SHI 9.14.22 – Closing The Barn Door …

SHI 9.7.22 – First, A Quiz!

September 7, 2022

SHI 9.21.22 — Tough Love, Baby

September 21, 2022

… after the horses have already left does no good. The horses are gone. May as well leave the doors open in the first place.

The problem is even worse, of course, if the barn in question has only 3 walls. If one is completely missing, the barn door on the opposite wall has absolutely no value at all. Open or closed, anything in the barn can simply wall out thru the missing wall. Standing outside however, facing the barn wall with the door, it appears the door — if closed — would effectively keep horses in the barn. Because you don’t know the back wall of the barn is missing.

“

Don’t worry about the door if a wall is missing.”

“Don’t worry about the door if a wall is missing.”

By now, you’re probably wondering what barns, doors and missing walls has to do with today’s blog or economics on the whole. Stay tuned.

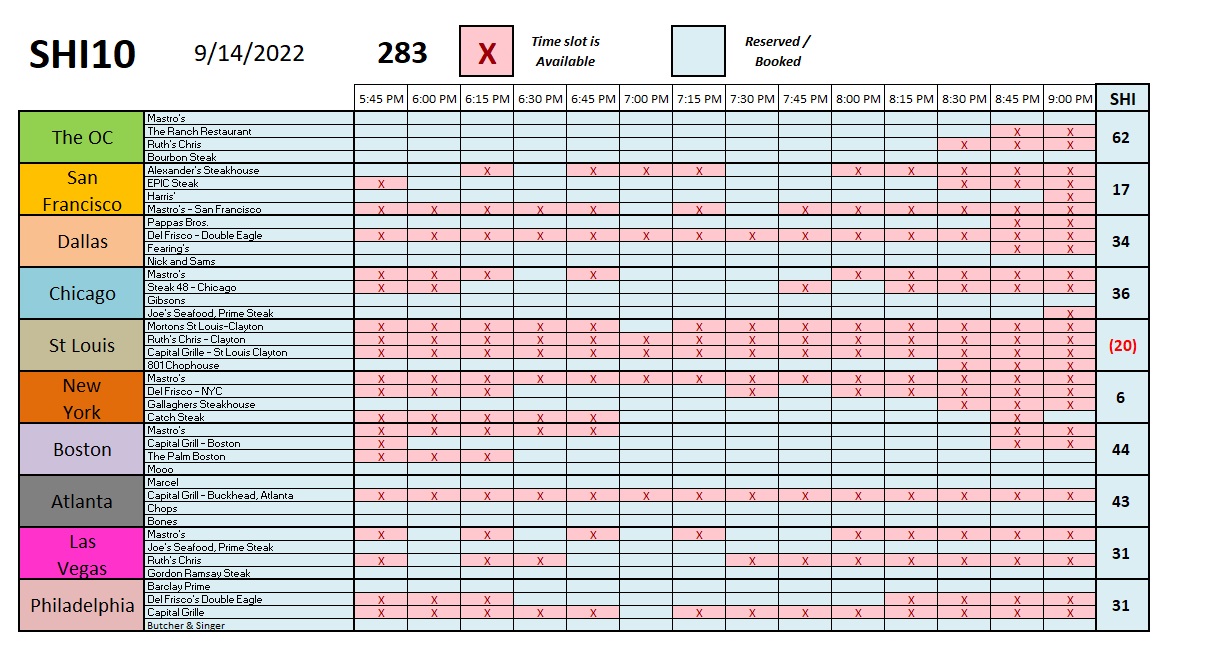

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Sort of. At the end of Q2, 2022, in ‘current-dollar’ terms, US annual economic output rose to $24.85 trillion. Yes, during Q1, the current-dollar GDP increased at the annualized rate of 7.8%. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the 3 big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

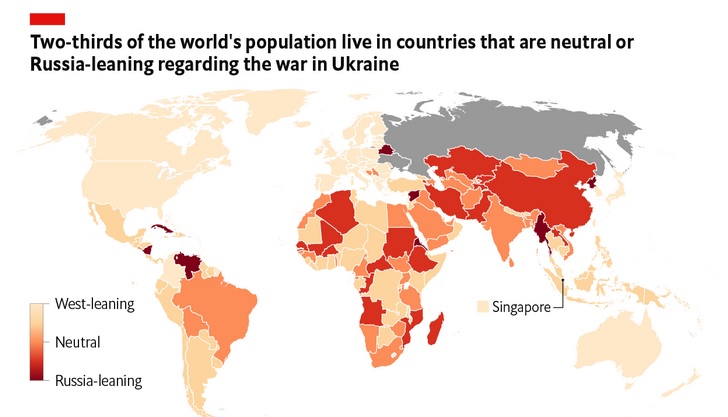

About 6 months ago, Russia invaded Ukraine. Russia and Putin were quickly condemned by the United States and the rest of the “Western World.” On March 2nd, 141 countries voted in favor of a UN resolution “deploring” Russia’s invasion of Ukraine. (For context, it’s worth noting there are about 190 countries total.) The US and Europe quickly decided Russia and Putin had to be sanctioned for their boorish behavior and choices. Here in America, we were told that these sanctions would crush the Russian economy, bring Putin to his knees, and potentially quickly end the skirmish. The US, Europe, Canada and Australia got together, built that proverbial “barn,” and together they pushed Russia inside. The sanctions, they assured us, would work.

But there was only one problem — a problem we didn’t hear about at the time, but know all-to-well today. They left off a wall. They built a 3-sided barn and Russia easily exited, avoiding many of the effects of the sanctions. Consider this image:

As we fast forward to today, we now know that 2/3 of the worlds population either (1) doesn’t care about the Russian invasion (they are neutral), or (2) they don’t object to the invasion or even side with Russia on it. Only 1/3 of the world’s population condemns Russia or Putin.

Heck, it looks to me like the barn has only 2 walls at best.

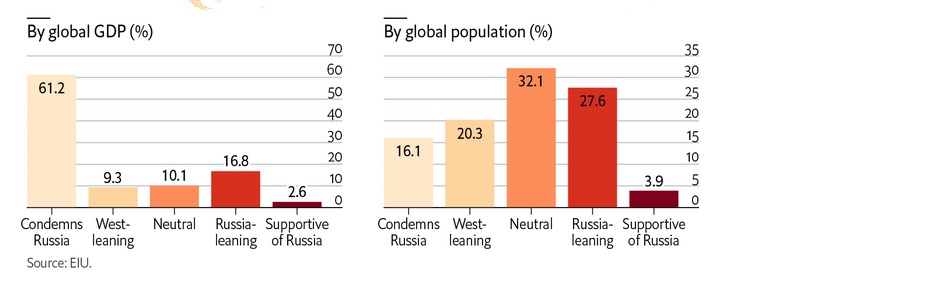

When viewed thru the GDP lens, the sanction numbers improve but not decisively:

It appears that while only 1/3 of global populations either condemn Russia or “lean” toward western opinions, those populations make up more than 61% of global GDP. So that packs a bit more punch.

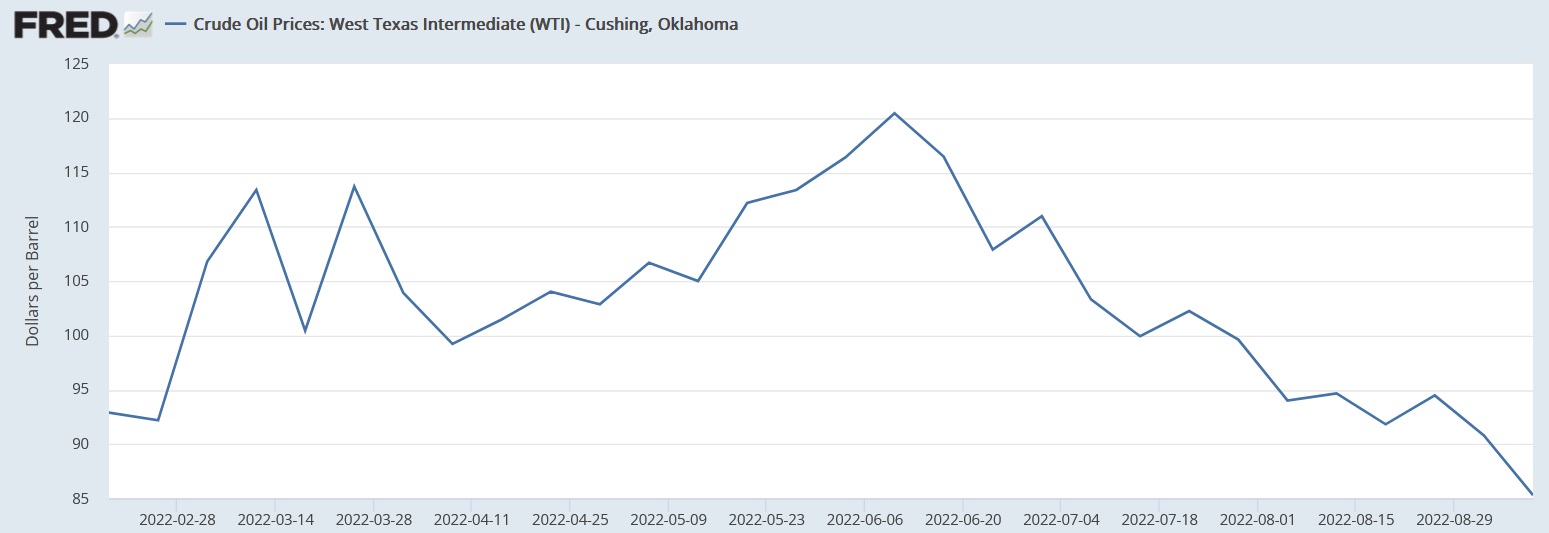

But not enough, unfortunately to make much of a difference in Russia or to their $1.8 trillion economy. Oh, the sanctions certainly generated a whole lot of negative results here in the west — massive additional supply chain disruptions and an inflationary spurt in commodities and other raw materials — and many have now reverted to pre-invasion levels. For example, consider the PPB of oil. Here’s a price chart of WTI from the week before the invasion thru today:

On February 18th, the PPB was about $93. It peaked on June 10th at just over $120. Today, the price is about $85. The round-trip is complete. The same has happened with agricultural commodity prices … and many other things. Why? Have the sanctions and “blockades” been completely unsuccessful?

Yep, they pretty much failed. Sure, about half of Russia’s $580 billion of current reserves are “frozen” within the US-controlled banking system. The US no longer buys Russian oil … and Russia’s firms cannot buy materials or supplies from the Western world. And you can no longer buy a BigMac in Russia … now you’ll have to be content with the new- and improved-alternative … the ‘BigPutin’. It looks like the BigMac, but the taste is a bit off … a bit gamey and chewy I hear. Folks from the West tend to cringe and turn pale on the first bite. But the burger is very popular in Moscow!

The problem, in the final analysis, it the fact that full- or partial-embargos are not being enforced by more than 100 countries with about 40% of global GDP. Which means that Russia is having little problems today selling their oil and importing other “stuff” they need. On second thought, this barn seems to have only one wall — the front wall where the door is.

And that’s where we find ourselves today. The sanctions were ineffective, Russia is doing OK … but here in the US we’re contending with pandemic and sanction-inspired inflation pressures, and in Europe, in retaliation an angry Putin has decided to weaponize the Nordstream pipeline, causing grave harm to western-European industries and citizens. Folks, its a mess.

My point? Don’t build a 1- or 2-sided barn and expect to keep your horses inside. It doesn’t work. It’s probably time to bulldoze these sanctions and try to find something else that works better. Coca-Cola and McDonalds left Russia. But their brands remained behind. Anyone fancy a ‘Cok?’

Welcome to Russia, comrade. Where Cok and BigPutins are all the rage. 🙂

One wonders with all the Cyrillic ‘Cok’ available and the bellicose ‘BigPutin’ burgers a-grillin, if our poor little steakhouses will have even one reservation this week? Should we pity those poor folks at Mastros and Bourbon Steak here in the OC. How will they possibly fill their tables, given all competition, price inflation, and the heavy-handed FED?

Apparently there is no pity needed. In fact, I can tell you from personal experience, the expensive eateries here in the OC are doing quite well, thank you very much. For purely market-research purposes, this past Saturday, I reserved a table for 4 at the local Bourbon Steak House in the Waldorf Astoria in Monarch Beach. Reservations at 7 pm, please.

The place was packed. Filled to the rafters. Unfortunately, the couple check-in just before us did not have reservations. Nor did they get a table. Packed. Nothing available. Again, for purely market research, we went to the hotel bar first. Where the research began. While seated at the bar, I was again surprised by how busy they were. They were packed as well. Four drinks, 20 minutes, and $112 later, I commented, “I wonder how expensive a room is here tonight?” The answer: The cheapest room at the Waldorf Astoria, Monarch Beach, this past Saturday was about $1,100. Ocean view: About 2 grand.

You may have guessed where this is going, but I’ll take the circuitous route. Dinner was awesome. What a fantastic restaurant! As I’m a “wine guy” and I know what I like, I brought my own bottle of red and one white. Corkage: $55 per. Hmmm…but when compared to their wine list prices, only $110 in corkage was a smokin’-hot deal. A $300 bottle of wine is very typical on their list.

The cheapest steak on the menu was a “4 oz filet” tipping the financial scales at $70. That’s right: 4 ozs. I opted for the 10 oz NY strip for the paltry sum of $98. When the dust settled, the dinner bill was over $740. Remember: I brought my own wine! 🙂

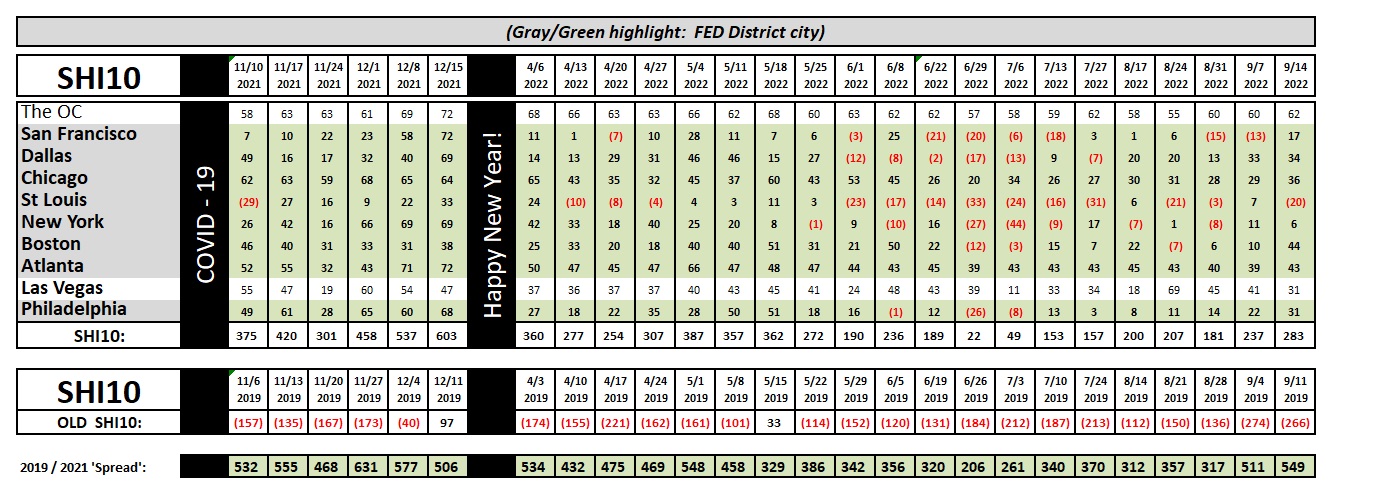

Here’s the longer-term trend report:

Bottom line: By the image above, and my personal experience, I feel pretty confident the opulent steak houses are generally doing quite well. And prices are up, up UP! So far, at least, the well-heeled patrons of the SHI40 seem to be holding up just fine. Life is good, steaks are sizzling on the grill, and the economy is cooking!

Get out there and do some SHI market research yourself. It’s fun! Paying the bill, of course, not so much. But dinner was awesome!

<:> Terry Liebman