SHI Update 6/21/17: Slowdown

SHI Update 6/14/17: Point to the Future!

June 14, 2017SHI Update 6/28/17: Inflation? Where?

June 28, 2017

What do US auto sales, oil prices and Japan’s GDP all have in common?

Welcome to this week’s Steak House Index update.

As always, if you need a refresher on the SHI, or its objective and methodology, I suggest you open and read the original BLOG: https://terryliebman.wordpress.com/2016/03/02/move-over-big-mac-index-here-comes-the-steak-house-index/)

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. Is it expanding or contracting?

The world’s GDP is about $76 trillion. Our US GDP is almost $19 trillion — about 25% of the total. No other country is even close.

The objective of the SHI is simple: To help us predict US GDP movement ahead of official economic releases — important since BEA data is outdated the day they release it.

‘Personal consumption expenditures,’ or PCE, is the single largest component of US GDP. In fact, the majority of all US GDP increases (or declines) usually result from (increases or decreases in) consumer spending. Thus, this is clearly an important metric to track. The Steak House Index focuses right here … right on the “consumer spending” metric.

I intend the SHI is to be predictive, anticipating where the economy is going – not where it’s been. Thereby giving us the ability to take action early. Not when it’s too late.

Taking action: Keep up with this weekly BLOG update.

If the SHI index moves appreciably – either showing massive improvement or significant declines – indicating expanding economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

What do US auto sales, oil prices and Japan’s GDP all have in common?

The answer: They are all accelerating.

Hold on, you’re probably thinking: “Just last week, didn’t Terry tell us the economy is slowing?” Yes, I did. It is.

I’m using the Physics definition of acceleration, not the Merriam-Webster definition. In physics, acceleration is a “vector quantity.” It is defined as “the rate at which an object changes its velocity.” Thus, an object is accelerating if its velocity is changing. Regardless of whether that change is an increase or decrease.

So a change in velocity – both increasing and decreasing – indicates acceleration. This is an important distinction. After last week’s BLOG, a number of people asked me, “Are you suggesting we’re heading into a recession?”

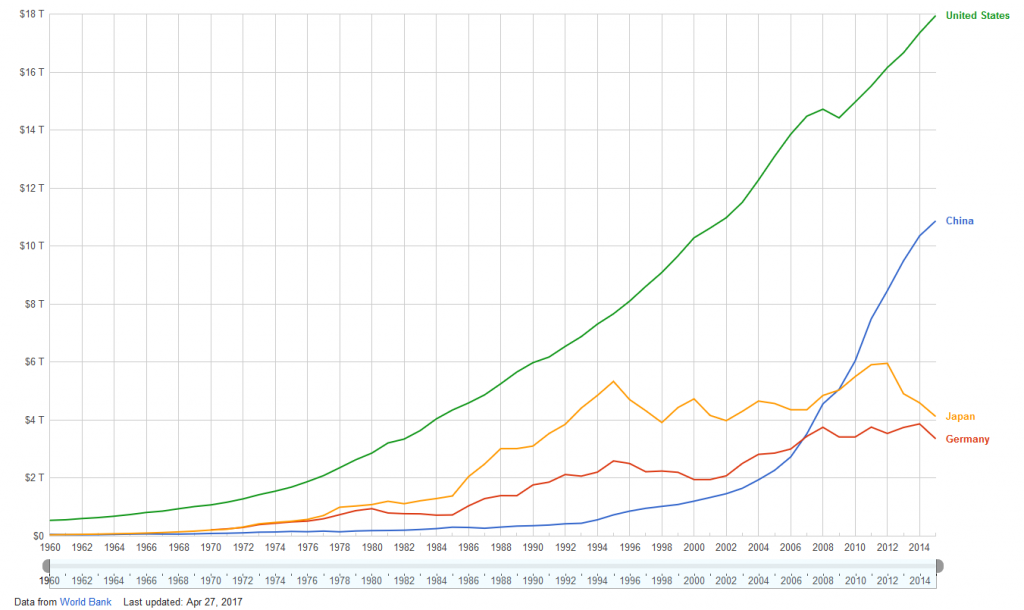

No is the answer. At present, a recession is not in the cards. But the velocity of GDP growth is changing. The velocity is slowing. The chart below, courtesy of the World Bank, helps illustrate the point:

While US and China GDPs have continued their upward trends, Japan has not. In fact, today’s GDP is almost back down to 2002 levels. US GDP, by comparison (in nominal terms) is up about 64% from 2002.

But here’s the interesting point: In spite of Japan’s tepid performance as a country, on a per-capita basis, their GDP has grown almost as much as the US per-capital GDP! Said another way, Japan’s aggregate economic results are poor NOT because of a feeble economy, but because of demographic factors: According to UN studies, in the 10 years since 2005 Japan’s “prime age” work force (folks between 15 and 64 years of age) has declined from 66% to 61% of their total population.

Sound familiar? Yep, the US is beginning to experience the exact same trajectory in our “civilian labor force.” Our civilian labor force (the CLF) — folks between the ages of 16 and 64 — may be starting to shrink. Here’s a chart for the prior year:

It’s been declining since peaking around 160 million in April. The CLF has declined before, so, in itself, the decline is not overly concerning. What IS somewhat concerning is this: the CLF — today — is slightly lower than the CLF in September of last year — 8 months ago. Our civilian labor force is showing signs of peaking. If our CLF continues shrinking, just as we’re seeing in Japan, our aggregate GDP growth will likely continue to accelerate – but at a lower velocity. 🙂

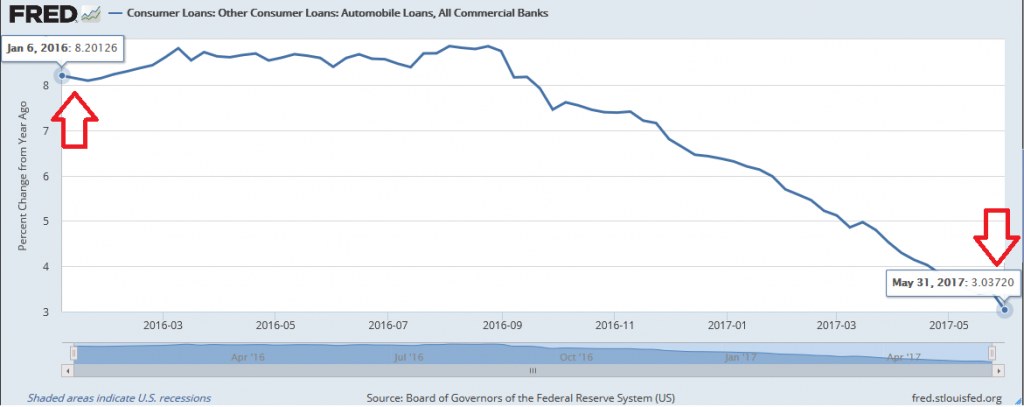

Another economic metric showing signs of fatigue are auto sales.

Auto sales (“light weight vehicle sales”) peaked at the end of 2016 at an annual sales rate of 18.32 million units per year. Also in December of 2016, Edmunds reported the ‘average’ new-auto sale price increased by 2.7% to a bit over $34,000.

In May, the annualized new car sales rate fell to 16.58 million – an almost 10% decline from just 6 months earlier. Is this important?

Yes. Auto sales are a huge part of the US economy and our GDP. Multiply the average price by the peak annual sales number and we get over $620 billion in annual sales. Suggesting auto sales, alone, represent about 3.3% of the TOTAL annual United States GDP.

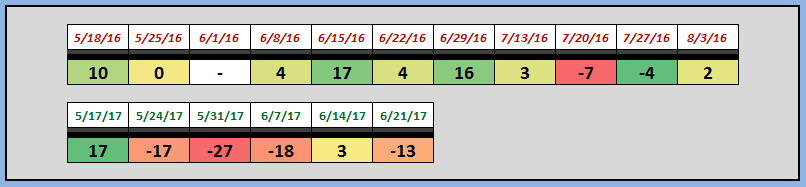

And now the question we’ve been waiting for: Are we seeing the same acceleration trend in the SHI?

Yes. The SHI, again this week, is showing continued weakness. Here is an abbreviated trend chart:

Copying the words of my associates on CNBC, I’m officially declaring the SHI to be in a bear market. The signs are clear: For five consecutive weeks, the 2017 SHI readings minus the 2016 SHI reading — for the same week in each year — has been between 14 and 27 points weaker. Here is this week’s chart:

This week, last year, only The Capital Grille was available at 7 pm. Today, with the exception of Mastros, this Saturday your party of 4 can dine at any restaurant at 7 pm. And just about any other time slot as well.

Demand for reservations at our high-priced eateries is clearly slowing. Demand for new autos, too, is clearly slowing. Both are strong indications of consumer consumption activity. One is more tangible, the other more ‘experiential,’ but both manifest the willingness (or ability) of consumers to spend their hard earned dollars.

What’s causing this slowdown? The FED interest rate increases? Fatigue? Insufficient general wage growth?

In the final analysis, the cause really isn’t overly important. What is important is how this trend impacts each of us, and the personal financial decisions we must make. But remember: this is only a velocity change. A slowing growth velocity. I don’t believe we’re seeing the signs of an economic contraction. Just an expansion that’s getting a bit long in the tooth.

- Terry Liebman

{kind=link}

2 Comments

Dear Terry,

I want to preface this comment by saying that I do not want to portray the Dunning-Kruger effect in my comments. I have low competence in economics compared to many others out there. That being said, I want to ask your thoughts on the auto industry as a whole and by each company individually.

I recently bought a new car and spent a large amount of time researching, examining, and driving cars. When it came down to it I bought a Honda Accord V6. In buying the car, I haggled down and down to make sure I received the best deal IN MY MIND. I had to finance the car and I locked in at X.XX% APR. With the recent rate hikes, did I buy at the most opportune time? Depending on that answer, I feel that (if yes) I made a great purchase for myself, but did I counteract the FEDs decision to raise rates? Even just a little? My thoughts are that if everyone was keen and bought cars prior to the rate hike, we would live in a sinusoidal wave of car buying.

This is very theoretical, and if it is full of bologna please disregard.

Sincerely,

The Steak House Disciple

Hello Disciple! Thanks, as always, for your continued interest and questions.

Needless to say, while many feel they can accurately forecast the next FED rate hike, the opposite is more often true. The FED meets 8 times each year. In the more recent past, they’ve demonstrated a reluctance to raise rates subsequent to most of those meetings; unlike years prior when rate increases could occur intra-meeting. So, no, I don’t think auto purchase decisions are in any large part correlated with FED rate increase timing.

Individuals make decisions which, when studied in the aggregate, tend to help analysts understand market conditions. And those analysts help manufacturers understand macro market conditions.

You or I may decide to buy a car – either because we need one, want one, but not typically because it’s a good deal. Auto manufacturers know this: Need and want are motivators, but a good deal may push fence-sitters or near-term buyers into buying decision today. Effectively pulling future demand into a sale today.

The next effect, however, is to deplete buyer interest in the coming months or year. Which, ultimately, may further exacerbate declining auto/truck sales figures and adversely impacting GDP when that occurs.

All this said, when auto/truck manufacturers (sellers) become a bit skittish, it is an excellent time for you (buyers) to negotiate a great deal. FED rate decisions notwithstanding, I think your timing is excellent.

– Terry