SHI 4.15.20 – FOMO and LOCO in the Great Lockdown

SHI 4.8.20 – Musicians, Hotel Rooms, Employment, China and the FED

April 8, 2020

SHI 4.22.20 – Bailouts

April 22, 2020

“The world is closed … trillions are lost … yet the stock markets are soaring. What gives?”

Are stock traders going LOCO, like the rest of us, staring at 4 walls and 24/7 bad news on CNN? Is FOMO driving the market surge? How bad is the economic fallout and devastation?

Bad. New unemployment claims will be reported tomorrow morning — 5:30 AM here in CA for you early-birds — and I fear another 5+ million poor unfortunate souls will find themselves without work. All told, combined, I believe the number of unemployed folks here in the US will likely eclipse 20 million — perhaps 12% or 13% of our entire labor force. Horrible. But oddly enough, US stock markets are soaring, up about 25% from their “COVID-fear” low points just weeks ago. How can this be? Are all these investors just dumb … or do they know something we don’t? Or is this just a market pause before a larger, deeper decline?

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Before COVID-19, the world’s annual GDP was about $85 trillion today. No longer. It has shrunk sizable during ‘The Great Lockdown.’ I did not coin this phrase — the IMF did. The same folks who track global GDP. Until recently, annual US GDP exceeded $21.7 trillion. Together, the U.S., the EU and China still generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Years ago, a financial advisor told me, “Terry, the proverb, ‘It’s always darkest before the dawn‘ is a commonly accepted reality, but it’s actually not true. As a matter of fact, it’s always darkest before pitch black.” No, he wasn’t the cheeriest fellow. In fact, while he saw himself as pragmatic, I felt he was downright dark and morose. Regardless, the perspective is worth mentioning, especially as we grapple with the human and financial implications of COVID-19.

So, the existential economic question remains: Are we metaphorically heading toward a brighter dawn … or is it lights out? I’ll save the answer to this question until the end of my blog. For now, let’s dive into some data and try to make sense out of the current stock market behavior.

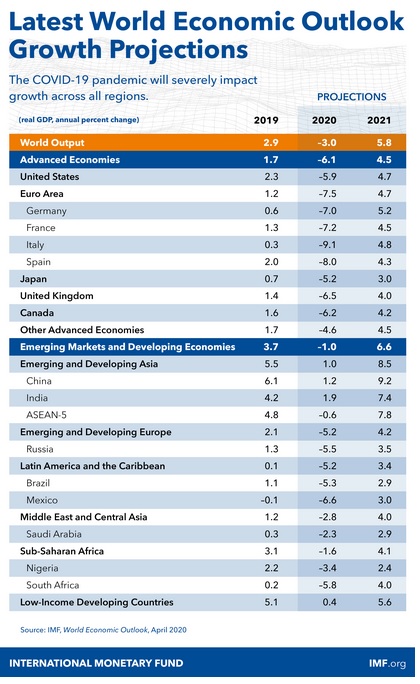

The IMF now believes The Great Lockdown — their phrase, not mine — will subtract about $9 trillion from 2020/2021 GDP. $9 trillion. Staggering. As you know, this amount is equal to about 10% of a full year’s economic output. To the right are the latest IMF country-by-country GDP forecasts. I won’t comment further … the numbers are clear, and you can read the chart. Of course, baked into these numbers are many assumptions, assumptions which may change depending on what happens in the next month.

In a teleconference on Tuesday, St Louis FED President Jim Bullard suggested the coronavirus quarantine is costing the US $25 billion a day in lost production. $25 billion. Each and every day.

Adding his own spin, on Tuesday Chicago FED President Charles Evans commented there is a “hopeful possibility” that the sharp recession facing the country can be a “temporary downturn,” but this optimistic view comes with several cautionary notes. “There are many caveats in the hopeful story line, and many, many things must go right in order to minimize the economic pain,” Evans said, during a discussion with students at Carnegie Mellon University in Pittsburgh. This notwithstanding, Evans said a candid assessment is that a deep downturn cannot be avoided.

Many economists are forecasting the US and the world will now experience the worst economic downturn we’ve seen in almost 100 years. I agree. This one is going to be bad. If my blog ended here, I wouldn’t blame you for heading to the liquor cabinet for a stiff drink or two. In fact, you might as well, because — hey, you’re at home — and while my comments below might temper your financial depression a bit, they won’t reverse them. Because make no mistake, the economies of the world are in deep, deep yogurt. So you may as well dive deep, deep into vodka. Or whatever your drink of choice might be.

All because of “The Great Lockdown.” Which clearly, has been anything but “great” for global economies. The lockdown was the government choice in most states, regions and countries, triggered at different times, across the globe, by the overwhelming human imperative from COVID-19. I understand. We all do. This pandemic is very real.

According to the latest statistics from www.worldometers.info, 210 “countries and territories” around the world are now reporting active cases of coronavirus. Which is amazing in itself, because, at last count, the world had 195 countries. Hmmm … what the heck is a territory? And when did we get 15 of them? Google it and you’ll find there are 61 territories across the globe. Who knew? 🙂

And with few exceptions, as we all know, the leaders across the developed world selected lockdown and “shelter in place” as the best choice to slow the spread. Or, said another way, perhaps they felt this was the best bad choice.

So it’s worth noting that Sweden took a different path. They made a different choice. Plenty has been written about their approach to “managing” the virus — mostly how foolish it it — and whether it was the right path or wrong. We’ll know in a month or two.

Essentially, Sweden has made the choice to take more “calibrated precautions,” isolating only their most vulnerable citizens. For example, gatherings of more than 50 people are prohibited, and high schools and colleges are closed. But Sweden has kept its borders open as well as its preschools, grade schools, bars, restaurants, parks, and shops. In doing so, they have made the opposite decision of almost every other developed nation. What’s their logic?

Johan Giesecke, Sweden’s former chief epidemiologist, and now adviser to the Swedish Health Agency, says that other nations “have taken political, unconsidered actions” that are not justified by the facts. From my perspective, Sweden’s theory asks: It is possible that the fastest and safest way to “flatten the curve” is to allow young people to mix normally while requiring only the frail and sick to remain isolated? No doubt, this is a bold choice. Let the “younger” folks do their thing … and quarantine only the older people and “high risk” groups — say everyone over 60 or 65 and those with impaired immune systems?

Is Sweden’s choice absurd? Inhumane? Irresponsible? Foolish and risky? You decide … and of course, we’ll know soon enough. But Sweden’s economy is less adversely impacted. Most businesses are open. Most restaurants are open. And most hard working folks still have their jobs.

The rest of the world cannot make the same claims. Much of it is closed. Tens of millions are unemployed. And yet, here in the US, our stock markets are soaring. At yesterday’s market close, the markets we up significantly from their (very recent) 52 week lows:

- The DJIA is up 31.5%

- The S&P500 is up 29.6%

- the Nasdaq is up 28.4%

So what the heck is going on? Are traders truly crazy … or is ‘fear of missing out’ — FOMO — ruling the day? Perhaps a dose of each? Or is something else at work here?

Something else is clearly at work here.

The market gains do not reflect traditional financial metrics. Corporate earnings have been pummeled, suggesting stock prices should be much lower, and yet they are not. Why? Why are stock prices behaving differently?

Because central banks and governments, around the world, have unleashed a double whammy: Fiscal and monetary stimulus, in scope and amounts never before seen, are flooding the globe. Never before, in the history of human existance, has this much financial stimulus rained down at once.

Knowing this would be bad, the FED acted quickly. Powell stressed that the FED has “lending” powers, not “spending” powers. But with lending powers firmly in hand, the FED wanted to assure the world that they were there to provide relief and stability “during this period of constrained economic activity” using their tools as “vigorous as possible.” Here are Chairman Powell’s own words:

- To those ends, we have lowered interest rates to near zero in order to bring down borrowing costs.

- We have also committed to keeping rates at this low level until we are confident that the economy has weathered the storm and is on track to achieve our maximum-employment and price-stability goals.

- Even more importantly, we have acted to safeguard financial markets in order to provide stability to the financial system and support the flow of credit in the economy.

- As a result of the economic dislocations caused by the virus, some essential financial markets had begun to sink into dysfunction, and many channels that households, businesses, and state and local governments rely on for credit had simply stopped working. We acted forcefully to get our markets working again, and, as a result, market conditions have generally improved.

- Many of the programs we are undertaking to support the flow of credit rely on emergency lending powers that are available only in very unusual circumstances-such as those we find ourselves in today-and only with the consent of the Secretary of the Treasury.

And finally, again quoting Powell, “We are deploying these lending powers to an unprecedented extent, enabled in large part by the financial backing from Congress and the Treasury. We will continue to use these powers forcefully, proactively, and aggressively until we are confident that we are solidly on the road to recovery.”

There you have it. Oh, and by the way, the FED balance sheet just eclipsed $6 trillion this week.

The list of countries offering monetary stimulus to their citizens is unprecedented:

- USA: $2.2 trillion

- Germany: $808 billion plus another $440 billion of loan guarantees

- Spain: $225 billion

- Japan: About $50 billion

- England: $40 billion plus numerous other wage programs and VAT waivers.

- Canada: Close to $40 billion in ‘tax deferrals’ and another $25 billion of aid to workers

- France: $50 billion plus another $330 billion of loan guarantees

- Italy: $27 billion plus $440 billion of “liquidity and bank loans to companies”

- The World Bank: $160 billion

- IMF: $70 billion

- China has pledged to “unleash trillions of yuan of fiscal stimulus”

… and the list goes on.

And this is why the stock markets are off their lows. The fundamentals may be bad, but the FED and the other members of the BIS (you remember the Bank for International Settlements?) are telling us they will not let the global economy fail. In fact, by these actions, central banks and governments are telling us they will do whatever it takes to ensure their economies survive COVID-19. Whatever it takes. And what it will take, frankly, is a whole lot of sovereign debt. More than we’ve ever seen before. As I said before, we’ll save this discussion for a more appropriate time. Because while the mountains of debt may prevent a global depression, this choice is not without its own set of implications.

Of course, at these levels the DJIA remains about 5,000 points below its recent 52 week high. Because no amount of fiscal or monetary stimulus can fix corporate earnings over the long term. Only the passage of time and the opening of American businesses can do that. So when will American business open? That’s the $64 trillion question. (It used to be the $64 billion question … I’ve updated it for the current circumstances.)

The $64 Trillion Question

Because only with a re-opening of the US economy — and the economies of the rest of the world — can we all begin to move back toward “normal.” Of course, the new normal will be not be the old normal. At least not until a vaccine is widely distributed or our aggregate ‘herd immunity’ is firmly in place. So, for the moment, let’s talk about the new normal without considering a clear and decisive medical solution.

Other countries have re-opened on a limited basis. China, South Korea, and this week, Austria. Austria is following these guidelines:

- It is compulsory for people to wear a mask in supermarkets and pharmacies

- From Tuesday (the 14th), shops under 4,300 sq ft in size are allowed to reopen, along with hardware stores and garden centers

- Larger shops, shopping centers and hairdressers can reopen from May 1st

- Restaurants and hotels could reopen from mid-May if health conditions allow

Other developments:

- Denmark was already opening schools for younger children from Wednesday, but Prime Minister Mette Frederiksen says hospital cases are falling so she will talk to other political parties about a further relaxation of the lockdown measures

- Spain allowed some businesses to return to work

- Poland will gradually lift restrictions on its economy from Sunday, probably starting with shops

- Montenegro’s authorities are to prevent church services from taking place over Orthodox Easter at the weekend

Here in California, previously the home of the 5th largest economy in the world, our governor recently commented his team is considering 6 metrics as they ponder re-opening timing:

- Expanding testing

- Protecting high risk groups, including seniors, the medically vulnerable and people in facilities like nursing homes

- Ensuring hospitals have enough beds and supplies to care for patients

- Progress in developing treatments

- Ability of schools and businesses to support physical distancing

- Ability to decide when to reinstitute stay-at-home orders if needed

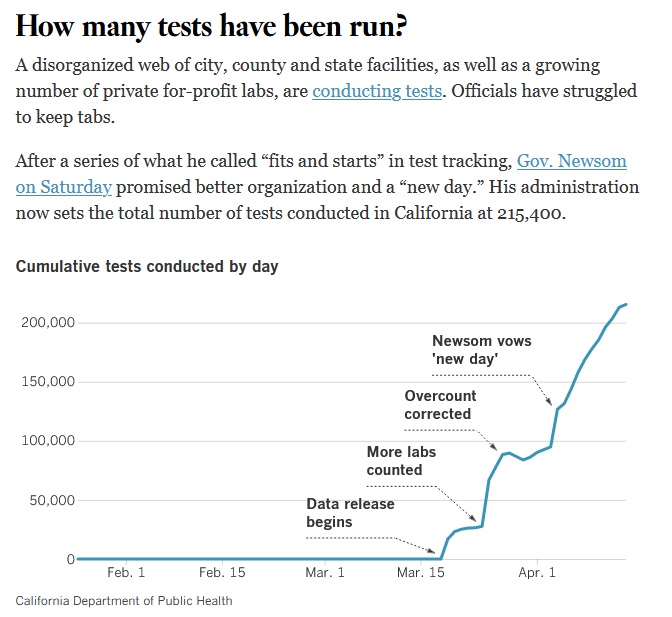

Testing is an interesting metric. So far, the US has done a pretty dismal job. As of April 13, fewer than 3 million people have been tested. Less than 1% of our total population. And yet most medical professionals and politicians tout wide-spread testing as one component of the solution.

As you can see from the graphic to the left, California isn’t doing any better. Of the almost 3 million tests completed in the country, to date 215,400 of them are from California. California has a population of almost 40 million people, so we haven’t even tested 1% of our population. And yet “expanded testing” is one of the primary metrics determining when our economy re-opens?

This is disappointing. One would surmise that in a country where the shutdown is costing us about $25 billion each and every day, our leaders could have done a better job with testing. Alas.

On the other hand, disappointment aside, we have to acknowledge that for the first time in human history, everyone on the planet is laser focused on one thing: COVID-19. Every day, all day. Behind the scenes, tens of millions of people are working around the clock to find or create unique medical solutions. So while we don’t know when or where solutions will show, we must expect they will. A testing solution will be found soon. And medical solutions must surely follow closely thereafter.

Today is April 15. While The Great Lockdown started on different dates in different places, here in California it began on March 19th. Amazing, right? This was less than one month ago … but it feels like an eternity. So it testing is a prerequisite to freeing all of us “stay at home” prisoners, Governor Newsom, then let’s get on with it!

When will the US re-open? When will Californians be free to mingle once again?

Soon. Probably sooner than you think. Locally, across the state, in the US as a whole, we still have obstacles to overcome … but we’re getting closer. Here in California, new cases in many counties have slowed dramatically. Hospital resources in California exceed need by 10X. Every day, the data changes and evolves. Every day, we are one step closer to a wide-spread testing and medical solution. Assuming we consider the governor’s “6 metrics” when making a re-opening forecast, it makes sense to believe:

- Between now and the end of April, I believe new cases across the state will continue to significantly decline and our hospitals will easily meet resource demand.

- This will permit more dialog around restarting the local economies as economic imperatives grow louder and occupy more of the conversation.

- Counties in California will re-open at different times based on local conditions.

- Different businesses will re-open at different times, depending on how each is able to solve the issues around face masks, temperature checks, and maintaining appropriate social distancing.

Earlier today, Cinemark movie theaters announced they plan a “soft” opening late-June and want to be fully open by July 1. Not fully, of course, and they feel they can “break even” at 20% or 30% occupancy. Interesting.

Other businesses should be able to open much sooner. When? I’ll be surprised if we don’t begin the re-opening process by the first week in May.

There remains much to do, and data changes daily. But I believe this forecast is reasonable. How about the stock markets? Will these levels hold? That’s a tougher question, but remember this: Historically, our financial markets tend to reach their lowest ebb well before the crisis triggering the declines has passed. Are the market lows behind us? Today I would say yes. But this forecast, too, is very dependent on a rapidly changing landscape.

However, regardless of the precise date, as segments of California business spin up again, they will be confronted with a very different business climate. Furloughed and fired employees will be re-hired, at different times, speeds and quantities, and so the unemployment levels will recede. But the unemployment rate will only recede at a pace highly correlated to, and inverse to, the speed of business re-opening. Business re-opening is the key to solving the unemployment problem. And the business revenue problem. The quicker the re-opening, the sooner our unemployment levels will fall. But make no mistake: It will be impossible for California, the US and the world at large to avoid a recession. How long will this recession last? I believe the answer is not long. I don’t anticipate a “V” shaped recovery. One pundit suggested the recover will resemble the Nike ‘swoosh.’ I agree.

However, decisions to re-open our economies made in the next 30 days will have a dramatic impact on how quickly our economies recover. Let’s hope our leaders keep this fact front of mind as they consider their choices.

Best of luck out there. Stay safe my friends!

– Terry Liebman