SHI 2.24.24 – Well, That Was Interesting

SHI 4.17.24 – Wine and EVs

April 17, 2024

SHI 5.1.24 – Look Out Below, The Yen is Falling

May 1, 2024

Today is Thursday. Sorry about the one-day delay, but I wanted to see today’s GDP report before completing this blog.

And I’m happy I did. The report exposed some very interesting, very explosive data. The stock market cratered at the open — the DJIA was down more than 700 at one point — but the markets recovered as the day progressed. Even so, the “explosion” left a giant hole in the ground where the S&P used to be. Inflation fears are back!

“

Today’s GDP report exposed a

serious challenge for the FED.“

“Today’s GDP report exposed a

serious challenge for the FED.“

And for the stock and bond markets. Both of which have been expecting a FED rate cut. I have not been expecting a rate cut — I’ve been expecting robust GDP growth. Which is what today’s GDP report verified. Of course, the media is painting today’s outcome as disappointing — below the expectation and forecasts from the Atlanta and NY FEDs. They are wrong. GDP growth remains quite strong.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. But is the US economy expanding or contracting? Expanding …. By the end 2023, in ‘current-dollar‘ terms, US annual economic output rose to an annualized rate of $27.94 trillion. After enduring the fastest FED rate hike in over 40 years, America’s current-dollar GDP still increased at an annualized rate of 4.8% during the fourth quarter of 2023. Even the ‘real’ GDP growth rate was strong … clocking in at the annual rate of 3.3% during Q4.

According to the IMF, the world’s annual GDP expanded to over $105 trillion in 2022. Further, IMF expects global GDP to reach almost $135 trillion by 2028 — an increase of more than 28% in just 5 years.

America’s GDP remains around 25% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Sure, ‘Gross Domestic Product’ grew by just 1.6% in the first quarter of 2024, according to today’s report from the Bureau of Economic Analysis. Disappointing, many analysts are saying.

Pure bunk, in my opinion. Remember: that’s the ‘real‘ increase, annualized, for America’s economy. The ‘current–dollar‘ GDP gain was 4.8% — identical to the current-dollar gain in the prior quarter. Identical. (Note: The Q4, 2023 current dollar figure was just upgraded to 5.1%.) This bears repeating: The Q1 2024 current-dollar GDP gain exactly matched the Q4, 2023 gain. Everyone thought Q4 2023 was great … so why is today’s number bad? Essentially the two readings were the same! Why did the stock market tank and bond yields spike?

From the ‘real’ GDP number alone, I would have thought today’s stock market behavior would be somewhere between boring at best and tepid at worst. But, no, nothing could be further from the truth. Stock and bond markets cratered today.

The GDP number, in itself, was not a market mover. No, the big market-mover number today was the number 3.4%. That number is the “personal consumption expenditure (PCE) price index” (the “PCED“) used to deflate the “current-dollar” GDP increase of 4.8%, on an annualized basis, to make it ‘real.’ That’s where the 1.6% number came from. Consider these facts: America’s GDP increased by $327.5 billion in Q1 … on top of a $346.9 billion gain in Q4, 2023. Interestingly enough, year-over-year, ‘real’ GDP growth is up 3.0%. ‘Current-dollar’ growth is much, much higher.

No, the markets sold-off today because the “inflation-fear trade” is back. Fear is back. Fear of rates staying “higher for longer” or — GASP! –a FED rate increase! Bond yields rose to a 5-month high today as a result. No, reading the data here, the FED will probably not cut rates any time soon.

The PCED was calculated at 3.4% this past quarter — up from just 1.8% in Q4, 2023. For a market that was expecting more of the same, the 3.4% reading was, definitely, a bit too hot. So, for now at least, rate-cuts appear to be off the table.

Yardeni does a great job tracking this type of data. Take a look at the chart below:

This quarter’s number is quite a spike (the vertical blue line on the right). But the yearly change — the red line — is clearly moving in the right direction.

Your take away today: Interest rates will be staying higher-for-longer. C’est la vie. To the steakhouses?

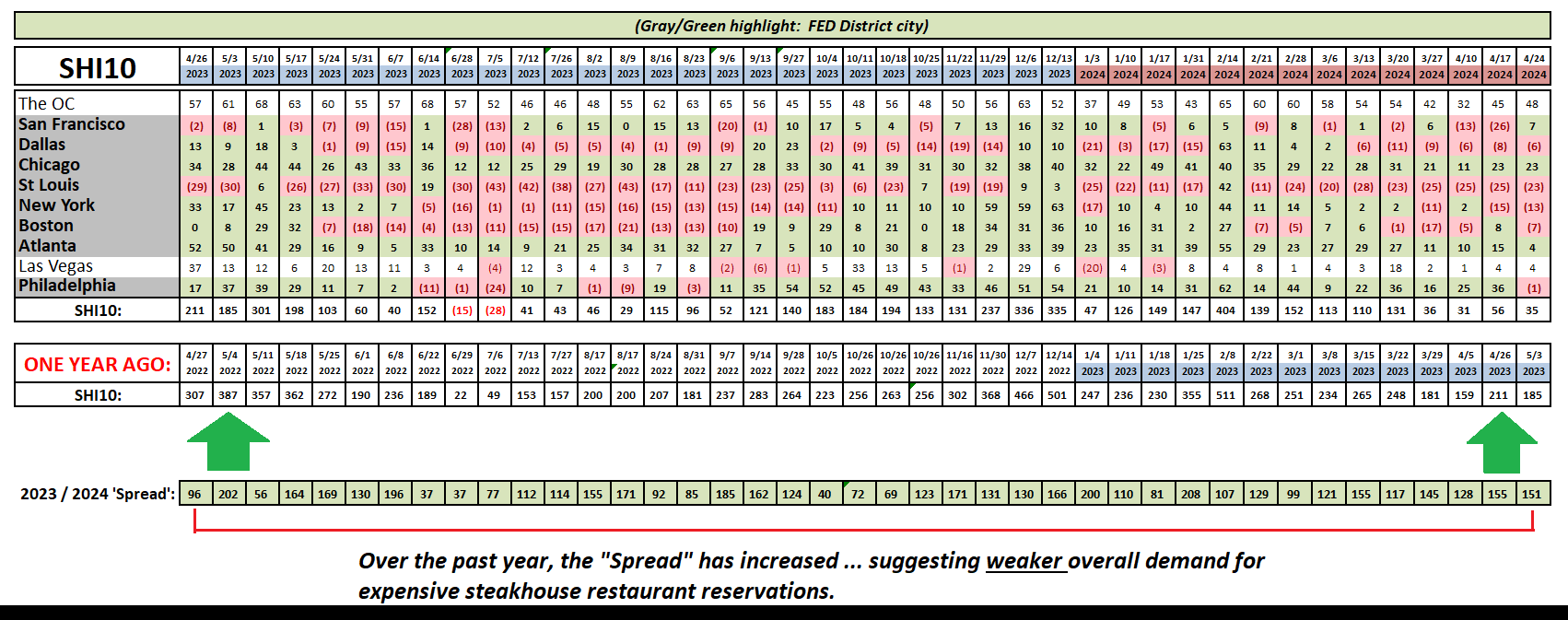

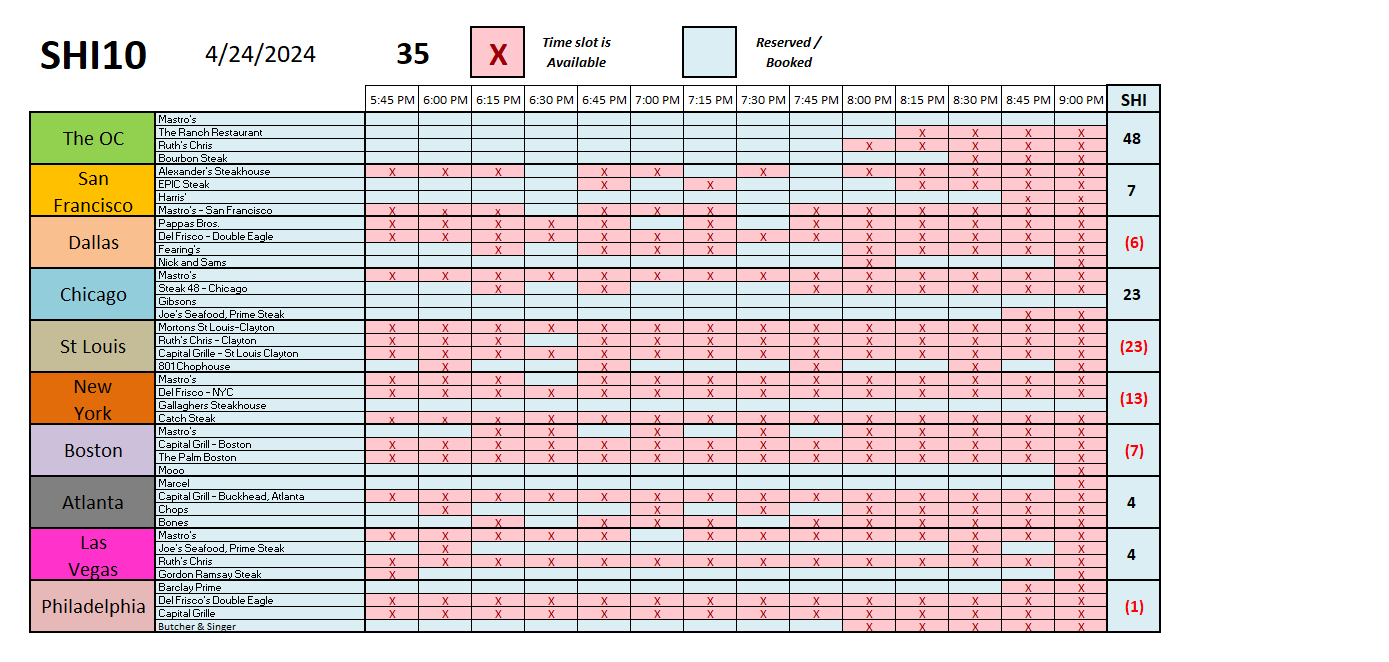

High level, demand for expensive eatery reservations are down from a year ago. They are consistent with recent readings … but definitely trending down over time. Most markets showed improvement this week, with only Philly falling off a cliff. Here are the individual restaurant results:

It is interesting to me how well our economy is performing under the weight of higher rates. Surprising, to some extent. But there you have it. Our economy continues to do quite well.

<:> Terry Liebman