SHI 3.17.21 – Letting it RIP!

SHI 3.10.21 – Spending $4.5 trillion

March 10, 2021

SHI 3.24.21: The Talking Heads

March 24, 2021

By any measure, life in the pre-colonial “Age of Exploration” was harsh.

Perhaps that’s why nascent explorers left their homes, their families, gave up all they knew, to sail into the unknown. Imagine this: You leave family, friends and home behind, board an rat-infested, overcrowded ship, likely with inadequate food and water supply. Time will tell. You’ve agreed to sail across the uncharted, limitless ocean without known destination. There is no map. Will your ship sail over the ocean’s edge? On board, with every rising sun, the witches cauldron of emotions boils hot: Hope, fear, and a dash of anxiety and despair, blend together. Everyone is on edge.

And then, miracle of miracles, the ship actually finds land! You have discovered “The New World!” Against all odds, the unknown becomes known. The journey a success, coveted riches are “found”, and soon thereafter, you expect to find your way home once again, wiser and richer.

But late one evening, or more accurately in the early morning hours of a new day, while the crew sleeps under a crescent moon, the captain orders all the ships burned. Hours later, awakening, you find only the smoldering embers of the ship husks to be visible. There will be no return trip. Welcome to your brave new world. Look forward … there is nothing behind you. Only the new future awaits.

“

Let the economic experiment begin. “

“Let the economic experiment begin. “

As I’ve commented in prior blogs, today we find ourselves in uncharted economic waters, not knowing what we’ll find when we get “to the other side” — whatever that means. The Economist magazine, first published 177 years ago, shares my concern:

“America is adding fiscal rocket fuel to an already fiery economic-policy mix. (With) President Biden’s $1.9 trillion stimulus bill, about $6 trillion is the total paid out since the start of the crisis. The Federal Reserve and Treasury plan to pour some $2.5 trillion into the banking system this year, and interest rates will stay near zero. For a decade after the global financial crisis of 2007-09 America’s economic policymakers were too timid.

Today they are letting rip.“

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Before COVID-19, the world’s annual GDP was collectively about $85 trillion. Then it shrank … then bounced back! We can thank global fiscal and monetary policy for the bounce. According the the Q3, 2020 ‘preliminary’ numbers, annual US GDP is back UP to about $21.1 trillion. And still, together, the U.S., the EU and China continue to generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

The Economist article suggests that the “good news” is not confined to just America. World-wide, manufacturing is spooling up. Expectations are that the US and other stimulus programs will ignite a global demand for goods, further boosting the US trade deficit by more than 50% of the pre-pandemic levels, as the US economy sucks in imports.

Good news? Bad news? Who knows. Time will tell.

But we know with absolute certainty that the “economic” ships that brought us here are gone. They have been burned down to embers. For the US and the world at large, there is no return passage to the pre-pandemic economic theories of Keynes and Friedman. No, like it or not, good news or bad, our “Brave New World” is some new-fangled de facto version of ‘Modern Monetary Theory.’ Once again, I’ll quote the Economist:

“Today’s policymakers have a guaranteed place in economic history, though they may not come to be seen as heroes. That is because America is running an unpredictable three-pronged economic experiment that features historic levels of fiscal stimulus, a more tolerant attitude at the Fed towards temporary overshoots in inflation, and huge pent-up savings which no one knows if consumers will hoard or spend.”

The stimulus programs, acknowledged and supported by the governments and central banks around the world, in response to the Covid-shutdowns, at their essence, represent a post-Keynesian, post-Monetarist era, and raise some fascinating economic questions: Can unprecedented expanding consumption, money supply and sovereign debt levels take place without a corresponding inflation bubble? Or will the theories of Mr. Keynes and Mr. Friedman still apply in today’s ‘Modern’ world?

We’re about to find out. The assures us they can contain inflation. Friedman would argue otherwise … but Powell and friends remain confident. Again, time will tell … because there will be no return to old-world economic theories. We are in the new world now.

“The danger for America and the world is that the economy overheats.”

The Economist magazine

This is the backdrop for today’s FED meeting.

The FEDs rate decision was unsurprising: Rates were left unchanged. What I found a bit more interesting were two of their new forecasts:

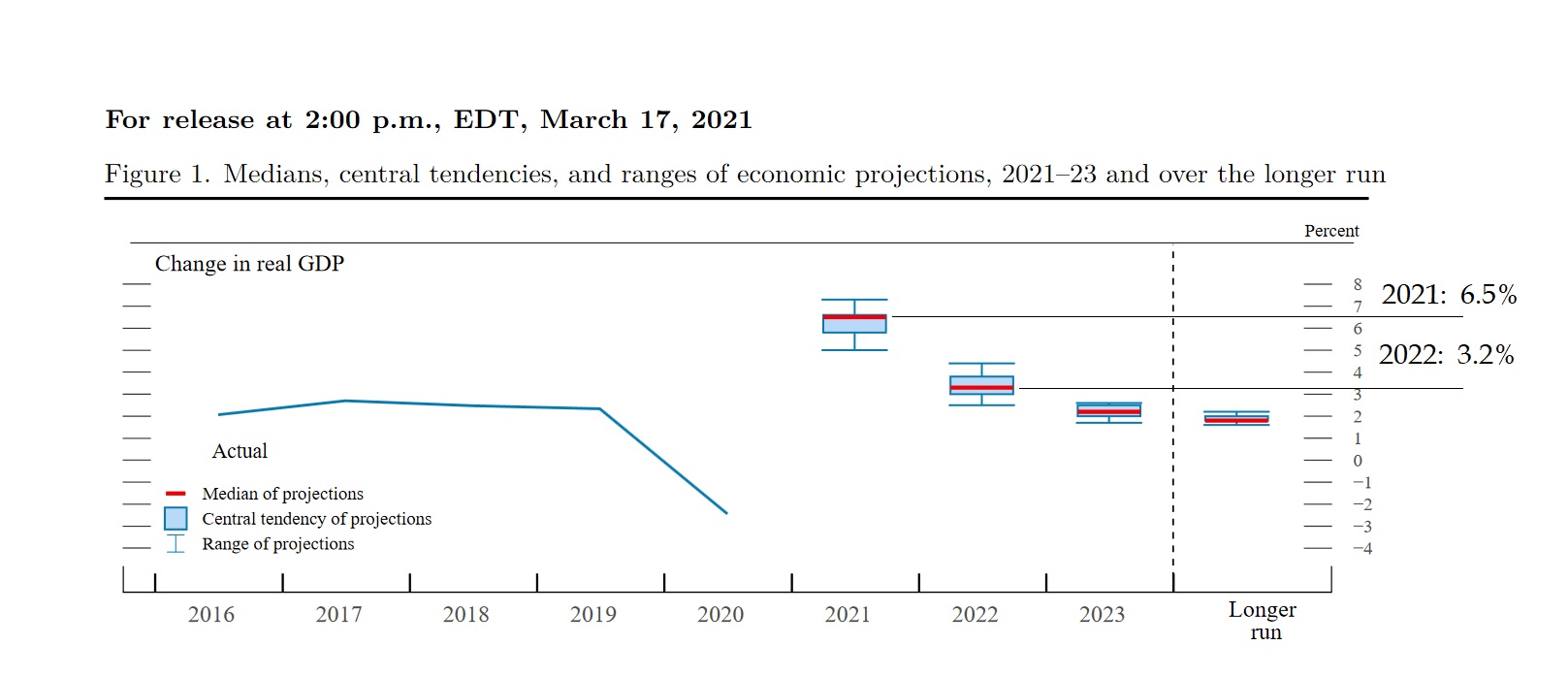

First, the FED expects inflation to run hotter in the 2nd half of 2021. They believe inflation is “on track” to “moderately exceed 2%” for some time. Second, the FED now expects 2021 GDP to eclipse 6.5%! Wow!

Finally, the FED maintained this policy:

“In addition, the Federal Reserve will continue to increase its holdings of Treasury securities by at least $80 billion per month and of agency mortgage‑backed securities by at least $40 billion per month until substantial further progress has been made toward the Committee’s maximum employment and price stability goals.”

That’s not new policy … but it does give them the leverage to step in and buy more than $120 billion each month — As needed to keep a lid on long-term rates. The FEDs “implementation notes” say they may:

“Increase holdings of Treasury securities and agency MBS by additional amounts and purchase agency commercial mortgage-backed securities (CMBS) as needed to sustain smooth functioning of markets for these securities.”

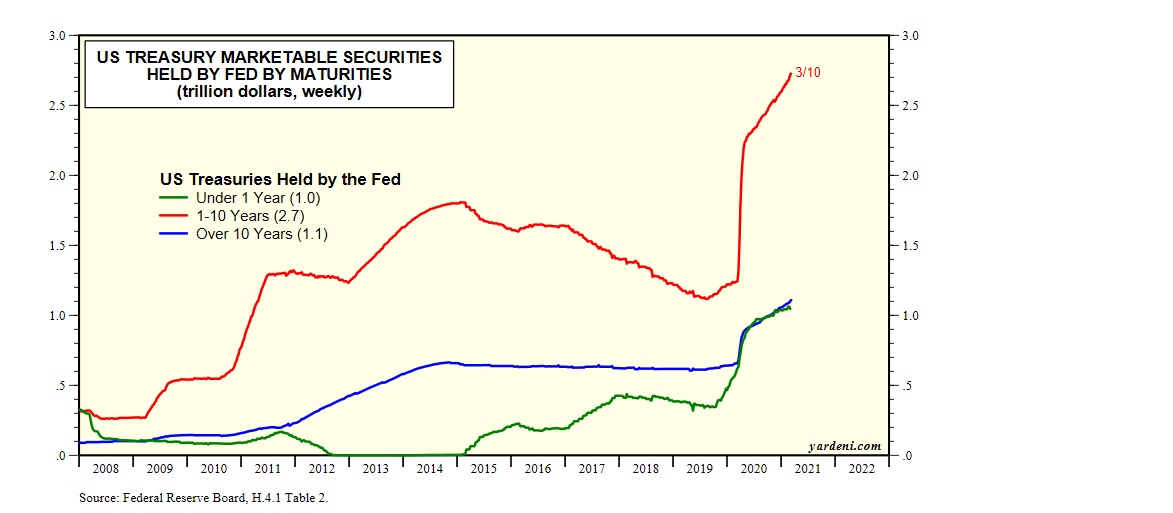

Right. Another “tool” in their long-term rate management tool-box is the choice of duration. The FED can purchase Treasury debt of any duration. To date, they have purchased predominately debt in the 1 – 10 year space, as evidenced by the graphic below, courtesy of Yardeni Research:

What would the FED do if rates rose in an “disorderly” fashion? Conceivably, they would shift purchases to more of the “over 10 years” variety, adding downward pressure on longer-term rates. Between this tool, and the ability to increase purchase levels as needed, I remain confident we won’t see more rapid increases in longer-term rates.

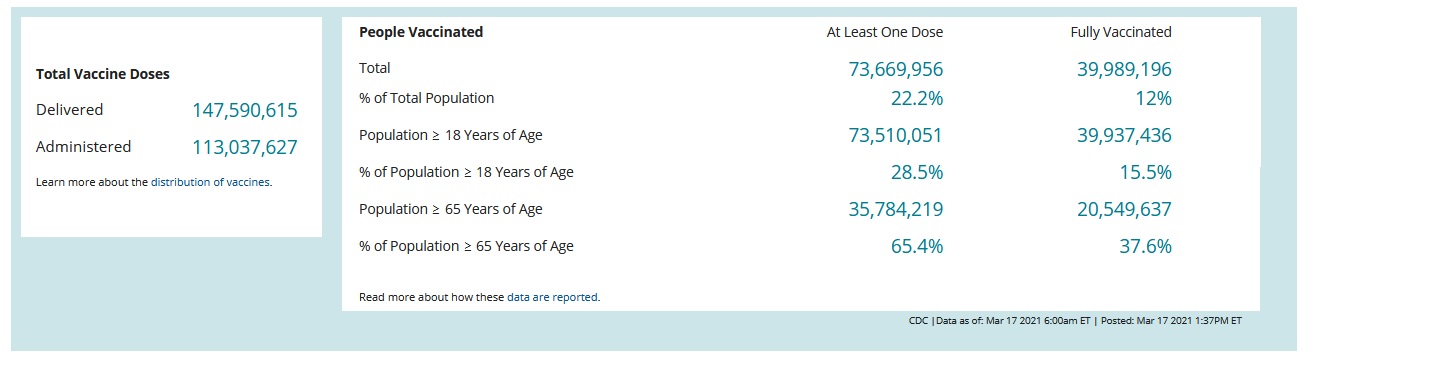

It’s also important to keep an eye on the pace of the vaccine rollout. Per the CDC, as of today, over 113 million vaccine doses have been injected:

Vaccination rates are expanding in the US. As the economies of the post-Covid world begins to gain traction, and the generous fiscal stimulus programs find their ways into the economic machinery, financial markets, economists and the FED are all convinced the economy is about to go on a tear. Let ‘er rip!

Huabei! Jiebei !!!

Mona Wang is 27-years-old. She lives in the Chinese city of Xi’an, works in finance, and at the end of last year owed more than $15,000 to various online lenders. Her total debt is roughly 15X her monthly income, primarily due to her spending on Salvatore Ferragamo shoes and other branded items. That’s a hefty debt load.

“Just spend!” and “Just borrow !!!” are the literal translation of Huabei and Jiebei, two of the ‘personal-lending’ services of Ant Group, the fin-tech arm of China’s behemoth ‘Alibaba’. China’s consumers have taken this suggestion to heart: They are spending and borrowing – big time!

Huabei and Jiebei were used by about half a billion Chinese citizens in the 12 months to June alone — most of whom do not have or use credit cards. Many used the short-term loans to pay for expenses such as prestige cosmetics, electronic gadgets and costly restaurant meals. They found credit easy to obtain, thanks to Ant and other Chinese fin-tech companies. In 2019, online loans accounted for as much as half of short-term consumer loans, according to estimates from Fitch Ratings.

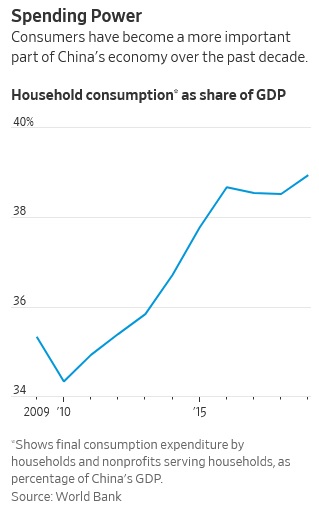

For decades, China’s has been a manufacturing and exporting powerhouse. They still are. But with rising wages, and the growth of on-line lending, their consumer-class is expanding too. In fact, in the past 10 years, ‘household consumption’ as a percentage of GDP has approached 40% of total Chinese GDP.

Sure, this lags behind the 65-75% figures from the developed nations of the EU and the US – but consumers in China are catching up fast. And remember: China’s population is 2X the total populations of the US and the EU combined! China has a population of about 1.4 billion people. They have a LOT of consumers!

According the data released on Monday by China’s “National Bureau of Statistics,” Chinese industrial output in the January-February period rose 35.1% from a year earlier while retail sales, expanded 33.8% over that same time frame. And like here in the US, housing demand is on fire: Home sales by volume, an indicator of demand, soared 143.5% in the first two months of 2021 from a year earlier, while property investment by value gained 38.3% over the same stretch.

The Bottom Line: We can bemoan the economic choices made, but, keeping in theme, that ship has sailed. 🙂

Global stimulus funds have begun to permeate the world’s economy. Now, we have to anticipate the impact and implications of this post-Keynesian, post-Monetarism era, and attempt to figure out how the new economic world will evolve under Modern Monetary Theory.

One thing seems certain. The FED and the Biden administration have delivered an electric jolt to the US economy — like it or not. And now, as vaccine distribution and individual bank accounts expand, the FED, too, believes this year’s GDP growth will be downright staggering.

Let it rip.

- Terry Liebman