SHI 8.14.24 – Making The Round-Trip

SHI 8.7.24 – Follow the Data, Not the Fear

August 7, 2024

SHI 8.28.24 – Tennis Millionaires

August 28, 2024“Transitory,” the FED said. The post-Covid inflation spurt was transitory.

And, of course, when the consumer price spike did not vanish quickly, the FED was excoriated. But essentially, at that time, I agreed: Consumer price inflation, I believed, would prove transitory. Of course, in the final analysis, your feeling on the outcome depends on your definition of the term. Here’s what I wrote on the topic about 2 1/2 years ago:

https://steakhouseindex.com/shi-2-23-22-keep-calm-and-dont-panic/

Pay particular note to my comments in blue:

“Consumer inflation is a serious concern for us all. American citizens are concerned and unhappy with current conditions. We were all much happier last year when the Treasury was handing out trillions of dollars, right? I feel the FEDs earlier characterization of inflation as “transitory” has given American’s the wrong idea — even if it does eventually prove transitory. Which I believe it will.”

“

CPI inflation is sooo yesterday.“

“CPI inflation is sooo yesterday.“

But as I said over 2 1/2 years ago, while today’s CPI reading definitively shows excessive price inflation is behind us, the impact lingers in our economy. And, in fact, the impact of the inflation spurt will, in my opinion, be permanent. As I commented back in February of 2022:

“Here’s where many American’s have it wrong: Once this bout of consumer inflation is reduced closer to longer-term trend inflation rates, prices will not retreat. I think many people believe that’s what the FED meant by transitory. No, I’m sorry to say consumer prices will likely remain at their elevated levels, but the rate of future price change will diminish. We are at a new price plateau, folks. The inflation rate will moderate … but not prices.”

Well said, Terry, if I don’t say so myself. 🙂

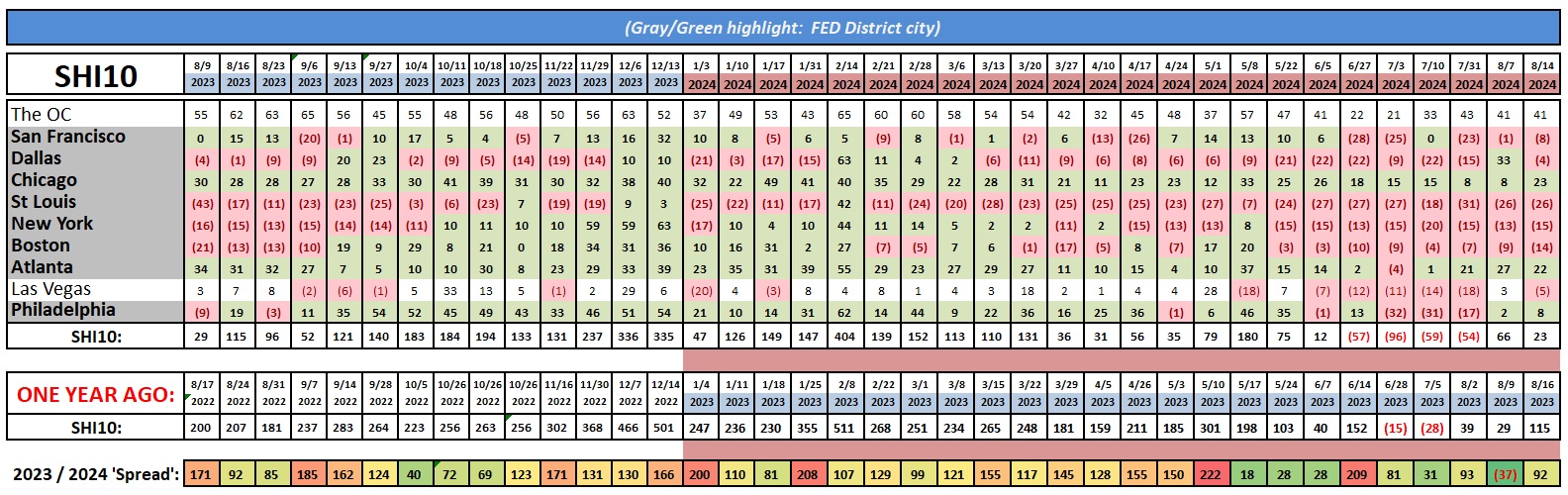

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. But is the US economy expanding or contracting? Expanding …. By the end of Q2, 2024, in ‘current-dollar‘ terms, US annual economic output rose to an annualized rate of $28.63 trillion. After enduring the fastest FED rate hike in over 40 years, America’s current-dollar GDP still increased at an annualized rate of 4.8% during the fourth quarter of 2023. Even the ‘real’ GDP growth rate was strong … clocking in at the annual rate of 3.3% during Q4.

According to the IMF, the world’s annual GDP expanded to over $105 trillion in 2023. Further, IMF expects global GDP to reach almost $135 trillion by 2028 — an increase of more than 28% in just 5 years.

America’s GDP remains around 25% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

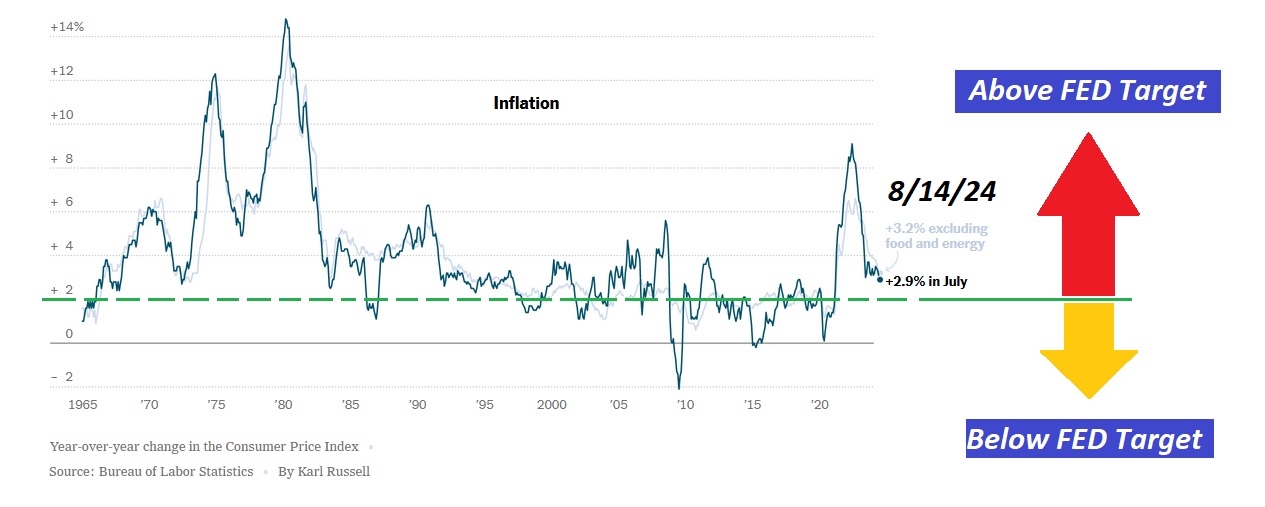

Take a look at this image, clipped from today’s New York Times:

Of course, I added the arrows and ‘tags’ on the right, and the ‘green line‘ showing the FED‘s target inflation rate of 2%. And the date, too. I added today’s date.

Because it’s worth noting that the inflation spike was transitory. At least thru a 50 year lens. Was it transitory thru a shorter lens? I guess that really depends on your definition of ‘transitory.’

The CPI really began hopping in April of 2021. By June of 2022, the “percent change from 12 months prior” had reached the annual rate of 9.1%. Ouch. Today, that rate clocked in at 2.9% — identical to July of 2018. We’ve come full circle.

However, while the inflation rate may have come full circle, prices have not. No, consumer prices are much higher — many by 25%, 30%, or more. And there they are likely to remain. From here, of course, now that the CPI rate is lower once again, moving toward the FEDs target, overall price increases will be much smaller.

But, I’m sorry to say, folks, prices are not coming down any time soon. Sorry. Get used to it. The inflation monster may have been tamed by some combination of FED rate hikes and supply chain healing, but the lasting result will be much, much higher prices across the board.

So what do we do? I suggest you go get a nice steak at Mastros. Sure, it will cost you a ton, but, hey, it’s only money. And after that large inflation spike, your money isn’t worth what it used to be!

Apparently, some people have taken my advice. The steak houses should be fairly busy this Saturday. But not packed. Pre-Covid, The Ranch restaurant here in the OC was generally fully booked by Wednesday for a table of 4 this Saturday next. Not today. Many reservation slots are available. And the same is true in most SHI cities. Plenty of reservation slots are available.

But as you can see in the longer-term trend grid below, this weeks SHI10 reading, while not setting the world on fire, is at least in the black.

Today’s CPI reading was likely the final data point the FED needed before inking a rate cut after their September meeting. The only caveat I’d offer is this: There is one more CPI report before the FED meeting in mid-September. If that number offered a big (negative) surprise, that might give the FED pause. But, in my opinion, a FED rate cut is now fully baked.

Expect a 25 basis point cut in September.

Which, of course, will thrill the Democrats and really irritate the other guys. Politicians will definitely see the rate cut as politically motivated. I don’t agree. It’s time to begin to cut rates. Politics aside. It’s time.

<:> Terry Liebman

{kind=link}

{kind=link}