GDP “Now-casting” Report Update May 27, 2016

Steak House Index Update 05/25/16

May 25, 2016Could a FED Rate Increase Actually Reduce Long Term Rates?

May 28, 2016This is an update of my Nowcasting blog from last week. If you missed that one, I suggest you read it before continuing:

https://www.newyorkfed.org/research/policy/nowcast

Why you should care: The NY FED Nowcast is a “sneak preview” into a highly probably future. In fact, earlier today, the BEA released its ‘second’ estimate of the 2016: Q1 GDP at 0.8%. (Note, this GDP reading is delivered to us 58 days after the quarter ended.) Today’s Nowcasting Report states their 4/28 reading for Q1 was 0.7% – extremely close.

Clearly, the Nowcast offers us a likely view of the future – before the future is here! And I have no doubt the FED is watching.

Taking action: As I’m certain the FED uses the Nowcast in their analysis, we must watch it carefully. Use it to make business and investment decisions ahead of GDP releases. Stay up with it each week or two – and you’ll be far more educated than your competition!

THE BLOG: This weeks update suggests 2016: Q2 GDP growth is picking up steam. Today’s Nowcast is 2.2%. Here’s the graphic (Click to enlarge):

The trend is clearly positive. From a reading only 4 weeks ago below 1%, today’s Nowcast is very upbeat. If this trend continues, the FED can easily argue GDP growth is recovering.

However, remember, one calendar quarter’s reading is simply that. 2016: Q1 was weak at 0.8%. For the first 1/2 of the year to show even a 2.0% GDP growth rate, Q2 would have to come in at over 3.2%. I believe this is very unlikely.

So, perhaps one of the 3 data metrics the FED needs to line up before they seriously consider raising rates is doing just that. We’ll watch each week and make sure.

How about employment? We’ll get an employment update a week from today, on Friday, June 3rd. I’ll report on that metric on the 3rd.

And then we have inflation. Will we see movement toward the 2.0% FED goal?

For insight here, let’s go to the Dallas FED and their report on the “Trimmed Mean PCE Inflation Rate”:

http://www.dallasfed.org/research/pce/

And what is a “Trimmed Mean PCE Inflation Rate”? Great question. Here’s the Dallas FED explanation:

“In spite of the arcane-sounding name, the concept of a trimmed mean is a simple one. In fact, trimmed means should be familiar to any follower of international figure skating. In the wake of the controversies surrounding the judging at the 2002 Winter Olympics, the International Skating Union adopted a scoring system in which a skater’s highest and lowest marks are discarded before the skater’s average score is calculated. Trimmed mean inflation rates are derived by a similar procedure.

In any given month, the rate of inflation in a price index like the Consumer Price Index or Personal Consumption Expenditures (PCE) can be thought of as a weighted average, or mean, of the rates of change in the prices of all the goods and services that make up the index. Calculating the trimmed mean PCE inflation rate for a given month involves looking at the price changes for each of the individual components of personal consumption expenditures. The individual price changes are sorted in ascending order from “fell the most” to “rose the most,” and a certain fraction of the most extreme observations at both ends of the spectrum are—like a skater’s best and worst marks—thrown out, or “trimmed.” The inflation rate is then calculated as a weighted average of the remaining components.

For the series presented here, 24 percent of the weight from the lower tail and 31 percent of the weight in the upper tail are trimmed. Those proportions have been chosen, based on historical data, to give the best fit between the trimmed mean inflation rate and proxies for the true core PCE inflation rate. The resulting inflation measure has been shown to outperform the more conventional “excluding food and energy” measure as a gauge of core inflation.”

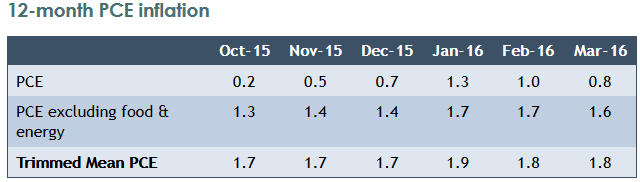

We see here a clearly defined, consistent methodology that tends to outperform traditional measures which exclude food and energy. Good. Let’s follow this too. At the same time, the raw PCE data remains important. Here are all readings thru March:

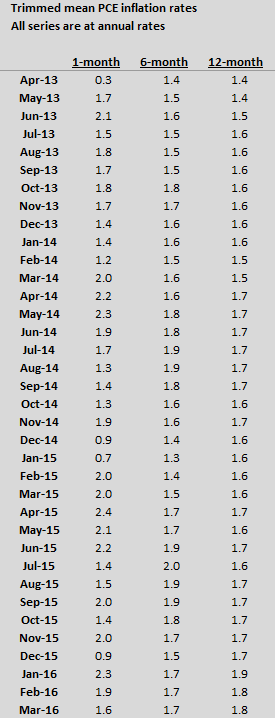

I don’t see any acceleration in inflation rate here. How about over the longer term, say 3 years? Here’s the raw data:

Again, I see no meaningful acceleration in inflation. Remember: Raising the interest rate will have an inverse effect on inflation and GDP. Both will tend to move lower.

Is that a risk the FED is willing to take in June? Absent a meaningful change here, I doubt it. Stay tuned!

- Terry Liebman