowers, can miscalculate, over-extend, and default. It happens. But today, the civilized world has spoken: Bullying the weaker “kid” next door will not be condoned. Should a country’s leadership intentionally push the world toward WW3 and/or nuclear armageddon, they will become a pariah.

Russia’s deep natural resource reserves may prevent complete insolvency and economic meltdown, but their access to the global capital markets is over. No one, perhaps with the exception of China, will lend them money now. And China has a whole host of problems on their own plate right now.

Sovereign debt defaults are interesting phenomenon. Since the time that Russia defaulted in 1998, Greece (2012), Argentina (2001, 2014, 2020), Venezuela (2017), Lebanon (2020), Ecuador (2020), and even Ukraine (2015) have defaulted on government debts. Each default was unique, but they were all the result of some sort of internal policy mismanagement within the country. While the Venezuela situation is debatable, none of these debt defaults were caused by a direct military attack on a neighbor, filled with clearly observable war crimes against innocent civilians. Today, the civilized world collectively agrees that those external acts are unforgivable.

Shall we grab a glass of Antinori Tasso Bolgheri, a beautifully grilled ‘prime’ filet Mignon, and head to the steakhouses?

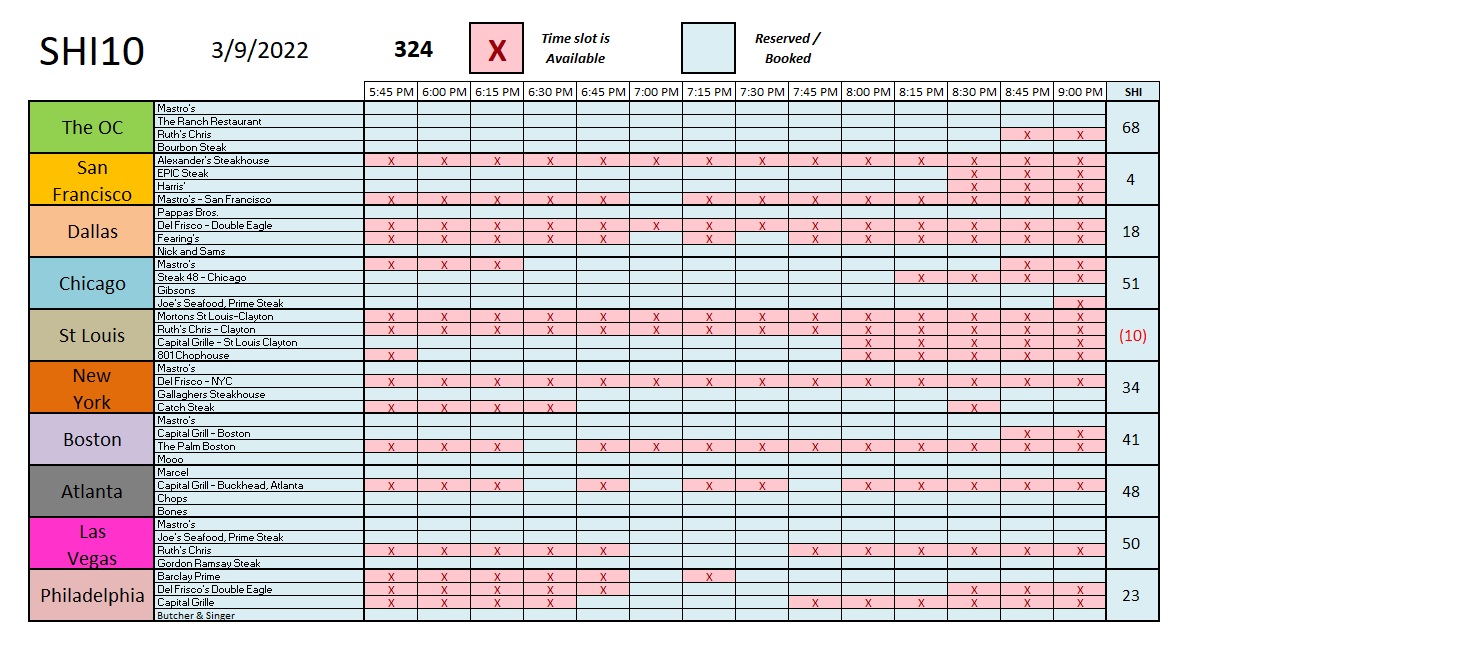

This week’s SHI10 is almost identical to the prior two. Take a look:

Once again, expensive eatery reservations are flying off the shelf in the OC; demand in ‘Vegas is as hot as the grills at Gordon Ramsey’s steak house; and, beef is in high demand in Chicago. Interestingly, week-after-week, reservations at the steakhouses in San Francisco are in low demand. Is this an economic commentary or a life-style choice? Has SF gone vegan? Hmmm….. 🙂

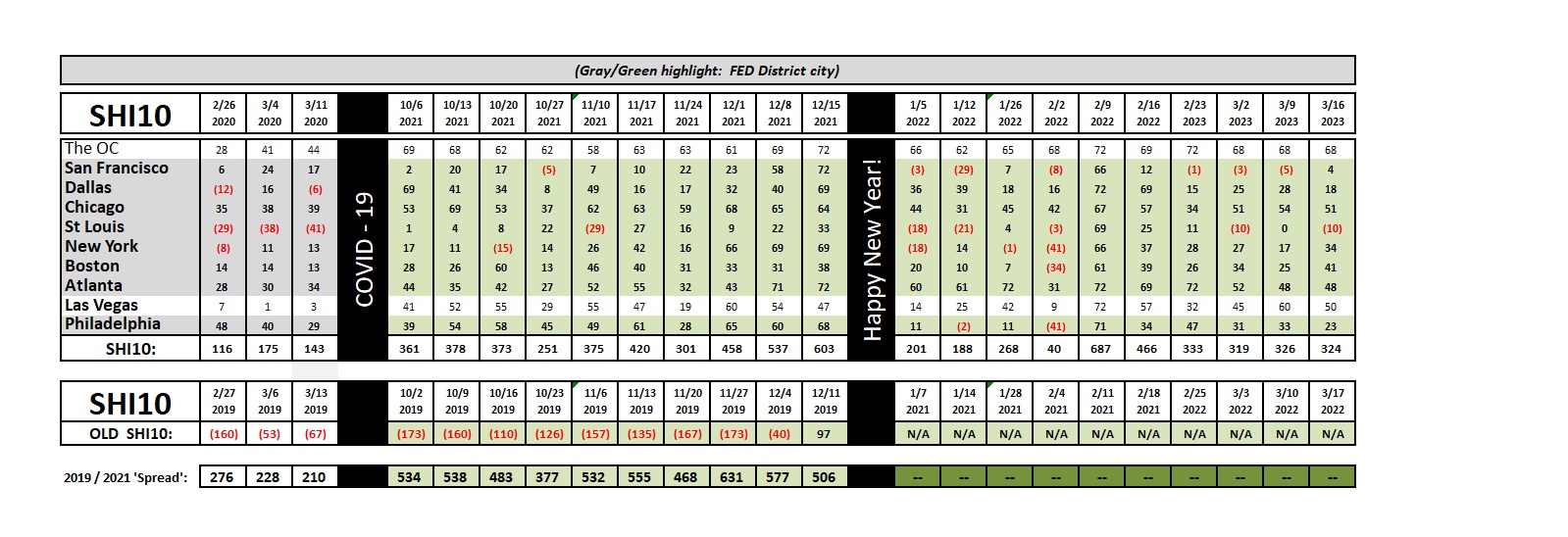

Here’s the trend report.

The SHI is telling us the US economy is steady-as-she-goes. All good here.

Hey: Here’s some good news! Well, for me anyway. Last week, I accurately predicted the FED’s rate hike!

The FED has finished their 2-day meeting and, as expected, they raised rates 0.25%. OK, OK, I know. Not overly impressive, right? After all, a couple of weeks ago, Powell pretty much said that’s what he planned to do. Effective immediately, the Federal Funds rate is now 0.25%. This is the first rate hike since December of 2018. Powell commented that during the meeting, members of the FOMC had productive discussions about the FED balance sheet, where ‘total assets’ as of 3/10/22 were $8.911 trillion, and they will continue to discuss “shrinking the balance sheet” in future meeting.

Since I did so well with my FED rate prediction, I’m feeling a bit frisky! How about another prediction? Ready? Here we go:

Right now, in real-time, we are witnessing the beginning of the end of globalization.

Bold, right? But I believe it’s accurate. That concept may seem a bit abstract to you, permit me a few comments on the topic, as well as the down-stream implications to you, me and the economy on the whole.

First, ‘globalization‘ manifests itself as the financial and economic tapestry woven stitch-by-stitch, year-by-year, country-by-country, since the end of WW2. Over the years, tighter and stronger bonds and supply chains linked consumers and countries across the globe, connecting people and products across boarders. Product costs fell, choice increased, and in the macro (my opinion) humanity was enriched. No, globalization is not all rainbows and unicorns, but I personally believe the good far outweighed the bad.

And then a global pandemic struck, spread and exacerbated by the deep global connections and integration of the people and countries of the free world. We all know what happened … and we’ve seen the broken supply chains, ‘critical supply’ (pharma, microchips, energy, etc.) security concerns, and on-shoring manufacturing talk. Again, I’m not suggesting these are good or bad outcomes. I’m a big fan of on-shoring and the long-term benefits to the US economy. But, like with all things, the proverbial ‘devil is in the details.’

The Russian invasion of Ukraine, to paraphrase again, put the nails in the coffin. Russia has been booted out of the global economic and financial systems. They are on their own. For the most part. Supply chains that began or ended in Russia are now, for the most part, permanently broken. Again, my opinion. Sure, some countries will trade with Russia — obviously that list includes China, Cuba, Venezuela, and others of that ilk. But Russia is now out of the club. On their own.

The Russian invasion of Ukraine will accelerate the de-globalization started by the pandemic. Countries will de-couple from the global system, when appropriate, as they consider the security needs of their citizens — thru the lens of medical, pharma, technology, energy and other critical supply needs. Essentially, the trust is gone. After decades of supply complacency, no longer do our leaders trust the system. And thus, de-globalization is here.

So, should you care? Yes. Because thru the economic lens, globalization and its highly integrated, well-orchestrated supply chains built over decades, were extremely anti-inflationary. Other problems (social, political) were created or exacerbated, but in the macro, globalization helped keep prices low. And I’m talking about food (think wheat, corn, soybeans); appliances (toasters, treadmills); products (basketballs, pasta, iPhones); and, the list goes on and on and on.

The bottom line: Expect the cost of just about everything to go up. Probably not forever, and perhaps not on everything. US technology and automation may be able to overcome some of the more detrimental impacts of de-globalization. But, in general, everything is going to be more expensive in years to come. Expect it.

My, my, I feel like Debbie Downer again. Sorry. 🙂

<:> Terry Liebman