SHI 3.30.22 – Q1 Ends with a Bang

SHI 3.23.22 – Is Recession Now Inevitable?

March 23, 2022

SHI 4.6.22 – Navigating Binary Choices

April 6, 2022

Both literally and figuratively. The first quarter of 2022 ends today … what a ride!

You may recall that almost exactly one year ago today, the SHI posted a blog that was quite outlandish. Downright unbelievable, in fact:

SHI 4.1.21: Face North to Maximize Investment Gains

And it was. Unbelievable, that is. The blog was mostly the work of a ‘guest blogger,’ the esteemed Mr. William Baldwin, who graciously agreed to help me with an “April Fools” day prank. I hope you enjoyed it as much as I did.

There will be no repeat this year. Current events are sufficiently outlandish and need no embellishment. So while April Fools Day may be tomorrow, everything in today’s blog is the gospel truth. Honest. Seriously. Really. You gotta trust me here. 🙂

“

Things are changing fast.”

“Things are changing fast.”

The first quarter of 2022 is now in the rear view mirror. And the world is rapidly changing and adapting.

And while we’d all agree 2020 and 2021 had no shortage of nail-biting moments, so far 2022 is one for the record books. We’ve seen the highest inflation rates in decades. Wild stock market swings — both down and up. Mortgage rates soaring up more than 50% from their lows. The threat of recession now looms large over Europe … and perhaps here in the US as well. The list goes on and on … And, of course, we have a war in Europe. Wow. What a difference from just one quarter ago. Amazing. And things are changing fast — broken supply chains are causing, or will soon cause, a lot more pain.

In some respects it’s hard to imagine that in a world flush with capital and wealth, many folks around the globe may find the balance of 2022 to be exceptionally difficult. But I fear that is precisely what’s in the cards.

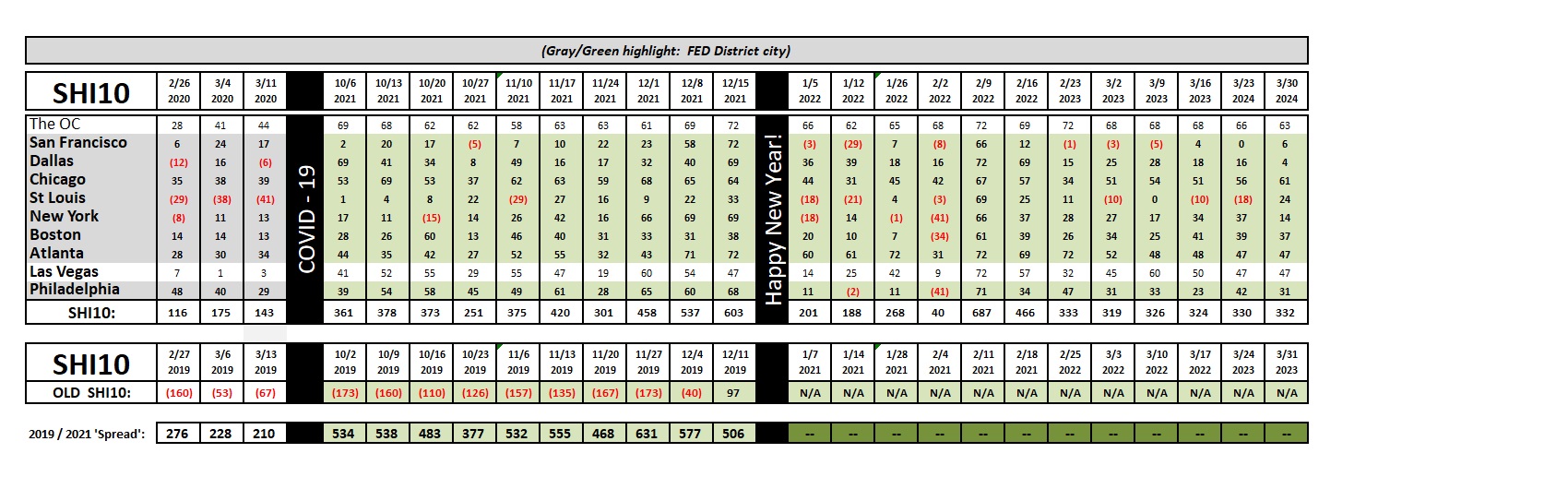

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Significantly. During 2021, nominal growth clocked in at $2.1 trillion. The US annual economic output was just under $23 trillion for the full year. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

History is replete with difficult time periods. Here in the United States, arguably the most difficult time was probably about 90 years ago. Ninety years ago this March, Franklin D. Roosevelt, the newly elected President of the United States, took the oath of office for the first time, at the depths of the Great Depression. He became the leader of an America that was almost broke and broken.

On Wednesday, March 1, 1932, governors in 17 states closed their banks to prevent runs that would have rendered the banks insolvent, declaring a ‘bank holiday.’ The Federal Reserve reported that $229 million of gold had been withdrawn in just the prior week. Consider this: The Treasury did not have sufficient funds to meet federal payroll; nor did they have sufficient cash to “pay” the $700 million of short-term certificates due 2 weeks later. The Stock Exchange was officially closed. By Friday the 3rd, another $500 million had been drained from the banking system.

“Banking in every state was wholly or partially suspended,” says William Manchester in his opus “The Glory and the Dream,” my source for much of the history here.

The very next day, May 4th 1932, Roosevelt was sworn in and became the United States President. Lucky guy, right? The country was almost completely broke. And the spirit of it’s people, broken.

Which makes the Bretton Woods Agreement of 1944 all that more amazing. A little more than 12 years later, newly victorious from the Second World War, and now the most powerful and wealthy nation in the world, the United States controlled about 2/3 of all the worlds gold deposits. And delegates from across the globe agreed that world currencies would no longer be pegged to gold … but to the US dollar, which, itself, was pegged to gold. And thus, by 1945, the US dollar became the world’s reserve currency. Let me repeat that:

In 1944, the US controlled more than 65% of all the gold in the world.

From the darkness and depths of despair just 12 years before, the United States had risen up and achieved global hegemony. How did that happen? From almost missing payroll in 1932 to become the wealthiest nation in the world … in less-than a baker’s dozen of years? There must be a fascinating story beneath the surface.

Things change.

Roosevelt’s first speech, after the Oath of Office, included these words, which you may have heard before:

“So, first of all, let me assert my firm belief that the only thing we have to fear is fear itself — nameless, unreasoning, unjustified terror which paralyzes needed efforts to convert retreat into advance. In every dark hour of our national life a leadership of frankness and vigor has met with that understanding and support of the people themselves which is essential to victory. I am convinced that you will again give that support to leadership in these critical days.”

“The only thing we have to fear is fear itself.” Wow.

Days later, by Sunday evening, Roosevelt was ready to act. Using the obscure “Trading with the Enemy Act” he declared a 4-day bank holiday. All banks were temporarily closed. But he had to find a way to get all that withdrawn gold back into the banks – and out of the hands of “hoarders.” He decided to use public embarrassment.

On Wednesday, March 8th, the Federal reserve made a national announcement: The FED would prepare and distribute a list of people who had taken gold from the banks … and the newspapers would print it all: Names, amounts, etc. It worked: Fearing exposure, people lined up in long queues to put gold back into the banks – banks that opened their doors for deposits only. By Saturday, the Federal Reserve had recovered $300 million in gold. Within a week, 13,500 of the country’s banks – 75 percent of them – were back in business, the stock exchanges opened and the Dow Jones jumped up by 15%.

Things change.

From Manchester’s book, I was fascinated to learn that John Maynard Keynes visited the White House and Roosevelt in 1934. Imagine being a fly on the wall during that conversation: Spouting personal economic theories not published until the following year (in 1935), Keynes attempted to convince Roosevelt that using deficits, the US could “spend its way to prosperity.” At that time, such theories must have seemed insane …. 🙂

Things change.

The Glory and the Dream is a masterful book, highlighting 4 decades of US history starting with the deep and painful depths of the Great Depression. This book of more than 1,300 pages is well worth your time – if only for the first 100 pages. Our America of today, by comparison to the conditions Manchester lays out 90 years ago, is a cakewalk for most of us. However, things are about to change, due to Russia’s invasion of Ukraine.

As bad as US food prices are today, they are likely to get much worse. I fear the US will soon suffer significant additional food inflation — beyond what we’ve already experienced. However, far worse, is my expectation that widespread famine and starvation are now possible — even likely — as a direct result of Putin’s invasion of Ukraine.

Just as the lingering Great Depression brought hunger to many families in the early 1930’s, a yet underappreciated result of Russian invasion of Ukraine could be many very hungry people later in 2022. Back in 1932, when asked about why the US needed federal relief programs considered controversial “in the long run,” an architect of those programs commented to Congress, “People don’t eat in the long run, Senator; they eat every day.” The same is true today.

According to The Economist, “War in Ukraine will cripple global food markets.”

In the US, this will likely manifest as much, much higher prices for food. But much of the developing world will fare far worse.

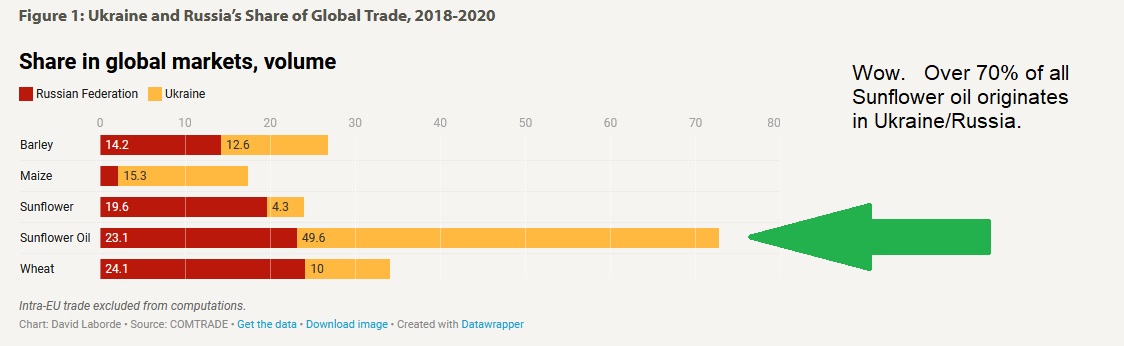

Russia and Ukraine, together, account for more than 30% of all international wheat sales. Recent poor harvests and pandemic-inspired hording have left global stocks of wheat 31% below the historic 5-year average. Fast-forward to today in war-torn Ukraine: Importers of “Black Sea” wheat aren’t getting their imports because Ukrainian ports are closed; some have been bombed. Boats trying to pick up grain from Russia have been hit by missiles in the Black Sea. The greater risk in Russia is more ‘blockaded exports’ than lack of production. But in Ukraine, future crops are in serious doubt at the moment.

The chart above, provided courtesy of the International Food Policy Research Institute (IFPRI), shows the amazing prominence of Ukraine/Russia in these grain markets. Corn is also a large export. The worry is easy to see: With bombs exploding and missiles flying, less farm area will be planted, further exacerbating global supplies. And even if planted, their production, harvest and exportation is in doubt.

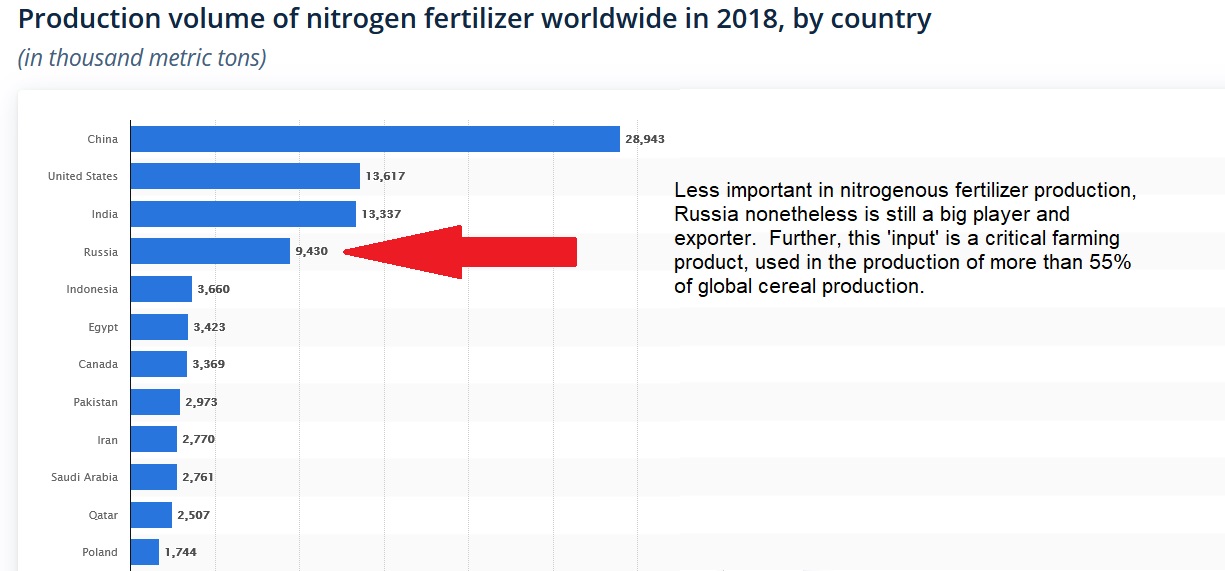

Add to this an additional problem: Fertilizers. Already reeling from record high prices, fertilizer costs are about to get much, much higher. Which, in turn, will drive food and grain prices much, much higher.

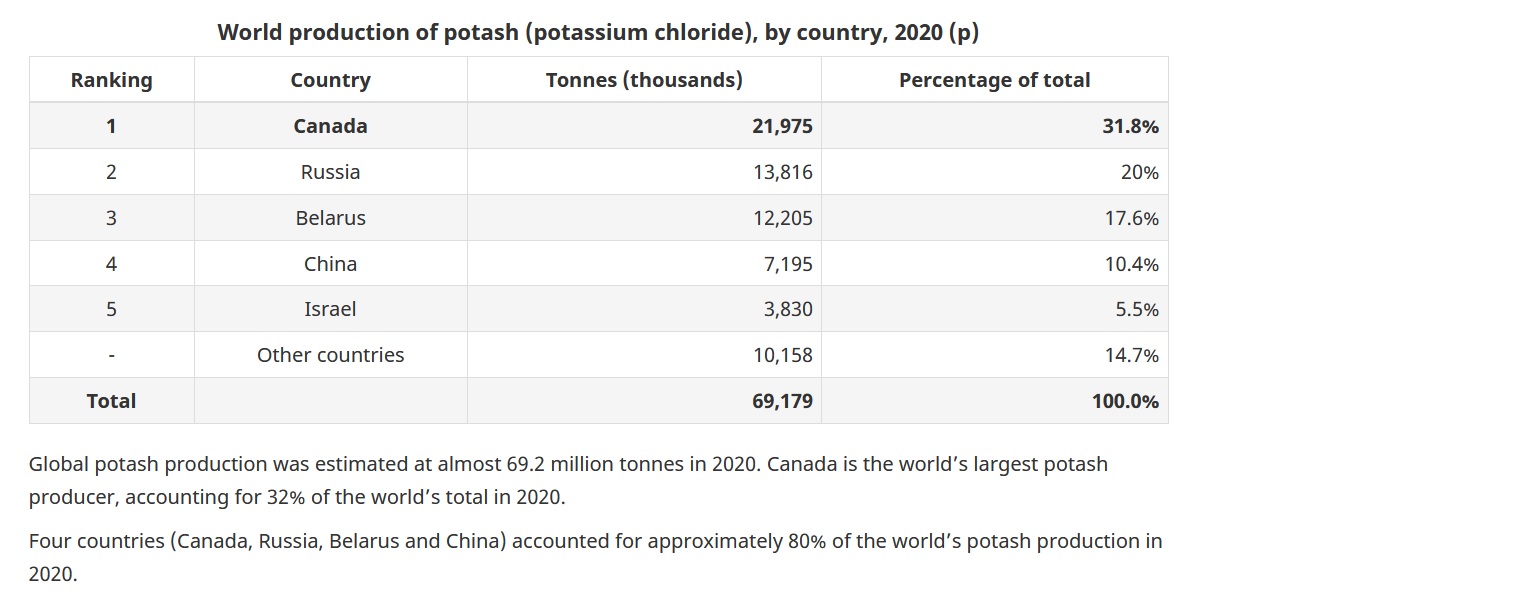

The US is a fairly large producer of nitrogen-based fertilizer. Almost double that of Russia. The bigger obstacle is the production of potassium, known in the fertilizer biz as “potash.” Potash is the name given to a group of minerals and chemicals that contain potassium, a basic nutrient for plants. And more than 1/3 of the worlds potash supplies originate in Russia and Belarus.

According to the IFPRI, farmers in western Africa import between 50-70% of their nitrogen and more than 90% of their potash fertilizers. China imports more than 50% of it’s potash; Brazil — a huge corn and soybean producer — more than 60%. (Annually, Brazil produces about 1/4 of the world’s corn output and more than 40% of global soybean output.) And even if nitrogen and potash are available for purchase this year, they are sure to be prohibitively expensive.

We all know the developed world has been focused on challenges within the global petroleum system. For good reason: Because of Russia, global supply is constrained. Western Europe — and more specifically Germany — is in a world-of-hurt right now, given their historic reliance on Russian imports. Prices for natural gas are thru the roof in the euro-zone. But for a variety of reasons, citizens have not yet felt the pain. I believe that will change in Q2. The euro-zone will feel the pain of exceptionally high energy prices in Q2. And they will feel the price sting and shortages developing within food and grain supply chains. I feel recession in Europe is now inevitable, if not during Q2 than certainly within Q3.

However, as bad as Europe’s near-term future looks, the future looks even bleaker for much of Asia, Africa and South America. Grains, and grain-producing inputs, if even available, are soon to become more expensive than ever. I’m envisioning a tsunami of cost increases for corn, soybeans, wheat, barley, etc. If I’m right, the cost of literally every food product will soon skyrocket. Why? Because the price of “farm” and “ranch” outputs, to a great extent, is directly correlated with the cost of the inputs. What is “corn” used for? Livestock feed. All over the world. So if fertilizer costs skyrocket, it’s likely the same will happen to grains, meats, dairy, etc.

Could I be wrong? Sure. And I hope I am. But everything I’m reading suggests a cost tsunami is on its way.

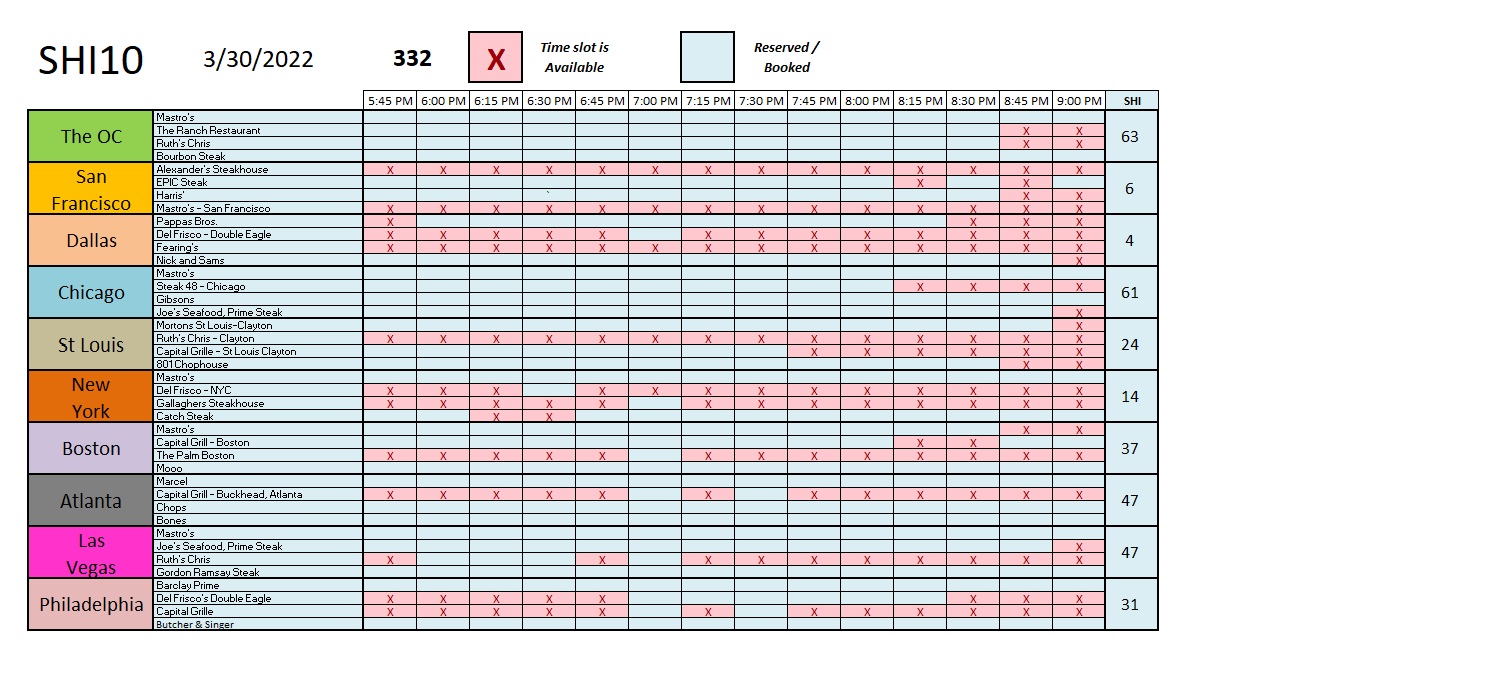

A friend recently told me my blogs have become quite depressing. I hear you, man. That’s not my intention, but I understand your point of view. I hate to be a Debbie Downer … but I have to call it how I see it. And here’s how I see it: As you can see from the SHI10 chart below, there are a fair number of open tables this Saturday in many of the 40 expensive eateries we track. Not many here in the OC or in Chicago, mind you, but the other 8 SHI cities have fairly good availability. I suggest you go to your local steakhouse this weekend. Take a few friends. Why? Well, first, as crazy as this sounds, the New York strip and filet prices at Mastros or Ruths’ Chris right now will probably look down-right cheap in 6 months. And second, that bottle of wine you like to enjoy with your steak? That is certain to become far more pricey too. So as expensive and opulent as these steakhouses are today, prices in 6 months are likely to be a whole lot higher! I see the tsunami coming … so before it hits, get out there and enjoy yourself ASAP!

At a reading of 322, this weeks SHI10 is right in line with previous readings. As you can see in the long-term chart below, while we see ebb and flow within the 10 SHI cities, in the aggregate, the SHI10 hasn’t moved much. Take a look.

By now, you may be asking: “What’s this all mean to me?” Great question … here’s what I think:

- > You should consider eating expensive steaks at our opulent eateries sooner than later. Prices are going up. Soon.

- > You should stock up on your favorite wines. Wine supply may not be in jeopardy, but glass bottle prices are sure to rise.

- > Don’t stockpile ‘perishables,’ but you might consider buying any ‘durable’ goods you’ve been putting off. Like a new washing machine or waffle maker.

Did I mention wine? You should definitely buy more wine.

It is extremely hard to gauge the downstream impacts of the Russian invasion and war vis-à-vis US GDP growth rates. Recall that ‘real’ GDP growth is deflated using an inflation factor. So it is entirely possible that here in the US, we see a 2022 ‘nominal’ GDP growth in the 5-8% range, but at the same time, actually enter a “recession” because the applicable GDP deflator rate is even higher than the nominal growth rate. That is quite likely, given current conditions. Further, rising food costs could possibly cause consumers to (1) substitute for less expensive products, if available, or (2) reduce overall consumer spending somewhat. I don’t yet believe this is likely, given the massive savings balances in consumer bank accounts, but I’m keeping a close eye on this possibility.

Which brings us full circle back to the FED. On one hand, CPI inflation is high and likely to rise further — further irritating politicians, the FED, and the general public. On the other hand, the number of economic heavy headwinds developed economies are soon to be facing are growing fast and furious and recession possibilities are now greater than ever. Will the FED stick to their programmatic rate increase schedule if European and US data suggests a slowing economy? Another great question … and one harder to answer, in my opinion, than the “food cost tsunami” that I believe is very, very likely.

Yep, I’ve become Debbie Downer. Sorry.

<:> Terry Liebman