SHI 7.13.22 – Beatings will Stop when Morale Improves

SHI 7.6.22 – Treasury Yield Tops 15.8% !

July 6, 2022

SHI 7.20.22 – Gone Fishing

July 16, 2022

I’ve always smiled at this one.

It’s both funny and absurd at the same time. Unless, of course, the “person” being beaten is the American consumer, and the one doling out the punishment is the US Federal Reserve. Like it or not, this is essentially the FEDs ad nauseam message: We will stop beating (punishing) you, ‘Mr. and Mrs. Typical American Consumer’, when you stop spending so much money, forcing up prices, thereby driving CPI inflation to 40-year highs. When you stop doing THAT (morale improvement), then we will stop raising interest rates, slowing the economy, making your life miserable, maybe not triggering a recession and higher unemployment. Maybe.

You see, folks, its all your fault. 🙂

“

Should this be the FEDs new motto?”

“Should this be the FEDs new motto?”

I can see it now: The FED can make and sell T-shirts slathered with this slogan. Everyone will want one! These babies will sell like hotcakes! Or, at the very least, like 800-degree NY Strip steaks at Ruths’ Chris.

Oh wait. That’s not a good idea. This sure-fire FED novelty item is sure to inspire even more consumer spending, likely pushing up the costs of cotton shirts and silkscreen ink … triggering even more inflation! If that happens, the beatings will continue! Oh no!

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Significantly. By the end of Q1, 2022, in ‘current-dollar’ terms US annual economic output clocked in at $24.38 trillion. Yes, during Q1, the current-dollar GDP increased at the annualized rate of 6.5%. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

This is the irony of our economic system. Everything is great … until it isn’t. And everything is horrible … until it isn’t. The fact is, America’s economic performance is simply an ‘S-curve” twisting and turning, in serpentine fashion, above and below the long-term growth trajectory. That’s the way it’s always been … and the way it is likely to always be.

Which is why I find the FEDs rhetoric so entertaining:

“We understand the hardship high inflation is causing,” Powell said. “We are strongly committed to bringing inflation back down, and we are moving expeditiously to do so. We have both the tools we need and the resolve it will take to restore price stability on behalf of American families and businesses.”

You have to admit, this is pretty funny. The FED wants you to understand they agree — inflation is too high. They have the tools and resolve to fix this problem. They simply have to raise interest rates quite a bit, making everything you buy with debt far more expensive; and, in doing so, they will restore price stability for you, my fellow Americans, in the not-t0-distant future. In other words, they will stop the pain of higher prices by inflicting more pain. Got it?

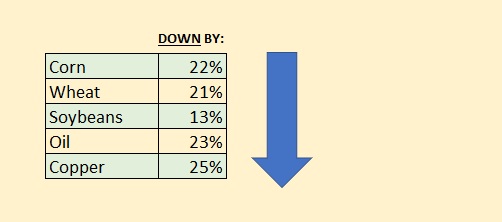

Well, the beatings seem to be doing the trick. Since mid-June, prices of many food and commodity inputs are down significantly:

Further, gasoline is down about 0.38 cents nationwide in the past month or so. And home sales activity has “cooled off” significantly.

But today’s CPI inflation report, once again, tells us consumer inflation remains at the highest level in 41 years. That’s right, today’s CPI number was one more ugly read in a long line of ugly reads this year. The FED is not happy with us right now.

HEY YOU CONSUMERS: STOP SPENDING SO MUCH MONEY AND THEN THE FED WILL STOP BEATING YOU! @#*&$%@ !!!!

🙂

Of course, if they beat us too much, and slow the economy too much, then we’ll have the opposite problem and the FED is likely to say:

HEY YOU CONSUMERS: SPEND MORE MONEY! WE NEED YOUR HELP TO BRING BACK AN ECONOMIC EXPANSION! @#*&$%@ !!!!

Anyway, I sometimes feel I beat this topic like the proverbial dead horse. Enough already, right? OK, ok, I’ll finish this thought and then we can head over to the steakhouses for a hard-earned, if not overly expensive, steak dinner.

About 70 years ago, the FED chairman was a guy named William Martin. He is famously knows as the guy who suggested it’s the FEDs job to take away the punch-bowl right as the party gets going. Assuming of course, the punch-bowl is spiked. Anyway, the quip suggests that the FED is an everpresent financial chaperone, with a perpetually watchful eye, making sure things at the “economic party” don’t get out of control. Martin also famously commented:

“Free markets, like free economies, have a way of going down as well as up, and thus reminding us that our system is one of profit and loss, entailing penalties as well as rewards.”

I get it. And, to some extent, I even agree with the premise. My issue with today’s FED behavior is simply this: I don’t believe the FED needs to remove the punch-bowl right now. I believe the markets will self-correct without the FEDs heavy-handed intervention. Notice I used the words heavy-handed. Light-handed, moderate intervention, in my opinion, is what is needed. Instead of removing the punch-bowl completely … perhaps they could simply remove some, or most, of its contents? Of course, the FED disagrees with my approach. They have their foot firmly on the brake.

In my opinion, the FED has overshot. They have smashed the punch-bowl, trashed the streamers, and tossed the canapes and hors d’oeuveres. Their message: Things are out of control in the US economy; so, party is over. Go home. But I simply don’t agree. They have gone too far … and the downstream repercussions concern me.

Martin’s 1955 speech is worth a read. I suggest you do. It’s only about 13-pages, double spaced: https://fraser.stlouisfed.org/files/docs/historical/martin/martin55_1019.pdf?utm_source=direct_download

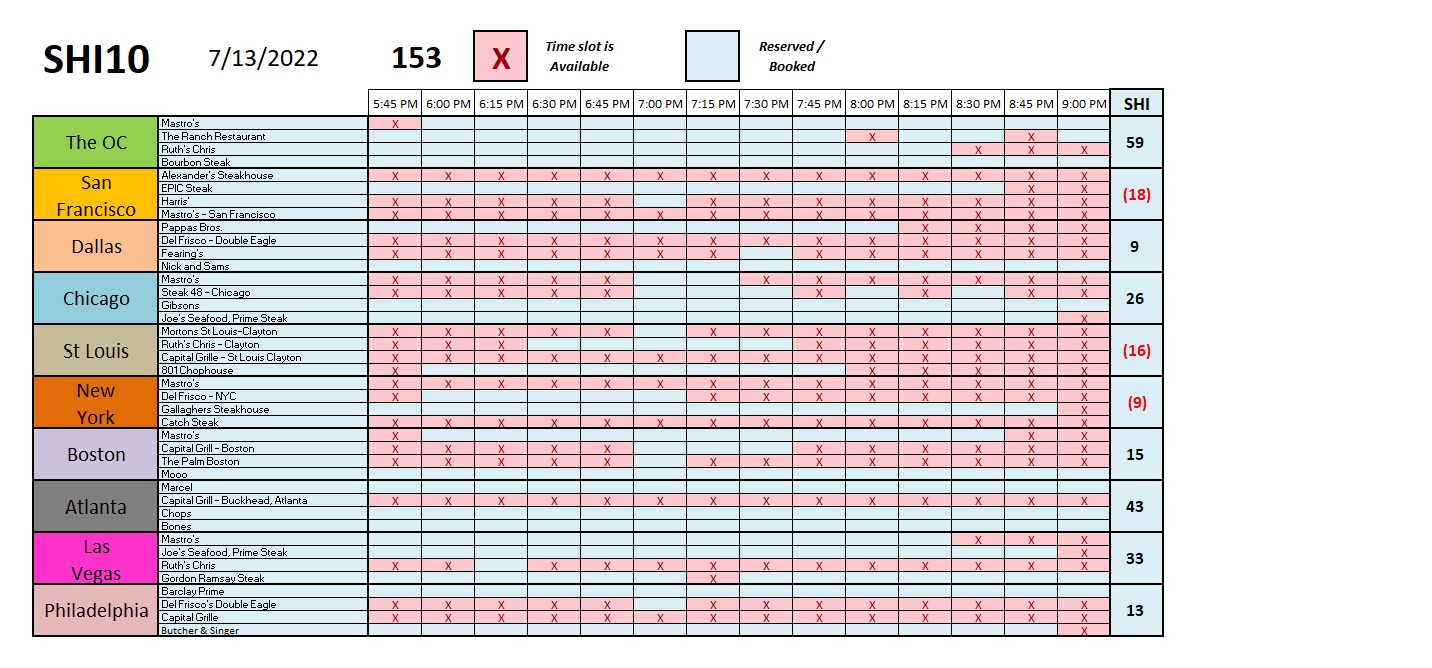

Well, this is interesting. You want to go to Mastros ‘Ocean Club’ this Saturday? Well, for the first time in months, a reservation-slot is open between 5:45 and 9:00 pm. Planning a trip to ‘Vegas? For the first time I remember, there is an open slot at Gordon Ramsay Steak. I don’t know if Chef Ramsay will be there … but if not, maybe someone else will yell at you. 🙂

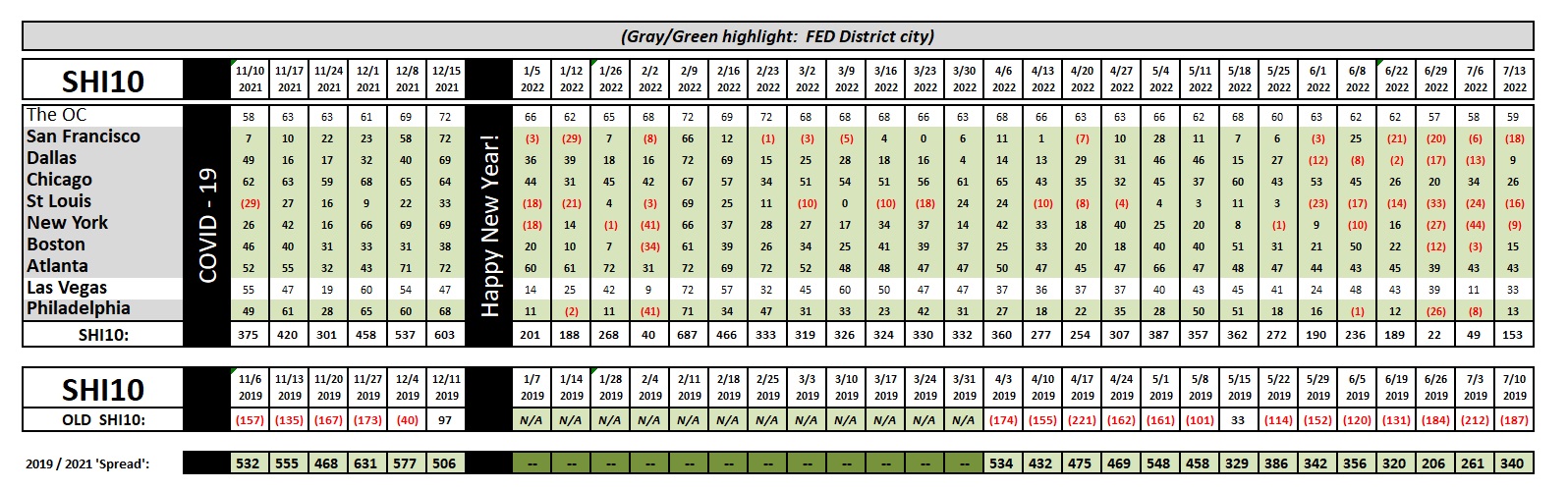

At 153, this week’s SHI40 is an improvement over the past few weeks. I doubt the improvement is economically significant, but — hey — improvement is improvement. Here’s the longer term trend report:

I’ll finish with this comment: The FED Beige Book is just out today. You’ll recall this is the FEDs commentary on current economic conditions across the US — much like our beloved Steak House Index!

Anyway, even with all the headwinds, the FED reports that: here are some highlights from today’s 32-page report:

Economic activity across the US “expanded at a moderate pace” since mid-May.

However, they stressed: Substantial price increases were reported across all Districts, at all stages of consumption:

“Increases in food, commodities, and energy (particularly fuel) costs remained significant, though there were several reports that price inflation for these categories had slowed compared with recent months but remained historically elevated. While several Districts noted concerns about cooling future demand, on balance, pricing power was steady, and in some sectors, such as travel and hospitality, firms were successful in passing through sizable price increases to customers with little to no pushback. Most contacts expect pricing pressures to persist at least through the end of the year.”

Well, there you go. Right or wrong, this is the reason they keep their foot firmly on the brake.

Thanks for tuning in.

<:> Terry Liebman