4.21.21 – Economy? Sizzling !!! Steaks? Nope.

SHI 4.14.21 – The Steakhouse is BACK!

April 14, 2021

SHI 4.28.21 – The Population Bomb

April 28, 2021

Last week, FED Governor Chris Waller told CNBC, “… the economy is ready to rip!“

I agree. The US economy will be blasting off soon, if it hasn’t already left the launch pad. But steaks? This week, they are still in the freezer. Frozen solid. The heat is pegged at ‘high’ for US business, but for some odd reason, this week the steakhouses are fairly empty. What gives?

“

Book a reservation. Mastros needs you. “

“Book a reservation. Mastros needs you. “

Last week, the SHI10 index reading was a positive 387 — an ultra-high reading when the maximum index value of 720 means that every single reservation time slot for the upcoming Saturday in all 40 of our SHI expensive eateries is booked. This week, conditions at the steak houses are very different: The index is a luke-warm negative <31>. Not great. Sure, the cows are celebrating (sorry Vegans) their stay of execution, but steak house operators are not.

If the economy is cooking, why aren’t steaks sizzling too?

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Before COVID-19, the world’s annual GDP was collectively about $85 trillion. Then it shrank … then bounced back! We can thank global fiscal and monetary policy for the bounce. According the the Q3, 2020 ‘preliminary’ numbers, annual US GDP is back UP to about $21.1 trillion. And still, together, the U.S., the EU and China continue to generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

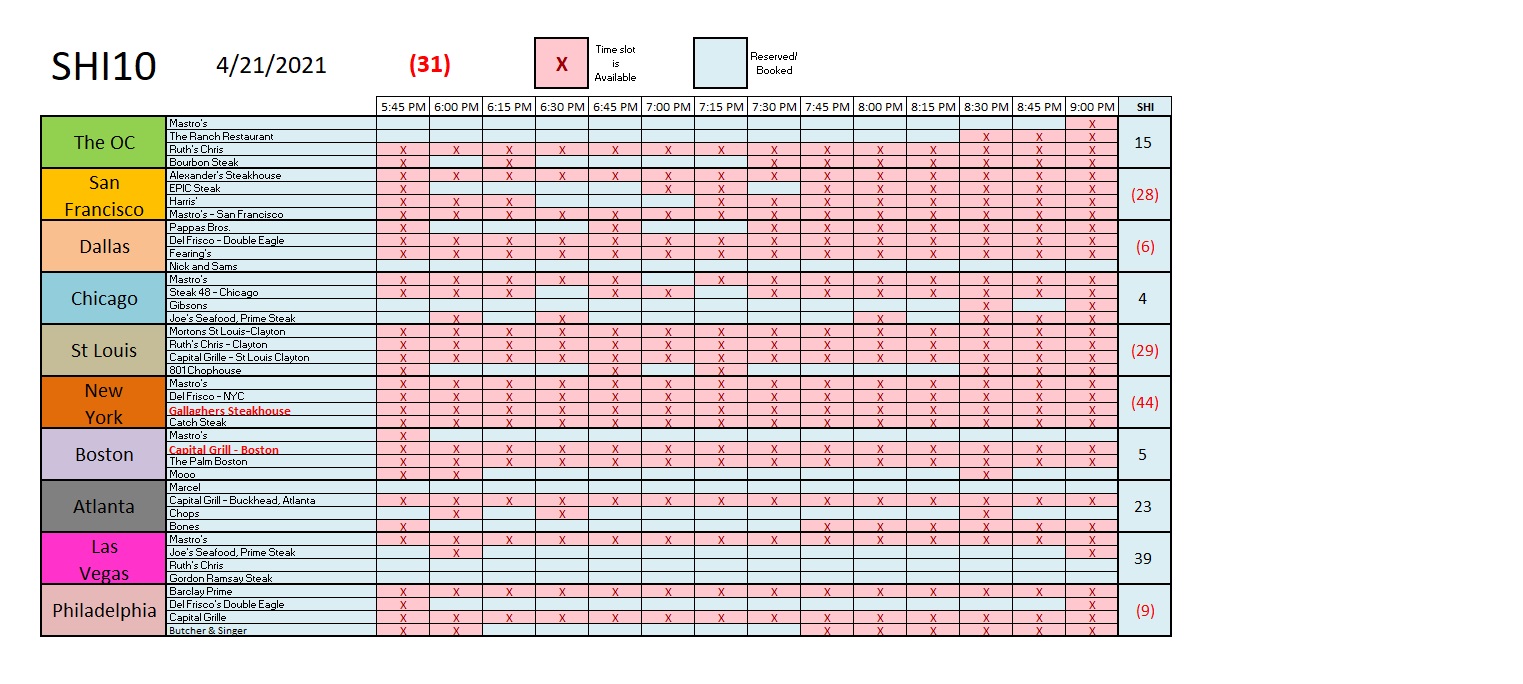

Let’s jump right in. Here is this week’s SHI chart:

That’s a whole lotta red. This chart is very much unlike last week when we saw an ocean of blue, reflecting the huge number of fully booked restaurants. Of course, different “open” levels most certainly impacted reservation availability. And probably still do this week.

Regardless, the steak house business is fairly brisk here in the OC, and most other markets across the US are mixed. But not ‘Vegas! Las Vegas is clearly back and booming. You can still score a table at Mastros, but pickings are slim elsewhere. Remember: This is before any conventions have returned to the city.

Reservations at New York’s pricey pubs are wide open. Perhaps because the city’s theaters, many office buildings, and business travel remain closed or muted. It will be interesting to see how the city opens up in the coming months vis-a-vis expensive steakhouse reservations. The weak SHI reading for San Francisco is a bit surprising. But I’ve heard anecdotal comments that folks in the ‘Bay Area’ remain very Covid-cautious.

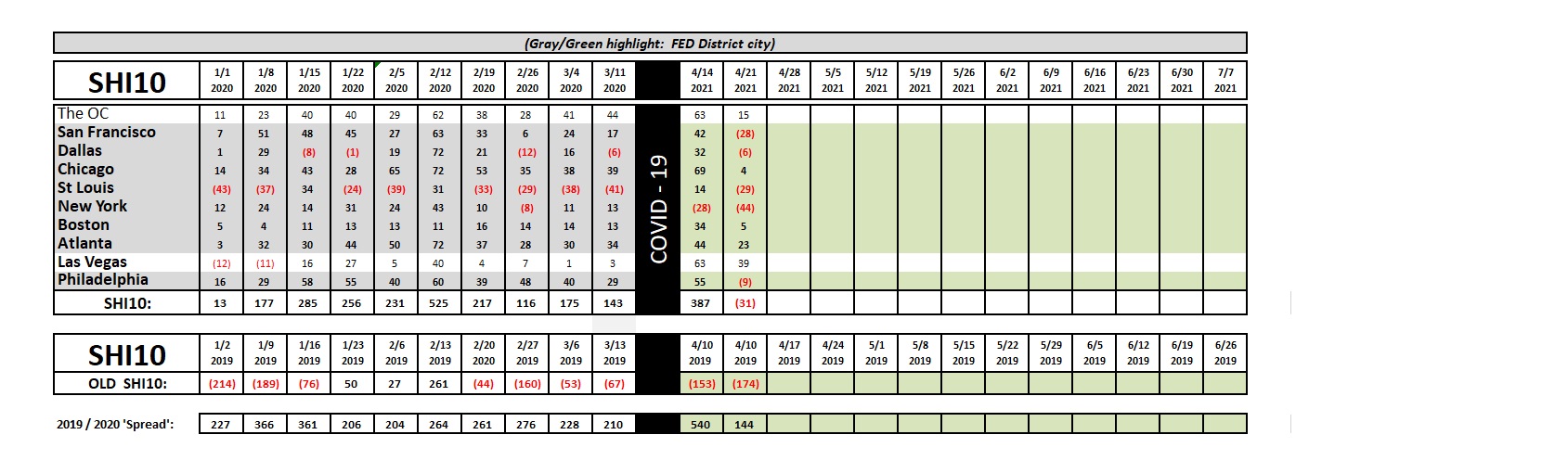

Here is the longer-term trend report:

It’s worth noting that from a historical perspective, an SHI10 reading of negative <31> isn’t horrible. At least when compared to the 2019 pre-Covid readings we see above. But it is a weak index reading when compared to those from early in 2020.

The challenge we face, of course, is assessing relevance. Vaccines are now available to any adult, in all 50 states, and per the CDC as of today over 87 million Americans have been fully vaccinated — over 26% of the population. It’s important to also note that 40.5% of all Americans have had at least one vaccine shot. Fabulous. As vaccinations pick up pace, I expect the US economy to fully thaw and sizzle.

At the turn of the 2021, US business activity was a lot like the steak photo at the top of this page. No longer. Retail sales spiked by almost 10% in March — clearly “stimulated” by the most recent federal stimulus, where $410 billion of the $1.9 trillion was paid directly to US consumers. It’s worth noting the huge jump in consumer spending took place even though quite a bit of those stimulus payments were either saved or used to pay down debt. Impressive.

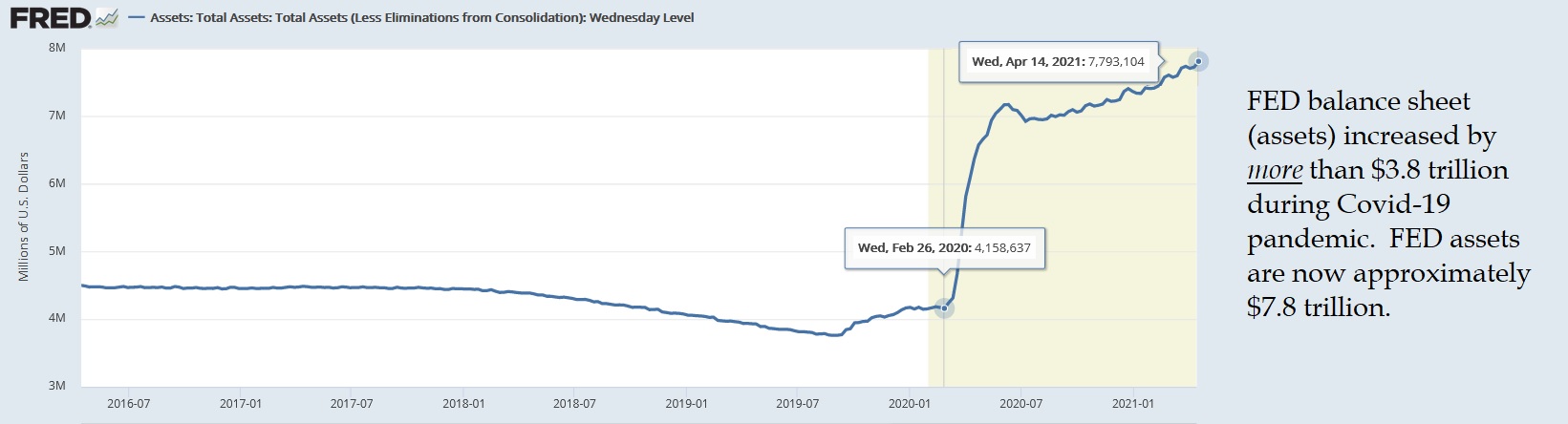

The FED, to their credit, is sticking to their guns. Every month, they continue to purchase at least $120 billion of Treasury or MBS securities, the addition of which continues to bloat their balance sheet:

I actually believe they will increase their purchases in coming months. Treasury bond supplies are growing like mushrooms in a dark, dank room. Thru March of this year, the US Treasury has ‘Total Receipts’ of $1.704 trillion and has spent a total of $3.410 trillion — resulting in a YTD deficit of over $1.7 trillion. And only 1/2 of fiscal 2021 is behind us. Ugh.

In the FEDs quest to reach “full employment,” and grow the economy, all while keeping long-term interest rates relatively static, I feel they’ll have to step-up the amount of their purchases. There is simply too much red ink, too many bonds, for them to stand pat. We’ll see, but I wouldn’t be surprised to see the FEDs balance sheet eclipse $8 trillion by mid-June and accelerate from there. Expect $300 billion per month in FED bone purchases at least during the summer. 🙂

Can the US “grow its way out” of this massive deficit hole? A great question. Assuming our ‘real’ GDP expands by more than 8% this year, and nominal GDP growth eclipses 10%, and further assuming federal tax collection rates rise back to their (almost) historical level of 20% of GDP, then a 10% GDP increase in 2021 could yield an annual $200 billion bounty for the Treasury. Over 10-years, a commonly used measuring metric when talking US budgets, this equals $2 trillion. Assuming we add another 5% nominal growth in 2022, this will add another $1 trillion to federal collections in the coming decade. Combined, that could become a $3 trillion “debt reduction chunk.”

Of course, the biggest wildcard remains interest rates. The US owes close to $27 trillion today. Were rates to rise by, say, 1% in the next year, then our interest carry cost would increase by $270 billion per year. A 2% lift would add over $500 billion to the annual interest tab. No, rates must stay low. I remain confident the FED agrees.

Steaks may be frozen solid, but our economy is defrosting. Pretty soon, we’ll be partying in the streets! Literally: That is, of course, assuming the powers-that-be allow all those temporary tents, tables and chairs to remain in the streets. 🙂

- Terry Liebman