SHI 4.20.22 – Regulation Nation

SHI 4.13.22 – This Just In!

April 13, 2022

SHI 4.27.22 – Bookmark This Site!

April 27, 2022

Is this a good time to buy a house?

Wait … before you answer, let me set the stage with a few thoughts that may help:

NO!

- Are you crazy? Prices have never been higher. This is a bubble, man!

- Fixed mortgage rates are over 5% again! Super high!

- The FED just beginning a rate tightening cycle.

- The odds of a recession have increased

- HOME VALUES WILL SOON DROP LIKE A STONE!

YES!

- There is no time to waste! Demand still exceeds supply by a long shot!

- New home construction remains far under trend. Supply will never catch up!

- US population is going up, UP, UP!

- Government regulation restricts home development, exacerbating the problem.

- During inflationary periods, you must own real estate!

- HOME VALUES WILL CONTINUE THEIR RISE TO THE HEAVENS!

Hmmm …. 🙂

“

So, the question remains: Buy or not?”

“So, the question remains: Buy or not?”

Conventional wisdom suggests this is a horrible time to buy a house. Why you ask?

When the FED enters a tightening cycle — something they have clearly done — interest rates go up. And even more alarming to the housing and mortgage market: The FED plans to simultaneously shrink their balance sheet! This sounds bad! And the financial markets agree. There’s a reason why ‘Rocket Mortgage’ trades today at a P/E of 4X and the home-builder ‘Lennar’ at a P/E of 6X … and that reason is not “because home sales and mortgage demand are hotter than the grills at Mastros!”

No. Quite the opposite. But — people — we don’t subscribe to conventional wisdom! Right? We are the intelligentsia at the Steakhouse Index … we make our own, informed decisions! 🙂

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Significantly. During 2021, nominal growth clocked in at $2.1 trillion. The US annual economic output, in nominal terms, finished 2021 at $24 trillion for the full year. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Pat Bates is my representative in the California Senate. Earlier this month, she office “reached out” to me via email to share some “important updates” from the state and local level. I thought: Cool! Important updates! I should read this email!

Which I did. And saw this:

For the 2022 Legislative Session‚ 2‚020 bills were introduced – 1‚361 in the Assembly and 659 in the Senate. In the Senate‚ each senator is allowed to introduce up to 40 bills per 2-year legislative session; however‚ as you’re well aware‚ not every issue requires a new law.

Wow, I thought. 2,020 new laws were proposed in California in just one year! And this fact got me thinking … I wonder how many were proposed in the last year in the US legislature? Get ready … drum roll please … during the 117th Congress — a 2-year Congress that has yet to finish — the total number of proposed bills and resolutions was ….

13,497

Yep. That’s right. Since 1/1/2021, almost 13,500 new “laws” have been proposed in the US Congress. And, yes, Ms. Bates, I think I agree that “not every issue requires a new law.” But apparently, US Senators — and CA Senators, for that matter, seem to disagree.

Unfortunately, America has become ‘regulation nation.’ With century’s of existing laws already on the books, apparently America still needs more and more every year. In the opinion of our regulators, that is. After all, that’s what we elected them to do, right? Maybe so. And this is a serious issue for all of us … and it has meaningful implications in general economics and, more on point today, to the economics of housing.

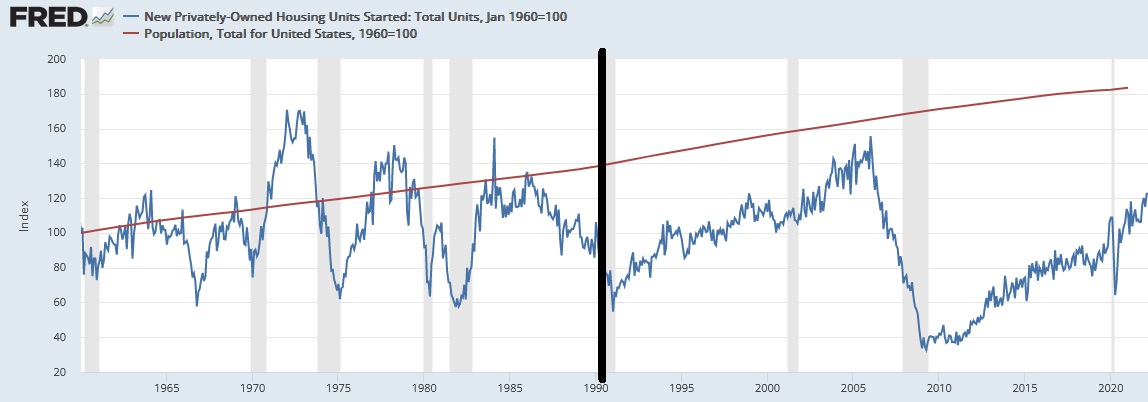

Let’s start here. The chart below has two lines — one red, one blue. Red: US population growth since 1960…with 1960 = 100 on the index. Blue: Newly permitted homes, again since 1960 with a 1960 index value of 100.

Both data points begin with an index value of 100. But while over the 60 years population increased to an index value of over 183, the new home construction index is fairly flat.

I added the vertical black line around the year 1990. I wanted to highlight the two, separate 30-year periods in the chart. In the first period — from 1960 to 1990 — the index value of new home construction exceeded population growth a number of times. In the early 1960s, much of the 1970s, and even a few times during the 1980s. But in the second period — specifically the 30-years between 1990 and 2020 — new home construction has lagged population growth … and since around 2008 by a significant margin. Why?

According to Paul Emrath, a Ph.D in Economics and Housing Policy over at the National Association of Home Builders,

“Rising regulatory costs are a limiting factor on housing supply ….”

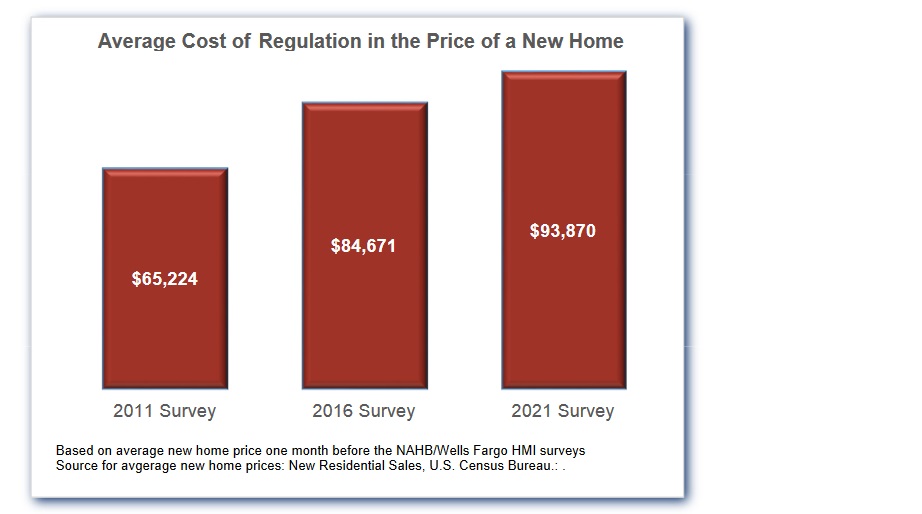

Consider this chart from his most recent study, entitled “Government Regulation in the Price of a New Home: 2021:”

Clearly the $93,870 price tag is exceptionally large. However, when one adds the fact that this is a national average … and for context purposes, it must be assessed against the average home price at the time of the study — $394,300 — then one sees that government regulation is responsible for almost 24% of the total cost of a new home across America. Ouch. Here’s a link to the paper, if you’re interested:

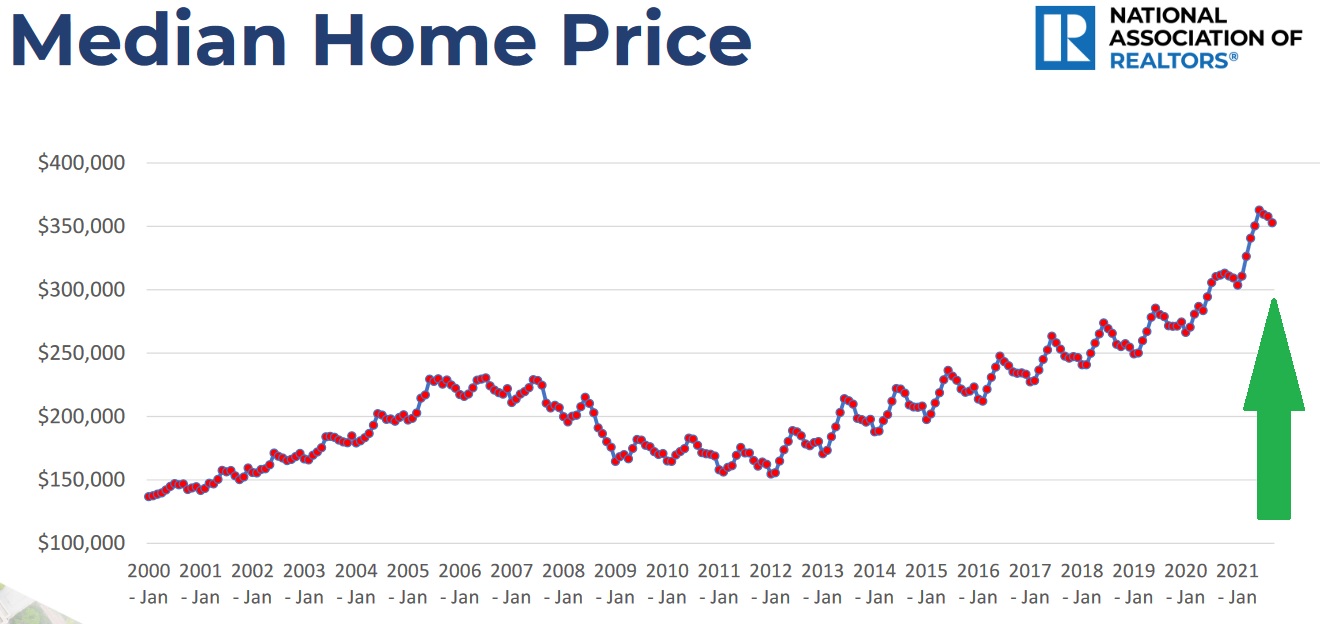

In the image above, you may have noticed the “government regulation” price tag increased from $65,000 to almost $94,000 in the past 10-years. Of course, existing housing values are up far more, of course, as the chart below suggests:

It’s interesting to see the acceleration in home values since 2011 … correlating strongly with the ever-rising “government regulation” cost of a new home. But as my long-time readers know, I am a strong believer that correlation and causation are not always the same thing.

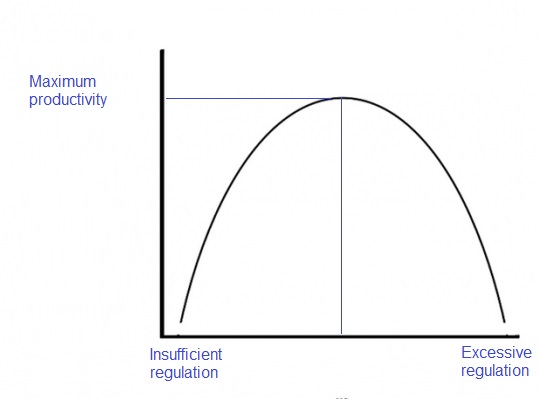

But here they are. Regulations of all types have worked together to both reduce new home supply and increase new home cost — and this relationship is exceptionally dramatic in the past 10 years. Politicians across the country agree that home prices are too high … too affordable … and this is a serious American problem. But I don’t think I’ve heard even one politician place any portion of the blame on themselves. No, I’m not suggesting we should eliminate all regulation and let builders run amuck … that would be equally foolish. Reasonable, pragmatic constraints are needed. But the nature of these constraints should evolve over time as the needs of society evolve. Which brings us to the root of the problem.

I find the best way to visualize issues like this is with an inverted U curve:

Imagine the efficiency of our economy if regulators used this image when considering the OPTIMAL amount of regulation needed at any point in time to maximize productive output? 🙂

New regulations are needed as America evolves. And … at the same time … old, existing regulations should be reviewed for relevance. Every year, regulators should both add new meaningful regulations and remove those they deem no longer necessary. Let me propose this idea, perhaps more as a guideline that a law: No new regulation may be enacted unless one existing regulation is removed. How does this sound? 🙂

As the years, decades, and centuries roll by, these sticky old laws and regulations clump together and create large roadblocks. “Red tape” is the phrase often used in the media and halls of Congress. They often become structural roadblocks that harm commerce and create unnecessary imbalances in supply / demand relationships. Moving from the topic of housing for the moment, consider these “transportation and infrastructure” observations from Michael Cembalest, the Chairman of Market and Investment Strategy at JP Morgan Asset Management on the topic of “structural issues that stand in the way of higher US growth”:

- <> Container ship problems in Los Angeles and Long Beach were exacerbated by local regulations that prevented the stacking of containers more than two at a time, ordinances preventing port owners from paving and consolidating plots they already own to accommodate more storage, and land use regulations that require two to nine years before warehouses can be built on empty land.

- <> No US port ranks in the top 50 globally in terms of cost or efficiency. The Los Angeles port ranks #328 and the Long Beach port comes in at a dismal #333. Existing contracts that prevent port automation, labor costs, limits on operating hours, weekend closures and other factors are partial reasons.

- <> The Jones Act and Foreign Dredging Act raise port handling and dredging costs and put pressure on trucks and rail to transport goods that should be carried by ship instead. Section 301 tariffs of 221% on imported Chinese truck chassis cut trucking capacity and exacerbate supply chain delays.

- <> US rail projects take longer to complete and are more expensive than projects elsewhere. US rail projects with minimal tunneling take six months longer to complete than non-US projects, while underground rail can take 1.5 years longer. Domestic rail projects also cost 50% more on a per-mile basis than in Europe and Canada, and 250% more in New York City. One example: a Metro Line in Toulouse, France was built underground at $176 million per mile while Houston’s Green Line is at-grade and cost $223 million per mile.

- <> Despite a worsening US trucker shortage that has existed for many years, the US effectively bars Mexican trucking companies from operating in the US. The number of American trucks available for inland delivery is reduced since many of them are picking up cargo at the Mexican border.

- <> From 1960 to 1994, the real unit cost of construction materials and construction workers in the US was unchanged yet real interstate highway spending per mile rose by 400%. What changed: the power of local governments and/or citizens groups to delay or block development.

- <> Environmental Impact Reports used to be 10 pages. Due to litigation, the current EIR is more than 600 pages plus appendices that can exceed 1,000 pages, and can take 4.5 years to complete. No ground can be broken on federal or private projects until an EIR makes it through the legal gauntlet.

The list goes on and on …but I think you get the idea.

I hate highlighting a problem without suggesting a solution, so here goes: I think my “one-for-one” idea is a winner: By decree, no new regulation may be enacted without the elimination of an existing (related?) regulation.

Let’s see what expensive steak house reservations tell us this week about the US economy. Here’s the SHI trend chart:

Reservation demand is definitely softening in about half the SHI markets. At least when compared to a month or two ago. Reductions are clear in the east, specifically in NYC and Boston. On the other hand, reservation demand in California is fairly consistent. It’s too early to derive any meaningful conclusion here … and when we compare this weeks reading to the SHI10 from the same week in 2019, the ‘spread’ has actually improved.

The FED released their Beige Book earlier today. Here are a few highlights thru their lens:

Overall Economic Activity: Economic activity expanded at a moderate pace since mid-February. Several Districts reported:

- <> Moderate employment gains;

- <> Consumer spending accelerate;

- <> Manufacturing activity was solid;

- <> Commercial real estate activity accelerated modestly;

- <> Office occupancy and retail activity increased;

- <> Strong demand for residential real estate, but limited supply; and,

- <> Outlooks for future growth were clouded by the uncertainty created by recent geopolitical developments and rising prices.

Let’s go full circle back to the original question: Is now a good time to buy a house?

Yes. I believe it is. Supply constraints are unlikely to be “fixed” any time soon. Sure, the exceptional movement in the 30-year fixed rate is troubling, but balance this move against the FEDs strong desire to avoid pushing the country into a recession and rising unemployment. It is very likely home value increases will moderate in the next year or two — which is probably a good thing. But I believe home values will continue to rise unabated.

So, yes, this is a good time to buy a house.

Oh, my attorneys have asked me to add this disclaimer: “This is the personal opinion of Terry Liebman and as such is not, and should not be construed by the reader as, financial or other advice. Buy a house at your own risk.”

Those attorneys. You gotta love ’em!

<:> Terry Liebman