SHI 5.4.22 – Over 2 Decades in the Making

SHI 4.27.22 – Bookmark This Site!

April 27, 2022

SHI 5.11.22 – Cult Members Needed

May 11, 2022

The last half-point rate hike was in 2000. Just as the 20th century ended, about 22 years ago, was the last time the FED felt the need to make a 50 basis point rate increase.

Until today. Today, the FED did what we expected and lifted the FED funds rate up to a whopping 0.75%. But that’s not news … everyone expected that. Let’s talk about something far more important.

“

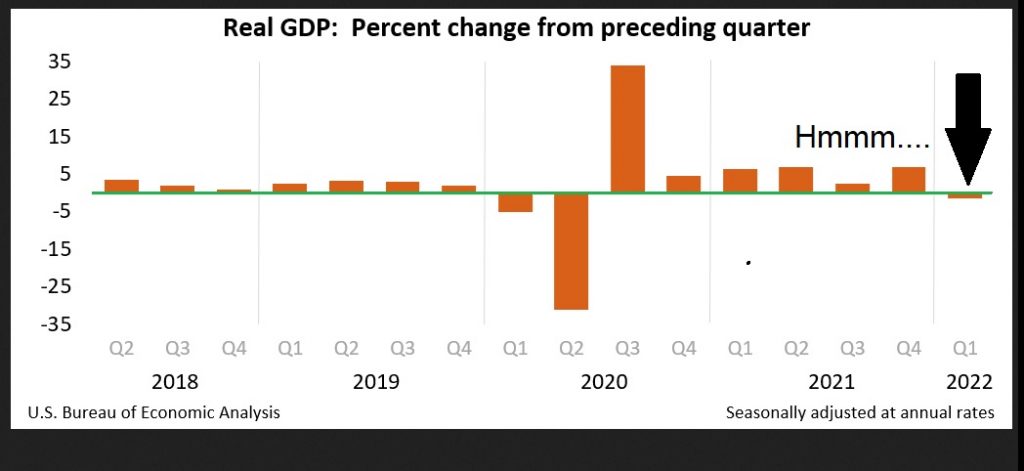

The US GDP shrunk last quarter.”

“The US GDP shrunk last quarter.”

What!?!

Yep. Last Thursday, the day after I posted my blog, according to the Bureau of Economic Analysis (BEA), America’s economic output actually actually shrunk in the first quarter of 2022. Wow. That was unexpected — by me, anyway. Sure, I was confident our economy was slowing … and opined on that in my blog. But I did NOT expect our GDP would shrink during the first quarter. And yet, according to the BEA, it did. GDP decreased at an annual rate of 1.4% in Q1. Wow … so our economy is shrinking … OR IS IT? Could the BEA be wrong?

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Significantly. By the end of Q1, 2022, in ‘current-dollar’ terms US annual economic output clocked in at $24.38 trillion. Yes, during Q1, the current-dollar GDP increased at the annualized rate of 6.5%. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Let me repeat the question: Could the BEA be wrong?

No. They are not wrong. However, once again, the proverbial ‘devil is in the details.’ And here are the details:

In Q1 of this year, in ‘current-dollars,’ US annual economic output increased at the annualized rate of 6.5%.

That’s right. In the first quarter, US GDP grew by 6.5%. But that growth rate is before the BEA completes the process and “deflates” the nominal growth rate by the “price index for gross domestic purchases” which, for Q1, ran at the exceptionally high rate of 7.8%. From there, the math is easy: 6.5% minus 7.8% equals a loss of 1.4% for the quarter. Thus the “real” GDP growth rate, in Q1, was a decline of 1.4%

During the first quarter, US economic output increased by $379.9 billion! It did not shrink. However, again, this is a current-dollar number and not a “real” number. Real numbers are post-inflation adjustment. And inflation, right now, is running hot.

Did you hear even one economic reporter comment on the impressive, pre-inflation 6.5% growth rate? I did not. Not one. Until today, folks! You heard it here! 🙂

In many respects, it was an excellent quarter. ‘Personal consumption expenditures‘ — that’s our stalwart consumer — increased at the annual rate of 1.83%. Investment and government spending pretty much cancelled each other out. And the biggest bite out of the the first quarter GDP reading was ‘net exports‘ which declined at the annualized rate of 3.2%! Ouch. That hurts. But, once again, it’s not a huge surprise, inasmuch as the value of the US dollar has been soaring against the currencies of our global trading partners:

In the past year, the USD is up 12.2% against the euro, up 10.1% against the pound sterling, and the USD is at a 20-year high against the Japanese Yen. Why you ask? Well, it’s complicated … but the up-move is most likely related to market-driven increases in the 10-year US Treasury … at a time when Europe’s rates are about half that amount, and the Japan 10-year rate remains close to only 25 basis points.

More importantly for the purposes of this blog, the up-move has adverse effects on US GDP. The up-move makes US exports more expensive and imports from other countries much cheaper. Think of it this way: If buying a US product now costs about 15% more than it cost last year, simply due to currency changes, why buy it? Why not buy something similar and cheaper from a different country? And many consumers in other countries have done … they “substitute” away from the more expensive US product. But here in the US, on the “flip side of the coin” so to speak, imports are 15% cheaper! WooHoo! So we buy more imports. And thus, in the final analysis, a “strong dollar” is bad for US exports … and it has the effect of dragging down GDP growth.

Let me summarize with this comment: Yes, by the official metrics, GDP did shrink last quarter. Because official metrics shrink the ‘current-dollar’ number by an inflation factor, the ‘price index for gross domestic purchases,’ which is running super-hot right now at 7.8%. However, consider this: Exactly one year ago, the price index was 3.9%. And the prior quarter, the price index was only 1.7%. If today’s reading was similar, GDP growth would have been positive in the first quarter — by a very large margin. Keep this in mind for contextual purposes. Our economy remains quite strong, in spite of the negative “real” GDP report from the BEA.

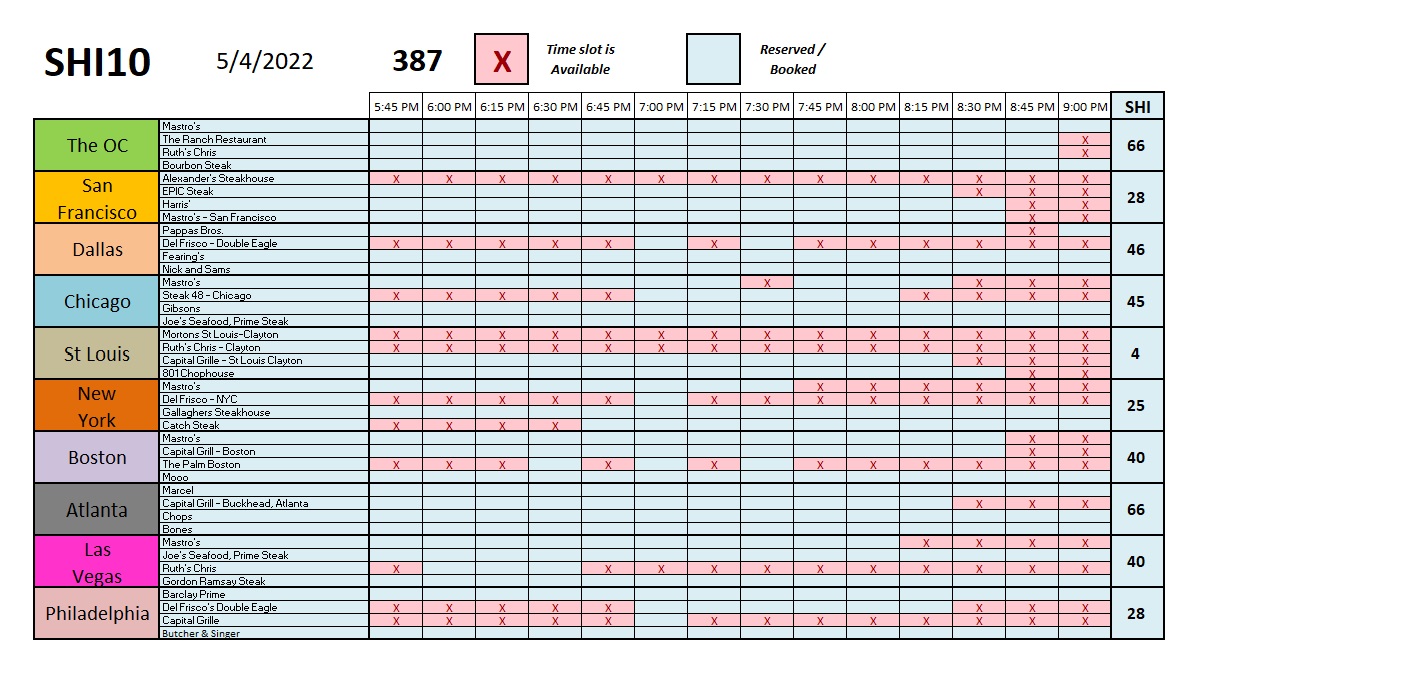

Let’s head to the steak houses!

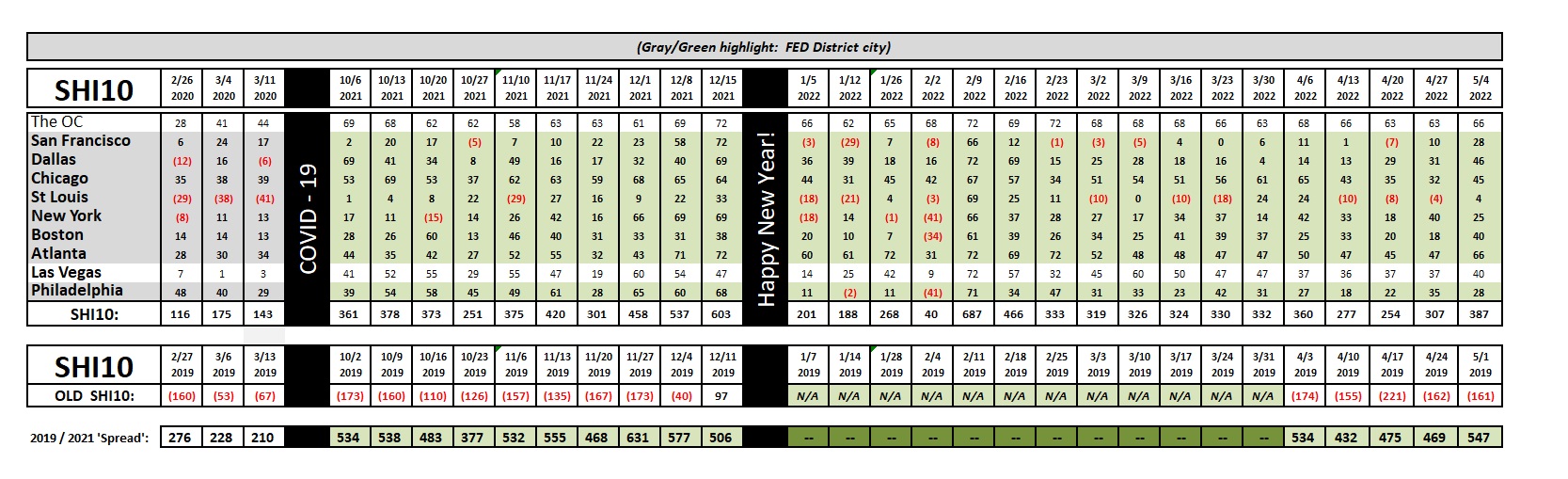

Reservation demand is fairly robust this weekend. But we have to remember that Sunday is ‘Mother’s Day’ and this has historically increased expensive eatery demand. Here’s the longer-term trend report:

The SHI40 is telling us the economy is strong. In fact, at Powell’s press conference following the FOMC meeting and statement, he said exactly that: “The economy is strong.”

We have to travel back to May of 2000 to find the last 1/2 point FED rate increase. There’s a reason for that. It’s a BIG move … one that sends a BIG message to the consumer and the financial markets. Interestingly, I’ve heard a few comments from economic experts like, “Why don’t they just increase the FED funds rate to 3.5% in one move and be done with it?” The answer is easy. Actually there are two reasons. The first, because such a move is dumb. Totally dumb. Because of the second reason: There is no play book here, folks. As I’ve said many times before, the FED must retain the ability to moderate their actions based on the continuous data stream flowing thru their hallways each and every day. Remember, while the FED funds rate is now around 0.75%, the 10-year Treasury has already moved up to around 3.00%. The FED has already “talked up” longer-term rates by discussing short-term rate increases and balance sheet shrinkage. And they’ve already “talked down” the stock and bond markets which, on the back of the war in Ukraine, have already shed trillions of dollars in value, thereby somewhat moderating the “demand” side of the economy.

At the press conference, Powell verbalized that the FED works hard to avoid adding uncertainty into our lives that large, rapid moves might cause. Remember: Ultimately increasing interest rates will adversely impact all American homeowners and they will eventually increase the unemployment rate, thereby injecting hardship into the lives of many folks living on the margins. These outcomes are inevitable; however, the ultimate extent of this pain will be highly correlated with both the size and duration of the FEDs tightening cycle.

“It will be a judgement call” he commented, at each future meetings, based on the most recent data. Good. Makes perfect sense.

<:> Terry Liebman