SHI 7.14.21 – Poor Pepper!

SHI 7.7.21 – Rolling the Dice in ‘Vegas!

July 7, 2021

SHI 7.21.21 – Working Without a Net

July 21, 2021

Who doesn’t love pepper, right? It is an essential spice, used by all our steak houses!

But apparently, one particular type of ‘pepper’ was found to be a bit to, well, ‘spicy’ to tolerate. Dressed in the vestments of Buddhist clergy and programed to chant sutras, Pepper the robot was ready to go to work! Pepper had been hired by Nissei Eco, a Japanese plastics company also happens in the funeral business, to read scripture to mourners. What a great, cost-effective idea! But Pepper kept breaking down during practice runs. The funeral-business manager was mortified. So she got fired. Poor Pepper!

“

Everyone loves pepper!“

“Everyone loves pepper!“

Well, no, apparently not everyone loves Pepper.

Pepper has failed to perform up to par in a number of gigs. According to the WSJ, she “botched” her job at a nursing home … and gave baseball fans a creepy feeling. So much, apparently, that Pepper herself may soon need a funeral. 🙂

‘Automation’ of ‘human’ jobs doesn’t always work. Sometimes a machine cannot do the job. A human is needed.

But what if NONE are available to hire?

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

The short answer? Expanding. A lot. Forever more, COVID-19 will be mentioned concurrently with any discussion about 2020 GDP. Collectively, the world’s annual GDP was about $85 trillion by the end of 2020. But I am confident all 2021 GDP discussions will start with a nod to the blowout 1st quarter GDP growth number, because our ‘current dollar’ GDP grew at the annual rate of 10.7%! Annualized, America’s GDP blew past $22 trillion during the quarter, settling in at $22.05 trillion. The US, the euro zone, and China continue to generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

The Covid public-policy response across the globe forced many hotels and bars to close. Millions of workers instantly lost their jobs. And while many of those unfortunate folks remained on the unemployment sidelines, quite a few moved on, exploring new careers in businesses that thrived during the pandemic like mortgage, shipping, digital-sales and technology,etc. Tens of thousands of these hard-working folks have moved on and out of the hospitality business. They have left quite a large hole in their wake.

To lure some back, restaurants and other hospitality operators have boosted compensation: In fact, the “average hourly wage” now paid for hotel and food-service labor, according the the Labor Department, is $15.14. This is quite a sizable increase from January of 2019, when the number was $13.38 per hour — more than 13% less than today’s wages!

Which helped. During June, restaurants and bars added 194,000 workers back to their payrolls.

But they still need another 1.3 million, just to catch up with pre-pandemic employment levels.

Some Covid-generated supply disruptions will self-fix over time. This one may not heal quickly. What is a restaurant or bar to do? Enter the “MATRADEE!”

According to Richtech Robotics, the Matradee is capable of opening kitchen doors, and delivering food to the table, using ‘Visual Nav’ and ‘LiDAR’ to detect — and navigate around — obstacles up to 20′ away. Need to clean up a mess? No problem! Send in DUST-E, an acronym for “disinfecting ultra-autonomous sweeping technology – express.” He’ll do the trick! Curious? Check out their website (right click, open in a new tab):

https://www.richtechrobotics.com/

Will it work? Will ‘Matra‘ and ‘Dusty‘ get a better reception than Pepper? Who knows.

But this is only one of many budding automation solutions. For example, in June ten (10) McDonald’s restaurants in Chicago announced they are testing “automated drive-thru ordering” systems using artificial intelligence software. Companies like Eflyn offers fully automated “self-order” and ‘point-of-sale’ (POS) kiosks for quite a few food (and other) operations, including food trucks. And others like Lightspeed now offer “tableside mobile POS systems” for contactless ordering and payment. If hospitality labor costs and challenges continue to increase, the speed of automation solutions will likely increase as well. It’s quite possible that in just years from now, we’ll see more automation than humans in restaurants and bars.

But in the mean time, I have to repeat an earlier admonition: Your wait time at your favorite steakhouse may be longer than it was pre-pandemic. If you remember to bring your own bottle of wine and your own wine key — you’ll have to borrow a wine glass from the table — you’re all set! Let’s see how the steakhouses are doing this week.

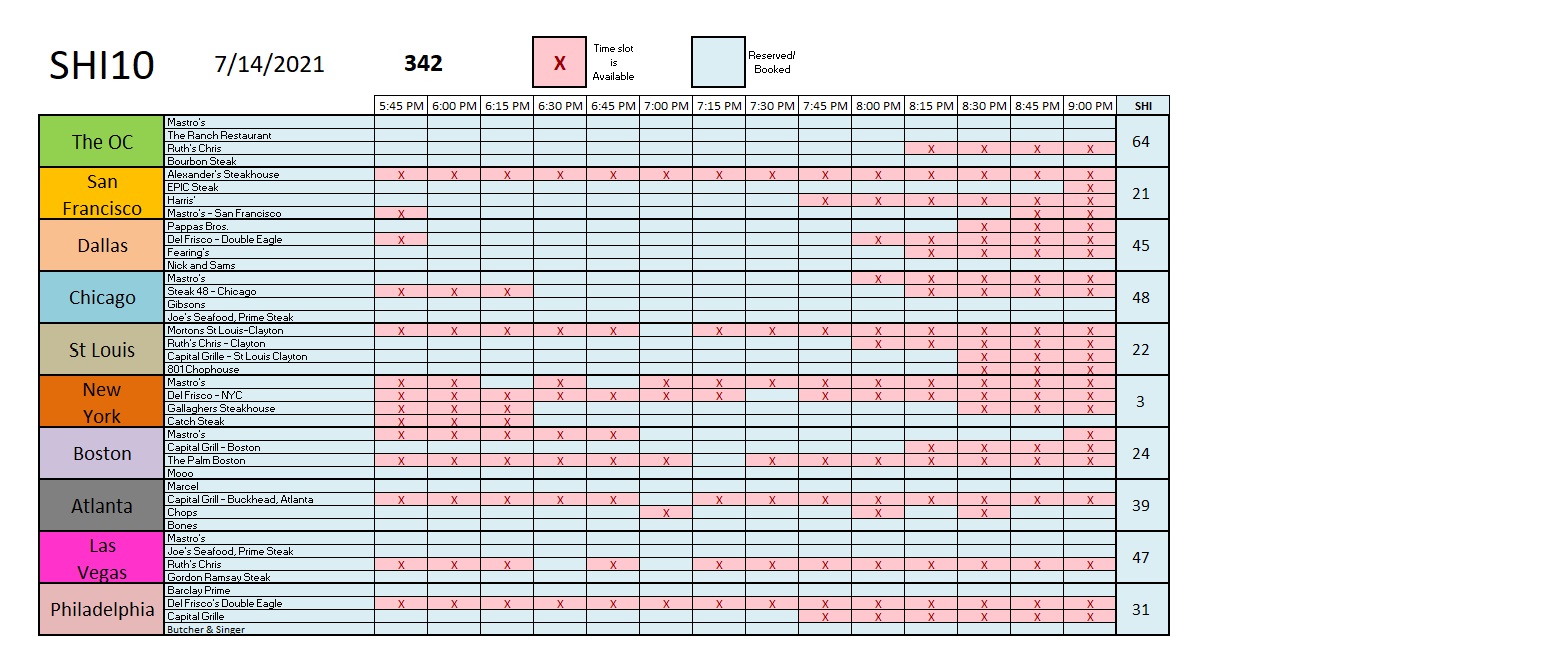

Like last week, the answer is “pretty good!”

Interestingly enough, from my perspective at least, expensive steakhouse reservation demand seems to be “normalizing” — at a high level, of course, but normalizing. Reservation demand tends to peak at or near the 7:30 time slot. Meaning that in a typical week, there will be fewer 7:30 time slots available than, say, 5:45 or 9:00 pm. And that trend is obvious from the grid above. There is more “blue” — representing an open table/reservation slot — around the ‘7:30 pm’ column than most other time slots.

It’s also worth noting that each of our 10 SHI cities are “in the black” so to speak — all SHI numbers are positive. That has not happened in quite some time. Here’s the longer term trend report.

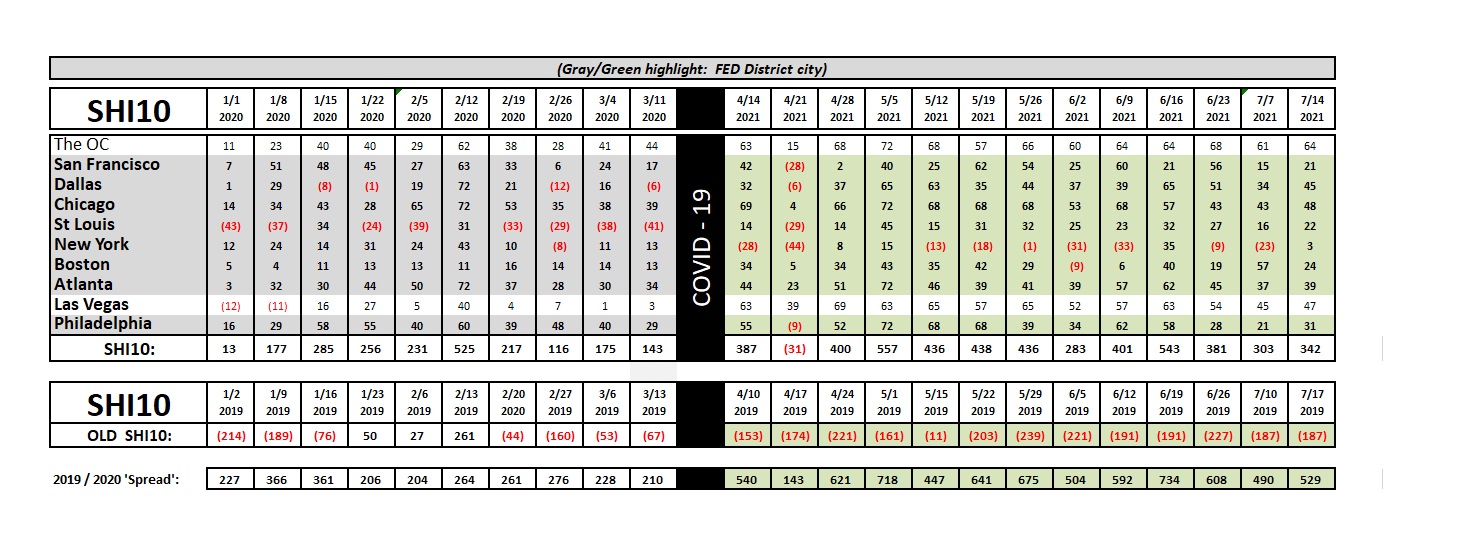

From the trend report above, we see the ‘Spread‘ remains quite high, indicating once again the strength of reservation demand across the country, and by extension the strength of the economic recovery.

The FED just released their most recent ‘Beige Book’ surveys across their 12 Federal Reserve Districts. They generally agree with the SHI10 assessment above. Here are some excerpts from the report:

Overall Economic Activity: The U.S. economy strengthened further from late May to early July, displaying moderate to robust growth. Sectors reporting above-average growth included transportation, travel and tourism, manufacturing, and nonfinancial services. Supply-side disruptions became more widespread, including shortages of materials and labor, delivery delays, and low inventories of many consumer goods. Strained car inventories resulted in somewhat lower car sales despite steady demand, and home sales rose slightly despite limited supply. Non-auto retail sales grew at a moderate pace on balance, and tourism was buoyed by the further abatement of pandemic-related concerns. Residential construction softened in several Districts in response to rising costs, while commercial construction was mixed but up slightly on balance.

Employment and Wages: Healthy labor demand was broad-based but was seen as strongest for low-skilled positions. Wages increased at a moderate pace on average, and low-wage workers enjoyed above-average pay increases. Labor shortages were often cited as a reason firms could not staff at desired levels, with firms in three Districts delaying expansion or scaling back services due to understaffing. All Districts noted an increased use of non-wage cash incentives to attract and retain workers.

Prices: Prices increased at an above-average pace, as seven Districts reported strong price growth and the rest saw moderate gains. Pricing pressures were broad-based and grew more acute in the hospitality sector, as the reopening of hotels and restaurants confronted limited supplies of materials and workers. Construction costs remained high, but lumber prices reportedly eased a bit. Container prices returned to very high levels after having moderated in the spring. While some contacts felt that pricing pressures were transitory, the majority expected further increases in input costs and selling prices in the coming months.

Clearly, things are cooking out there. Both “steak” and “economically” speaking, activity is hot. And at the center remains the debate of just “how hot is it?” and what implications, if any, this super-heated economy will have on longer-term inflation. We’re certainly seeing plenty of the “transitory” type right now, assuming it is, in fact, transitory. And short-term (1-year) consumer inflation expectations expectations are also heating up like a T-bone on the Catch Steak grill — it increased 0.8% in June up to 4.8%. Note: It had been hovering closer to 2.5% for quite some time. But longer term expectations showed a more luke-warm increase … which is positive news.

Our economy has a head of steam and a long way to run. In my opinion, all the noted challenges aside, it’s ‘risk on’ time. 🙂

Good luck out there.

- <|> Terry Liebman