SHI 2.10.21 – Inflation Hide and Seek

SHI 2.3.21: The Irony is Thick

February 3, 2021

SHI 2.17.21: Baskets Full of Data

February 17, 2021

Where is inflation?

Clearly, it’s not in the CPI. Earlier today, the BLS released their latest report: “Consumer Price Index – January 2021:”

“The CPI index for all items – less food and energy – was unchanged in January. The indexes for apparel, medical care, shelter, and motor vehicle insurance all increased over the month. The indexes for recreation, used cars and trucks, airline fares, and new vehicles all declined in January.”

Nope. No inflation here. Thus, for now … and the foreseeable future … I believe …

“

Inflation is well anchored at current levels.“

“Inflation is well anchored at current levels.“

During the 12-months, the CPI rose 1.4% — well below the FEDs inflation target of 2%. If we can’t find inflation in the CPI … where can we find it?

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Before COVID-19, the world’s annual GDP was collectively about $85 trillion. Then it shrank … then bounced back! We can thank global fiscal and monetary policy for the bounce. According the the Q3, 2020 ‘preliminary’ numbers, annual US GDP is back UP to about $21.1 trillion. And still, together, the U.S., the EU and China continue to generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Used car and truck prices were up 10% in the past year. Apparently, when air traffic falls 90%, people buy cars and hit the road. Increasing both demand and prices for autos and gasoline. But price increases in most other CPI items were muted.

Our search for inflation considers two paths: Actual inflation and inflation expectations. First, inflation expectations.

Expectations remain well anchored. Per the FED ‘Survey of Consumer Expectation’ in January, consumers expect inflation to run about 3% during the next year. This is up from one year ago — when the reading was 2.54% — but is identical to January of 2019. The University of Michigan also takes a monthly survey of consumer expectations. Respondents are asked these questions:

- <> Do you think prices in general may rise, fall or remain unchanged in the next 12 months?

- <> What percentage of growth/fall do you expect in the next 12 months?

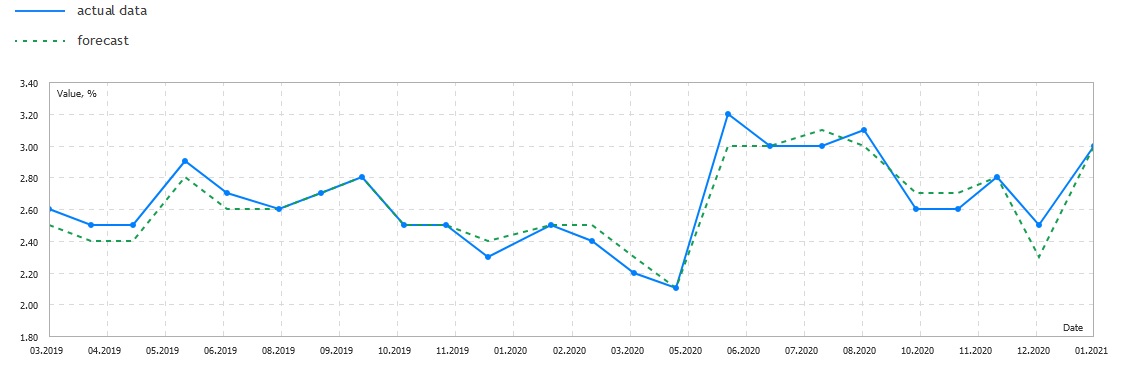

This chart reflects their beliefs:

Why are inflation expectations so important to the question? Because over the decades, the public inflation expectation tends to be a very accurate predictor of the actual level of inflation. Notice the blue line above — actual inflation data — and how highly correlated expectations are to actual results.

So … does the actual result create an expectation … or is the opposite true? Which comes first? A great question… a la the proverbial ‘chicken and egg’ question. Answer that one — which came first? — and then I’ll gladly answer the question I posed. 🙂

On the chart above, inflation expectations may be lower now than the middle of last year, but they are trending upward. Slightly.

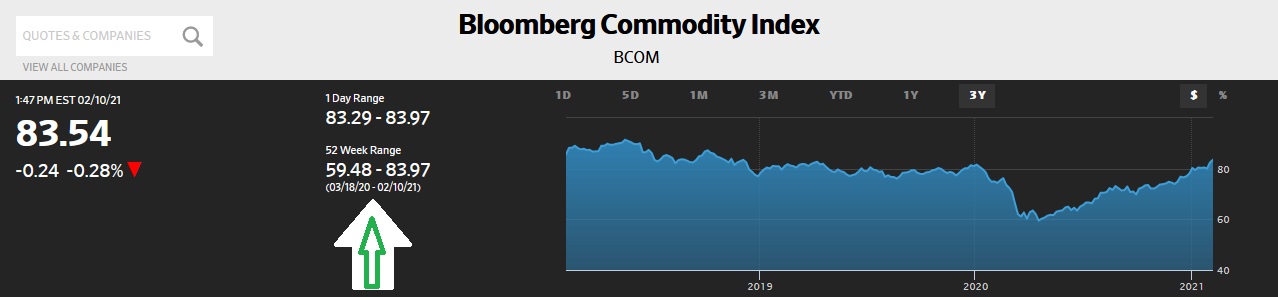

Probably because we’re seeing the green chutes of inflation popping up in a number of places. Consider commodity prices. Here’s the ‘Bloomberg Commodity Index‘:

See the arrow? The current index reading is 83.97 — the 52-week high-point. This index reading is very close to the index in January of 2020 — and is definitely below the readings from prior years — but after collapsing in the early days of the pandemic, the index is clearly up significantly.

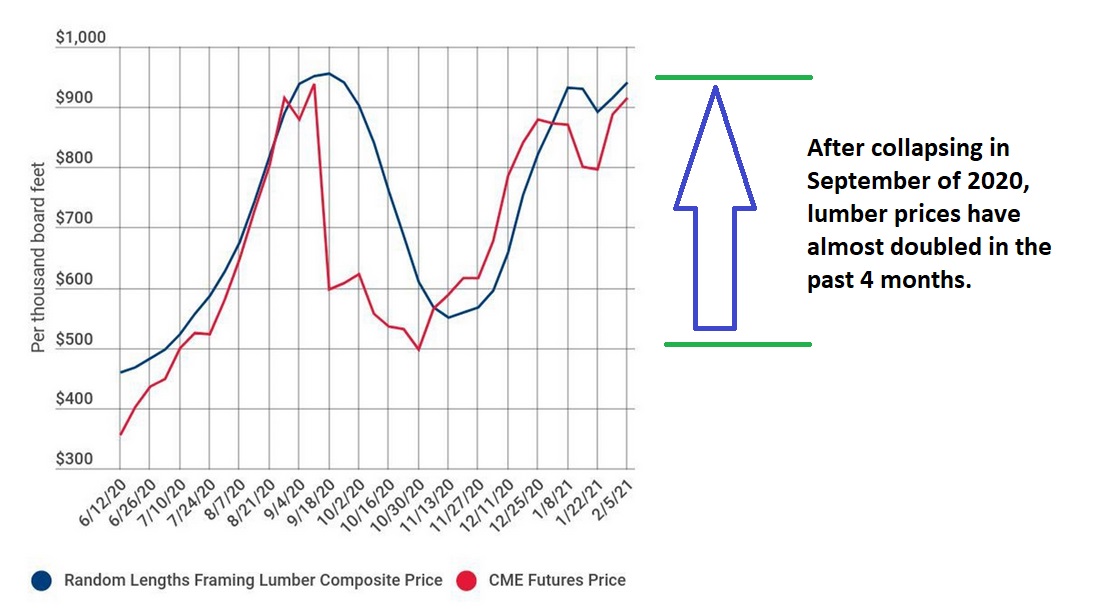

Which means commodity prices are up significantly in the past 6 months or so. Corn prices are at their highest levels since 2013. And if you plan to build a house, you’d better plan to spend a lot more for lumber:

Per the NAHB, ‘framing lumber’ represents about 15% of new home cost. Rising commodity prices further increase costs.

Throw in massive federal fiscal stimulus, significant increases in money supply, and we can certainly understand where inflation concerns begin to form. Copious data sources support a concern that we may see rising inflation in the months and years to come.

But In the final analysis, I believe history suggests that actual inflation is the the result of permanent increases in consumer inflation expectations which subsequently triggers a rising wage expectation and demand. However, history also suggests this cycle requires many years to come to fruition and is usually the result of persistent actual consumer price inflation. Which we’re not yet experiencing.

So, for now, we wait. Inflation remains hidden. But like the FED, we’ll continue playing the ‘Hide and Seek’ game, waiting to see what develops.

For now, I continue to believe we can all relax. No inflation. Yet.

- Terry Liebman