SHI 2.23.22 – Keep Calm and Don’t Panic

SHI 2.16.2022 – A War of Words

February 16, 2022

SHI 3.2.22 – Rising Uncertainty … Uncharted Waters

March 2, 2022

“Let’s talk calmly about Ukraine, consumer inflation, interest rates, and supply chains.

Global financial markets are filled with fear and anxiety today. What an amazing quantum shift from just a month or two ago.

“

These are transitional times.”

“These are transitional times.”

… and let’s keep everything in perspective, OK? Yes, these are transitional, uncertain times. No doubt, things are changing all around us. But they are not as bad as they might seem in the media …let’s establish some perspective.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Significantly. During 2021, nominal growth clocked in at $2.1 trillion. The US annual economic output was just under $23 trillion for the full year. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Things happen for a reason. Usually. But sometimes reasons are hard to decipher — until much later. Take the Ukraine “situation” for example. Why is Russia doing what they are doing? For that matter, what ARE they doing? We don’t really know right now. All we can do is stay calm, assess developments as they occur, and navigate economic and financial obstacles as they arise.

Ukraine, consumer inflation, interest rates, and supply chains

Perhaps Russia has a legitimate beef in the region. I really don’t know. But there are plenty of other potential explanations for Russia’s potential (second) invasion of Ukraine. One explanation might simply be because they can. Who’s to stop them? Russia is a natural resource powerhouse. The world needs their oil. And western Europe REALLY needs their natural gas. Especially Germany. Sanctions aside, Russia will continue to export petroleum products … just as the equally unstable middle east does … because the world is completely dependent on Russian petroleum products. Here’s a one-year chart showing the price of WTI:

As of this morning, WTI was trading above $92 per barrel. Up from about $70 when the new year began. This is why you’re paying close to $5 for a gallon of gasoline at the pump — at least here in CA. And this is one of the reasons consumer prices are up significantly.

Consumer inflation

But as bad as the per-gallon price might be here in CA, the Ukraine problem is far worse for western Europe. In the short term, their citizens are in for a lot of economic pain … as the price of petroleum products continue to skyrocket. This “problem” might push the EU into a recession. Sure, Europe and the US are both pushing hard for “green energy” but unfortunately a conversion to renewable energy sources will take decades, not a few years. In the mean time, US production of oil and natural gas should protect our economy from too much damage. Europe is far worse off; here, the economic impacts will not be too bad.

But consumer inflation is sure to be adversely impacted. And the CPI will continue to impacted if petroleum prices remain high. As price is purely a supply/demand relationship, price movement is very difficult to predict with any accuracy. But in the near term, I expect petroleum prices to remain elevate.

Consumer inflation is a serious concern for us all. American citizens are concerned and unhappy with current conditions. We were all much happier last year when the Treasury was handing out trillions of dollars, right? I feel the FEDs earlier characterization of inflation as “transitory” has given American’s the wrong idea — even if it does eventually prove transitory. Which I believe it will. Here’s where many American’s have it wrong: Once this bout of consumer inflation is reduced closer to longer-term trend inflation rates, prices will not retreat. I think many people believe that’s what the FED meant by transitory. No, I’m sorry to say consumer prices will likely remain at their elevated levels, but the rate of future price change will diminish. We are at a new price plateau, folks. The inflation rate will moderate … but not prices.

Supply Chains

Global supply chains are broken or damaged. Some permanently. After almost 40 years in the making, globalization is no longer the economic darling we all grew to love pre-pandemic. Nor do I feel it ever will be again. The bloom is off the rose. 🙂

The manufacture of products important to a country’s safety and internal security — however they define it — will probably move back inside that country. The pandemic and Russian aggression have both assured that outcome. But products like that exceptionally cheap toaster at Walmart and those $20 kids shoes at Target will continue off-shore manufacturing, as those and other similar products will never be essential for internal country security and welfare.

Of course, the on-shoring to manufacture those essential products will also increase the prices of those products. The more important a product is to America’s health, economic vitality and internal security, the higher the price is likely to become. Sorry, President Biden, this is more bad news on the consumer inflation front.

Interest Rates

They are moving up. The 10-year Treasury already has moved up. And mid-March, the FED is almost certain to do the same with short-term rates. I expect a 25 basis point increase in the FED funds rate, the Prime Rate, SOFR and every other related index. Rates are moving up. Only in this way can the FED attempt to discourage and slow consumer spending.

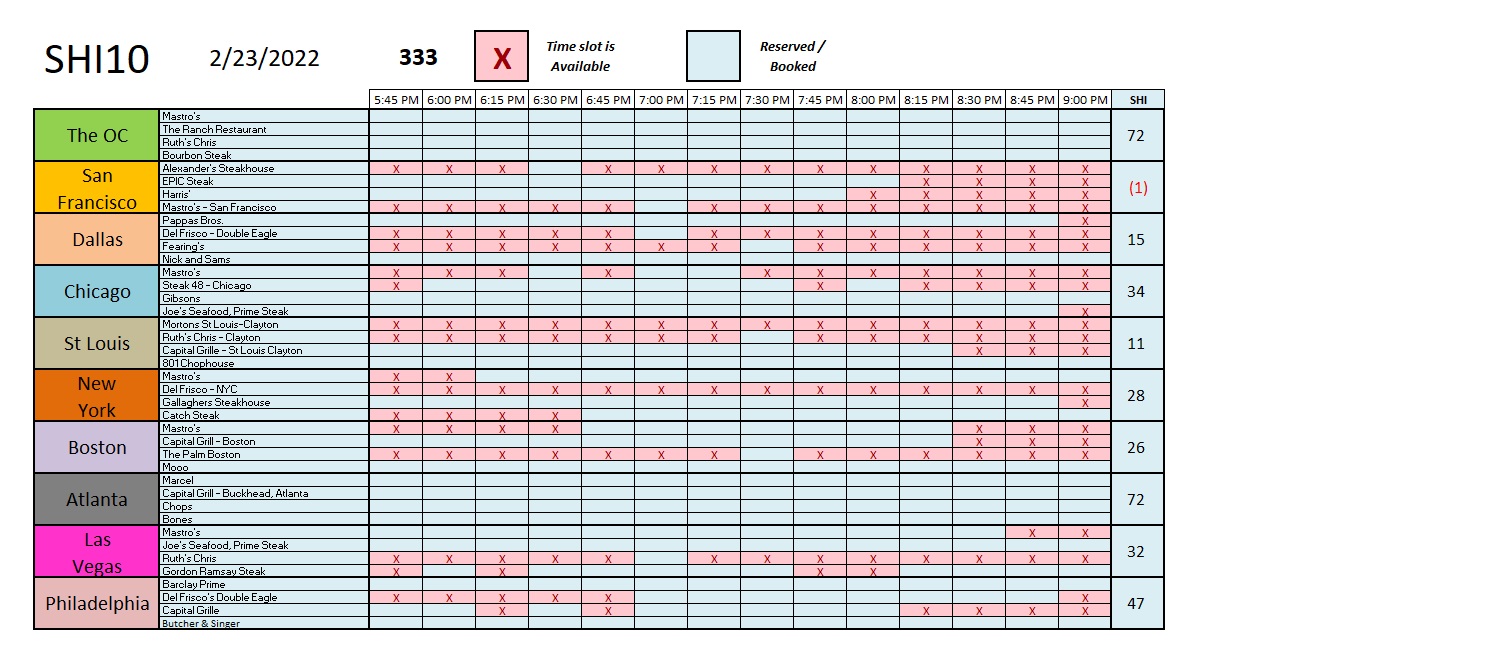

But keep this in perspective: Short term rates have been at their current levels for years now — essentially zero. Thus a 25 basis point increase is almost insignificant in the big picture. And assuming the FED actually raises short-term rates 6 times in the next 8 or 9 months — something I do NOT personally expect to happen — short term rates would only be about 1.50%. By historic standards, that’s an exceptionally low rate. So remain calm, don’t panic, and take it as it comes. Things aren’t as bad as the media might suggest. Are the steakhouses still doing well? Is reservation demand at our pricey steakhouses still holding up with all these worries? Let’s take a peek:

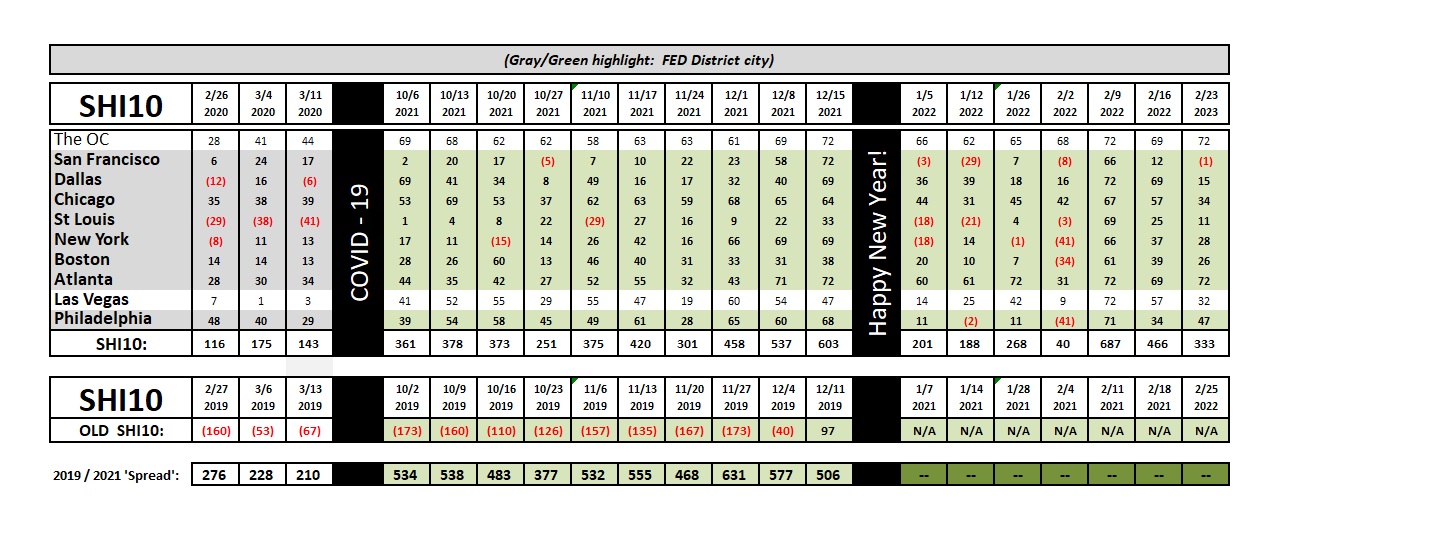

Yes, they are! It’s a mixed bag, to be sure, with steak-lovers in the OC and Atlanta grabbing every available table for 4 this coming Saturday. If you live in either area, you will probably be grilling your Tomahawk T-Bone at home this weekend. On the other hand, tables are widely available in San Francisco and St Louis; and expensive eatery reservations in Dallas, this weekend, are also surprisingly wide open. Here’s the longer term trend report:

The SHI10 is telling us that the US economy has already let off some steam. Economic strength seems more patchy, more geographic, than before. Clearly consumer behavior responds to elevated inflation, FED rate-hike talk, and Ukrainian invasion threats. Not in a binary fashion, mind you, but in shades. As the consumer moderates their consumption, US GDP numbers should soften from their hyper-active levels, and the FED will likely moderate their behavior in response. Everything is connected and the FED will be data-dependent when making interest rate choices over the coming months.

Economically speaking, the American economy remains vibrant, and should continue to be, in spite of all the anxiety and worry.

<:> Terry Liebman