SHI 4.13.22 – This Just In!

SHI 4.6.22 – Navigating Binary Choices

April 6, 2022

SHI 4.20.22 – Regulation Nation

April 20, 2022

Have you heard the news? Inflation is running HOT!

Right. Everyone knows that. Even people on the International Space Station know that. But here’s something you may have missed:

“

Putin vows Russia will return to the moon.”

“Putin vows Russia will return to the moon.”

Yup. I kid you not … apparently Putin can multitask! This spellbinding nugget was reported in today’s Wall Street Journal.

I have so many questions: Does he plan for Russia to “invade” the moon … like he did the Ukraine? Could Putin believe Russia is threatened by both Ukranians and martians? Alternatively, it’s entirely possible he saw the above photo and said to himself, “Hey, that moon is close! … it might be easier for us to invade there since martians are pure fiction.” Or, if invasion is not the plan, what’s the point? Does the Hermitage plan to expand its moon-rock collection?

Who knows. And perhaps more importantly, who cares. As news goes, this is a complete yawner. Especially as it was reported in the same WSJ issue that proclaimed, “Putin Says Ukraine Peace Talks Hit Dead End.” Now that’s news … unfortunate news, but news nonetheless. The moon thing? Yawner.

Perhaps you’ll find this next morsel a bit tastier — I certainly did! From the Q4, 2021 Ruth’s Hospitality Group public report, the parent of Ruth’s Chris restaurants shared this fact:

“Total beef costs increased 43% compared to the fourth quarter of 2020.”

Ouch. That’s painful. After all, we are the Steakhouse Index … not the moon rock Index. Putin could be heading to the moon simply to get away from high steak prices … one of his favorite breakfast foods after a rigorous weights regime.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Significantly. During 2021, nominal growth clocked in at $2.1 trillion. The US annual economic output, in nominal terms, finished 2021 at $24 trillion for the full year. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

The moon is no closer to the Earth today than last year, but beef prices are sky-high. Thus causing the entire staff here at the Steakhouse Index to ponder a few interesting questions: Might expensive eatery reservation demand fall if steak prices rise appreciably? Or is any noticeable reduced demand attributable only to economic slowing? On a tangentially-related topic, I don’t know about you, but to my eyes I’ve observed no change in traffic patterns at $3.00 gas and $6.00 gas. Can the same be said for expensive T-Bones?

Have pricey steakhouses raised their prices? Yes. Just about everyone in the restaurant ‘biz’ has raised menu prices. Unappetizing, according to Nation’s Restaurant News, “Restaurant chains from Burger King to Noodles and Company to Texas Roadhouse to Shake Shack all announced menu price increases during their quarterly earnings during this earnings season.” However, to date, my anecdotal read from internet-based research suggests the price increase, so far, have been fairly tame. Especially when compared to the restaurant cost increases — in all areas.

Thus, any reduction we might see this week in reservation demand is more likely associated with this:

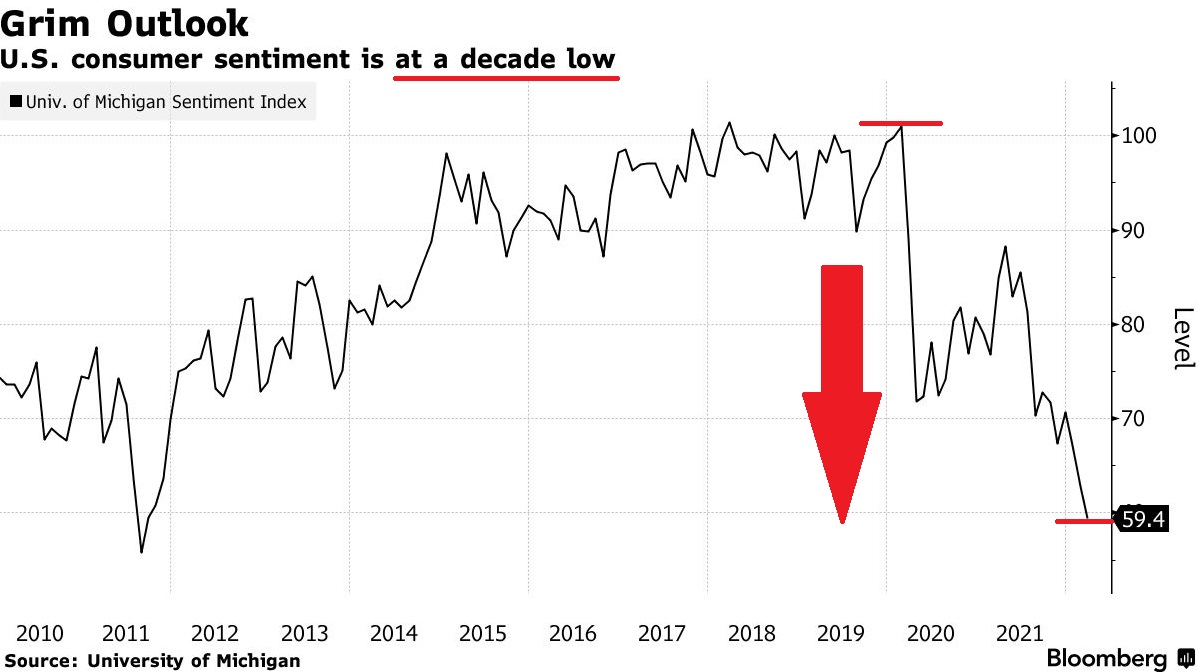

Yes, the consumer is quite unhappy these days. Consumer Sentiment, based on consumer surveys by the University of Michigan, is at a 10-year low. Significant price increases in gas, food and housing are all very front-of-mind, resulting in a very unhappy consumer. As about 2/3 the US economy is reliant on consumer spending to support GDP growth, this is certainly troubling. Often, an unhappy consumer is a frugal consumer. Which, in turn, is bad for economic growth.

Of course, it’s entirely possible that the remaining $2 trillion of government stimulus still sitting in American bank accounts will be spent whether the consumer is happy or not. And while they are rising a bit, levels of non-housing consumer debt remains quite low … so we see a lot of potential spending power there, too. Only time will tell which “feeling” is more powerful: Unhappiness or the typical urge to SPEND ALL THAT MONEY IN THE BANK … AND THEN SOME!

Interestingly, from a FED of New York survey entitled “Survey of Consumer Expectations” from about the same time, we learn consumers believe that while the median one-year ahead “inflation expectation” increased to a “series high” of 6.6%, the median 3-year ahead expectation declined, slightly, to 3.7% (from 3.8%) during the month of March. So, to repeat, per the March 2022 NY FED survey, consumers feel inflation will go up quite a bit in the short-term (1-year) … however over the next 3-years or so, they’re feeling a little more optimistic about inflation levels.

So what’s our take away here? Simply this: After a decade of exceptional price stability, the changes are fairly ubiquitous. Humans are generally not big fans of change. And so these rather adversarial price changes are not making folks happy. Will it cause them to change their behavior? A great question, to be sure. As I said above, I’ve noticed no thinning of traffic on the LA freeways in response to higher gas prices. Time will tell.

Here’s the NY FED survey, if you’re interested:

https://www.newyorkfed.org/microeconomics/sce#/

Let’s pop over to the steak houses.

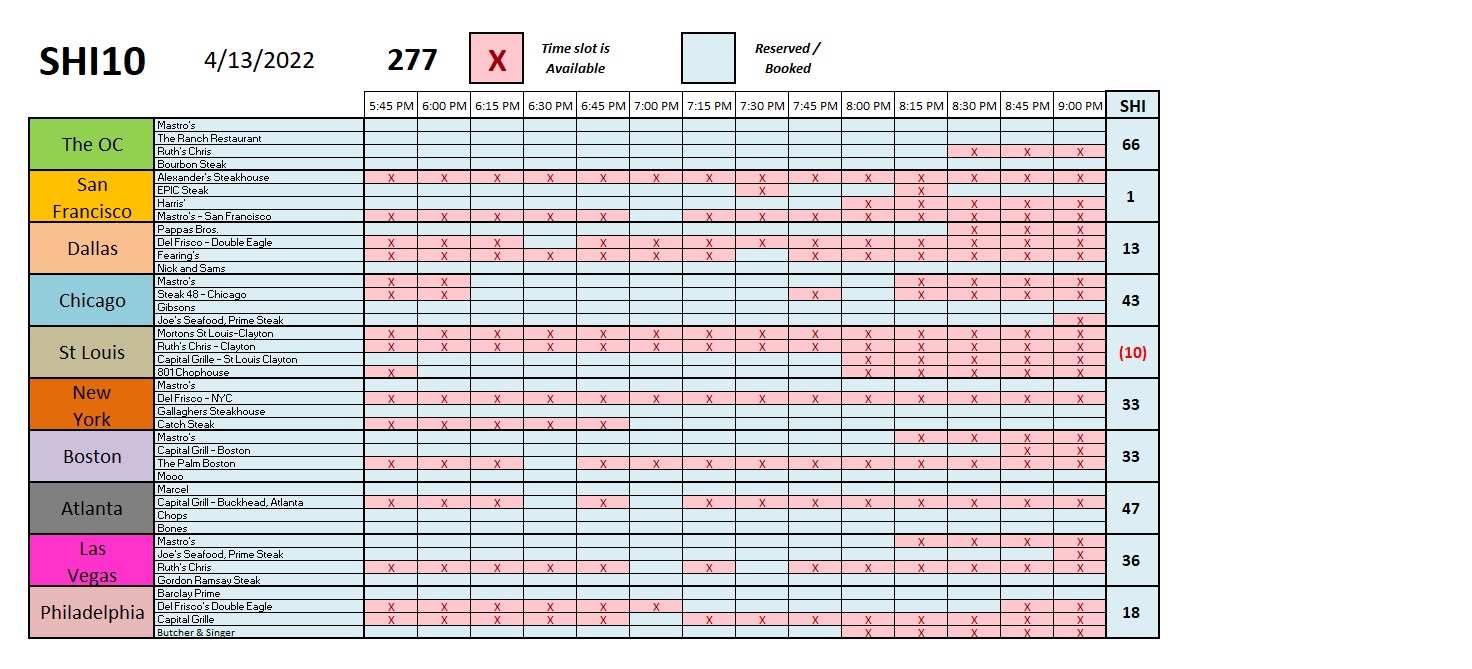

Interesting: Today’s is the lowest SHI10 reading since January. Take a look.

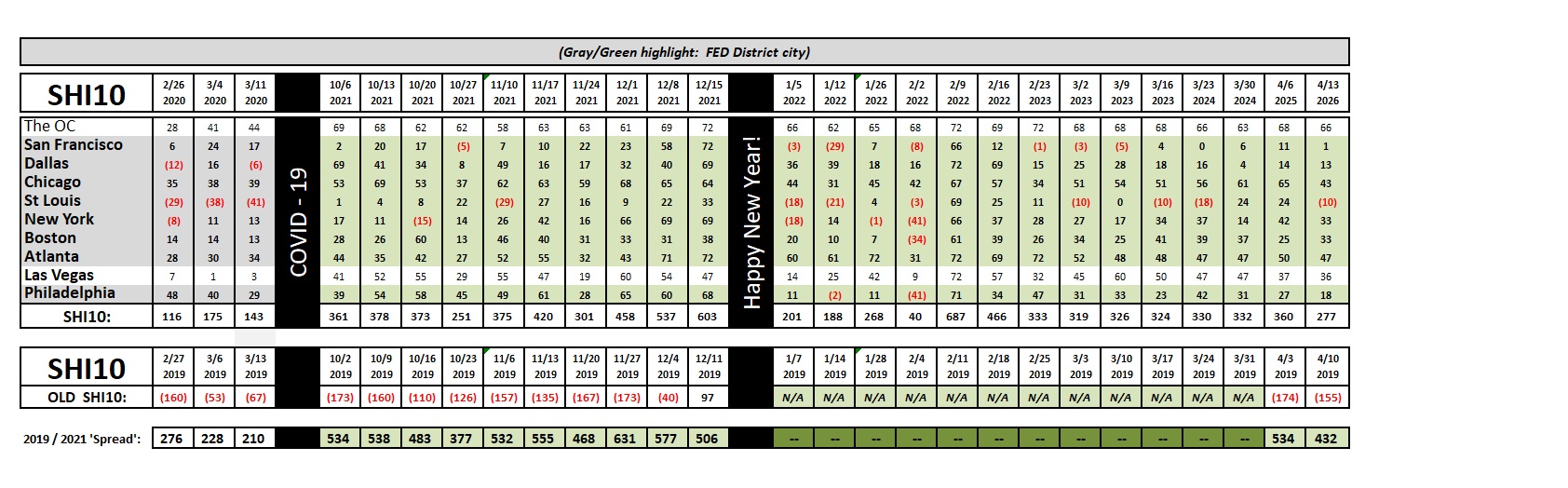

The only market seemingly immune to the swirling changes all around us is here in the OC. Every other ‘opulent eatery’ market seems to be off … anywhere from a little to a lot. Here’s the trend report:

It’s worth noting that the “spread” did not weaken that much … but the SHI10 reading of 277 is meaningfully lower than prior weeks.

Is this an indicative metric? Not yet. For now, it’s only a data point. But we’re seeing plenty of data to suggest our economy is already cooling. Which, of course, is the FEDs current objective. Clearly they believe a 14% nominal GDP growth rate is too frothy. 🙂

And perhaps they’re right. But personally, I remain unconvinced. 2020 and 2021 were aberrational years — in SOOOO many ways. We’re still feeling the repercussions of the “once in a century” and “once in a generation” events in the past 2 years. This will continue for some time. If the FED were to ask me my opinion, I’d suggest that a strong reaction to the wildly fluctuating data is ill advised. These are times to wait and watch … not to make sweeping economic changes. The data is simply too fresh and unreliable. If the FED “overshoots” in response, many will become newly unemployed. Remember: a 1% increase in the unemployment rate means that 1.5 million people just lost their job. Unemployment is at historic lows right now … this is a good thing. So, Chairman Powell, I’d move slowly here. My request to my 6 blog readers: Be sure to mention this to the FED if they ask you what Terry thinks. 🙂

But unlike me, the FED is, unfortunately, at least partially moved by the political winds. And the winds are blowing … because the consumer is unhappy, politicians are unhappy. In the final analysis, the FED may be filled with bankers, but they are not the dispassionate, uncompromising bankers portrayed decades ago in ‘Mary Poppins’. Today, they care. Somewhat. And the fact that the consumer is quite unhappy carries weight. How much? We’ll see …

<:> Terry Liebman