SHI 2.21.24 – Landmine Explosions

SHI 2.14.24 – Riding The Rocket

February 15, 2024

SHI 2.28.24 – Money, Money, Money

February 29, 2024

Hot air balloons and economies can both deflate.

And in both cases, while a small “loss of air” is no big deal, a large deflation event can be very dangerous. In both cases, people can get hurt. This reality is beginning to firmly take root in China.

“

China is deflating.“

“China is deflating.“

Mainland China housing prices continue to plummet, crushing confidence and consumer spending. Once considered the safest bet in China, home values have fallen and losses are accelerating. Even Hong Kong, long one of the globe’s most expensive luxury home markets, is feeling the pinch. Across the island, Hong Kong mansion prices are down an average of 25% since 2002 — and many are trading at 50 cents on the dollar. If Hong Kong was on your list for second home locations, today is a good time to start looking. 🙂

Meanwhile, back on mainland China, consumer prices are also falling at the fastest rate in more than a decade. What’s worse, as we cannot trust any “official” economic data out of China, we really have no legitimate idea how bad this truly is. China’s official data suggests the country’s GDP is growing nicely. I find this really hard to believe. I think their GDP is actually declining I believe their economy is deflating along with consumer prices.

Apparently so does Tamura Hideo, the senior staff writer for the Japanese newspaper Sankei Shimbun. Last month, China’s ‘National Bureau of Statistics’ reported that their 2023 ‘real’ GDP growth was 5.2%. Mr. Hideo believes the Chinese economy actually shrank by more than 2% in 2023.

Far on the other end of the spectrum, here in the US consumer confidence, consumer spending and home values are all up nicely. The US is inflating … and China is deflating. Hmmm …interesting.

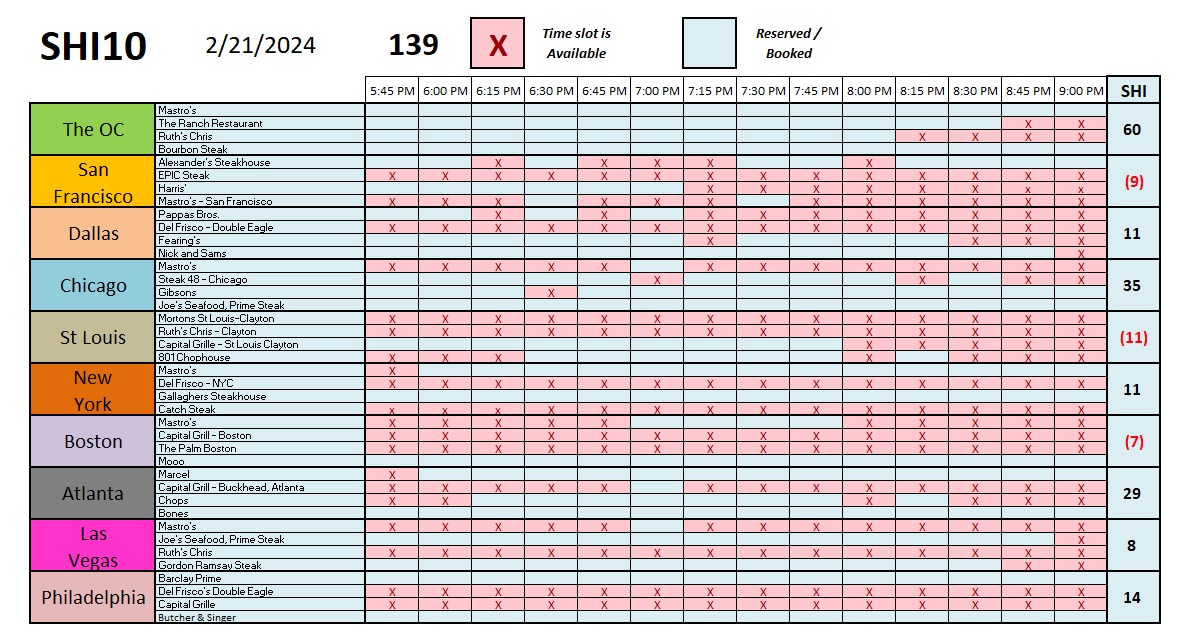

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding …. By the end 2023, in ‘current-dollar‘ terms, US annual economic output rose to an annualized rate of $27.94 trillion. After enduring the fastest FED rate hike in over 40 years, America’s current-dollar GDP still increased at an annualized rate of 4.8% during the fourth quarter of 2023. Even the ‘real’ GDP growth rate was strong … clocking in at the annual rate of 3.3% during Q4.

According to the IMF, the world’s annual GDP expanded to over $105 trillion in 2022. Further, IMF expects global GDP to reach almost $135 trillion by 2028 — an increase of more than 28% in just 5 years.

America’s GDP remains around 25% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

At more than $18 trillion, China is the world’s second largest economy. But I agree with Tamura Hideo: China’s GDP shrank 2023. And it will probably shrink faster in 2024. Thru an economic lens, should we be concerned? Might this financial contagion overflow their boarders a-la-Covid and adversely impact our American economy?

Maybe, but probably not. Companies with outsized exposure to the Chinese consumer may be in for a rough ride, but I don’t believe China’s problems will slosh over their borders.

But my read of the tea leaves is clear: China has entered a deep and long recession.

Ironically, the entire thing is self-inflicted. Government regulation triggered the collapse in their housing market which, in turn, triggered numerous other financial and economic problems.

The housing problem took root more than a decade ago. Home speculation became the national sport of China, with many households owning two, three or more homes — most of which remained unoccupied. Fast forward to 2020 when the China central government implemented a policy known as the “three red lines.” Party chairman Mr. Xi insisted, “Housing is for living in, not for speculation.” Speculation, he stressed, was the enemy of “common prosperity” and had to be stopped immediately. It did. The new regulations did the trick. All of a sudden, the massive home developers — like Evergrande and Country Garden — faced extensive borrowing restrictions. Eventually, Evergrande, Country Garden, and most of China’s other large home developers, unable to complete or sell homes, collapsed and are in various stages of failure.

In China, a failed investment is known as a “landmine explosion.” The term seems fitting to me. Tens of thousands of affluent Chinese folks have suffered from landmine explosions in recent months. According the The Economist magazine, an investment firm named Zhongzhi “went bust in December,” and owes its 150,000 clients $36 billion.

The magazine continues: “And explosions are not confined to wealth-management firms. By far the most common investment in China is property, and property values have been falling for almost three years. The stockmarket, too, is sliding: the Shanghai Composite, one of the most prominent indices, has dropped by over 20% since its peak in 2021. And whereas the government has in the past stepped in to help investors hit by plunging asset prices….”

The Economist magazine article continues,

“China publishes almost no official data about the distribution of wealth,

perhaps for fear of revealing just how unequal it is.”

Perhaps. I can’t imagine it’s worse than US inequality, but, on the other hand, unlike the US, China is a communist country supposedly promoting “common prosperity.”

Regardless, it turns out The Economist magazine found this topic as interesting as I do. Using their proprietary methodology, they were able to “yield a rough breakdown of who owns most of the financial assets that are losing value so fast, and so allowed us to infer what the swooning markets might mean for China’s economy and society.”

Their findings:

“The survey data suggest that about 50% of China’s wealth is in the hands of the 113 million or so people with a net worth of 1m-10m yuan. This cohort — just 8% of the population — has even more influence over financial markets than their wealth would suggest. They own 64% of all publicly traded shares, for instance, and 61% of investment funds….”

The article claims half of China’s housing wealth belongs to the “got-rich-first” group. And while there is no official, nationwide home price data, government claims ring false. The Communist party line is values have barely budged in Shanghai. But local economic experts disagree, suggesting they have fallen almost 30% in some areas and are likely to fall further in 2024.

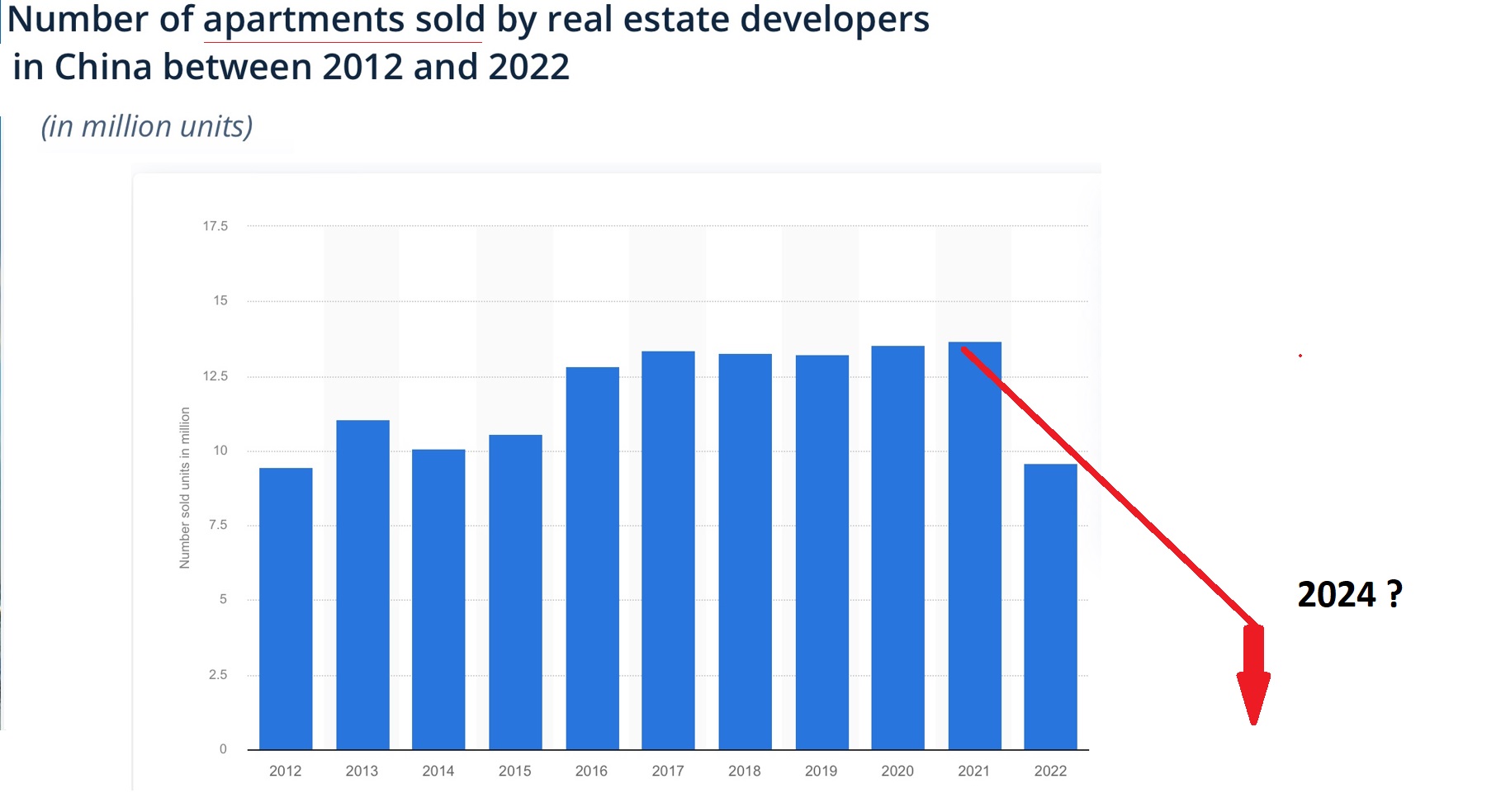

Chinese folks spent a total of about 16.3 trillion yuan buying homes in 2021. In US dollars, that’s about $2.25 trillion. (By contrast, here in the US, American homebuyers spent about $1.5 trillion last year.) This did not repeat in 2022 or 2023. 2022 fell off a cliff (below). We can only imagine how bad 2023 looked … and 2024 looks even bleaker still …..

China’s government created this problem back in 2020. Hoping to rein in accelerating housing speculation, they implemented draconian regulations designed to trim the fever. It worked. Housing sales are now plummeting.

Oddly, to this point, the government has not seemed too worried. Let the housing market crash, they seem to be saying. Pervasive deflation alone should have them at least a little concerned. Chinese authorities have been steadfast: To crush housing speculation, and prevent bubbles, they seemed to be saying, they had to remain firm.

According to that same article in The Economist magazine:

“They worry that too much of China’s household wealth—some 80%—is concentrated in housing, compared with about 30% in America, for example. There is little systemic risk: banks are well capitalised and mortgages form a relatively small share of their assets. Local governments, meanwhile, see a chance to acquire lots of apartments on the cheap, to be used as low-income housing.”

That statistic — if true — is amazing: 80% of household wealth in China is home equity? Staggering. And very concerning.

But finally, at last, the game of ‘chicken’ is over — China’s government blinked. This week, their central bank — the “People’s Bank of China,” also known as the PBOC, finally lowered their 5-year loan prime rate. The cut was not exceptionally large. But it proves China’s government is worried. Good. They should be.

Repeating, I don’t think China’s economic hardship, falling stock market, deflation, and a home-value crash will spread beyond their borders like an “economic virus.” Sure, there are many US companies that sell into China. Starbucks. YUM Brands. And, of course, Apple. But in the final analysis, the consumer challenges faced by a handful of US companies will not create any large ripples in our economy. But it’s important to keep these developments front of mind, if for no other reason than the potential for social unrest and/or military action. Nothing quiets down, and focuses, an unhappy population as quickly as a war, right? Ouch.

To the steak houses!

It’s no surprise that this week’s SHI is far lower than the prior “Valentines Day” boosted reading. Today’s reading — a solid 139 — is almost identical to that of two weeks ago. Unlike Chinese home values, the SHI has been quite consistent and stable. 🙂

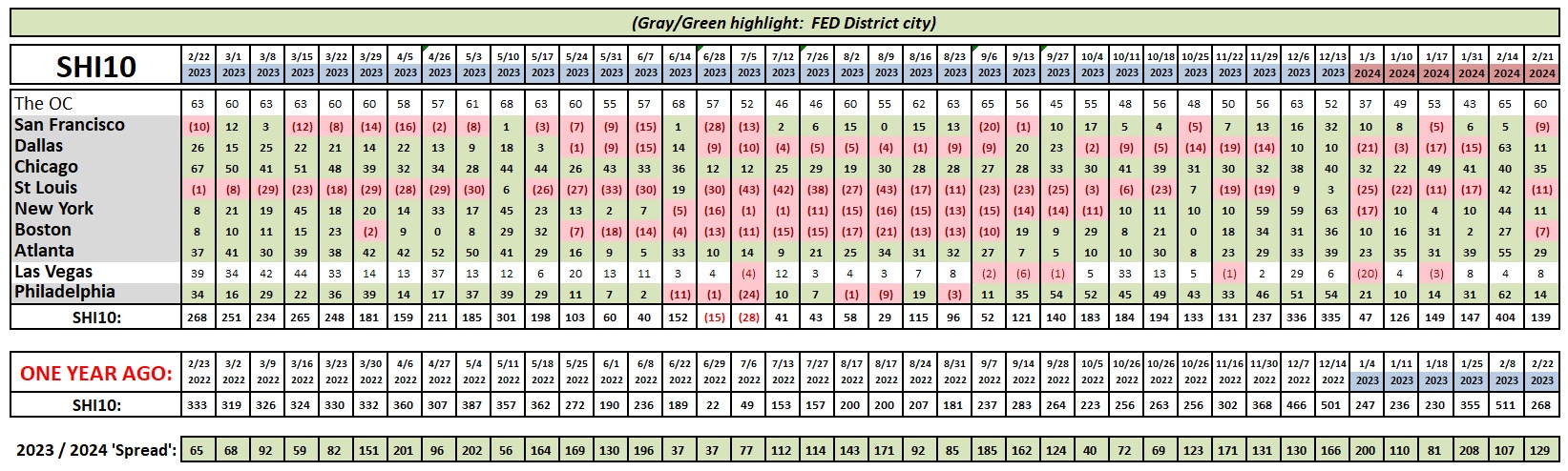

Here’s the longer-term trend chart.

Thanks for tuning in. Best,

<>–()–<> Terry Liebman

{kind=link}