SHI 4.6.22 – Navigating Binary Choices

SHI 3.30.22 – Q1 Ends with a Bang

March 30, 2022

SHI 4.13.22 – This Just In!

April 13, 2022

Let’s get ready to RRRRRRRRUUUUUUUUMMMMMMMMMMMMMMMMMMMMBLE!

The FED must backstop two very different opponents in the economic fight today. Their choice is unfortunately binary – they are forced to bet on one and only one.

Here’s the boxing announcer introductory play-action:

In corner #1, the current heavyweight champeeeeeeen of the world: FULL EMPLOYMENT! After the bone-crushing employment collapse, causing 20 million to lose their jobs seemingly overnight, less than 18-months later the post-Pandemic monetary and fiscal response ignited economic activity, just about everyone who wanted a job got a job. Amazingly, with the unemployment rate now clocking in at 3.6% (while lower in early 2020, this is the lowest unemployment rate in over 50 years), US employers still seek over 11 million new workers and wages are rising faster than they have in decades!

In the opposite corner, corner #2, weighing-in like an 8,000-pound gorilla: RUN-AWAY INFLATION! The combination of the post-Pandemic fiscal and monetary response jet-fueled liquidity and money supply, while at the same time, supply-chain disruption severely reduced quantities of goods available for purchase. The resulting imbalance — excessive demand with inadequate supply — triggered a “bidding war” of sorts and a rapid rise in consumer prices. Adding further fuel to the fire (yes, that was an oil pun), Russia’s invasion of Ukraine has caused further destruction of both commercial trust and supply chains across the developed world, likely cementing additional near-term producer price inflationary pressures in both agriculture and commodities.

What a fight! Who will you bet on?

“

Let the fight begin!”

“Let the fight begin!”

The US economy has been growing like a weed. ‘Current-dollar’ GDP grew at 14.5% during the 4th quarter of 2021! On an annualized basis, GDP increased by OVER 800 BILLION DOLLARS during the quarter! But that economic expansion rate, while exceptionally impressive, is now paired with exceptionally high inflation. Which is something the FED now wants to stop. Without, of course, throwing the US economy into a recession. Can the FED tame the inflation gorilla?

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Significantly. During 2021, nominal growth clocked in at $2.1 trillion. The US annual economic output, in nominal terms, finished 2021 at $24 trillion for the full year. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

We tend to forecast future events based on past experience.

It’s human nature to do so. And this is where we find Powell’s bigger foe: Not inflation itself, but aggregate long-term inflation expectations. This is the true opponent. If the FED can successfully bob-and-weave between the two opponents in the ring, while preventing high-inflation rate expectations to firmly root, then they may win this fight without ruining the economy.

The problem is the 8,000-pound gorilla is already out of his cage and rampaging thru town. Like a tornado in a trailer park, the gorilla will do more damage before it moves on, but the majority is already in his wake. The FED can talk a tough game, and the financial markets will react as markets do, but the proverbial pig is already deep in the python here. For the first time in decades, the inflation genie is out of the bottle and no amount of FED posturing or effort will get it back in. (My god, Terry, that’s a lot of metaphors.)

That is, of course, assuming the FED cares about the US economy and truly wishes to prevent a horrible recession. Do they?

Sure. But preventing a recession is their second choice. If forced to make the binary choice, they will pick crushing the inflation monster.

Also remember: This ‘fight’ is happening right now, in real-time, against the deflationary backdrop of (1) a land war in eastern Europe and (2) an almost certain recession in Europe and China into recession in 2022. That’s right: Europe AND China. You’ve already seen my comments on Europe. But today, I’m throwing China into the deep end of the recession pool, too. President Xi seriously miscalculated when he crushed China’s housing industry. That was dumb and heavy-handed. And now, with COVID running rampant all over the country, and 80% of new cases appearing in Shanghai, Shanghai is in complete lock-down. The entire city of over 28 million must stay home. No work. No shopping. Stay home. For context, consider this: The entire state of California has about 39.5 million people — the city of Shanghai alone has population equal to about 70% of California! Can you imagine the hit to California’s economy if everyone was forced to stay home indefinitely? Ouch.

China, a country notorious for statistical fibbing, claims the city had 13,000 new infections on Tuesday. Applying “China-Math” to this number … let me see … multiply by 88, carry the 3, divide by .003, subtract 44 and VIOLA! The actual number is 675,993 new cases on Tuesday! Trust me on this … the math works. 🙂

The point here is China is now in deep yogurt – economically speaking. Their housing market slowdown has already taken a huge toll on economic growth … and now, 2 years after the rest of the world entered COVID lock-downs, China is deep in the mix. According to the WSJ, at least 390 populous areas are now under lock-down in China. Changchun, a city of about 5 million and a major manufacturing hub, has been locked-down for almost 4 weeks. Serious economic storm clouds are forming over China. An economic slowdown is very likely.

My point here? Simply this: The FED must tightrope walk the inflation/employment wire, all the while considering the potentially deflationary implications of recession in Europe and China. This math is more complicated than “China-Math.” So, let me caution you to take all “news” with a grain of salt. The landscape is evolving quickly … and no matter what you read, hear, think or believe today, it may change tomorrow. Stay loose! Economically speaking, of course.

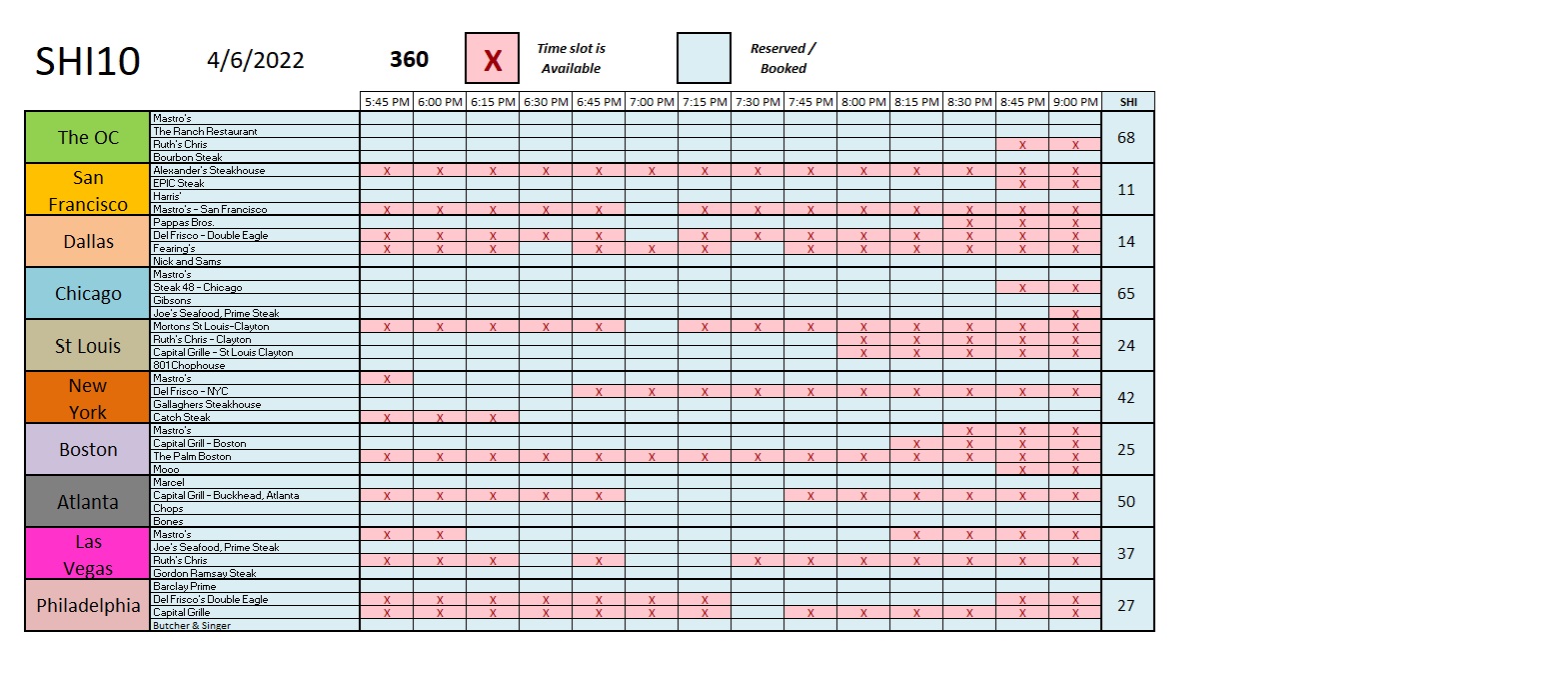

OK … to the steakhouses!

Today’s SHI10 is similar, once again, to last week’s chart. A few more San Franciscan neanderthal meat-eaters have existed hibernation and made expensive eatery reservations this Saturday. And a few in Philly went back into the cave. Otherwise, today’s SHI reading is consistent with what we’ve seen over the past month or so:

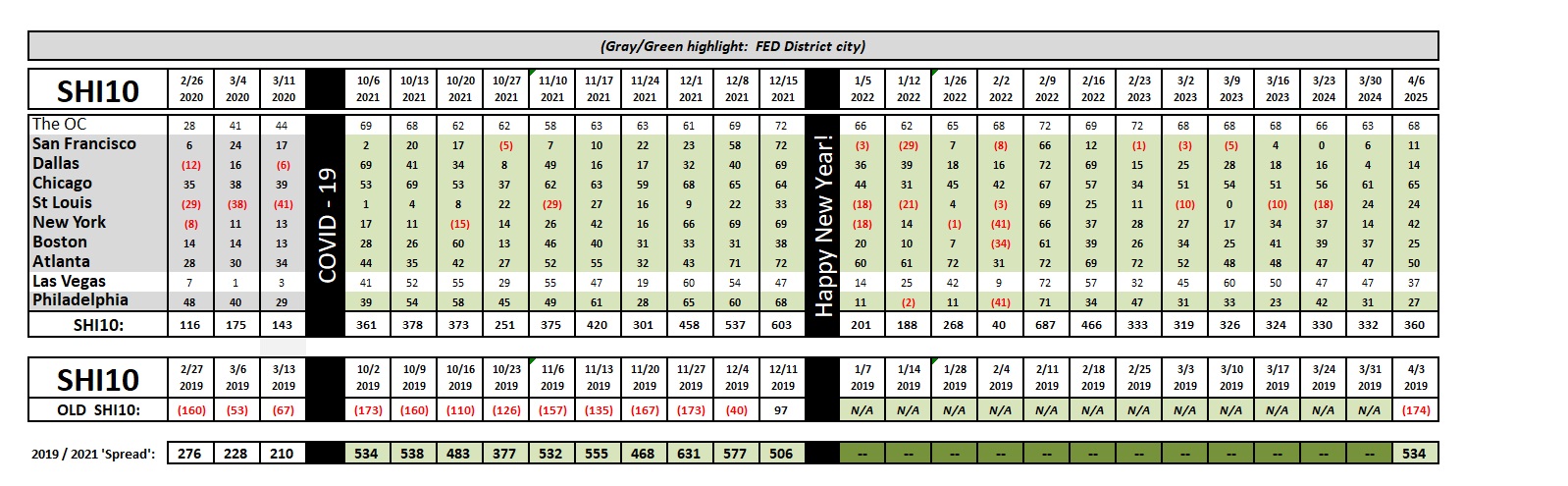

Note that the “spread” is back! Yes, we can now compare current pricey steakhouse reservations to a similar week in 2019. As we see above, reservation demand at present is far greater than this week back in 2019. So far, FED machinations aside, the SHI10 suggests the economy remains sound.

In the final analysis, the FED really has only King Solomon’s choice today: They must select “none of the above.” They cannot split the economic baby. Well, somewhat. If forced, the FED will let the US economy falter in order to crush inflation expectations. I’ll repeat: NOT inflation … but inflation expectations. But unless forced to make that choice, the FED will walk the wire. They must delicately walk a tightrope between the two … talking tough on inflation, but carefully navigating to prevent massive job losses and a deep recession.

They can easily crush inflation if they choose – but they cannot do so and simultaneously keep the US expansion intact. If they do make the “Volcker Choice” and recklessly lift short-term rates into the stratosphere, they can expect an unemployment rate over 10% and a deep recession. With only these binary options, I believe Powell will choose neither. They know they cannot control inflation at this moment in time. The genie was out of the bottle once Russia invaded Ukraine. However, with aggressive posturing, they may be able to control inflation expectations. If they can prevent expectations from becoming intractable, they may be able to stay up on the wire, delicately balancing between the two exceptionally difficult choices.

The minutes from the last FED meeting was released to the public this morning.

https://www.federalreserve.gov/monetarypolicy/fomcminutes20220316.htm

From the minutes, I quote: “Prices of commodities that Russia exports, particularly oil and natural gas, soared over the period. While oil prices partially retraced late in the period, options prices suggested considerable probability that oil prices could remain elevated or rise further in the months ahead. Alongside the rise in commodities prices, measures of near-term inflation compensation increased sharply across advanced economies.”

I’ll repeat what I said above: These events are outside their control. No matter what they hope to do … their focus must be on the public’s inflation expectation.

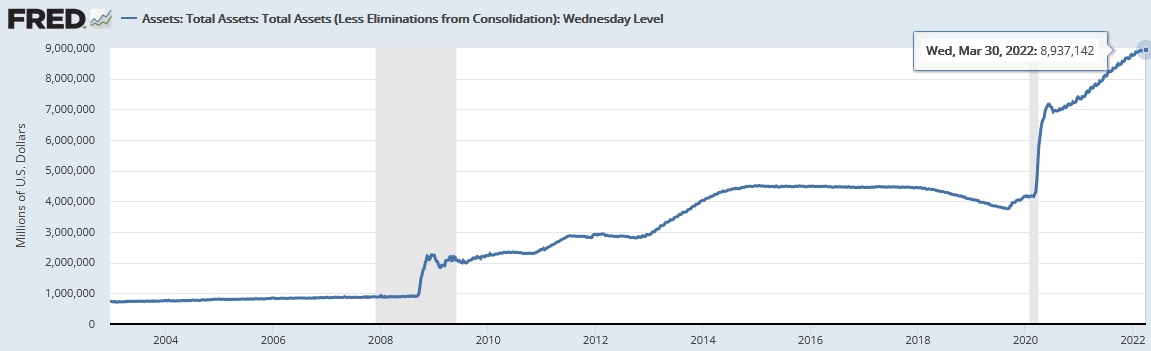

Above is a ‘clip’ from the FRED website, showing the current level of FED assets (balance sheet) as of the end of March. Almost $9 trillion in total.

Also per the minutes from the last meeting, they now plan to reduce this balance, permitting ‘run-off’ of $95 billion a month — $60 billion in Treasuries and another $35 in mortgage-backed securities (MBS). So, if today the FEDs assets total $8.937142 trillion, and they start to ‘shrink’ at this rate, in 1 year the balance will be down to about $7.8 trillion. At this rate, they will drain about $1.1 trillion of liquidity from the markets per year. Frankly, in the big scheme of things, this isn’t much. In my opinion, this is a fairly benign move. And it is probably reflective of their concerns in Europe and China.

Can the FED win this fight and keep America out of a recession within the next year or so? Time will tell. But for now, good news: Our economy is robust and economic activity is strong. Stay tuned! 🙂

<:> Terry Liebman