SHI 09.12.18 Ratatouille

SHI 09.05.18 Investors Agree with Trump

September 5, 2018

SHI 09.19.18 One Thing is Certain …

September 19, 2018

“The US stock market is enjoying the longest “bull market” in history.”

At the same time, risks to the bull market and the US economic expansion continue to rear their ugly heads. Much like mushrooms on a perfectly manicured lawn. Bull … mushrooms … ratatouille … this must be the SHI!

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will continue to be true for years to come.

Is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $80 trillion today. US ‘current dollar’ GDP now exceeds $20.4 trillion. In Q2 of 2018, We remain about 25% of global GDP. Other than China — a distant second at around $11 trillion — the GDP of no other country is close.

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

We’ll get to our mouth-watering pricey eateries in a moment, but before you rush out this Saturday and spend $600 for that perfectly grilled NY strip at Ruths Chris, consider this:

- We’re already seeing casualties of the “trade war.” According to the FED ‘Beige Book’ released just moments ago, 3 of the FED’s 12 districts — St. Louis, Philadelphia and Kansas City— reported weaker growth in August. While the overall U.S. economy expanded at a “moderate pace,” trade concerns and a lack of workers were delaying projects. There were also “some signs of a deceleration” in prices of final goods and services. Could this be a sign?

- Rising short-term interest rates in the US have simultaneously buoyed the US dollar and weakened emerging market country currencies around the globe. Argentina, Turkey, Indonesia, and many others are struggling as a direct result. The fear? Contagion. Could this be a sign?

- The Down Jones Commodity Index has fallen about 9% since May 23rd. Could this be a sign?

- Finally, comments by FED governor Lael Brainard suggest that the FED won’t stop raising rates because they fear the effects an inverted yield curve. If economic strength warrants rate increases, she fully expects the FED to continue tightening. Could this be a sign?

Our economic state reminds me of a large plate of ratatouille: Across the landscape, we see a myriad of economic conditions, many very positive and many negative. Is the end near?

Naaa….go buy that steak. Enjoy. Sure, there’s plenty to worry about. But here are my thoughts:

- The trade war will cause supply chain problems. There will be casualties. But I think this will not be a catalyst for a general economic slow down. At least, not yet.

- Emerging markets will not impact US economic performance.

- Commodities are a proxy for manufacturing input prices. The 9% drop belies the full scale of the decline, as oil is up quite a bit, but the move isn’t enough to cause me to worry. Again, at least not yet.

- Lael’s comments aside, the FED will pay attention to yield curve inversion.

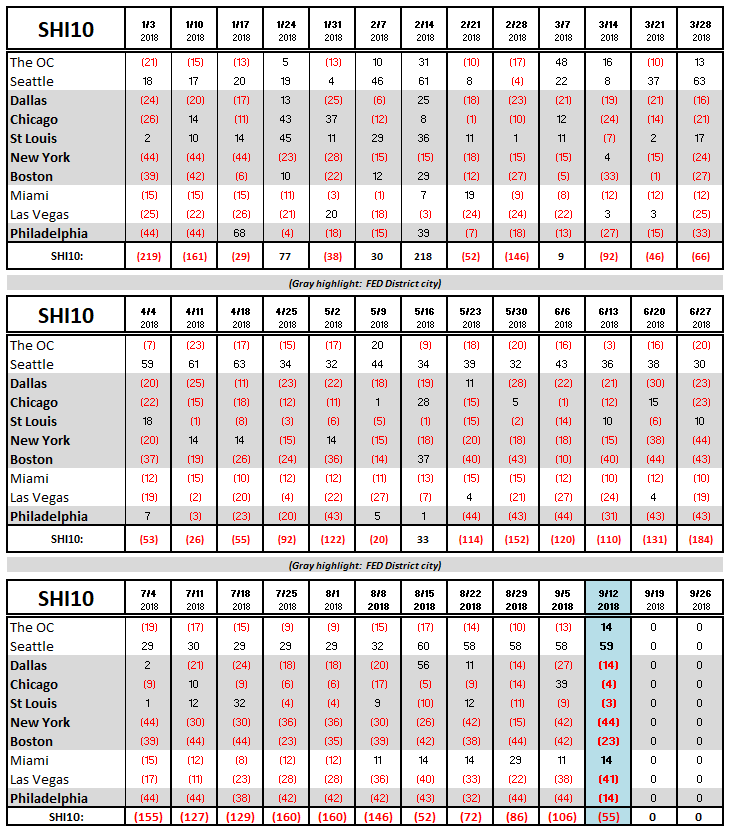

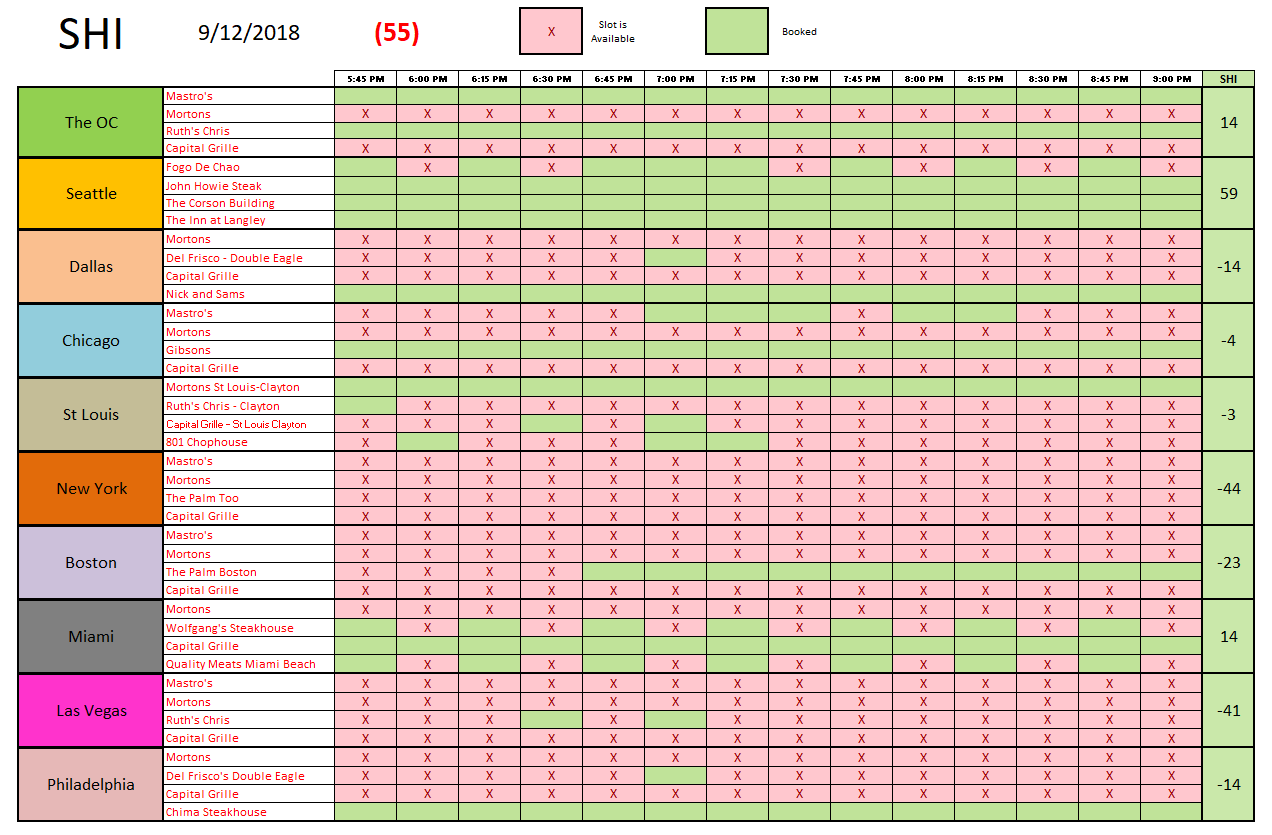

OK…time for that steak! Apparently, lots of folks agree with me: This weeks SHI10 has improved significantly:

While a reading of negative 55 isn’t a barn-burner, it’s pretty good. Reservation demand in Seattle is near all-time highs, the OC SHI has turned positive, and even Philly has a ‘sold-out’ restaurant! Take a look:

Once again, the SHI10 is predicting continued strength in consumer spending and a solid GDP reading. Thanks for tuning in. See you next week.

- Terry Liebman

{kind=link}