SHI 6.29.22 – $22 in 2022

SHI 6.22.22 – We Are Not Alone!

June 22, 2022

SHI 7.6.22 – Treasury Yield Tops 15.8% !

July 6, 2022

$22 in 2022.

That’s the headline today. Bank of America is trumpeting the fact that they have raised their minimum wage to $22-per-hour for full-time employees. Annually, that rate equals $45,760. Wow.

For a brief time while in college, I was employed as a ‘bank teller’ at the now-defunct Gibraltar Savings and Loan. I don’t remember what I was paid for one-hour of my time, but I can assure you it was a whole lot less than $22. I am amazed by the fact that in 2022 a bank teller can earn almost $46,000 per year. And the good news doesn’t end there for bank tellers: Bank of America has also shared that they plan to increase their minimum hourly wage to $25 by 2025. The translates to $52,000 per year for a full-time employee. Double wow.

I see what they’re doing here … $22 in ’22 and $25 in ’25. Catchy.

“

Wages are moving up.”

“Wages are moving up.”

All wages are moving up. Significantly. Across all industries. “Labor,” as a direct input cost, is becoming far more costly for most, if not all, companies. Big and small. But you already knew this, right? So maybe you can answer this question: How can Bank of America afford to pay such a high minimum wage and still remain profitable? It’s an interesting question to be sure … and one that kicks off today’s blog.

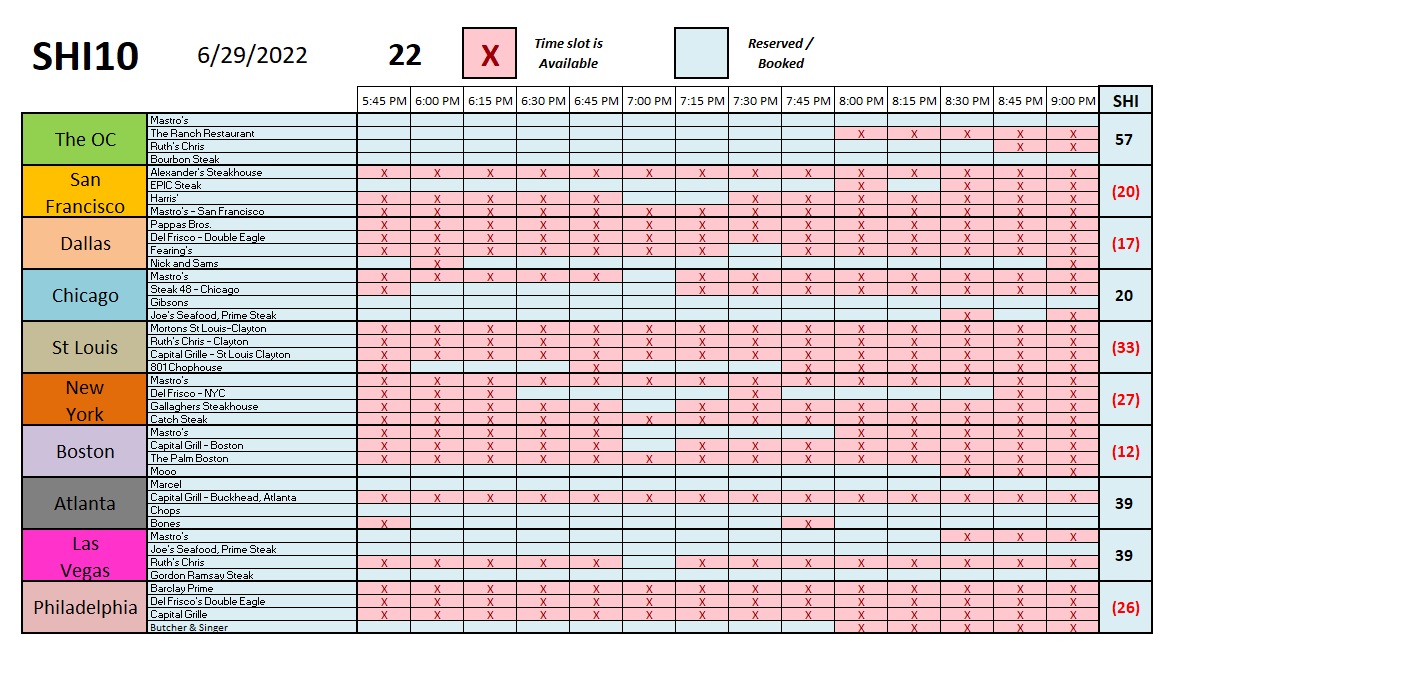

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Significantly. By the end of Q1, 2022, in ‘current-dollar’ terms US annual economic output clocked in at $24.38 trillion. Yes, during Q1, the current-dollar GDP increased at the annualized rate of 6.5%. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

How can Bank of America (B of A) pay a minimum hourly wage of $22 and remain profitable? Consider this fact: B of A has over 200,000 employees — many at wages far above the minimum. Business dynamics for banks are the same as for every other business: Gross revenue minus costs equals net income. If costs go up … the business better be able to lift income to remain profitable.

According to Bank of America, the 2022 minimum wage is up 46% since 2017. So in just 5-years, their minimum annual wage is up 46%. And that’s just their minimum wage. All other wages have most assuredly kept pace. Has their profitability suffered?

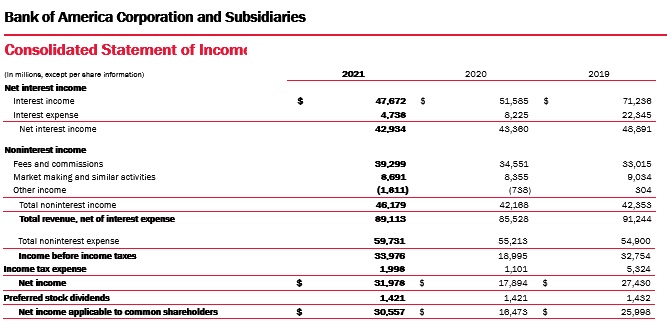

I copied the chart below from the B of A “2022 Annual Report,” reflecting annual operating results for 2019, 2020 and 2021. Let’s take a closer look and see if Bank of America has been able to remain profitable in the face of these substantial wage increases (Sorry for the slight blurriness — I enlarged the font for easier reading:)

Before we talk about profit, let me point out a few interesting items. First, notice that “interest income” declined from over $71 billion in 2019 to a paltry $47 billion in 2021. Ouch. Fortunately for B of A, at the same time “interest expense” declined from over $22 billion to just under $5 billion, meaning that “net” income from interest was down by less than $6 billion during that time. So while their income was dramatically impacted by the super-low rates, the amount of interest they paid out to depositors was also much lower.

Simultaneously, “non-interest income” increased significantly. Interesting. Non-interest income…for a bank. Hmmm. What would be included in non-interest income? That would be an interesting pool for a deeper dive. I’ll save this for a future blog.

Anyway, fear not! Bank of America remains profitable! Even with all the wage hikes, Bank of America was able to squeak out a $30 billion profit last year. That’s right: $30 billion. Phew. I was worried. 🙂

In the interests of brevity, I removed the “non-interest expense” section. Suffice it to say that “compensation and benefits” amounted to $31.9, $32.7, and $36.1 billion, respectively, for 2019, 2020, and 2021. Said another way, this wage costs were up 2.5% in 2020 over 2019, and up 13.2% in 2021 over 2019. This is a far-cry from the 46% minimum hourly wage increase. How is this possible? How can wages be up 46% (in the past 5-years), and yet the bank’s reported compensation costs are up only slightly over 15% in the past three years. Sure, the time periods are not perfectly aligned, but I guarantee you wage increase in 2017 and 2018 were very small. I’ll repeat? How is this possible? Hmmm…..

Of course, we’re looking at the past here … not the future … and it is that future that is far murkier. What impact will far-higher wages have on B of A in coming years? How will they maintain profit levels?

I contend the answer is relatively simple: The higher unit-labor costs become over time, the fewer employees B of A will employ. I suspect this process is already quite far along. How you ask? Automation.

According to the stock market, technology is dead right now. Tech companies are getting crushed. The “ARK Innovation ETF” — ticker ARKK — is down over 68% in the past 1-year. One dollar invested this ETF one year ago is now worth about 32 cents. Ouch. But stock prices don’t tell the whole or real story. Nothing could be further from the truth. Technology is doing just fine, thank you very much.

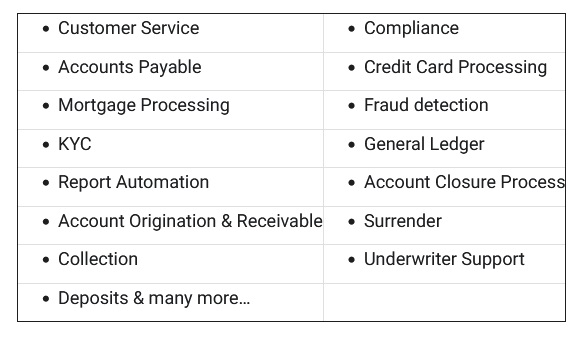

In fact, in recent years banking has embraced technology and Robotic Process Automation:

One company in the space, AutomationEdge, is now offering a product called “Conversational ITPA” with it’s “CogniBot” which does something I don’t really understand, as I am a mere, simple-economist type: It “engages customer with AI-powered conversations to provide end-to-end resolution to IT issues.”

Huh? CogniBots? Artficial Intelligence? Man, am I getting old.

Anyway, they describe RPA as “Robotic process automation has also dramatically streamlined a wide variety of back-office processes that once bogged down bank workers. By shifting much of these tedious, manual tasks from human to machine, banks have been able to significantly reduce the need for human involvement, which has had a direct impact on everything from performance and efficiency levels to staffing issues and expenses.”

Have you visited an ATM lately? Of course you have. Have you used your iPhone to deposit a check remotely? Sure. In fact, ask yourself this question: When was the last time you waited in line at a bank to see a bank teller? Right. I don’t remember the last time I was inside a bank.

According to AutomationEdge, robotic process automation has also dramatically streamlined a wide variety of back-office processes that once bogged-down bank workers. By shifting much of these tedious, manual tasks from human to machine, banks have been able to significantly reduce the need for human involvement, which has had a direct impact on everything from performance and efficiency levels to staffing issues and expenses, in areas such as:

In summary: In general, wages are up. Perhaps like me, you were amazed to learn that the “lowliest” of full-time employees banking are now earning almost $46,000 a year. But as sure as the sun will rise in 2025, Bank of American will have fewer employees in that year than they do today. Far fewer.

Social commentary aside, in the macro my take is that all wages are moving up quickly, today, and will achieve a significantly higher plateau than pre-pandemic. But when the dust settles after the FEDs current machinations, many companies will seek automation solutions to trim their growth in unit labor costs. Longer term, this once again suggests there will be fewer jobs available … but those individuals retaining or finding a positions will be earning quite a bit more than in pre-pandemic years.

And of course, the “billion-dollar question” is whether the trend will continue in future years. I contend it will not. I contend once the new wage-plateau is reached at higher income levels, the future trendline will then return to that of the 2010’s — wage growth rates will slow back to the historic mean.

Are you ready for a trip to the steakhouses? In light of the LOWEST-EVER reading in “consumer sentiment,” as reported yesterday by the University of Michigan — almost 4 out of 5 surveyed believe there are “bad times in the year ahead for business conditions,” — I’m chomping at the bit to see if reservation demand at the priciest of steakhouses has been dented by the consumer’s dour mood.

Yep. I’m sorry to report that expensive eatery reservation demand for Saturday is down. Significantly. We haven’t seen an SHI40 number this low since beginning the Steak House Index data tracking post-pandemic. If the FED has been hoping to slow consumer demand in their battle against inflation, I have good news for them: IT’S WORKING! YOU HAVE SUCCESSFULLY DESTROYED DEMAND!

Clearly, across the country, well-heeled, expensive steak-loving folks are cutting back … “trimming the fat” so to speak. For the first time post-pandemic, opulent steak houses that are perennially fully booked — like “Bones” in Atlanta, “Joe’s Seafood” in in Chicago, and “Mooo” up on Boston’s Beacon Hill — have openings this Saturday. They are typically fully booked. Here is the weekly SHI … take a look:

High-trend inflation, the FEDs efforts, and the all the resultant fear or anxiety from media reports have done their job. The SHI is flashing red, telling us the economy is now definitely slowing. Economic results for Q2 are now almost fully baked, so current conditions will probably show up in Q3 results. Q2 results may be strong. But the SHI is telling us, in no uncertain terms, there is trouble ahead for the US economy. How much … time will tell.

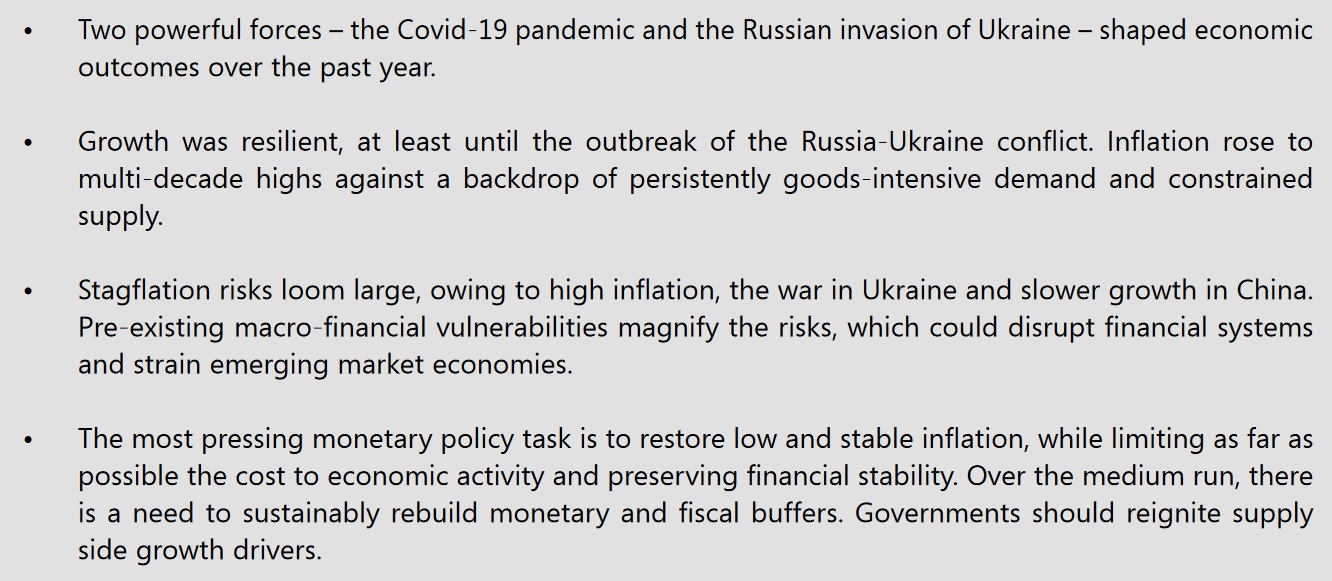

You may recall that last week I mentioned the Bank for International Settlements in my blog. I’m sure you’ll be excited to learn that they just released their 2022 Annual Economic Report! It tips the scales at a paltry 138 pages … so I’m sure you’ll want to read the whole thing! Here’s the link: (Right click … open in new tab.)

https://www.bis.org/publ/arpdf/ar2022e.pdf

Oh? You’re not interested in reading the report? OK, I understand. let me offer a few highlights, summarizing — thru an economic lens — how we got here today:

I thought the BIS summary above was spot-on. Accurate and succinct.

You may not be familiar stagflation. Essentially, the word suggest two economic events happen simultaneously: First, continuously high rates of inflation become the norm. In this regime, inflation rates remain high, month after month, without relief. Second, stagnant or declining GDP growth becomes the norm. Remember that “real” GDP growth is the nominal or “current dollar” GDP growth rate, deflated by the inflation rate. So, it’s worth mentioning that if inflation is running, say, 8% per annum, and nominal GDP grows 8% at the same time, the “official” GDP reading is zero.

Said another way, in a stagflationary environment, the United States could report no GDP growth for a quarter or a year, and at an 8% nominal growth rate, our $24 trillion economy will have grown by almost $2 trillion. That’s stagflation, folks. 🙂

Permit me to offer a small, silver-lining around today’s otherwise dismal report: I don’t believe long-term stagflation is in the cards. Sure, Q1 GDP results were a prime example of stagflation … and we may see a few more quarters where exceptionally high inflation readings dampen “real” GDP results. In the long-run, however, I still fully expect the inflation rate to fall and return to 2% or below. I may be the only remaining optimist in American on this topic, but I am steadfast!

Good luck out there … it’s gonna be a bumpy ride!

<:> Terry Liebman