SHI 3.23.22 – Is Recession Now Inevitable?

SHI 3.16.22 – It Will be Tough from Here

March 16, 2022

SHI 3.30.22 – Q1 Ends with a Bang

March 30, 2022

“We now see the risk that the U.S. enters a recession during the next year as … 20-35% … by models based on the slope of the yield curve,” said Goldman Sachs Chief Economist Jan Hatzius.

Why?

Well, it’s not because the US economy has been performing poorly. Quite the opposite. Until recently, that is. Reasons might include:

-

- FED and other Central Bank rate hikes.

- An inverted Treasury ‘yield curve.’

- Unresolved and war-exacerbated supply-chain bottlenecks and disruptions.

- Raging US and global inflation beyond just energy.

- Exceptionally tight labor markets, partially the result of a Covid-shrunk labor force.

- FED shrinking the ‘balance sheet.’

- Rising home-loan rates, with the 30-year fixed now averaging 4.72%

- The war in Ukraine.

- Russia weaponizing commodity exports.

- Commodity price turbulence and shocks.

- De-globalization and erosion of sovereign trust.

… and the list of headwinds goes on from there. So … is a US recession now inevitable?

“

Recession? It’s complicated.”

“Recession? It’s complicated.”

Remember: The US National Bureau of Economic Research (“NBER”) defines the word ‘recession’ as:

“… a significant decline in economic activity that is spread across the economy and that lasts more than a few months.“

And while that definition, in my opinion, lacks both context and quantification, it does summarize the concept fairly succinctly. The words “decline” and “a few months” are descriptive … and set the stage for a deeper dive into the topic. Ready to go? 🙂

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Significantly. During 2021, nominal growth clocked in at $2.1 trillion. The US annual economic output was just under $23 trillion for the full year. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

When I was a kid, I subscribed to Mad Magazine. I loved the irreverent and edgy humor, evident in their mascot Alfred E. Neuman’s unctuous smile, “What? Me worry?” … implying he didn’t have a care in the world. Now, many years later, much older and (in theory) wiser, I sometimes hearken back to the simplicity and peace of mind Neuman seemed to embody all those years ago. Things were certainly a mess back then — just like today — and he wasn’t worried. The world is no more complex or dangerous today; of course, the challenges are very different. But as much as things have changed, we faced obstacles then just as we face them now. So, should we be worried?

With a slight cringe and grimace, I have to say ‘yeah’ … we should be a little worried. Sorry Al. I’m having trouble maintaining my sanguine demeanor. 🙂

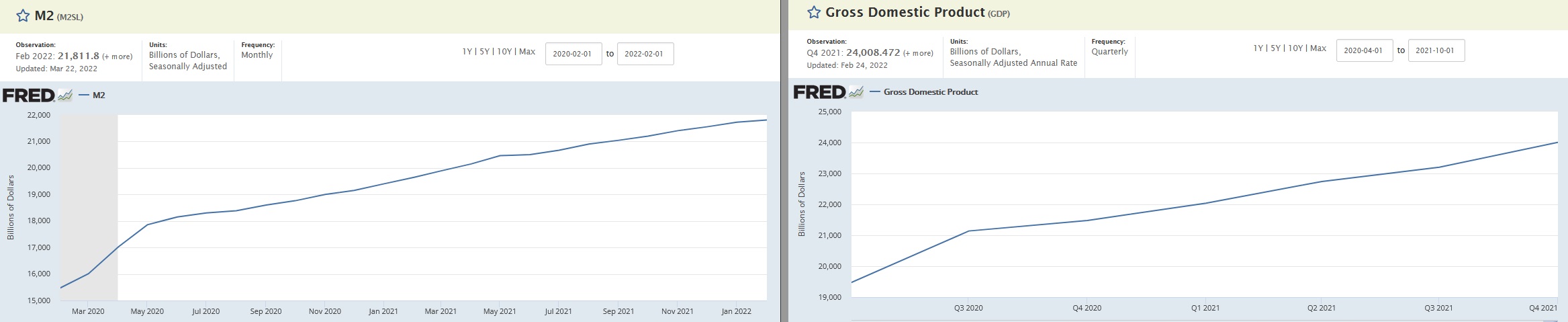

On one hand, in the counterbalance to all the recession talk, we have to consider the spectacular growth in the US money supply since the pandemic start. M2 increased from about $15.5 trillion in February of 2020 to over $21.8 trillion today — a staggering 41% increase. Consider this amazing fact: In only two years, the amount of US dollars floating around out there, available to spend, save or and invest, increased by almost 41%. Thru this simplistic lens, in a vacuum, perhaps we shouldn’t be surprised inflation has spiked.

But neither life or economics are quite that simple. Of course the infamous ‘Monetarist’ Milton Friedman would vehemently disagree with me. He would say that economics is that simple. Sort of. Even Friedman tempers the money supply growth = inflation ‘talk’ with a nod to GDP growth, suggesting that the inflation rate can remain relatively constant if the growth rate of money supply and nominal GDP are relatively aligned.

So were they aligned during 2020 and 2021? Did nominal GDP grow at about the same rate as M2 money supply? No. During that same period, nominal (current dollar) GDP grew by a little over 23% — from about $19.5 trillion up to a little over $24 trillion. So, effectively, thru Milton’s lens, the US experienced “excess” money supply growth of about 18% in the past 2 years. That’s quite a bit better than 41%, right?

The money supply issue, while critically important, doesn’t provide the whole picture today. Not even close. Today’s ‘economic’ world today is far more complex that during the times of Alfred E. Neuman and Milton Friedman. There was no pandemic to deal with. Millions of folks did leave the labor force back then, opting for an early retirement, as the pandemic raged on. Savings rates were much lower. Globalism was just a budding ‘twinkle’ 50 years ago: Supply chains were nowhere near as widespread, complex or integrated as they were in February of 2020. And the “natural” (normal) rate of interest, known as “r-star” or r*, was quite a bit higher in decades past.

No, things are very different these days. Thanks to the money supply growth and elevated savings rates, the US consumer — in the aggregate — has been able to shoulder much of the past price shock in food and energy. It’s worth mentioning that according to the Federal Reserve’s “Z.1 Report” …

“household wealth” increased by $33 trillion in the 2-years between the end of 2019 and the end of 2021.

That’s right. Household net worth increased from about $117 trillion …. up to over $150 trillion during this period. Which is the primary reason why I have felt a recession was unlikely, in spite of all the other challenges we faced.

But then Russia felt compelled to attack Ukraine … and a whole new set of problems arose. You may be surprised by the ‘chain of dependency’ the world has with Russia, and their natural resources:

-

-

<> Russia ranks number one, two and three, respectively, among the world’s exporters of natural gas, oil and coal.

-

<> Europe gets the bulk of its energy from its eastern neighbor.

-

<> Russia also accounts for half of America’s uranium imports.

-

<> It supplies a tenth of the world’s aluminum and copper, and a fifth of battery-grade nickel.

-

<> Its dominance in precious metals such as palladium is even greater.

-

<> Finally, as you’re probably aware, Russia is a huge supplier of wheat and fertilizers.

-

Perhaps the most shocking material on the list above is uranium. The US imports 1/2 of our uranium from Russia? Wow … I had no idea. And herein lies the problem. These supply chains are now very much at risk — if not already broken into pieces. There are talks that a wheat and fertilizer shortage could, conceivably, cause a new wave of global famine. Russia’s metals exports are critically important in many industries. And, of course, in current conditions, Europe’s dependence on Russian petroleum products is both massively inflationary and a massive threat to their economic growth.

Given the supply chain and material interdependence in place when Russia invaded Ukraine, and the disruptions and shortages likely to develop, I will be surprised if the inflation rate — here and in Europe — does not spike more than it has. And if it does, will the FED and the Bank of England react with even larger interest rate increases? Will ECB President Christine Lagarde join the fray … also raising short-term interest rates? So far, the ECB has resisted the urge … but can they stay on the sidelines if inflation spikes further?

The current inflation spike may have been transitory before the war, but no longer. De-globalization will speed up as the bonds of trust between countries, established over many decades, fades or evaporates. Shortages will become even more exacerbated … and companies will scramble to find new or alternative supplies of critically important materials and/or components. We’re in for a slog, folks. This will not be pretty.

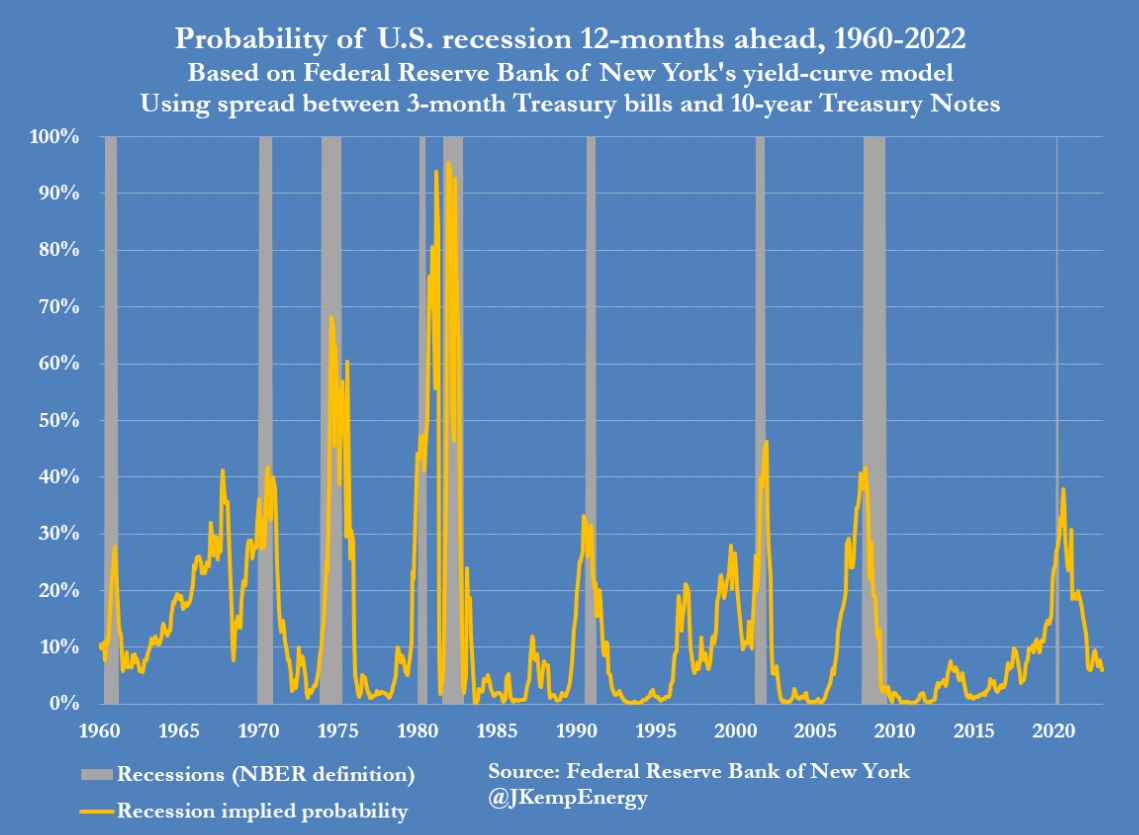

But this doesn’t mean a US recession is imminent. It might be … but the US economic system is so large and complex, it’s hard to predict. Sure, as Goldman indicated above, the inverting yield curve is indicative, but while some models are flashing red, others are not:

According to this more than 60-year chart of the model at the New York FED, US recession odds are still quite low.

As I sit here today, I feel the EU is far more likely to enter a recession than the US during Q2 of 2022. The demand destruction resulting from their excessive over-reliance on Russian energy is likely to cause, in the words of the NBER, a “decline” in economic activity for much more than “a few months.” Given the excessive inflation rates Europe is likely to experience in the months to come, combined with an expected slowing in their economic activity, a recession in Europe is quite likely. But here in the US conditions are far different than across the pond.

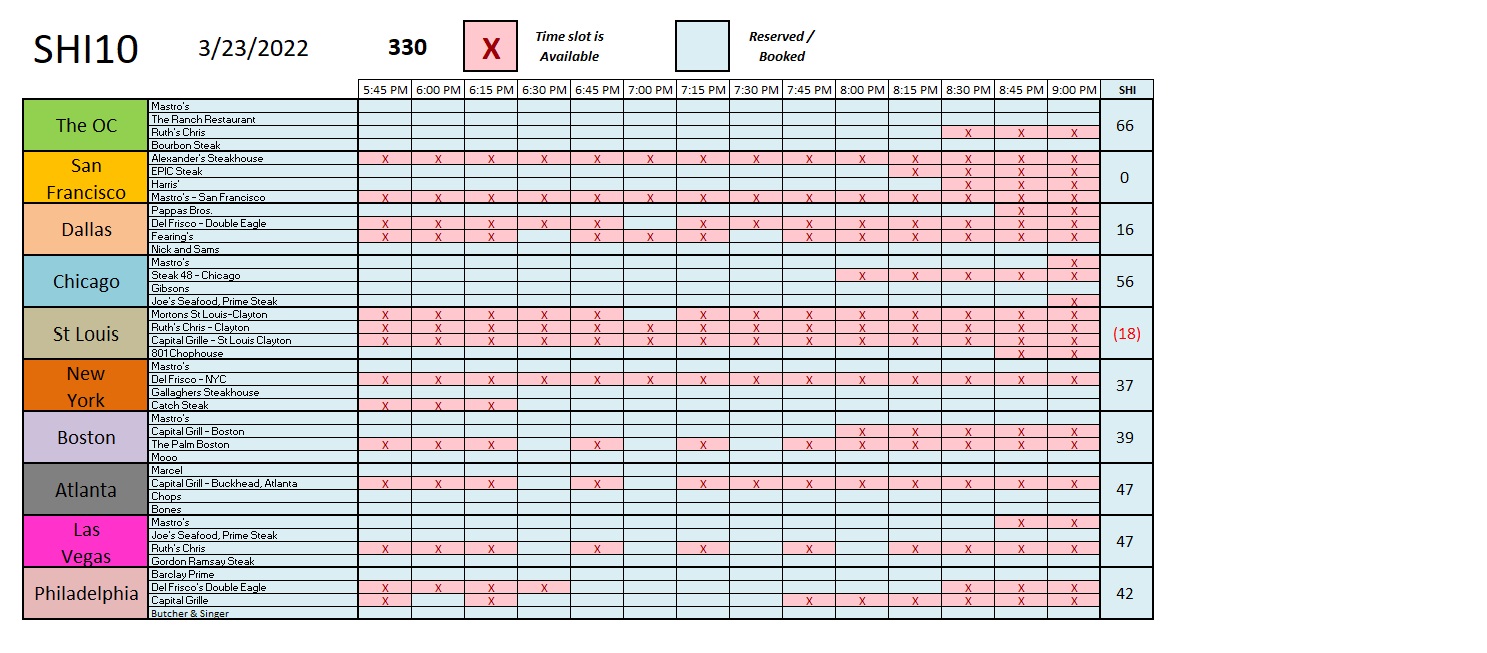

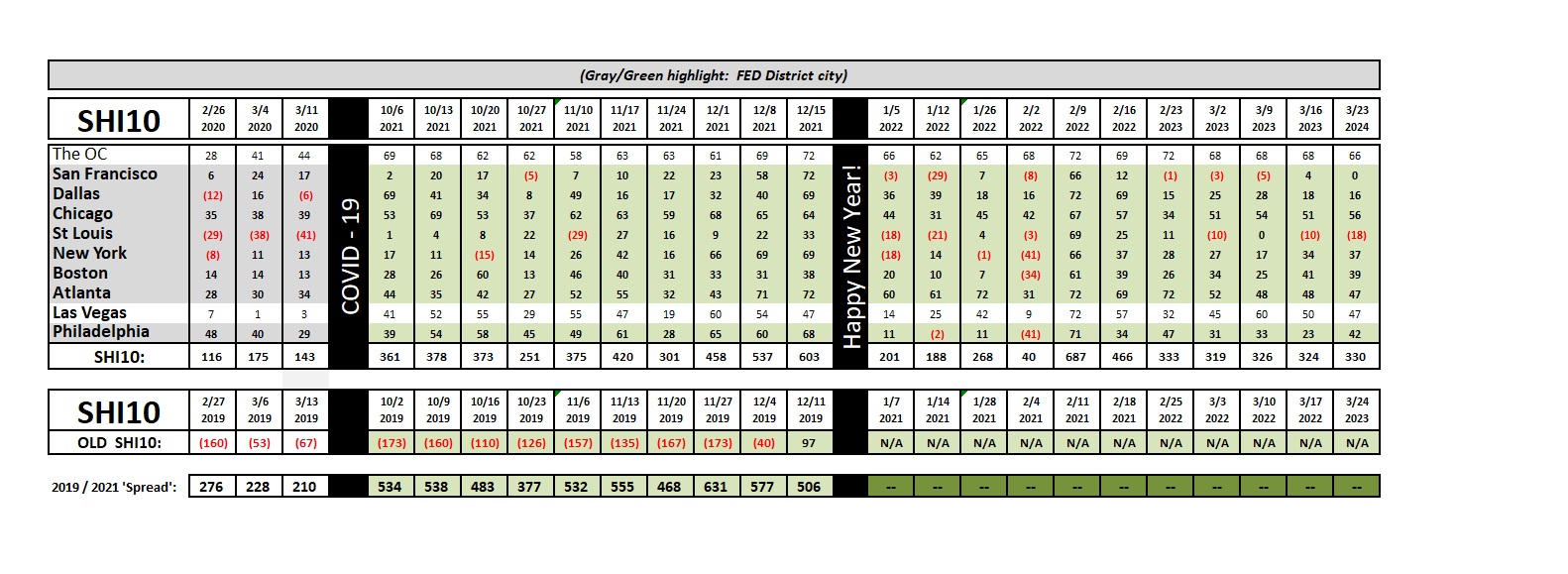

So, in my mind, the jury is still out. Let’s see what the steakhouses are telling us:

Not much of a change here from last week. Folks here in the OC still have a strong hankering for an expensive steak; the vegans of San Francisco are still shunning the steakhouses; and, only St Louis has an SHI in the red. It’s not ‘rare’ to find an open table at their opulent eateries. Conditions in the other SHI cities are very similar to those we saw last week:

Right, not much change, other than in Philly, where the spring thaw may be encouraging hibernating meat-eaters out of their caves and into Barclay Prime. 🙂

I’ll summarize with these comments: As I said above, our economic picture complicated. It may be simple for the steakhouses right now … but the US and global economic damage is just beginning. And so is the FEDs response to the economic, political and human challenges that may result. Things are very much in flux … and so we’ll just have to patiently watch and see how they unfold.

Maybe Alfred E. Neuman was right. What? Me worry?

Right.

<:> Terry Liebman