SHI 9.7.22 – First, A Quiz!

SHI 8.31.22 – Supply and Demand for Steaks and Labor

August 31, 2022

SHI 9.14.22 – Closing The Barn Door …

September 14, 2022

That’s right! A quiz! Ready?

Which country leads the world in electric vehicle sales (per capita)?

China? The US? How about Germany? Nope … none are even close to the global leader: Norway.

Sales doubled in 2021, to 6.6 million cars. And in January of 2022, 83.7% of all new cars sold in Norway were EVs. Don’t believe me? Here’s the source data

https://ofv.no/bilsalget/bilsalget-i-januar-2022

OK, true, the site is written in Norwegian. Anyone read Norwegian? No? OK, you’ll just have to trust me.

No? Tough crowd. OK, if that’s just not how you roll, use “google translate” and you’ll see I’m not making this up. ?

“

By 2025, Norway plans to only permit EV sales.”

“By 2025, Norway plans to only permit EV sales.”

That’s right: Norway has set a target to completely phase out the sale of internal combustion engine cars by 2025 – a fascinating fact for many reasons, least of which is that Norway is ranked 13th in the world in oil production. Clearly, they won’t be using much that oil in Norway. Germany must be pleased.

By now, you’re probably wondering what this has to do with economics, finance or the sale of high-priced cuts of meat at our steak houses. Absolutely nothing. I simply found the data to be extremely surprising…so I decided to share! ?

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Sort of. At the end of Q2, 2022, in ‘current-dollar’ terms, US annual economic output rose to $24.85 trillion. Yes, during Q1, the current-dollar GDP increased at the annualized rate of 7.8%. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the 3 big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

What goes up, can also go down.

I’m quoting myself from last week’s blog. Inflation is up. Way up. Here in the US. In Europe … the UK … and even in Japan.

I believe it’s already heading down here in the US. Quite a bit actually. But will the inflation rates around the world eventually fall below 2% again, as the FED expects as early as 2024? I have my doubts. Why? I believe inflation is sticky this time. Not super sticky, mind you. But stickier than it’s been in the past 20 or 30 years. Why? What’s changed?

De-globalization. To quote a recent a recent Economist magazine article, “… there are slow-burning changes to the structure of the global economy.” Absolutely. Quoting further from that article:

“Both emerging and advanced economies engaged in a wave of liberalizing reform from the mid-1980s to the mid-2000s. Tariffs fell, while labor and product markets grew more limber. These reforms contributed to a surge in global trade, large-scale shifts in global production and falling costs across a range of industries. Reform may have bolstered productivity growth, too, which ticked up in advanced economies at the turn of the millennium and in emerging economies in the 2000s.”

For decades, central bankers around the world seem to now be realizing, globalization acted as a “gigantic shock absorber” – quoting Isabel Schnabel from the ECB – where shifts in demand were easily met by a distributed network of global manufacturers. But this chapter is now closed. Nailed shut by the pandemic.

Then completely encased in concrete and tossed into Lake Baikal after the Russian invasion of Ukraine.

For the first time in decades, the pandemic and unpredictable despots have convinced us all that the world is a dangerous place. Gone are the halcyonic economic days of 1980 to 2020. Gone forever. Today, in this dangerous new world, countries are making the choice to “on-shore” mission-critical industries and manufacturing. New international alliances are forming, adding to the “us vs. them” mentality.

Don’t get me wrong: Globalization is not dead. Far from it. No, it’s simply the long-term trend that is changing direction. A highly integrated world was built over the past 4 decades. It is now slowly decoupling … and this trend will likely continue for decades into the future. This change translates to stickier inflation. “Stuff” will cost more than it did before 2020 simply because the input costs and manufacturing expense are both likely to increase over time. Add to this challenge the post-pandemic labor issues and slowing population growth in the developed world, we have a world where stuff will cost more in the future. Which means inflation will likely be stickier in future years.

How much stickier, of course, is hard to predict. But this does suggest that the FED and other central banks face a real headwind as they attempt to reach their 2% inflation goal.

How does this condition impact my belief that long-term interest rates are heading lower? After all, isn’t the current inflation rate a structural component of interest rates? Sure, that’s what economic theory tells us. Theory suggests that the safest “real” rate of interest is always some combination of the current inflation rate plus some minimal return investors expect. And riskier rates of interest include a “risk factor” of some amount. But in a world awash with capital, this relationship doesn’t appear to hold. The past two decades have made this clear. So has trillions of dollars of “negative” sovereign debt.

No, I’m afraid that theory no longer holds. Longer-term interest rates are no longer set by, or highly correlated with, the current inflation rate. Long-term rates are heading lower. Not now, of course, but soon.

To the steakhouses!

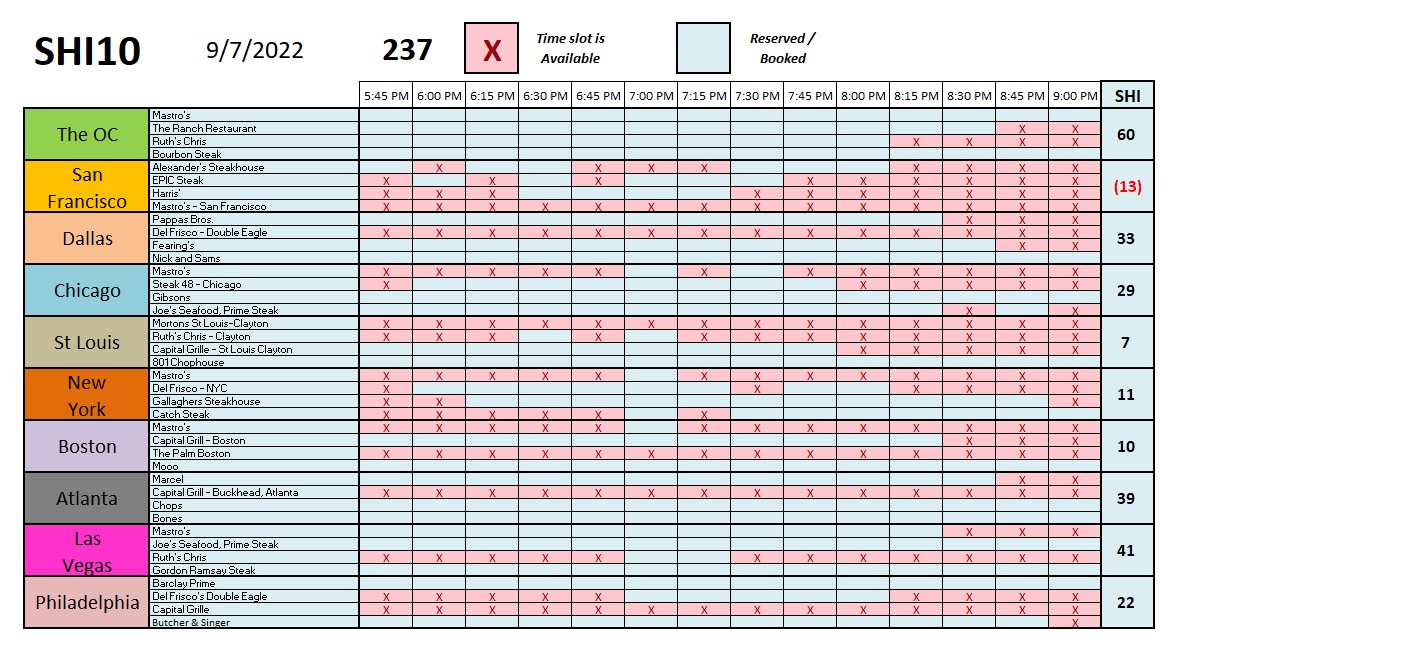

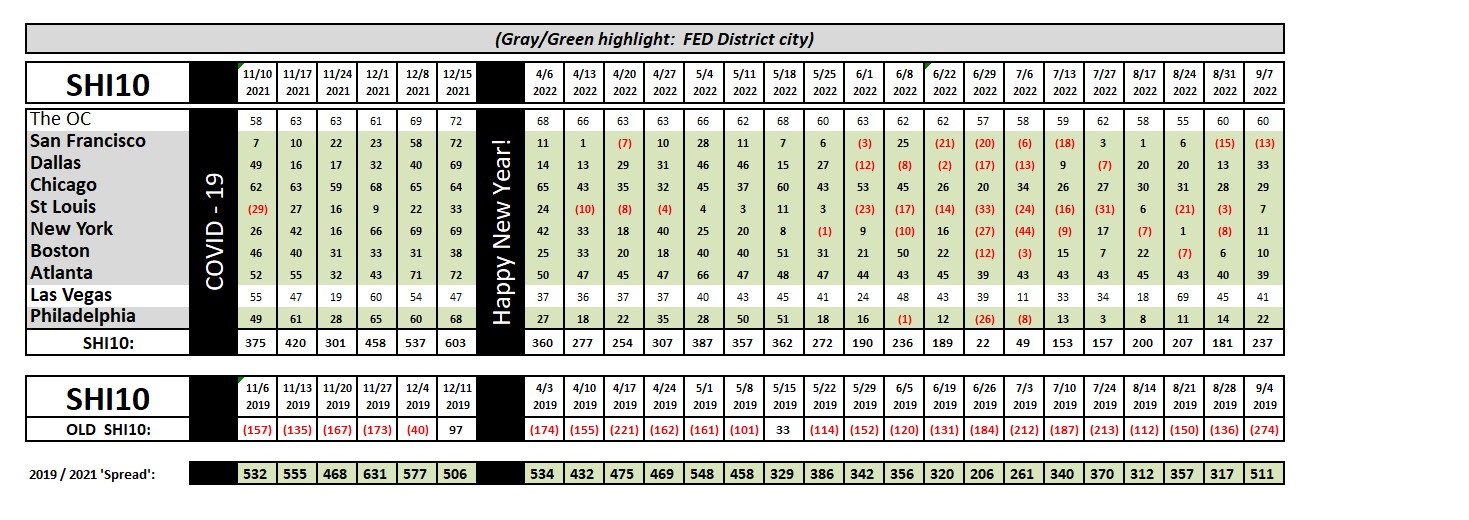

A small improvement in this week’s demand level for expensive steakhouse reservations on Saturday. This week’s SHI10 is up slightly to 237 from last week’s relatively consistent read of 181. Demand remains very consistent in the OC; we’re seeing a slight up-tick in the other markets; and, a large demand jump in Dallas. Overall, however, I seen nothing this week to indicate any meaningful directional change. Here’s the longer term trend chart:

It’s worth noting that this week’s “spread” is significantly higher than any week going back to 4/6. However, all in all, I’d say we’re in a very steady demand period. It’s also worth noting that the FED released the Beige Book earlier today. Essentially, they agree with my assessment:

“Economic activity was unchanged, on balance, since early July, with five Districts reporting slight to modest growth in activity and five others reporting slight to modest softening.”

Steady as she goes.

<:> Terry Liebma