SHI 2.16.2022 – A War of Words

SHI 2.9.22 – Fun With Numbers!

February 9, 2022

SHI 2.23.22 – Keep Calm and Don’t Panic

February 23, 2022

“Every battle is won before it is ever fought.” – The Art of War, Sun Tzu.

Talk of war is all around. On the border of Ukraine. And here in the US. Here? Yes, here. The FED has “declared war” on inflation. Sure, the FEDs war is a very different type of war … or is it? It’s entirely possible that Russia will “invade” Ukraine — again — but just like the FED battle, I believe the battle in Ukraine is a war of words, too. My opinion. Time will tell.

Sure, we know Russia has moved a large military force — reported 150,000 troops strong — to their border. And, yes, they could “invade” any time. But keep in mind that Russia previously owned the equipment. And they previously employed the troops. Both were simply moved from one place to another. My point? The movement of equipment and troops to the border has cost Russia nothing … except, perhaps, the cost of gasoline to move the tanks. And Russia has plenty of gasoline.

So, for the moment, let’s assume the “Ukraine conflict” is also a war of words…and Russia has no intention to move across the border. In this scenario, how might Russia define a “win” here?

“

The economics of war and words.”

“The economics of war and words.”

War has chanced since Sun Tzu’s time. Words move faster than bullets today.

So what is Russia’s objective in Ukraine? Has Ukraine insulted Russia in some way? Is national pride at risk? Or does Russia want to annex Ukraine because the country is geographically or strategically important? Could Ukraine contain natural resources important to Russia? Or is some other factor driving Russia and Putin?

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Significantly. During 2021, nominal growth clocked in at $2.1 trillion. The US annual economic output was just under $23 trillion for the full year. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

I am suggesting Russia’s actions in Ukraine are primarily economic.

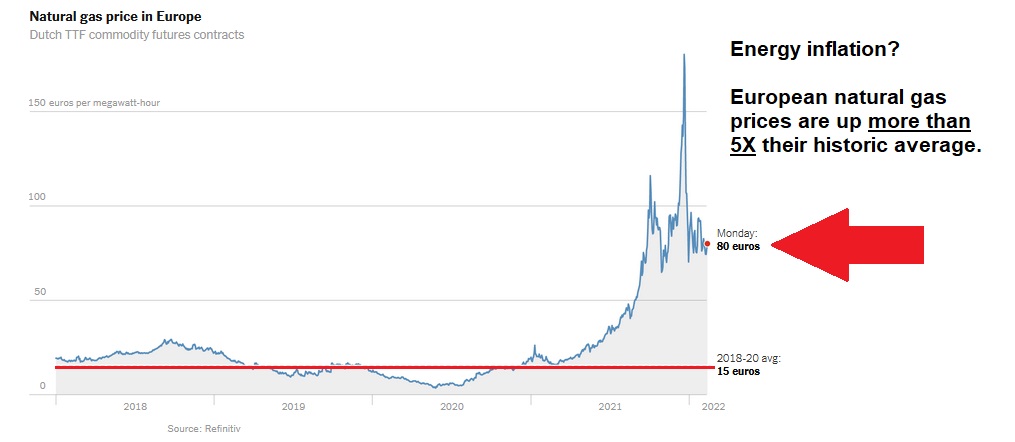

Again, I could be very wrong … but stay with me for a few minutes. Let’s explore what a Russian “win” might look like here. Could Russia’s decision to amass troops, tanks and armor on the border be primarily economic? After all, since the move, natural gas prices in Europe are thru the roof. Take a look at this graph:

:

That’s right. The price of natural gas in Europe has increased by more than 500% in the past year or so. As you see above, the index price increased from 15 euros to over 80 euros in a very short time. How does this move benefit Russia you ask? You may be surprised to learn that Russia owns almost 25% of the world’s natural gas reserves. Another fun fact: The Russian company Gazprom produces the most natural gas in the world. They produced over 431 billion cubic meters of gas in 2020. And where do they sell all their gas? To their west … Europe.

There is nothing natural or normal about the price movement we’ve seen in the past year. The movement is man-made. And it’s all fear based. This, I suspect, was Russia’s primary objective when they moved troops to the border.

Of course, just about every news report we see focuses on the “NATO angle” — and the suggestion that Russia is considering invading and annexing Ukraine for internal security reasons. If Russia can keep Ukraine from joining NATO, the reports suggest, then they will have a large land buffer between themselves and Europe should hostilities break out. I’m a skeptic. I contend they have amassed troops on the Ukraine border to trigger fear, a natural gas price spike, and frighten European countries dependent on Russian oil and gas. Frighten? Yes. The Nord Stream Pipeline, primarily owned by the Russian company Gazprom, carries natural gas from Russia to Germany. Nord Stream 2, which has yet to “open,” originates near St Petersburg, travels 1,200 kilometers under the Baltic Sea, and also ends in Germany. #2 will double the annual capacity of #1. If Russian actions can inspire enough fear and anxiety inside Germany and the European Union as a whole, I believe (1) they’ll get approval to turn on #2, and (2) they will be making a boatload more money. Thru Russia’s lens, it’s a HUGE win.

This price movement was not triggered by a simple supply/demand fluctuation. How do I know? Well, ask yourself these question: Has something, some event, triggered a 500% increase in demand for natural gas in Europe? No. Nothing. OK, well, then has something caused a significant reduction in supply? Yep. It’s a supply thing. Or, at least, fear of a supply constriction. So, with prices up 5X, it’s a darn good thing Gazprom had the foresight to build a second pipeline, right? And, ironically, #2 is ready to turn on right now! All they need is EU approval! 🙂

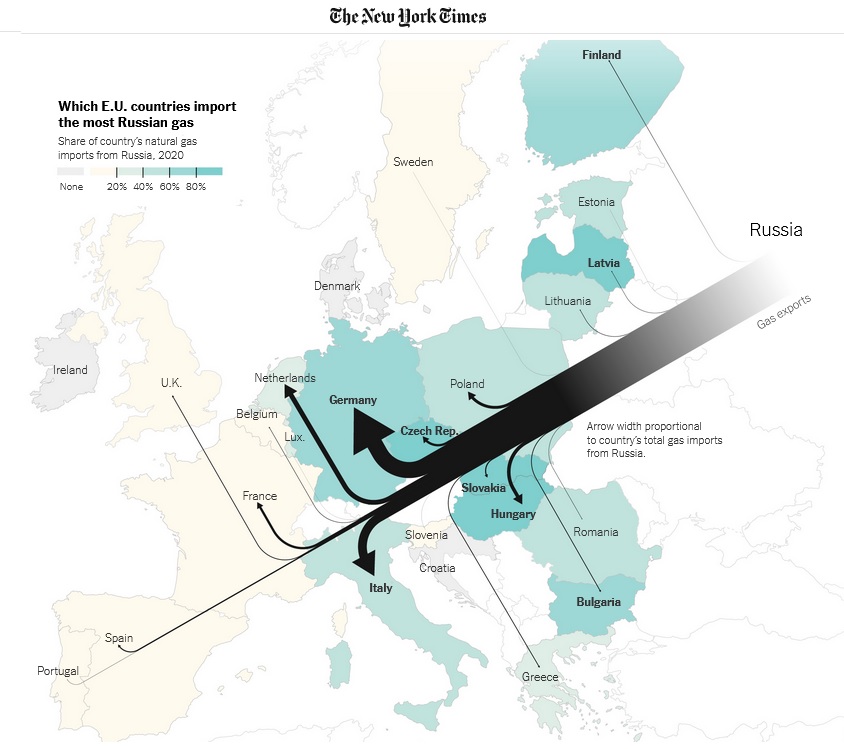

Consider this image, courtesy of the NY Times:

That’s right: Germany — a country with the 4th largest GDP in the world — imports almost 60% of their natural gas from Russia. The Czech Republic, Latvia, Slovakia and Hungry import more than 80% of their natural gas from Russia. At the current time, due to infrastructure reasons, they have almost no other options. They must buy Russian natural gas. At almost any price.

Who owns Gazprom? Russia, primarily.

I could be wrong. Maybe Russia’s primary inspiration is not economic. This could be a legitimate border security issue for Russia. It’s possible. Belarus and Ukraine are all that stand between Russia and a very large NATO block. So, perhaps, this is a legitimate concern for Russia, too. But I don’t think it’s their primary concern. They saw an opportunity to make a whole bunch of money. So they did.

Speaking of making a whole bunch of money … how are the opulent eateries doing this week? Let’s take a peek:

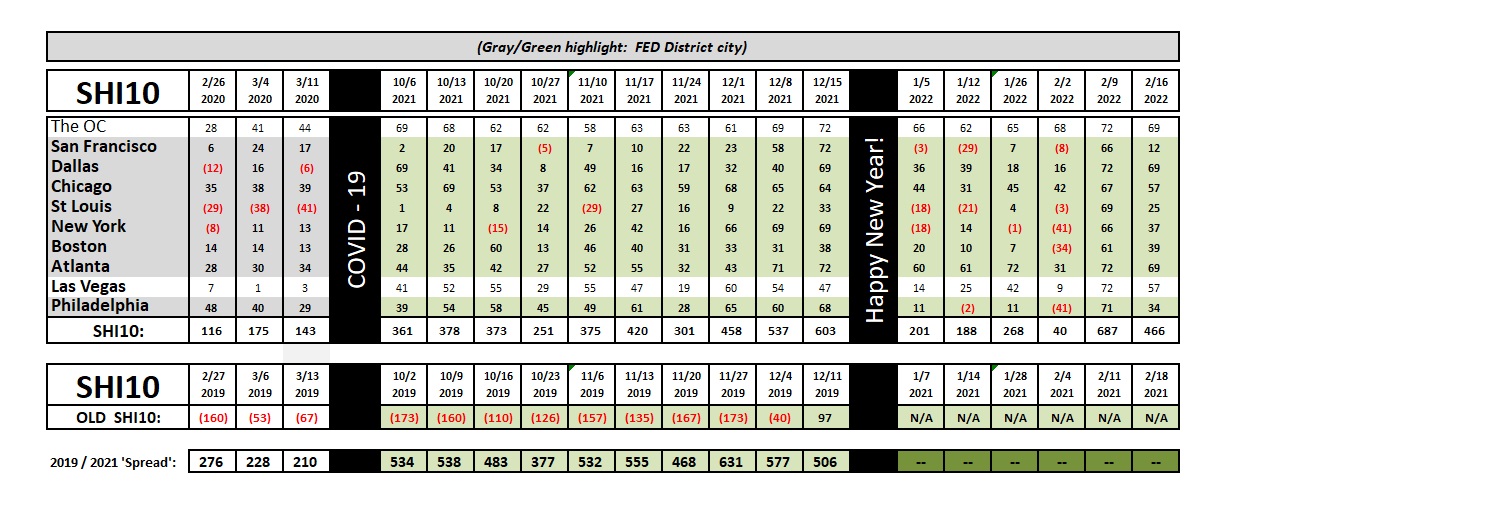

Good news for our expensive steak houses! Reservation demand for this Saturday remains strong … hordes of steak lovers plan to invade shortly! Last week, of course, demand was exceptionally strong — again, I suspect it was a Valentine’s Day phenomenon. But this weekend, demand in most of the 10 SHI cities remains quite strong. San Francisco reflects the weakest demand … and the OC, Dallas and Atlanta are all tied for the greatest reservation demand. Assuming the SHI10 is predictive of US economic strength, the economy is looking good this week!

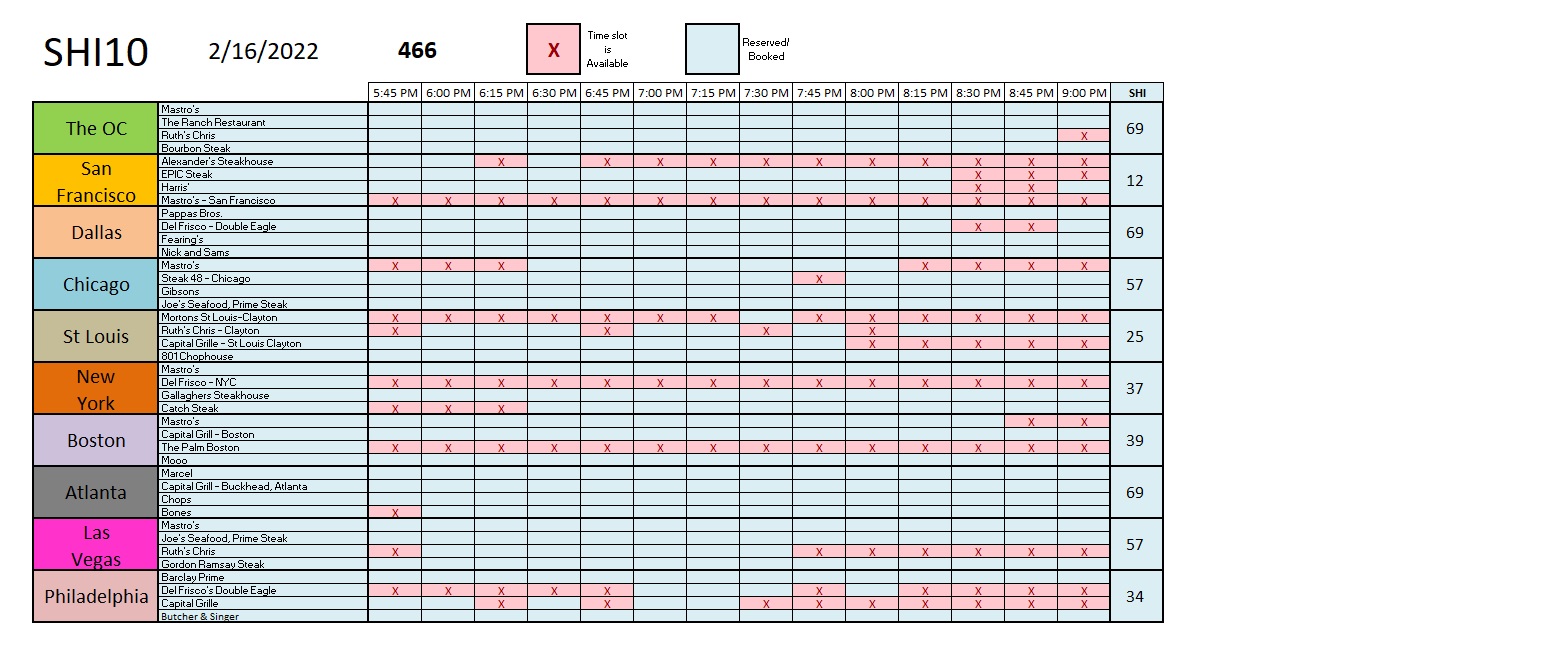

Here’s the weekly SHI40 survey:

It’s interesting to note there are only 1 or 2 reservation slots remaining open this Saturday in the OC, Dallas and Atlanta. Well heeled consumers are feeling flush.

Earlier I mentioned the FED. While we’ve seen little action from the FED, we’ve heard a lot of talk. Yields are up. Stock and bond markets are down. When the FED speaks, markets listen. The 10-year Treasury is 0.5% (or more) higher. Without changing a thing — the FED funds interest rate and the FEDs balance sheet are unchanged — words alone have lifted the 10-year Treasury rate by 50 basis points or more. Impressive.

The next FED meeting is mid-March. Will they raise short term rates? Almost assuredly. How much? That’s the question of the day … but I suspect the number is 25 basis points. Why not 50? Well, while they want to tame inflation, they don’t want to choke off and crush the economy. With the yield curve, for the most part, already up over 50 basis points with just jawboning, they should decide to make a small move mid-March, see how the markets and inflation react, and then make adjustments as needed.

Again, my opinion. But last time I checked, the FED has yet to ask for my opinion. Perhaps they’ll call me soon. 🙂

<:> Terry Liebman