SHI 7.6.22 – Treasury Yield Tops 15.8% !

SHI 6.29.22 – $22 in 2022

June 29, 2022

SHI 7.13.22 – Beatings will Stop when Morale Improves

July 13, 2022

No joke … the 10-year Treasury yield rose to more than 15.8% …

… back in September of 1981. That was the all-time high for the 10-year yield, lifted to those heights by a vigilant Federal Reserve attempting to crush almost 2-decades of continuous inflation. Earlier that year, the fed-funds rate actually hit 20%. And if you had a personal loan pegged to the ‘Prime Rate’ index in 1981, plus a margin of 2.5%, the monthly interest rate you paid on that loan 2%. That’s right: 2% per month … or 24% per year. Ouch. By comparison, the interest rates today look pretty tame, right? 🙂

“

Imagine a 10-year Treasury at almost 16%.”

“Imagine a 10-year Treasury at almost 16%.”

It actually happened. Could this happen again? Could today’s inflationary pressures push treasury rates to sky-high levels seen only once in America’s history … over 40 years ago? Naaaa…. I’m happy to report that will not happen. Not now. Not ever. In fact, treasury rates are heading lower.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Significantly. By the end of Q1, 2022, in ‘current-dollar’ terms US annual economic output clocked in at $24.38 trillion. Yes, during Q1, the current-dollar GDP increased at the annualized rate of 6.5%. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Believe me … treasury rates are heading lower. Just not right now. And perhaps not for a while. But longer term, they are heading lower.

How can I be so certain?

Perspective. It’s hard to maintain when you’re smack in the middle of an unprecedented event. Like we are today. The pandemic has opened an economic Pandora’s Box, triggering crazy event after crazy event. Now, the FED is roaring like a lion, telling us they plan to rip inflation to shreds…and perhaps shred the economy at the same time. Recession fears run rampant. Our American consumer is very unhappy about prices at the grocery store and the gas pump. The stock and bond markets appear downright bi-polar, unable to decide if they should be worried or ebullient, knee-jerking every day with wild swings up and down. Don’t get me started on Tech stocks and Cathie Wood’s ARKK index, down over 65% in the past year. Many cryptocurrencies are in near free-fall, and NFT values, according to the JPG NFT Index — an index that tracks a handful of “blue-chip” NFTs — is trading down more than 70%.

And then we have interest rates. Ahhhhh …. interest rates. More than 230 years since it’s debut, the 10-year Treasury finally hit bottom, briefly touching a rate of 0.318% (in overnight trading) in early March of 2020. Imagine that … the 10-year Treasury almost touched zero in the early days of the pandemic.

And today it continues to bounce around like a cork on an angry ocean.

230 years. That’s a long time ago … America was brand-spanking new, and Alexander Hamilton was our Treasury Secretary. Yep … you know him … he’s the guy from the play Hamilton! 🙂

Anyway, I’m sure you’d agree that we could certainly gain a meaningful perspective on interest rates if we had 230 years of data, right? I mean, 230 years of ups and downs, 230 years of causes and effects, sure that data could help us develop a deep understand of rate movement … and perhaps we could even accurately forecast future rate movement! But where might we find such amazing data?

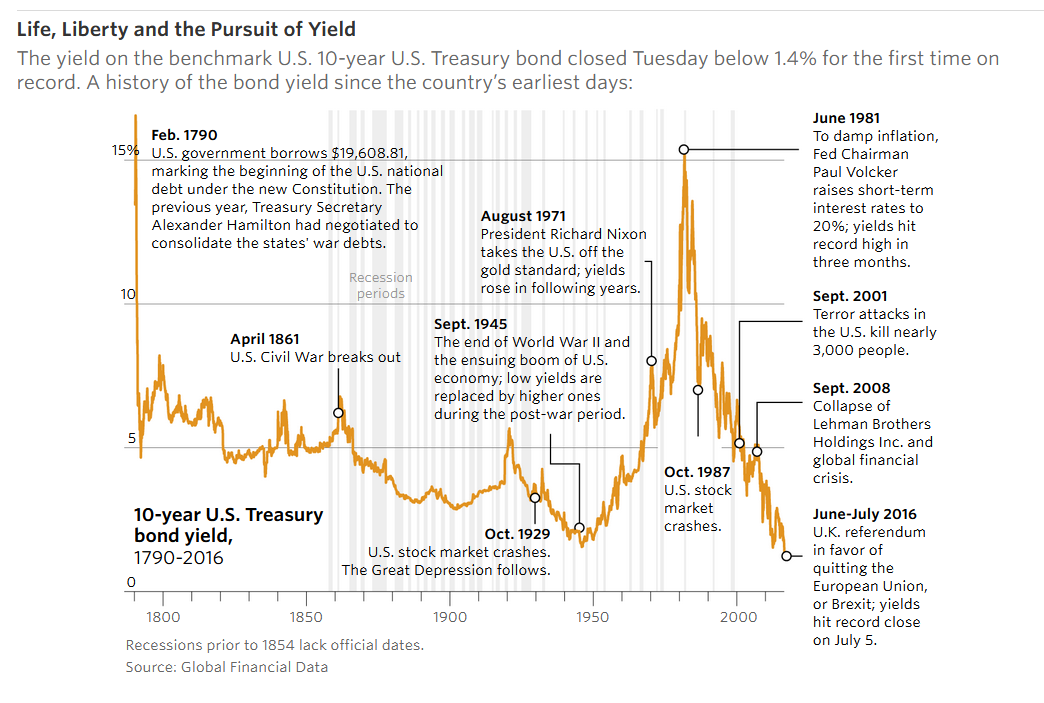

I thought you’d never ask. Right here, it turns out. Well, modesty requires that I give credit where credit is due. The Wall Street Journal did the research for us … and published it on July 6, 2016. Here’s the article if you’re interested (right click, open new tab.)

https://www.wsj.com/articles/are-treasurys-headed-for-1-new-lows-in-a-35-year-downtrend-1467760959

If the article won’t open, or you simply want to stay with me for the moment, let me share their awesome graphic:

Fabulous. Not only does the yellow line above show all rate movement since Alexander Hamilton introduced the 10-year Treasury around 1790, it offers some great insight on events at many of these pivotal historic times.

Yes, our federal debt was quite small at inception. Perhaps the “first” tranche of debt sold was $19,608.81 as the article suggests; however, according to the official numbers from the US Treasury and their site called “TreasuryDirect,” on January 1, 1790, our US federal debt stood at just over $71 million — $71,060,508.50 to be precise.

From that same site comes this brief history lesson:

Alexander Hamilton was the first United States Secretary of the Treasury, a Founding Father, economist, political philosopher and confidant of George Washington. He was one of America’s first Constitutional lawyers, and co-wrote “The Federalist Papers,” a primary source for Constitutional interpretation. As Washington’s Treasury Secretary, Hamilton was very influential in the policy decisions of the new government. An admirer of British political systems, Hamilton emphasized strong central government and implied powers, under which the new U.S. Congress funded the national debt, assumed state debts, created a national bank, and established tariffs and taxes. “A national debt, if it is not excessive,” Hamilton argued, “will be to us a national blessing.”

Hamilton, estimating the total public debt at $77.1 million, called for the issuance of new federal bonds to cover the debt. By assuming the obligation to pay this debt, the government firmly established its good credit. By February 1792, interest-bearing government bonds were selling for $1.20-on-the-dollar. A shrewd investor, buying $100 in bonds in 1786 (at a market price of about $15) could have sold the replacement bonds issued by the new government for $121.50 in 1792, realizing a handsome profit. The system of debt management instituted by Hamilton worked well to consolidate the debt and permit the government to make interest payments as they came due.

Fast forward to “modern history,” the 10-year climbed significantly during the 1920s, and then cratered post-“Great Depression” in the 1930s, where it remained quite low until it hit the “Mt Everest” of interest rate events: The Great Inflationary Spiral beginning in the 1960s, many believed triggered by run-away money-supply growth and the Viet Nam War; fueled further when Nixon took the US off the gold-standard (no longer could the holder of $35 US exchange that paper for an ounce of gold); and, finally, by efforts of the Federal Reserve and Chairman Volcker to crush inflation, once and for all.

Fantastic graphic. Clearly, there is no such thing as “the interest rate” for a 10-year Treasury. The interest rate at any moment in time is highly volatile. Rate movement over time is dependent on a large, but highly variable, group of data points which are in the aggregate opaque at any moment in time. Only in the rear-view mirror do cause/effect relationships appear obvious.

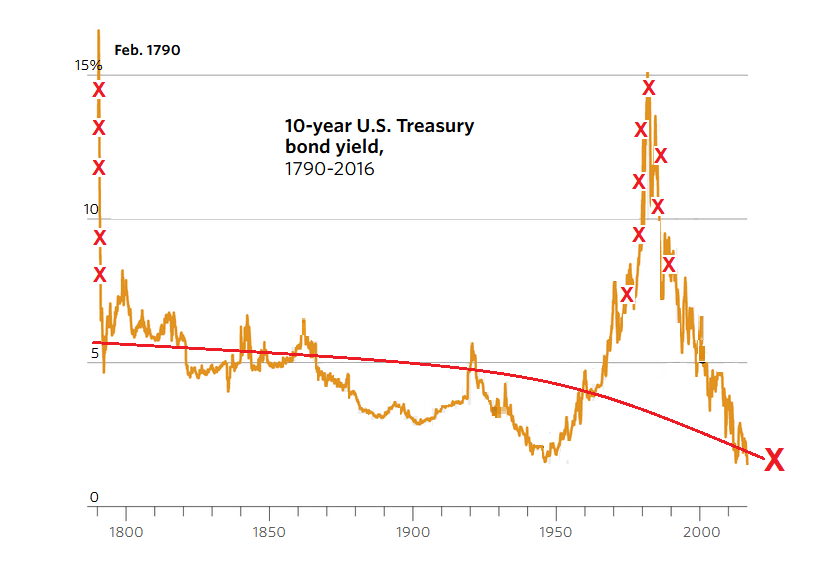

But is there any take-away here? Yes, I believe there is. Permit me to modify the graphic a bit and offer some of my own perspective. Take a look:

The yellow line is unchanged. But I’ve removed all the other “noise” from the image. And I’ve added a red line and some red “Xs.” Let me explain.

First, I eliminated all the commentary and the vertical recession ‘graybars.’ Then I added a number of red “Xs” over certain sections of the chart. I added them first where the time-line begins, back in 1790. The introduction of US Treasury debt for sale was clearly turbulent … and took a few years to settle in. For today’s purposes, we can safely ignore the very early rate data. Second, let’s talk about the rate climb over Mt. Everest. That episode was triggered by three things: Number 1: Year-after-year of exceptionally high inflation, beginning around 1965, a period now known as “The Great Inflation”; Number 2: Triggered by massive gold redemptions (the result of US inflation and dollar devaluation), Nixon eliminated the gold standard in 1971, triggering even greater inflation; and Number 3: The FED raises short-term rates to 20%. There’s your interest-rate climb over Mt. Everest. And here’s my belief:

This combination of events will never repeat.

Obviously, the United States can only abandon the gold standard just once. Once done, the event cannot repeat. Thus, the “Great Inflation” era that kicked into high-gear in the years immediately following the US exit from the gold standard will also not repeat:

And for that reason, we can ignore the “Mt. Everest rates” on the above chart for rate-forecasting purposes. Further, while it’s always possible the world will experience another pandemic-induced financial panic, the last one was about 100-years ago, so I think we can throw out the recent low-point of about 0.3%.

So we’re left with a rather interesting conclusion. As my red line shows on the 10-year bond graphic above, rates are heading lower. In my opinion, after things settle down, the 10-year Treasury is likely to head back to 2.00% or lower. I believe the direction is indisputable … only the timing is questionable. 🙂

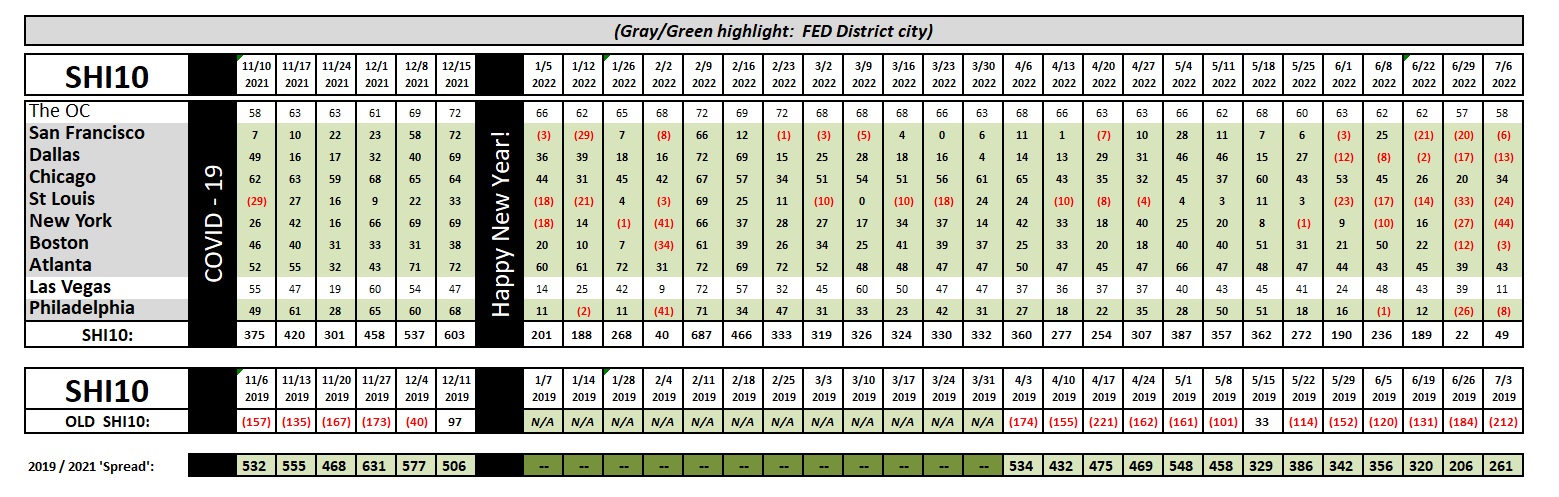

Let’s head over to Mastros.

Well, not much change from last week. Today’s SHI10 reading of 49 remains weak when measured against other 2022 results — at least those prior to last week. Reservation demand declined this week in most markets; however, demand increased slightly in Philly, Atlanta, and Chicago, to name a few. Orange County remains strong but ‘Vegas weakened noticeably. The numbers are weak … but they don’t suggest “recession” to me.

Nor do today’s numbers in today’s press release from the Bureau of Labor Statistics, the “Job Openings and Labor Turnover Report,” known as the JOLTs report. I was surprised to see how strong the ‘jobs openings’ number remains. On the last day of May, employers were still seeking 11.3 million new employees. Amazing. With all the FEDs efforts to crush inflation, I expected to see a significant drop. Nope. In fact, reading the report, the two words that seem to repeat over and over again are “little changed.” Openings were little changed from last month. Hires were little changed. Separations were little changed. I’m surprised. The employment market remains exceptionally strong.

Frankly, if we’re in a recession or economic down-turn right now, as many economists seem to be saying , it’s the weirdest recession I’ve ever seen. The National Bureau of Economic Research, known as the NBER, is US organization responsible to make the “official” determination about when a recession begins. And ends. Their pronouncement usually happen far after a recession begins or ends. Regardless, one criterion in just about every NBER recession is a rising unemployment rate. Which is not happening — at least not yet. Employment numbers are likely growing — next official release is on Friday. And the job openings certainly remain at exceptionally elevated levels. Weird times, folks. Very odd.

The FED minutes were released earlier today too. The buzzword from last year was “transitory.” These days, the FED likes to use the word “entrenched,” describing an inflation-expectation condition they hope to avoid. In other words, they hope any entrenchment of inflation expectations is transitory. Look at that: I got both words into the same sentence. 🙂

Strange times indeed. Thanks for tuning in.

<:> Terry Liebman