SHI 9.21.22 — Tough Love, Baby

SHI 9.14.22 – Closing The Barn Door …

September 14, 2022

SHI 9.28.22 — Rhymes With Dread

September 28, 2022

… A few months ago, I wrote a blog entitled, “Beatings Will Stop When Morale Improves.”

Here’s a link to that piece: https://steakhouseindex.com/shi-7-13-22-beatings-will-stop-when-morale-improves/

Apparently, “morale” has not yet improved. 🙂

Earlier today, the FED acknowledged this fact and continued to dole out punishment to Americans and American business. They raised the federal funds rate — the shortest-term interest rate — by .75%. When today began, the fed funds rate was 2.5%. Now, it weighs in at 3.25%. When today began, the WSJ ‘Prime Rate’ was 5.5%. Tomorrow it will likely be 6.25%. Ouch. And don’t ask about 30-year mortgage rates. If you have to ask … you can’t afford one. 🙂

“

We’re doing this for your own good.”

“We’re doing this for your own good.”

That’s the FED‘s belief. ‘We DON’T want to punish you! But we must … and it’s for your own good’ they seem to be saying with today’s rate increase and forecast. They want to make “stuff” more expensive for you to buy. They want to make homes more expensive to buy. They want you to slow your purchase decision, in the aggregate. And they want to stunt corporate America’s ability to keep raising prices. They want to cause short-term pain for our collective long-term benefit.

Will this work?

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Sort of. At the end of Q2, 2022, in ‘current-dollar’ terms, US annual economic output rose to $24.85 trillion. Yes, during Q1, the current-dollar GDP increased at the annualized rate of 7.8%. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the 3 big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

David Kelly, a financial expert from JP Morgan was talking on CNBC just after the FED announced their rate increase decision around 11 am. His comment: Our economy now has … “one foot in the grave, and the other on a banana skin.” Funny. But is it accurate?

It’s hard to say … because while the FED is now forecasting a peak in short-term rates at 4.6% by early 2023, I’ll make a forecast of my own: They are wrong. The ‘terminal’ short-term rate will not be 4.6%. They are wrong. It will probably be lower … and it might, conceivably, be higher. But it won’t be 4.6%.

The FED wants to slow the US economy. As you know, it plans to do so by raising short-term interest rates. Eventually, their hope is that you and I adjust our consumer purchases just enough to slow inflation, stop run-away rental and home value increases, bring down the prices of used cars, and prevent US corporations from increasing the price of their goods and services too much. But therein lies the seeds of their own destruction.

What is too much? Is it possible they can engineer interest rates to precisely the right level to reach the perfect balance between a “too-hot” economy and one they’ve tilted into a recession?

They probably can’t. It’s an almost impossible task. Because, as David Kelly commented, our economy has one foot in the grave and the other on a banana peel. Sort of. My read is a bit different. I believe the US consumer has both feet on a pile of bananas. Or slippery, juicy steaks. Because for the moment, at least as far as our super-expensive steak houses are concerned, business is just fine, thank you very much.

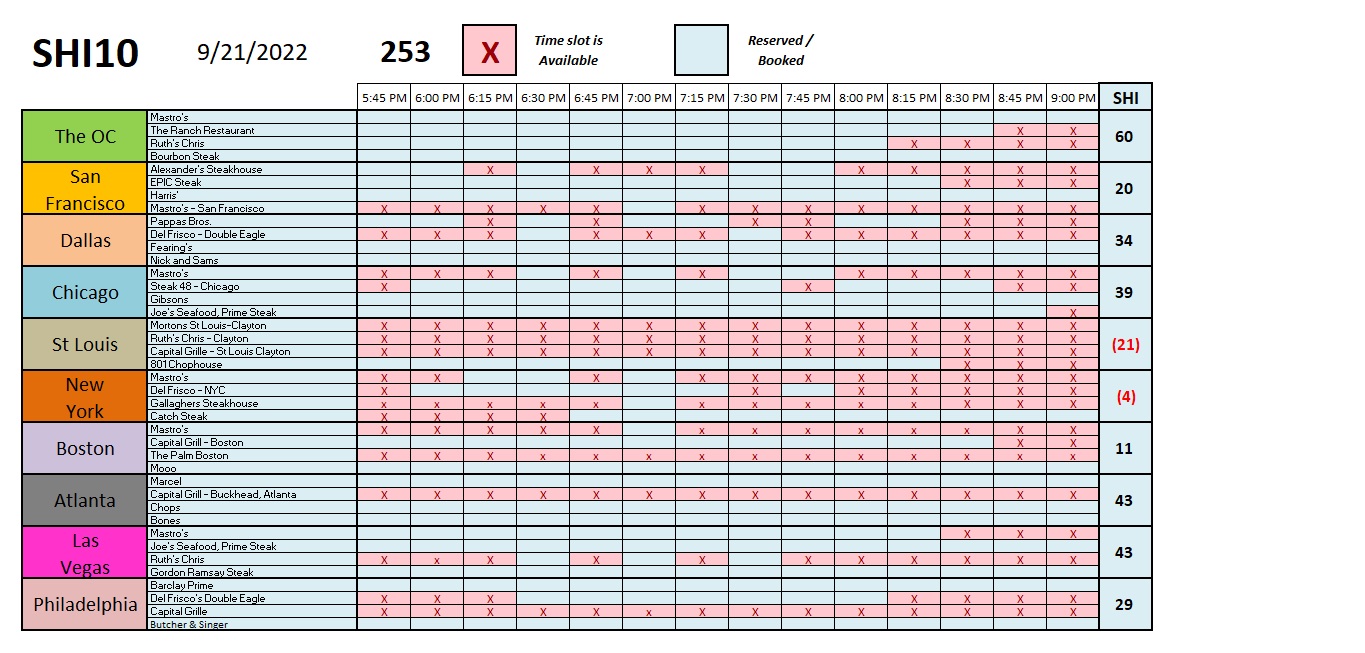

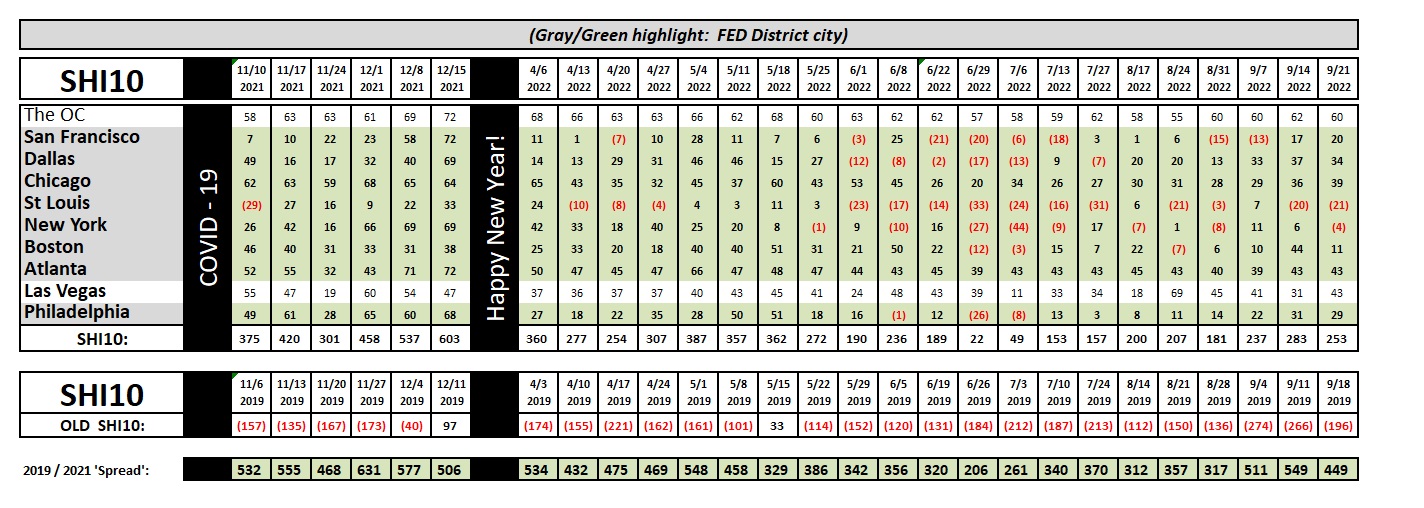

Weighing in at 253, this week’s SHI10 remains quite consistent with weeks past. I see no meaningful change in opulent eatery reservation demand in any of the 10 major cities where we track reservation demand. If the American consumer economy already had “one foot in the grave” as David Kelly suggested, I would expect to see a significant decline in demand at America’s priciest-of-steak-houses across the country. As we can see in the longer-term trend below, expensive steak demand remains consistent and fairly robust:

I have no doubt that large segments of American consumers are feeling the pain right now — from both inflation and FEDs interest rate hikes. Sure, gas prices are down — which helps many consumers — but that’s only one small piece of the total “spending” pie. And I have no doubt some American industries are also feeling serious pain — consider the home builder, the Realtor or mortgage lenders. These businesses have literally slipped on banana peels and then fallen off a cliff.

But the $100 steak is selling just fine over at Mastros in the OC or at ‘Bones‘ in Atlanta. There isn’t a reservation to be had at either restaurant this coming Saturday evening. These places are packed and their grills are smokin’.

Because this is a very different “downturn” than the Great Recession of 2008.

In that recession, the US economy was near total collapse. Between 2002 and 2007, consumers, investors and US industry — and the entire world, to some extent — pushed their chips “all in” completely believing the financial engineering story sold by S&P and Moody’s. I won’t repeat all the contributing factors today, but suffice it to say that today we know a single-debt issue (whether a mortgage or corporate bond), with a single borrower, when sliced into 10-different pieces, and sold to 10-different buyers does not magically improve the quality of that debt issue. Nope. A banana is a banana, whether whole or sliced into 10-different pieces.

Anyway, because of this voodoo and financial chicanery, back in 2008 the US economy almost completely collapsed. Every consumer and every business was impacted identically. In 2008, our entire economy slipped on banana peels and fell off a cliff.

Not today. No, today, some segments of the economy are doing quite well … and others, well, not so good. And so the FEDs incremental rate hike earlier today was designed to push more consumers and business from the “I’m doing just fine” camp into the “I’ve slipped on a banana peel and fallen down” camp. With each incremental increase, the FED hopes to slowly push our economy back to that equilibrium point where, in the aggregate, the economy is no longer too hot.

Chairman Powell is much like Goldilocks at a porridge tasting: This one is toooooo hot, you’ll recall she said. This one, too cool. But this one … this one is JUST RIGHT!

Time will tell … but I think making porridge at the correct temperature is much easier. 🙂

<:> Terry Liebman