SHI 5.10.26 — Should YOU Build a Data Center?

SHI 6.3.26 – A Stairway to Heaven

June 3, 2026

SHI 6.17.26 — The New Federal Reserve

June 17, 2026

Apparently, the answer is yes. Everyone else is. 🙂

The hyperscalers are building them. ‘Cloud’ providers are building them. Private equity firms are building them. Real estate developers are building them. Utility companies are building them. Hedge funds are building them. Countries are building them.

Even Kevin O’Leary is building them.

Well, “building” may be an overstatement. Attempting to build them is probably more accurate. His proposed Utah project was originally slated to encompass roughly 40,000 acres and consume up to 9 gigawatts of power. Nine gigawatts. For a number of reasons, O’Leary’s plans have hit a few roadblocks.

For context, consider that 9 gigawatts could power every home in Utah for a full year. Additionally, every home in Nevada and Arizona. And there would still be enough electricity left over for another million homes in Idaho. That’s how much power 9 GW is.

“

Data centers for everyone!“

“

Data centers for everyone!“

The true scale of this construction boom we see around us is hard to fathom unless you look for it. It is massive and unprecedented. And it is truly ubiquitous across the globe. And yet, somehow, this whole thing seems perfectly reasonable to people.

Which raises some obvious questions: Doesn’t it have to end sometime? Don’t all booms end? When will it end? What does “the end” look like?

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. But is the US economy expanding or contracting?

Expanding … according the ‘advanced’ reading just released by the BEA, Q4, 2025 GDP grew — in ‘current-dollar‘ terms — at the annual rate of 5.1%.

The ‘real’ growth rate — the number most often touted in the mainstream media — was 1.40%. In current dollar terms, 2025 US annual economic output reached almost $31.50 trillion.

According to the IMF, the world’s annual GDP will expand to over $126 trillion in 2026. Of that amount, the US makes up over 25% — expected to reach $32.4 trillion by the end of 2026. Further, IMF expects global GDP to reach almost $135 trillion by 2028 — an increase of more than 28% in just 5 years.

America’s GDP remains around 25% of all global GDP. Just four countries—the United States, China, Germany, and Japan—generate roughly half of all economic activity worldwide. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

I believe the AI economy is rapidly becoming the world’s largest game of infrastructure musical chairs. Every player seemingly wants to be “first.” Each seems to assume they will secure land, labor, power, transformers, turbines, cooling equipment, memory chips, GPUs, building permits, and project financing before their competitor does. Of course, the problem is that every participant is making the same assumption. Can they all be right?

Probably not. Regardless of the outcome, this is truly one of the most extraordinary capital expenditure booms in modern history.

The 5 largest hyperscalers are now expected to spend $750 billion in 2026, with most of it directed toward AI infrastructure, data centers, networking, and power. Nvidia cannot produce enough chips. Micron cannot produce enough memory. Utilities cannot connect enough power. Contractors cannot find enough electricians. Turbine manufacturers have order books stretching years into the future. This group is tapping global debt markets rather than relying solely on internal cash generation. Bloomberg news recently framed the AI buildout as a roughly $3 trillion capital project—and possibly much more if you include power generation, transmission, and supporting infrastructure; they argue the scale of the buildout has moved beyond normal corporate spending into something closer to an industrial revolution-sized infrastructure program.

And yet everyone continues to announce new projects.

As I’ve commented in prior blogs, the biggest obstacle isn’t Nvidia’s chips. It’s power. Without power, a data center is simply an expensive concrete warehouse. And unlike semiconductors from Taiwan, electricity must be generated, transmitted, permitted, connected, and delivered locally.

Why? Because while power can theoretically be generated anywhere, using available local resources, it must use transmission lines, and all the related mechanical components, to move from source to user. Which is why we’re seeing an ever-increasing amount of “behind-the-meter” (BTM) electricity production from natural gas sources, “dedicated” power plants, and (in theory) small modular nuclear reactors.

Data centers may be “AI factories,” but data center owners are becoming utility companies. Google, Meta and Amazon? Power companies? Yep.

Again, for context, consider that in 2025 the entire US reportedly had roughly 1,300 GW of installed generating capacity. O’Leary’s proposed Utah project has a power requirements approaching 9 GW. That’s one project. In some cases, a single data center being built today could require nearly 1% of the entire capacity of the US. Consider these quotes from a “UtilityDive” article from 2 days ago:

A colossal data center is rising amidst the farmlands of Richland Parish, Louisiana. It will guzzle 2.2 GW of power, about twice as much as the entire city of New Orleans on a peak summer day.

Near Cheyenne, Wyoming, an even larger data center looms on the horizon. While its first phase requires only 1.8 GW, it is ultimately designed to scale to 10 GW, as much power as all of New York City draws at its peak.

As necessity breeds invention, the hyperscalers move BTM. They are building their own power plants. According to Bloomberg’s BNEF, about 100 GW are planned right now across 115 data center projects for behind-the-meter power generation. This is on-site gas-fired generation capacity, equal to about 18% of all existing U.S. natural-gas generating capacity. And that’s what’s in planning now. What will tomorrow bring? Obviously more.

And here’s where the story gets interesting.

You might think the BTM story will keep utility costs for the typical consumer lower. But UtilityDive says no, that is not the case:

Building your own natural gas power plant might appear to protect other energy customers by reducing new demand on the grid, but that’s not the case. Natural gas is a market-traded commodity, meaning data centers that gobble up lots of natural gas will naturally compete with other gas customers, increasing prices.

That does more than just worsen home heating costs. Since natural gas supplies 43% of U.S. electricity and gas-fired generators set the price of electricity in most hours, higher natural gas prices also raise electricity costs.

In fact, data centers with on-site gas plants could spike American energy bills more than connecting those data centers to the grid.

Hmmm … that’s a problem. It’s no wonder public backlash is building. Every new data center project either directly or indirectly competes against homes, factories, hospitals, and schools for power. Power is scalable, but power is finite. Certainly low-cost power is finite.

Fast forward, these days I suspect every proposed facility will encounter objections. As these objections build, many of the proposed 500-acre, multi-billion-dollar electricity-consuming data center may never be built. These conflicts are just beginning to grow in size.

Which brings us back to the obvious question: Is this a bubble?

Well, it’s complex. The short answer is probably yes. And probably no. The 1990s internet bubble popped, crushing the stock market, but the internet itself was not a bubble.

At that time, telecom companies buried extraordinary amounts of fiber-optic cable around the world, much of it unused and “dark fiber” for years after the dot-com collapse. Investors lost fortunes. But over time, the excess cable became instrumental for the internet proliferation.

Something similar might happen here. Might. Then again, it might not, depending on how much the current obstacles slow down future development. Remember, forecasts suggest this boom will continue for years.

But at some point, one of three things happens: First, demand for “compute” might slow or becomes saturated. Of course, that’s not the case today. According to research, there seems to be no sign of compute saturation. Demand remains insatiable.

The second potential problem: Costs become prohibitive. Input costs continue to spike. Component shortages, land costs, power, these are all rising. Again, this is a ‘finite’ problem. Even the hyperscalers will at some point decide the cost for another data center is too high. That time may be far in the future, but it is a legitimate constraint.

Third, local and national obstacles may at some point become insurmountable. The backlash is building. Quickly.

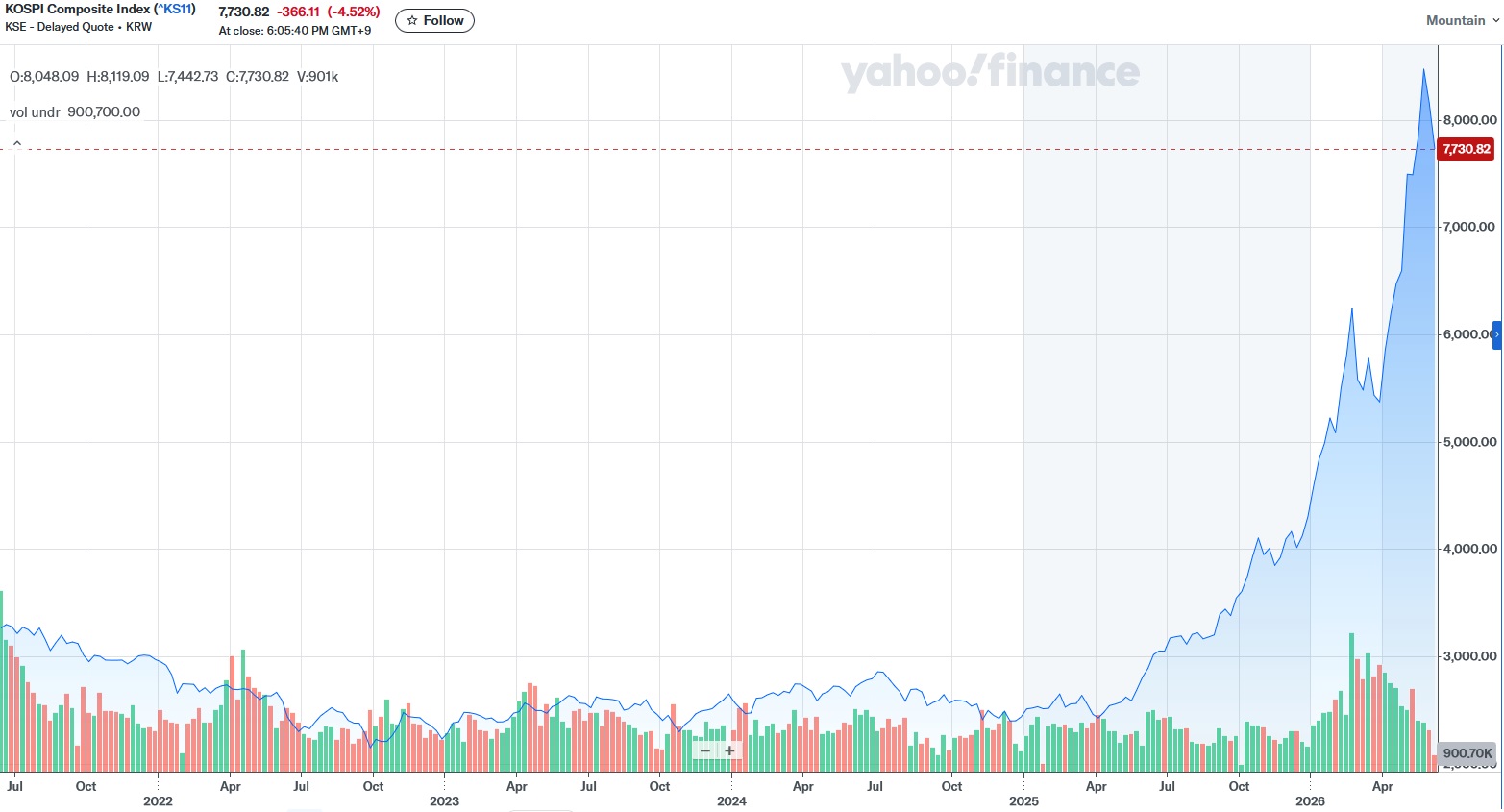

Consider the image below, the past 5-year performance of the South Korean stock market. Is this a mirror for growing data center construction costs? I wonder:

Known as the KOSPI index, this market has historically been fairly sleepy. Fast forward to April of 2025, when the index closed around 2,500. A year later, that number was about 8,500. There are 847 companies in the KOSPI. But that 6,000 point lift was generated by just a handful of companies.

What goes up must come down? Perhaps. Whether you believe it or not, if you are a stock investor today, I have two words for you: Be careful. We live in a world of contrast. Peaks exist because we have valleys. Just sayin. 🙂

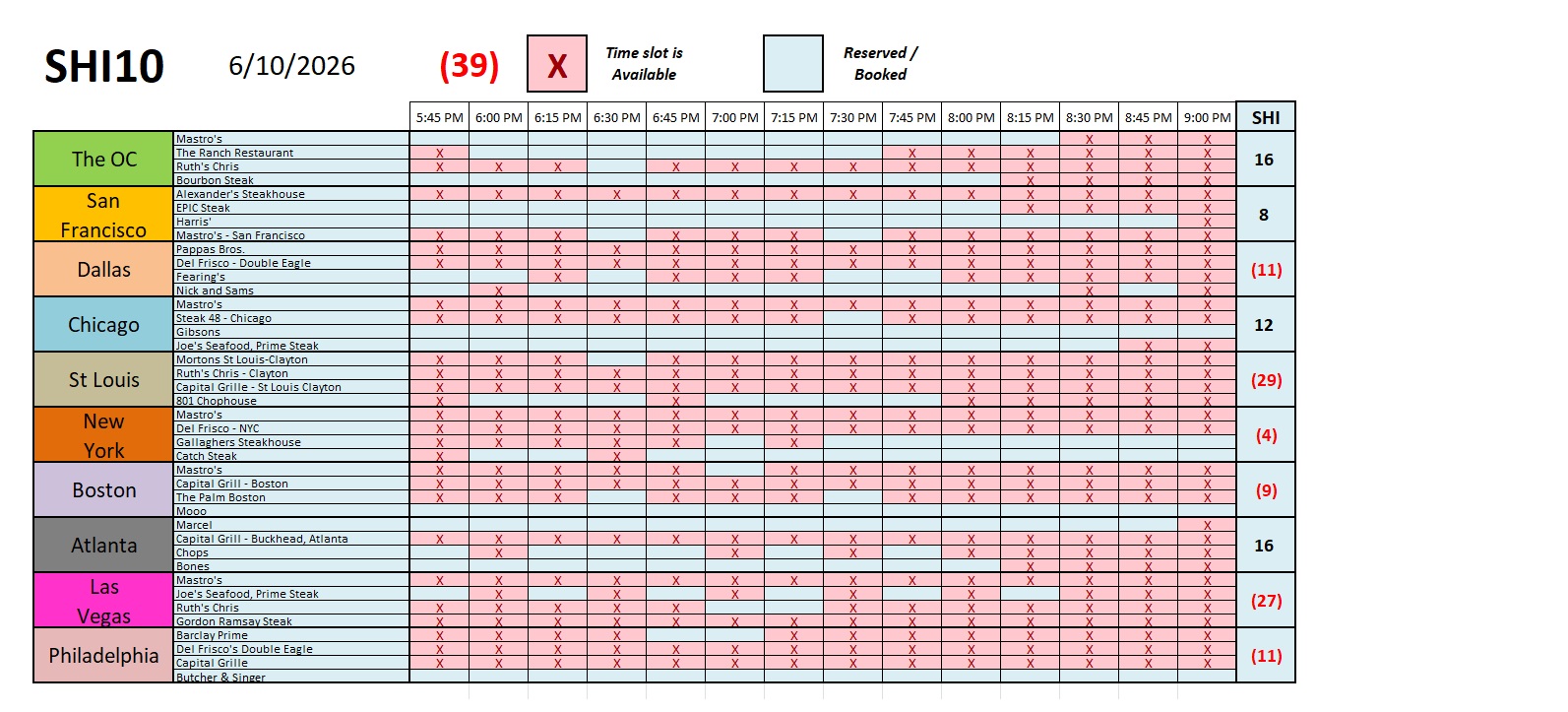

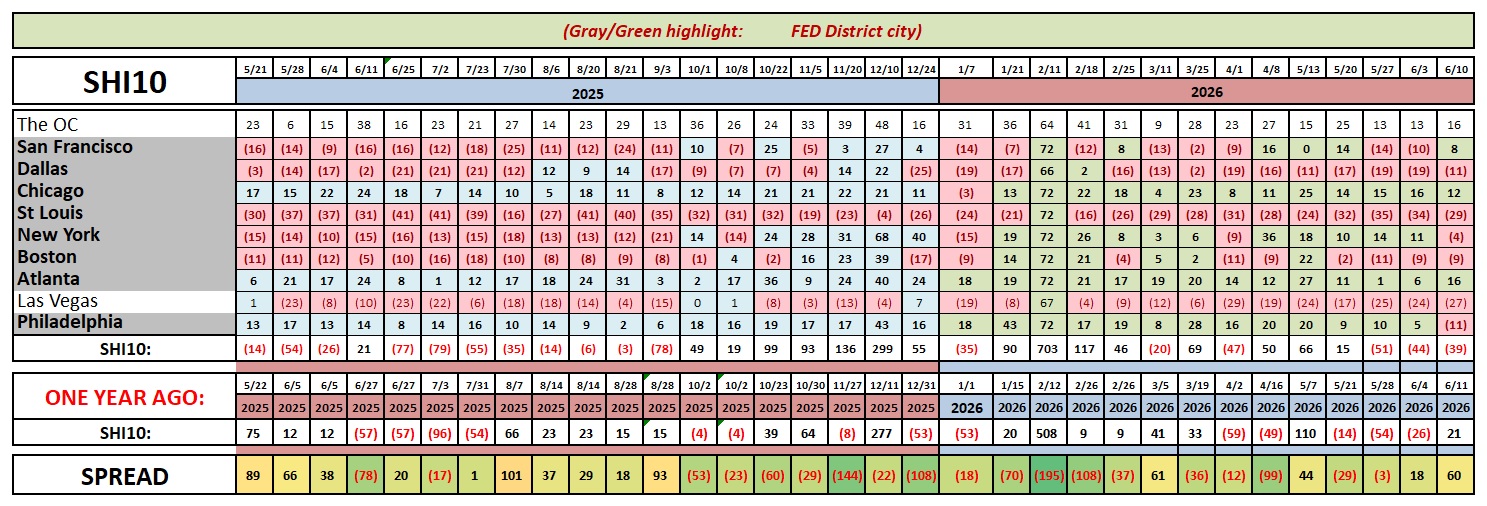

The SHI10 continues to merrily bounce along, reflecting a stable demand picture for expensive eatery reservations. The weekly numbers are above; the longer term trend, below.

I do find the trend in our OC steakhouses to be quite interesting. Recall that the maximum SHI reading for any one of our 10 cities is 72. The average for 2026 in the OC has been 27. While that number isn’t stellar, it has been consistent. And remember, this is an anecdotal index: There are a number of other market dynamics that may impact demand — such as the supply of expensive steakhouses to pick from — beyond basic GDP economics. There is also a diminishing utility for expensive steak dinners: At some price level, even if the economy is booming, some people will ‘opt out’ of the experience.

Make no mistake, however, there are storm clouds on the horizon. Maybe there are always storm clouds on the horizon. 🙂

Here’s one.

The Global Supply Chain Pressure Index (GSCPI), managed by the New York FED, is absolutely flashing signs of renewed stress.

After sitting quietly in negative or near-zero territory for most of 2023 and 2024—a period economists called the “great normalization”—the index has broken its stable, low trend. The reading spiked to 1.82 standard deviations above its historical norm. Concurrently, the World Bank’s companion Supply Chain Stress Index has surged back near its 2022 pandemic-era peaks. The supply chain normalization story is officially over. We can thank a perfect-storm of three catylists: First, the Iran conflict. Need I mention “Hormuz?” Second, we’re seeing a violent spike in manufacturing backlogs. Why? Well, the massive spike in data center construction, of course. Finally, both disruptions have triggered commodity price hikes around the globe.

There’s plenty of stress out there. But for now, the AI data center story is far more positive than negative. For now. 🙂