SHI 5.27.26 – GENIUS or Dumb?

SHI 5.20.26 – Steaks Don’t Lie

May 20, 2026

SHI 6.3.26 – A Stairway to Heaven

June 3, 2026

Genius or Dumb?

In the rear-view mirror, factual developments in global finance and economics are easy to understand. Assessing human history is far more simple than making accurate predictions. What did Yogi Berra say about this? I think something like, “Prediction is difficult, especially if it’s about the future.” 🙂

Consider this piece of history: Growing US deficit spending in the 1960s triggered an M2 explosion; the M2 explosion destabilized the US dollar internationally; then, President Richard Nixon terminated the “gold standard” which ultimately led to the demise of the Savings and Loan industry within a decade or so.

“

A real-life economic murder mystery!“

“

A real-life economic murder mystery!“

Regulation Q became law in 1933 as part of the Glass-Steagall Act. About 40 years later, without notice or fanfare, Reg Q murdered the Savings and Loan Industry. Reg Q stabbed S&L industry right in the heart. Truth be told, it was probably more ‘manslaughter’ than murder. I don’t believe Req Q intentionally kill the S&L. But it did. Of that, there can be no doubt.

To tell this true story in a meaningful, financial and economic way, we have to travel back in time to the late-1960s and early 1970s. Ready? Let’s go.

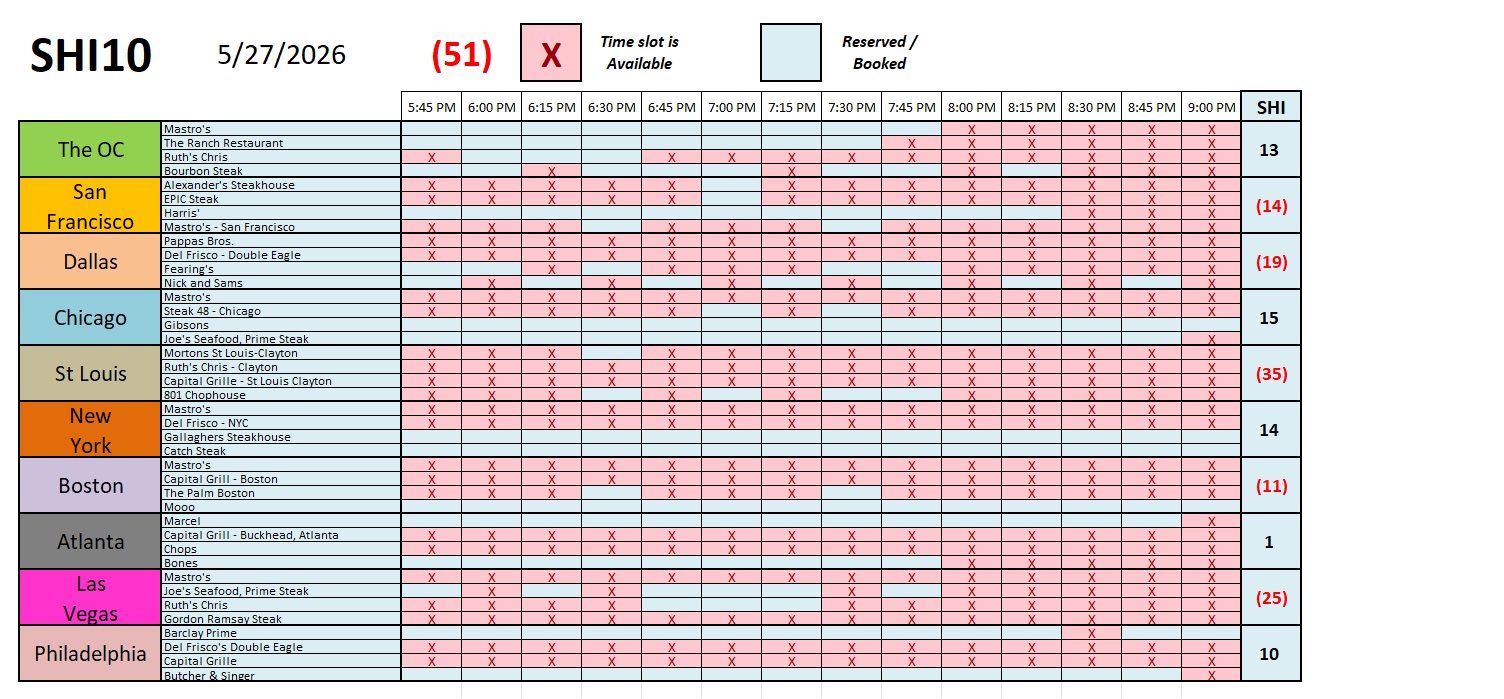

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. But is the US economy expanding or contracting?

Expanding … according the ‘advanced’ reading just released by the BEA, Q4, 2025 GDP grew — in ‘current-dollar‘ terms — at the annual rate of 5.1%.

The ‘real’ growth rate — the number most often touted in the mainstream media — was 1.40%. In current dollar terms, 2025 US annual economic output reached almost $31.50 trillion.

According to the IMF, the world’s annual GDP expanded to over $115 trillion in 2024. Further, IMF expects global GDP to reach almost $135 trillion by 2028 — an increase of more than 28% in just 5 years.

America’s GDP remains around 25% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

The Savings & Loan industry was born from depression-era regulation. President Rosevelt championed a sweeping spate of laws we now collectively call “The New Deal.” The “Federal Home Loan Bank” (often called the FHLB) was created, giving the Savings & Loan system new standards and far greater liquidity. Regulation Q was a cornerstone of Glass-Steagall: It “capped” the rate the S&L could pay to a depositor, thereby assuring the S&L of a profitable business plan – AS LONG AS SHORT TERM RATES STAYED LOW.

Which they did for about 40 years. Between the 1930s and 1970, short term rates remained stable and low. But then things changed. As they often do.

Inflation was the trigger. Inflation was out of control by the early 1970s. The cause, most economists agree today, was the massive expansion of US money supply, necessitated by the huge spending deficits from the Vietnam War. Between 1965 and 1971, money supply (known as M2) increased by more than 60%.

Did you know that post-WWII an ounce of gold was pegged at $35? Further, did you know that a foreign central bank with 35 US dollars could “convert” that $35 into an ounce of gold on demand? By the end of the 1960s, because they could, many overseas central banks – at an accelerating rate – opted to convert the US dollars they held into gold. Imagine a run-away freight train, filled to the brim with gold, leaving Fort Knox for England, France and oil-rich Saudia Arabia.

Struggling with this accelerating de facto emptying of Fort Knox, in August of 1971 President Richard Nixon did the unthinkable: He announced the US dollar would no longer be convertible into US gold. The “Nixon Shock,” as it is know known, ended foreign government’s ability to redeem US dollars for gold at the $35 price.

Imaging for a moment you are Saudia Arabia. By agreement, oil was priced in US dollars. So, essentially, you are trading your barrel of oil for a pile of US dollars.

But the currency debasement triggered by the massive money supply made those dollars less valuable. So imagine how you felt when the country issuing said US dollars announced that the security behind that currency, the guarantee that the US dollar had the value printed on the face of its currency, the assurance you relied upon when you sold all your oil in dollars believing you could use those dollars to buy other things, was quietly and consistently becoming worth a lot less money. And then, in an instant, the guarantee you could convert $35 into an ounce of gold was discontinued.

Saudi Arabia and the other OPEC nations were not happy. Not at all.

For the decade before the Nixon Shock, a barrel of oil had been priced at near $2.00. After the Nixon Shock, in 1972, OPEC negotiated for about a 25% price increase. And in 1973, they pushed for even larger increases to offset the loss of the dollar purchasing power: the posted price for a barrel of oil jumped to almost $3.00.

Unsurprisingly, as oil was in widespread use in the US economy, our inflation rate went thru the roof. As did short-term interest rates. By the mid-1970s, short-term interest rates were hovering between 8% and 12%. On the last day of 1979, the Federal Funds rate was about 13.8%.

Let’s circle back to the S&Ls. Under Reg Q, daily liquid “Passbook” savings accounts were capped at 5.25%. Commercial banks, on the other hand, were capped at 4.00%. Longer term CD rates were a bit higher, but they required the depositor “lock up” their money for the duration of the CD. 6-month CD rates were at 6%.

Given the evolving financial strains, it’s no great surprise that the innovative “Money-Market” fund was launched in 1971. It quickly became a desirable alternative to the S&L passbook savings account.

The first Money-Market account paid slightly more than the passbook account. But by the end of 1972, Money-Market accounts paid up to 5.8%. From there, it really took off: When 1973 ended, MM accounts paid 7.5% … and by the end of 1974, upwards of 9.00%. By comparison, that 5.25% rate at the S&L looked pretty darn paltry. It’s really no surprise that S&L depositors removed their funds and quickly deposited them into a high-yield MM account.

Inflation and Reg Q made way for the Money-Market account. Inflation on steroids in the later half of the 1970s triggered an explosion in MM accounts paying returns (say, 9%) far above those available at the S&Ls (limited to 5.25%), causing the largest deposit flight in US banking history. Money left S&Ls slowly at first, in a year or two the outward flow resembled a torrential river.

Why didn’t the commercial banks collapse as well? That’s a good question. After all, they paid a low return to their depositors too. However, banks were structurally different from the S&L. Remember, the S&L was designed to “borrow short” and “lend long”. The S&L primarily made 30-year fixed rate home mortgages using their depositors daily deposits. That was the primary purpose of the S&L. When those deposits left, they had an entire portfolio of fixed-rate, 30-year mortgages. And few deposits. They quickly became insolvent.

Commercial banks, for the most part, structured loans as variable against an index. They too were harmed by the rapid fund outflow to the MM funds, but not critically.

Now, let’s fast-forward to today.

The GENIUS Act is approaching its 1-year anniversary. It was supported by legislators on both sides of the aisle and passed with wide-spread support. But within this new legislation can we see seeds of future commercial bank failures? Or even worse: Obstacles for the US dollar? As the future evolves, could the GENIUS Act prove to be as dumb as Reg Q proved to be in retrospect?

JPMorgan has almost $5 trillion on their balance sheet. They are a behemoth. Yet about a couple years ago, JPM created a very non-bank type of asset: A brand new type of Money-Market fund. Technically, this is a US dollar tokenized and permissioned blockchain-based, institutional Money-Market fund. It has a ‘ticker’ but it does not trade on a public market or exchange.

By creating this product, JPM became the first major bank in the world to tokenize a Money-Market fund and offer it to institutional clients inside a proprietary, permissioned blockchain environment.

OK, what’s that all mean you ask? Here’s the essence. Recognizing the potential existential risk that digital currencies might pose to modern commercial banks, JPM decided to make an early move: They created their own digital fund backed primarily by short-term US treasuries. Using a digital blockchain to create digital tokens, this (theoretically) 100% safe and 100% collateralized institutional Money-Market is programable and permits its owners 24-hour-a-day access and fund settlement.

OK, what’s THAT all mean? Holders have instantaneous access to money every second of every day. Inside JPM. It’s 100% safe and completely digital. And it offers the ability to program payment functions. This product is called MONY. MONY is a tokenized share class of the JPMorgan Managed Reserve Fund, an institutional money‑market fund backed primarily by US treasuries. MONY yields about 3.5% to its owners.

Interesting. Why did JPM create MONY?

I’ll get back to that question in a moment. First, a bit more on the GENIUS Act.

This new regulation fully legitimized the stablecoin industry. It authorized the creation of a digital currency. And it strictly prohibited the payment of interest to stablecoin holders. The commercial banks fought hard for this prohibition. They were wise: Without it, their continued existence was in doubt. After all, commercial banks rely on very cheap capital to be profitable. Banks pay only about 0.07% APY for interest bearing checking accounts and only 0.38% for savings accounts. If stablecoin accounts, fully backed and secured by US treasury securities, were legally able to pay interest to their holders at around the rate of the short-term treasury, say about 3.6% APY, we would likely see a repeat of the S&L debacle. So, by law, stablecoins cannot pay interest.

So the banks won that battle. But did they win the war? I’m not so sure. I fear they may have inadvertently left the door to the castle open.

Even before this Act was passed, blockchain technology of the cryptocurrency industry was under intense scrutiny by commercial banks and others. Could it have a foundational use case in commercial banking? Might the technology have application to create a commercial bank digital currency? JPMorgan decided yes it might have that use.

700 years ago, if a large, aggressive marauding army attacked your castle walls, you defended it with everything you had. Even better: Build a moat! A moat can keep the enemy far, far away from the walls and gates.

And I believe that’s what MONY is. Essentially, it is a financial moat. And for a couple of years now, they’ve been testing it. It’s probably not available to you or me. Only large, institutional clients of JPMorgan can use this product for corporate treasury, collateral or settlement purposes. CoPilot suggests the minimum cash balance needed by a large treasury client is in the $50 million range. Who uses it? Likely the big guys like Amazon, Walmart, FedEx, etc.

But I’m wondering if the commercial banks missed their opportunity to regulate digital currencies and restrict the issuance of those currencies to commercial banks only? I’m wondering if they should have pushed for this provision within the GENIUS Act?

Not much later, early 2024 to be specific, BlackRock decided to pioneer here as well, announcing a similar money-market fund. BlackRock is not a commercial bank. They are not subject to the same regulations as commercial banks. And yet, just like JPMorgan they were able to create a digital currency.

Named BUIDL, an acronym for ‘BlackRock USD Institutional Digital Liquidity Fund’, this MM fund is also a tokenized blockchain‑designed financial product. It is also transactionally programable offering holders a perpetual, 24-hour-a-day access and settlement. BUIDL has current assets of about $2 billion today.

Like MONY, it’s not open to the general public. It’s not even open to ‘Accredited Investors.” To buy into BUIDL, an investor must be a “Qualified Purchaser” which is defined as an individual with $5 million or more in liquid investments. Research indicates that BlackRock intentionally designed this fund for Qualified Purchasers in order to avoid regulatory filings associated with public funds. BUIDL is paying owners a yield of about 3.45%.

But the JPMorgan and BlackRock digital currencies, I believe, set the stage for more. And if tokenized digital currency Money-Market accounts become widely available to you and I, paying a US treasury-sized interest rate, completely safe and secure, offering instantaneous access and settlement, might this cause a flood of money to move away from commercial banks into these funds?

No, I don’t think so. But what it WILL do, in my opinion, is change the financial plumbing at commercial banks. Their days of super cheap capital are probably over. To compete with non-bank digital currencies, they will have to offer their own. And they will have to pay a commensurate rate of interest.

If all this comes to pass, commercial bank ROIs might be at risk. And this might impact their viability and enterprise value. I’ll say this plainly: If tokenized, block-chain Money-Market accounts become common and widely adopted, I believe the value of banks and their bank share prices will decline. This is the door I believe they left open. I’m of the opinion they should have dealt with this and related issues in the GENIUS Act. Failing to deal with this inside the GENIUS Act will not prove fatal for the commercial banks, but it could prove dumb in the years to come. My opinion.

Digital currencies are coming. For good reason, central banks appear reluctant to dive in. But private enterprises seemingly see opportunity. As evident to these early movers. As digital currencies and stablecoins evolve, so will our traditional banking system. Keep your fingers crossed that we don’t see a “Reg Q type of intermediation” in commercial banking as an unintended consequence. That would be bad.

To the steakhouses?

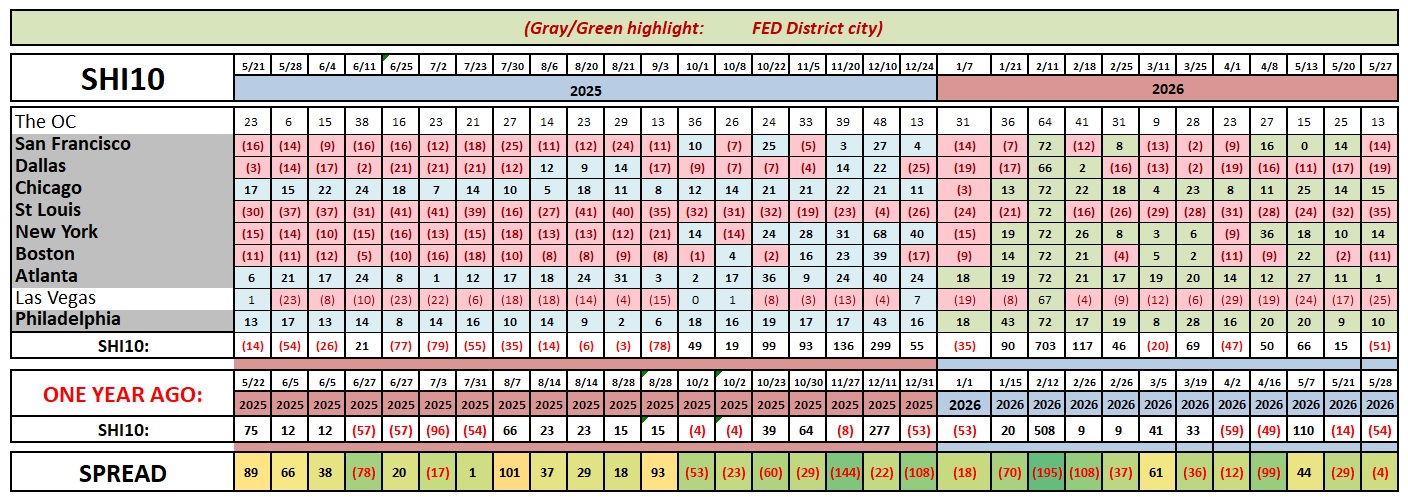

Above is this week’s chart; below, the longer term trend. Reservation demand in our California SHI restaurants is noticeably weaker this week.

But I don’t see any reason to consider this a trend. At first glance, this movement seems consistent with historic values.

The SHI10 is intended as an anecdotal proxy for the more mainstream economic data we get from more traditional sources. One resource that I often consider is the ‘GDPNow’, a weekly forecast produced by the Federal Reserve Bank of Atlanta. The next update is scheduled for tomorrow. The forecast from 6 days ago suggested that Q2 GDP will be 4.3%.

I am also expecting a strong reading. But an annualized rate of 4.3% would be stellar by any metric. Remember this is the ‘real’ GDP number — as opposed to the current-dollar figure. If the CPI is running close to 3% right now, this would suggest the US economy is expanding at the annual rate of over 7%. Staggering.

While this is a forecast, it is indicative. What I find even more amazing is this growth may have come before the overall economy has experienced the productivity expansion I believe will come from widespread adoption of AI inside commercial work flows.

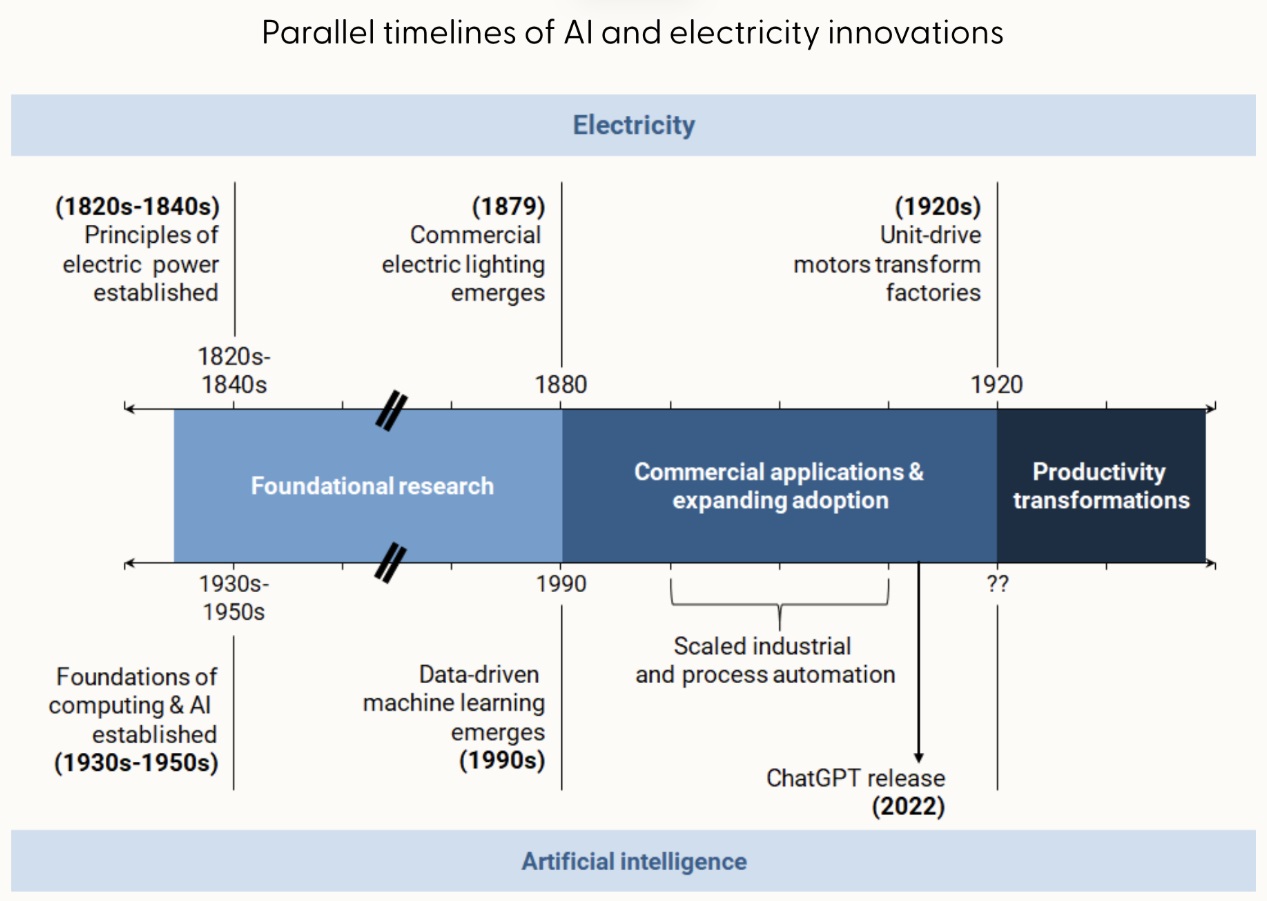

Mary Daly is the President of the San Francisco FED. The SF FED intently studies labor and capital productivity and produces excellent research on the topic. In a recent speech at the San Jose State University, Ms. Daly made these comments:

“Today, I’m going to talk about artificial intelligence (AI). Now standing here in Silicon Valley, many of you might find AI exciting, full of promise and possibility. For others, it may feel more worrisome, a potential disrupter to lives, livelihoods, and what it means to be human.

This is not surprising. People also had mixed feelings about electricity and the automobile, with some fearing them as dangerous, supernatural, even evil, while others imagined their potential, quickly adopting the novelty of driving or using electricity in their homes. Irrespective of where they stood, almost everyone wondered how these technologies would change the role of humans in the world.”

Clearly, she is acknowledging the turbulence inherent with the adoption of new technologies. And she’s driving home the fact that transformations take time. Consider the below image clipped from her Economic Letter:

If we’re already realizing a 4.3% (real) annualized GDP growth rate, imagine the unleashed power our economy will experience once the full effects of AI are realized? Staggering.

If you’d like to read Mary Daly’s full economic letter, click HERE

Time will tell! Thanks for tuning in.

-||- Terry Liebman -||-