SHI 4.27.22 – Bookmark This Site!

SHI 4.20.22 – Regulation Nation

April 20, 2022

SHI 5.4.22 – Over 2 Decades in the Making

May 4, 2022

There is no shortages of gossip and opinions on the web. But reliable data is harder to find.

Until now, that is! I have a great website for you … courtesy of the US Census Bureau, that offers us insight into 18 important data-points. Additionally, by selecting the “I Want To … “ button, you can download current press releases and excel data AND you can even access trend charts! I know, right? Fun! 🙂

“

Opinions matter but data is critical.”

“Opinions matter but data is critical.”

OK, maybe I’m overstating the entertainment value of this website just a tad. You may prefer a good movie over a good data-feed. No worries. Me? I like both … but today we’re talking about data. Because accurate data matters to all of us. And I’ll probably throw in an opinion or two. 🙂

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Significantly. During 2021, nominal growth clocked in at $2.1 trillion. The US annual economic output, in nominal terms, finished 2021 at $24 trillion for the full year. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

OK, now that you’re salivating for that website, here’s the link. Again, ‘right click’ and ‘open in a new tab.’

Impressive, right? Not only is the data set quite comprehensive, but the format is easy to understand and follow. For example: Did you know that almost 2 out of every 3 American households owns their own home? We can debate the level of wealth and income inequity in the United States, but the “homeownership rate” of 65.5% is a fact. And, once again, we can debate the importance of home equity in personal wealth, but it is an indisputable fact that during Q4 of 2021, the value of home equity increased by almost as much as the value increase in corporate equities. And that value increase benefited over 65% of American households. (See page 138 of the most recent FED z.1 report https://www.federalreserve.gov/releases/z1/20220310/z1.pdf)

Data is critically important.

With only a quick glance, we see that quarterly profits for both retailers and manufacturers were up double-digits Q4. Month-over-month ‘construction spending,’ however, is slowing. Significantly. And while US exports are still increasing as of January of 2022, the rate of increase is slowing. Dig into the data. Read a few press releases. I think you’ll find it fascinating. I certainly did.

My point: In the aggregate, data tells a story. I try to interpret it … which is where the facts end and my opinions begin.

The US economy is slowing.

Hold on. I didn’t mention the “R” word. No, a recession is not imminent. Nor, at this moment, do I believe the US will have one in the near future. However, the FED is working awfully hard to change my mind. It wasn’t more than 9 months ago when the FED assured all investors that they would not raise interest rates until some time in 2023. Well, that changed in a hurry. We’re not even half-way thru 2022 and FED rate-hike worries are ubiquitous. Will they raise 50 basis points … again, and again, and again? Maybe. I don’t think so, but maybe. But what is far more clear is (1) the magnitude of the FED pivot and (2) the speed of the market response.

Sure, sure, we all know why. The “I” word. The FED had to respond or risk losing credibility. And the financial markets responded too: Long term interest rates immediately increased significantly. And, as they typically do, the equity markets immediately fell. Remember: Interest rates are a foundational pricing mechanism for equities — the relationship is inverse, of course. P/E ratios have always been impacted by interest rates beyond simple recession fears. Generally, the higher the FED funds and Treasury rates, the lower the P/E ratio. For example, back in 1980 when interest rates were rising to the moon, average forward S&P500 P/E ratio was about 7X earnings. Compare that to over 20X in the past year or so. It makes sense: If an investor can get a long-term 10% return on a Treasury bond with no principal risk, why invest in equities?

And so fears of FED rate hikes, and the almost inevitable recession to follow, have done a number on investor expectations. Will the extremely rapid home-loan rate increases do the same thing in the housing markets? Sure … somewhat. History suggests that outcome is inevitable. Home loan rates are up more than 2% in just a couple of months. That increase will take a large bit out of US home affordability. “For sale” inventories are sure to rise…which is good news for you house-hunters. And home value increases are likely to slow.

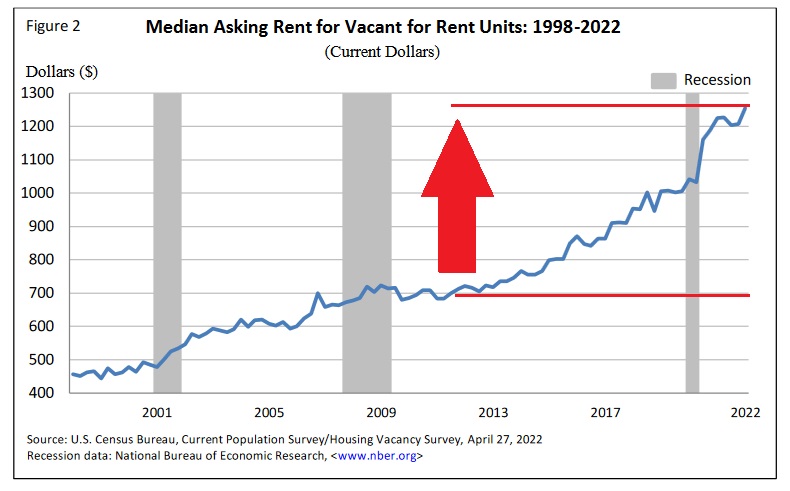

But, is renting a viable alternative? Is renting a better choice?

Nope. In the past 10 or so years, rents have almost doubled. This is a fact … and this increase has lifted the CPI quite a bit. So what should you do? Bite the bullet and buy that house … even though rates are way up? Or sign a 1-year lease, knowing that in 13 months, your rent will probably jump about 10%? My suggestion: Ask your boss for a raise. 🙂

Which brings us full circle back to the FED. They are in a difficult spot. They must slow the economy and attempt to find a sustainable level of economic growth and employment. Can they do it without pushing us into a recession? The jury is out. We’ll have to see. A recession is not inevitable … as the FED is sure to remain “data dependent” when making decisions. They track and analyze data in far more depth and quantity than we possibly could. So the hand-wringing over “will the FED raise 50-basis points 4 times!” or once, or twice, or will they throw in a 75 basis point increase, etc, is just that: Hand-wringing. No one knows. Not even the FED knows at this moment. They will take it as it comes and adjust accordingly. And they will make decisions based on data. Will they make the “right” decisions? Again, time will tell.

Recall that US GDP is determined by measuring growth in four (4) economic components: Investment spending (like plants and equipment), net exports (exports minus imports), government spending and consumer consumption. I am convinced rate of investment spending will slow in the coming year, and the rising value of the US dollar against other currencies is almost a guarantee that exports will slow and imports will increase. Government spending is likely to remain fairly consistent. So what about consumer spending?

Consumers are spending. Per the BEA, ‘personal consumption expenditures‘ increased by .2% in February, following an exceptionally strong reading of 2.7% in January. And for now, I believe they will continue to spend … thereby firmly underpinning the US economy. Savings levels remain high and revolving credit balances remain low. Both will act as a tailwind for consumer spending. For now. We’ll have to watch the data to see how FED and market actions impact consumer behavior and consumer confidence. It’s an every-changing landscape, folks.

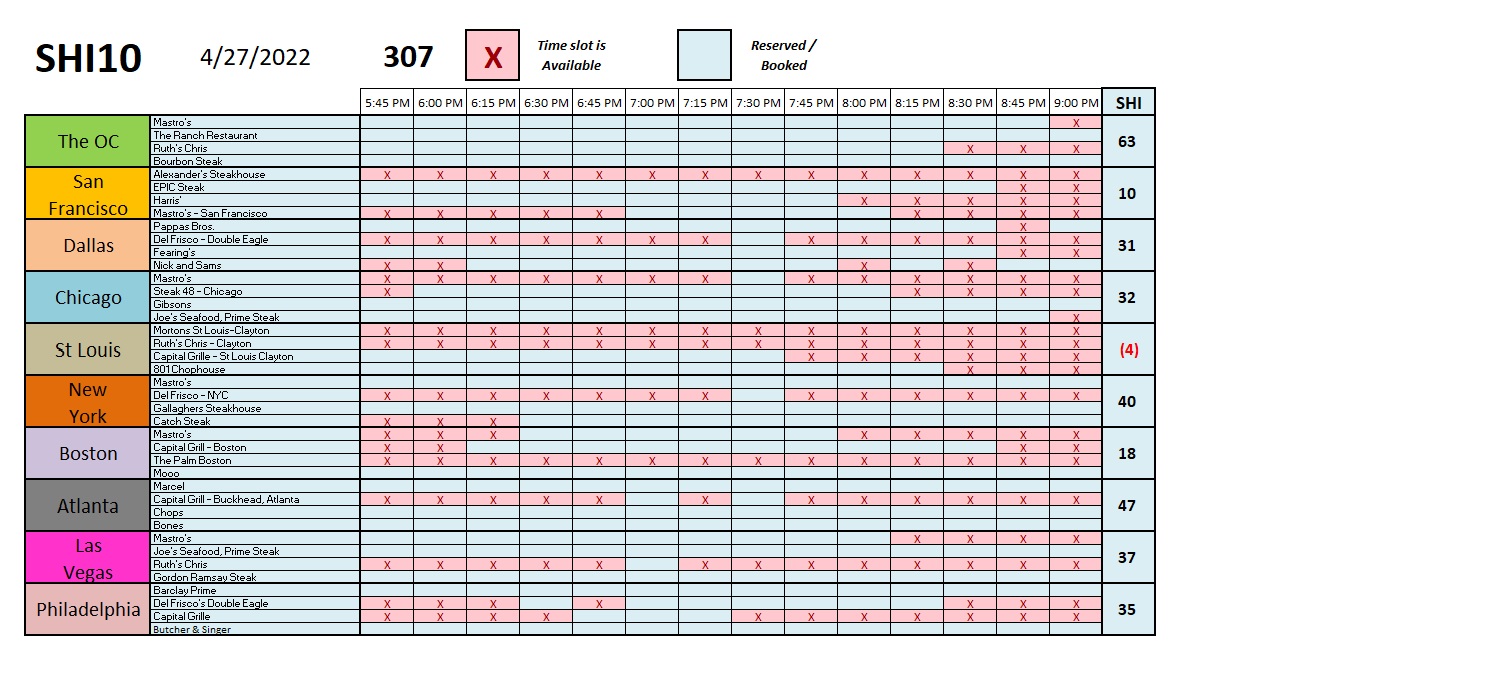

What are the steak houses saying this week? Let’s take a peek:

Not bad. The SHI10 is up from last week … a little. Stronger SHI markets remained consistently strong … and even the perennially weak San Francisco market is showing signs of life. The carnivores have returned! 🙂

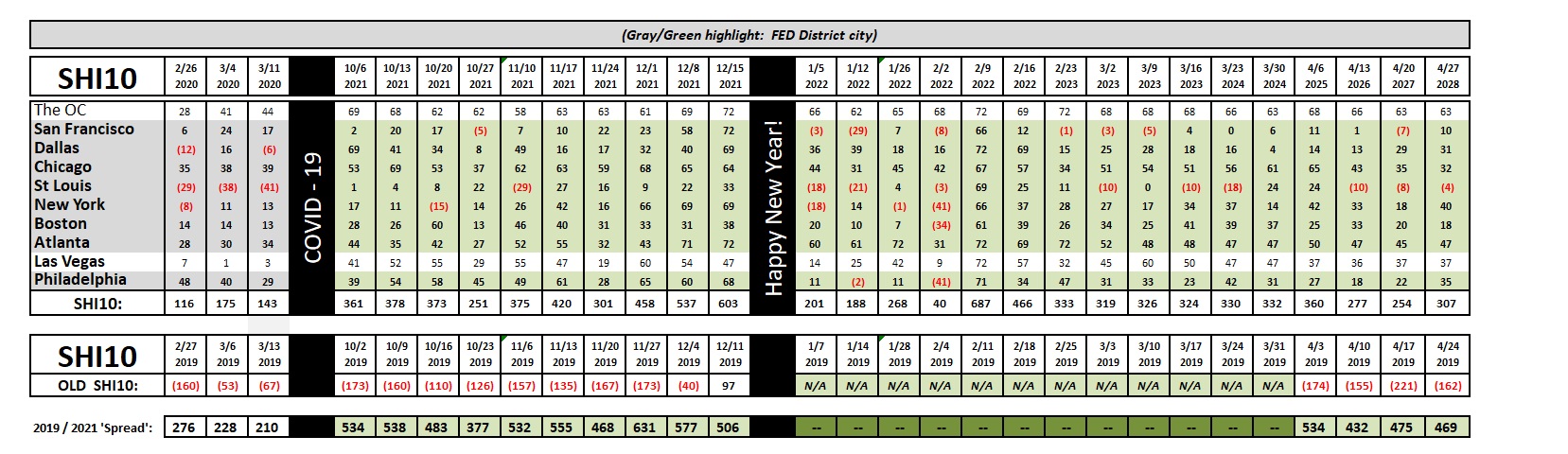

Here’s the longer term trend report:

In my opinion, there is no doubt the US economy is slowing. But there is simply no possible way 2022 GDP growth could replicate the sizzling 14% ‘nominal’ growth rate we had in Q4. Even without the FEDs help GDP growth would have moderated. But now they’re stomping the brakes pretty hard. But will they push us into a recession? In my opinion, no. That said, the “R” word and the “I” word are both realities. And both are extremely data-dependent. So, unfortunately, we’ll have to wait and see. But I remain quite bullish on the US economy. Thanks in large part to the consumer.

As the FED interprets and digests incoming data, expect their words and actions to evolve and moderate. But our economy remains strong — far stronger, in fact, than in those in Europe and China. Hang in there. We’re actually doing fine. That’s what the data tells me.

<:> Terry Liebman