SHI 9.28.22 — Rhymes With Dread

SHI 9.21.22 — Tough Love, Baby

September 21, 2022

SHI 10.5.22 – Chaos in the Kitchen

October 7, 2022

Years ago, a TV show called “The Tonight Show” starred Johnny Carson. For decades, he was a late-night comedy icon. He used to do a “bit” early in the show where he play-acted as “Carnac the Magnificent,” a character much like me – someone who could see far into the future!

Never magnificent, but often funny, Carson would “predict the future.” OOOOOOOOoooooo!

We saw him holding a plain, white envelope up to his forehead, closing his eyes for a moment, and then he would utter something like “rhymes with dread.” With great flourish, he would then tear open the envelope, take out the contents, and with a serious voice and deadpan facial expression, read those contents, whereupon we would see he miraculously predicted the future!

“

I predict ……………. ”

“I predict ……………. ”

In this case, had Carson uttering “rhymes with dread” with the envelope resting on his forehead, later reading the message, he would have said, “… rhymes with dread …. How you feel before you open your most recent monthly 401-K retirement plan statement.”

But of course, that doesn’t rhyme with ‘dread.’ I’m making this up … Carson would never have made such a gaff. 🙂

However, ‘FED’ rhymes with dread. And right about now, everyone from CEOs to lowly employees, from sophisticated investors to individuals with 401-Ks, are worried about the ongoing FED rate hikes and the damage done. FED definitely rhymes with dread. Don’t open your mail! Shred that monthly statement! Wow: Shred rhymes with dread, too!

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Sort of. At the end of Q2, 2022, in ‘current-dollar’ terms, US annual economic output rose to $24.85 trillion. Yes, during Q1, the current-dollar GDP increased at the annualized rate of 7.8%. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the 3 big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Predicting the future is serious stuff.

And hard to do. At least accurately. For example, consider the image to the right. About one year ago, financial experts who’s business and livelihood depend on their ability to accurately predict the future of interest rates, using primarily data and commentary from the FED, believed that at this time in September of 2022, the FED funds rate would be less than 0.25%. Boy were they wrong.

By May of this year, that same group of financial wizards agreed the rate would be closer to 1.875% by September of 2022. Back in May, by the years end, they predicted the rate would be 2.875%. Today, as you can see from the light-blue dot-line to the right, that same group expects the FED funds rate to be about 4.25% when 2023 begins.

Boy were they wrong.

But we probably need to give them a pass on this one … because the primary source of data for their predictions was the FED itself. About a year ago, you may remember Chairman Powell’s comment, “We’re not event thinking about thinking about raising interest rates.” Boy was he wrong.

But perhaps we need to give Mr. Powell a pass too. Because the FED employs just over 400 PhD economists who’s full-time job is to accurately predict the future on behalf of the FED … and the United States … and, by extension, the entire global economy.

Boy were they wrong.

https://www.federalreserve.gov/econres/theeconomists.htm

And I won’t give them a pass, either. 400 PhDs. Wow. You’d think this esteemed academic group of brain-i-acs would have been, at the minimum, “a bit closer” with their forecasts, right? I mean, I’m just one guy, and I definitely don’t have a PhD in Econ. But at least I signaled an inflation concern about 18 months ago when the US rained-down trillions of dollars in post-pandemic stimulus. (Right click, open a new tab.)

https://steakhouseindex.com/shi-3-10-21-spending-4-5-trillion/

https://steakhouseindex.com/shi-3-17-21-letting-it-rip/

Let it rip indeed.

“America is adding fiscal rocket fuel to an already fiery economic-policy mix. (With) President Biden’s $1.9 trillion stimulus bill, about $6 trillion is the total paid out since the start of the crisis. The Federal Reserve and Treasury plan to pour some $2.5 trillion into the banking system this year, and interest rates will stay near zero. For a decade after the global financial crisis of 2007-09 America’s economic policymakers were too timid.

Today they are letting rip.”

Recall this quote was from the economic experts over at the Economist magazine. Even so, financial experts from all reaches of the globe believed the massive money supply stimulus was needed to ensure the world avoided a massive depression post-pandemic. For good reason. Throughout history, many economies were crushed for years post-pandemic. Consider the European experience after the Bubonic Plague: The plague killed more than 20 million people in Europe between 1347 and 1352 — one third of Europe’s entire population. It is estimated that GDP fell by over 6% in 1349. Life for those who remained was dismal. It was a horrible time.

But not for surviving laborers: Perhaps not surprising, Europe found they had labor shortages. Just as we do today. As people died, it became harder to find anyone to plow the fields, harvest crops and produce goods and service. ‘Peasants’ began to demand higher wages! Sound familiar? 🙂

European rulers tried to suppress wage increases. There’s nothing a king likes less than paying a peasant more money: An English law in 1349 attempted to force workers to accept the same wages they received in 1346. A similar law, the ‘Statute of Laborers,’ was issued in 1351. The statute said that every healthy unemployed person under 60 years old must work for anyone who wanted to hire him. Wow.

Workers who violated the Statute of Laborers were fined and were put in stocks as punishment. Double wow. But in 1360, punishments became even worse: Workers who demanded higher wages could be sent to prison and—if they escaped—branded with the letter “F” (possibly for Fugitive) on their foreheads.

Ahhh … the good old days.

Of course, I’m kidding! Put down those pitchforks! I’m kidding! 🙂

Clearly, European governments didn’t hand out stimulus payments to their peasants back in the 1340s and 1350s. Unlike today. However is is interesting to note today’s repeat of the post-pandemic labor problems from centuries ago. I wonder if any of the FEDs 400 brilliant PhDs considered making a similar labor prediction? Hmmm….

Back to those 401-Ks for a moment. The FED, in symphony with every other developed world Central Bank, is engineering the large decline in your 401-K. Significant interest rate increases change the ‘business landscape.’ By making borrowing capital more expensive across the board, all business — some slowly, some quickly — are adversely impacted. Meaning, in theory, corporate earnings are now expected to be lower than prior forecasts, which means the company’s value is lower than before. As the price of your 401-K stocks reflect this movement, they are down in value, by extension. This is the source of your 401-K dread. The FED. Rhymes with dread.

And it may make you wonder what all those egg-heads at the FED do with their time. What did they envision in the post-pandemic playbook? Did they anticipate a shrinking workforce causing labor shortages? Did they predict the massive fiscal stimulus and supply-chain problems might trigger significant inflation?

I’m guessing no. Because they all seem in a panic today. They seem to be tripping over themselves in their haste to raise interest rates. Here and across the developed world. Why didn’t they expect and anticipate labor shortages and wage increases? Why didn’t they anticipate the inflationary implications of the fiscal stimulus?

Who knows.

But interestingly enough, some of the early price increases are now back to about where they were pre-pandemic. It appears business segments most sensitive to higher interest rates are reverting to the mean the quickest. Consider lumber prices, the primary component of new homes:

Full circle. Is this what the FED is hoping will ultimately happen to labor costs? Interesting question, right?

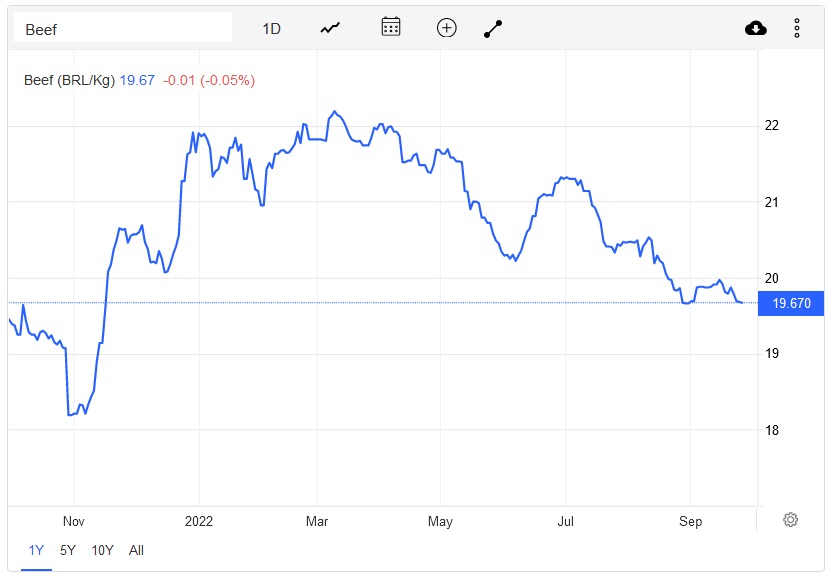

Of course, here at the Steak House Index we’re most concerned about beef prices. Beef prices? Have they gone full circle too … returning to their pre-pandemic price? Will expensive steak prices decline at Mastros?

Not so far. Beef prices are down over 10% since the beginning of 2022 … but they are still more than double their cost back in 2018. So the trend is good … but prices have a long way to reach the average $10 back in 2018. I believe beef price movement is more closely aligned with general agricultural conditions than interest rates. Thus, their price movement is less impacted by rising interest rates than general supply/demand influences.

While beef prices are down in 2022, expensive steak prices are not. When I began the SHI years ago, I commented that dinner-for-4 at Mastros or Ruths’ Chris on Saturday night would set you back about $400. No longer. Today, with food and drink, I think you’d be fortunate to enjoy your amazing meal for less than $600. And yet, well-heeled patrons are still lining up to make reservations and slap $600 or more on their AMEX or VISA.

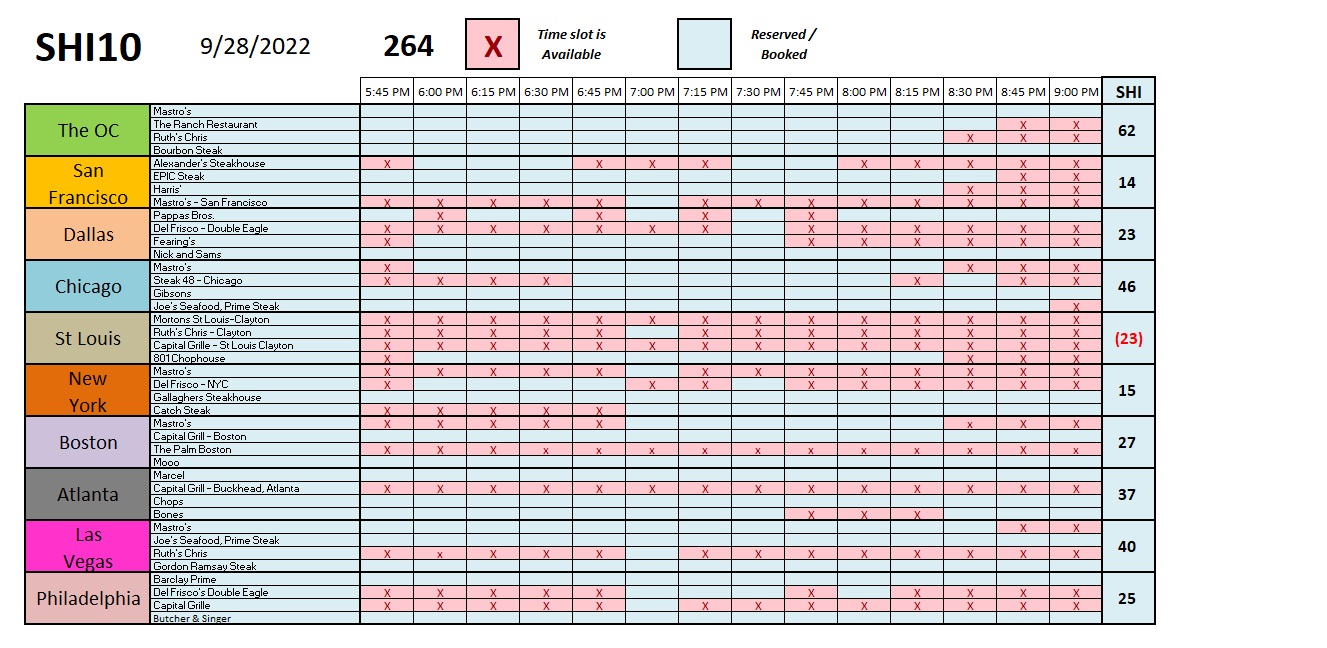

This week, as we see above, only one SHI market is in the red. St Louis seems to be having a tough time right now. As you know, the “Eighth District” of the Federal Reserve banking system is located in St Louis. Here is the August 2022 “Summary of Economic Activity” provided by the St Louis FED:

“Economic conditions have declined slightly since our previous report. Consumer demand for goods and services has slowed slightly and price increases have continued across a broad range of sectors. Labor shortages have limited activity in service sectors, and employers continue to raise wages to attract and retain workers. Input prices rose, and most firms reported plans to pass additional increases on to consumers. Real estate contacts saw homebuying activity slow significantly, while demand for rental properties strengthened. The agriculture and manufacturing sectors experienced continued supply chain bottlenecks and input shortages that contributed to price increases. The overall outlook for business conditions over the next 12 months has improved slightly but remains pessimistic.”

My italicized highlights do not paint a pretty economic picture for St Louis. That report is consistent with the current level of opulent eatery steak-house reservations we are seeing in our two SHI charts.

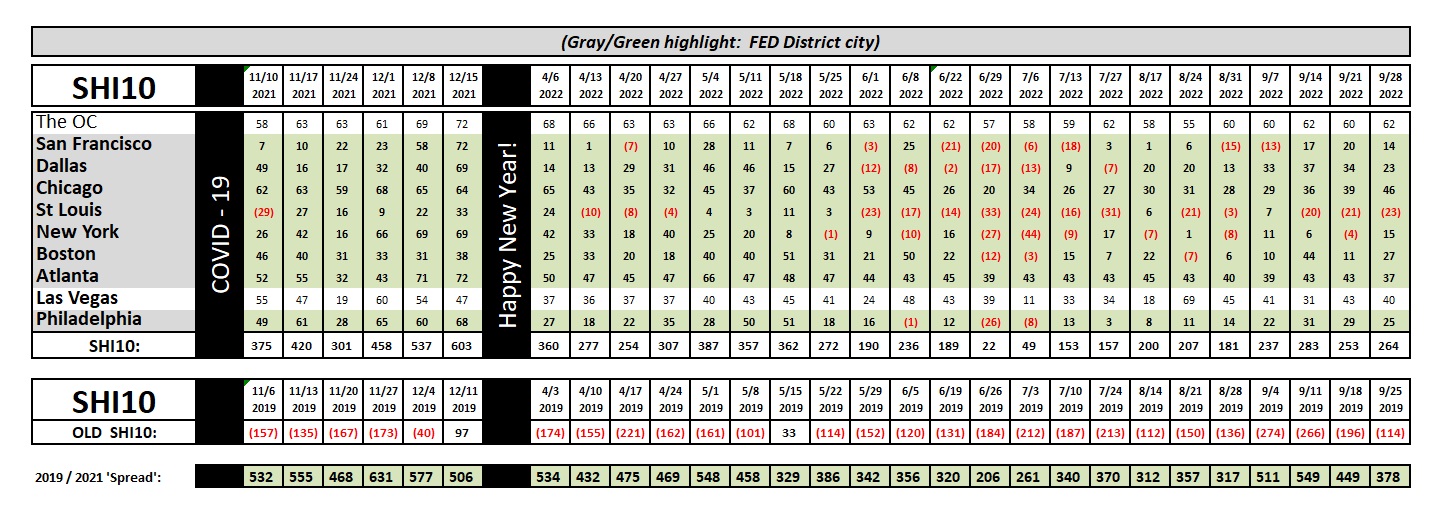

Here’s the longer term trend report.

Big picture: So far at least, FED rate increases have had little impact on the top quartile of Americans who can spend $600 on dinner. Our most expensive steak houses are doing fine. Will this change? It all depends on how draconian the FED decides to be in the next 3-6 months. If their 400 economic PhDs pay close attention to unfolding economic data, perhaps they will advise the FED to pivot, much like the Bank of England did today, and cool their jets for a while. Time will tell.

Happy Birthday, Dad.

<:> Terry Liebman