SHI 8.4.21 – Facing the Delta

SHI 7.24.21 – Keeping it Real

July 28, 2021

SHI 8.11.21 – Deconstructing Productivity

August 11, 2021

Facing the future and the unknown, David Rosenberg is all gloom and doom.

“The bond market is saying we’re going to slow down materially now that the fiscal stimulus is over,” said Rosenberg Research chief economist David Rosenberg a couple of days ago. “We’re facing the delta … we’re going to have global headwinds. We’re past the easiest point of this ….”

In further comments, he called the 2nd quarter, 2021 GDP growth figures “disappointing.” Disappointing? Really?

Nope. Not even close. In fact …

“

… the US economy is cooking!“

“… the US economy is cooking!“

Real gross domestic product (GDP) at an annual rate of 6.5% in Q2 of 2021. That is a stellar number. Sure, it is less than the 8+% real growth rate expected by many economists, but if you dig just a bit deeper, you begin to realize just how stunning this achievement actually is.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

The short answer? Expanding. By a staggering measure. In fact, during Q1 and Q2, annualized 2021 ‘real’ growth averaged about 6.4%. In nominal terms, our US economy averaged almost 12% growth — adding $1.245 trillion of economic activity during the first half of the year. Forever more, COVID-19 will be mentioned concurrently with any discussion about 2020 GDP. Collectively, the world’s annual GDP was about $85 trillion by the end of 2020. But I am confident all 2021 GDP discussions will start with a nod to the blowout 1st quarter GDP growth number, because our ‘current dollar’ GDP grew at the annual rate of 10.7%! Annualized, America’s GDP blew past $22 trillion during the quarter, settling in at $22.72 trillion. The US, the euro zone, and China continue to generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Sure, the delta variant thing is a concern. And it should be. Once again, we face the unknown … there is much we do not know.

But we know a whole lot more now than we did 18 months ago. For example, from the CDC we know that as of today 70.1% of all adults have received at least one (1) dose of the vaccine. We also know, again from CDC data, that more than 99.99% of fully vaccinated people have not been hospitalized or died from a “breakthrough Covid-19 case.” That’s right: The updated CDC stats report that as of July 26, “breakthrough cases” resulted in 6,239 hospitalizations and 1,263 deaths. At that time, more than 163 million people in the United States were fully vaccinated against Covid-19. Thus, less than .004% of fully vaccinated folks ended up in the hospital … and less than .001% died. To be sure, this is a horrible outcome for those poor folks, but the statics don’t lie: If you’ve been fully vaccinated, for now at least, Covid is one less cause of death for you to worry about. Car wrecks should concern you more.

So, in the column of other things we know, we know the vaccine is extremely effective.

But delta is a concern. Rosenberg is right. Infections amongst un-vaccinated adults are growing quickly. So go ahead and add this to your bucket of things to worry about … and throw in a few others while you’re at it: New government-mandated shutdowns, new viral variants, variants that are vaccine resistant, lead in our municipal drinking water pipes — oh, no, that one actually did happen. Look, I could go on, and on, and on, but I’ll leave the scare-mongering and hand-wringing to other media sources. Worrying about the US economy is my beat, and fortunately for me, that’s one thing I believe we do not have to worry about right now. Because … and this is a direct quote from the BEA report …

“Current–dollar GDP increased by $684 billion in the second quarter to $22.72 trillion. This is an annualized rate of increase of 13%. In the prior (first) quarter, current–dollar GDP increased 10.9%, or $560.6 billion.”

OK, sure, the numbers I’m quoting above are not the ‘real’ numbers, so many economists would say I’m cheating. Those other economists would say that the ‘real’ number is more accurate, as it removes the effects of inflation from the quarterly economic growth figure. They would say that the nominal, or current-dollar, figures overstate growth because the ‘excess’ portion is not the result of operational improvement, but simply the fact that stuff cost more today than a calendar quarter ago. Valid arguments. But I would counter that we don’t live in a ‘real’ world — we live in the nominal world. The world where every day, the price we pay for stuff like houses, cars, groceries, cat food, electricity, gasoline, etc. is the ‘current-dollar’ price — and not the ‘real’ price.

Expensive steaks, too. We buy those using ‘nominal’ dollars, too. Can you imagine telling your waiter, “Wait! No, the price you’re quoting me for that filet Mignon is too high! I don’t want to pay that ‘current-dollar’ price … I want to pay the ‘real’ price … you know, the one determined from chained (2012) dollars? Right. That one!” That’s the price you want to pay, because that price, for your ‘current-dollar’ $60 filet is only $51! And while I don’t know if the waiter would throw you out of Mastros after calling you a ‘loon,’ there is one thing I know for sure: If you want that expensive steak, you’re gonna pay the price shown on the menu.

Look, here’s the point. Both numbers are meaningful. The ‘real’ number is an excellent way to track economic progress over time. With inflation effects removed, we are able to accurately measure true economic growth. But the ‘current-dollar’ number is quite meaningful, too. Like the inflated value of your house, it, too, offers us an accurate glimpse into the full picture — not the one adjusted downward for the effects of inflation.

Further, the BEA report says GDP increased by 6.5% in the second quarter … and the current-dollar number increased at a 13% annual rate … suggesting that the “appropriate inflation deflator” was about 6.5%. Which is absurd. Sure, sure, sure, the PCE price index, annualized, was running hot during the quarter. It clocked in at 6.4% … but using this factor to deflate the measured GDP current-dollar figure is excessive. In my opinion.

Frankly, I’m still blown away by the 13% annualized rate of increase. The US hasn’t seen that kind of GDP growth in decades. Let’s dig a bit deeper into the numbers: Where was the growth?

In consumption. In ‘personal consumption expendatures,’ (PCE) to be more specific. Yes, it should come as no surprise that people purchase a whole bunch of goods and services during Q2. In fact, PCE contributed all of the GDP growth for the quarter and then some. That’s right: The GDP figure was 6.5%, while the PCE contribution was 7.78%. That’s right — PCE increases exceeded the entire GDP growth for the quarter. That’s because “net exports” and “Government consumption expendatures” were both negative during Q2. The consumer, once again, is carrying the US economy.

As far as our national economy is concerned, the pandemic is over. The 2019, pre-pandemic, current-dollar US GDP of $21.43 trillion has now grown to a whopping $22.72 trillion (annualized). Amazing. Perhaps even more amazing is this quote from a recent article in the Economist magazine:

” … during the pandemic households have built up $2.5trn of extra savings, equivalent to 12% of GDP in 2019. In June a record-high number of Americans told Gallup, a pollster, that they themselves were thriving financially. It may be hard to lay your hands on a decently priced car, but so long as Americans venture out of their homes, the service sector can power the economy.”

Well said. To be sure, American faces headwinds and obstacles as it re-opens. Danger remains. But I’m betting the strong growth will continue. Shall we head to the steak houses and see if they agree? This week, let’s start with the trend report.

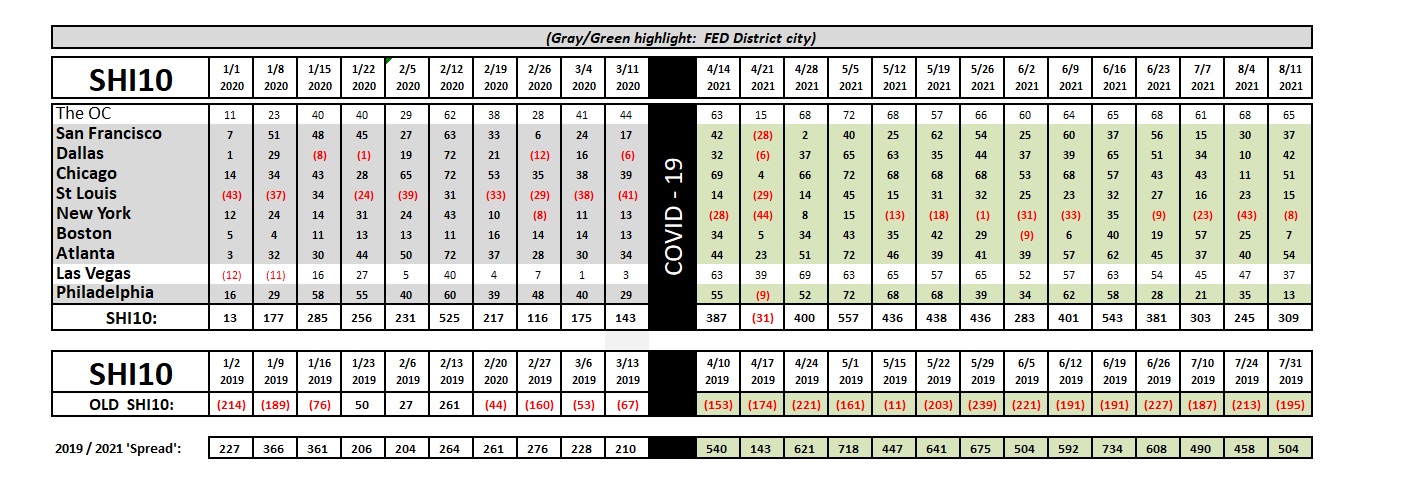

Interesting. The SHI10 ‘spread’ remains relatively consistent once again. However, the individual city contributions to this week’s SHI number were quite different from last week. This week, we saw significant increases in reservation demand in NYC, Dallas and Chicago. Expensive eatery demand weakened in Boston and Philly. Meaningful? Hard to say. With the rise of delta, NYC recently mandated that people who attend “indoor activities” — after August 16th — must show proof of vaccination. Will this help or hinder reservation demand? Time will tell.

Here are the detailed SHI10 numbers for this week.

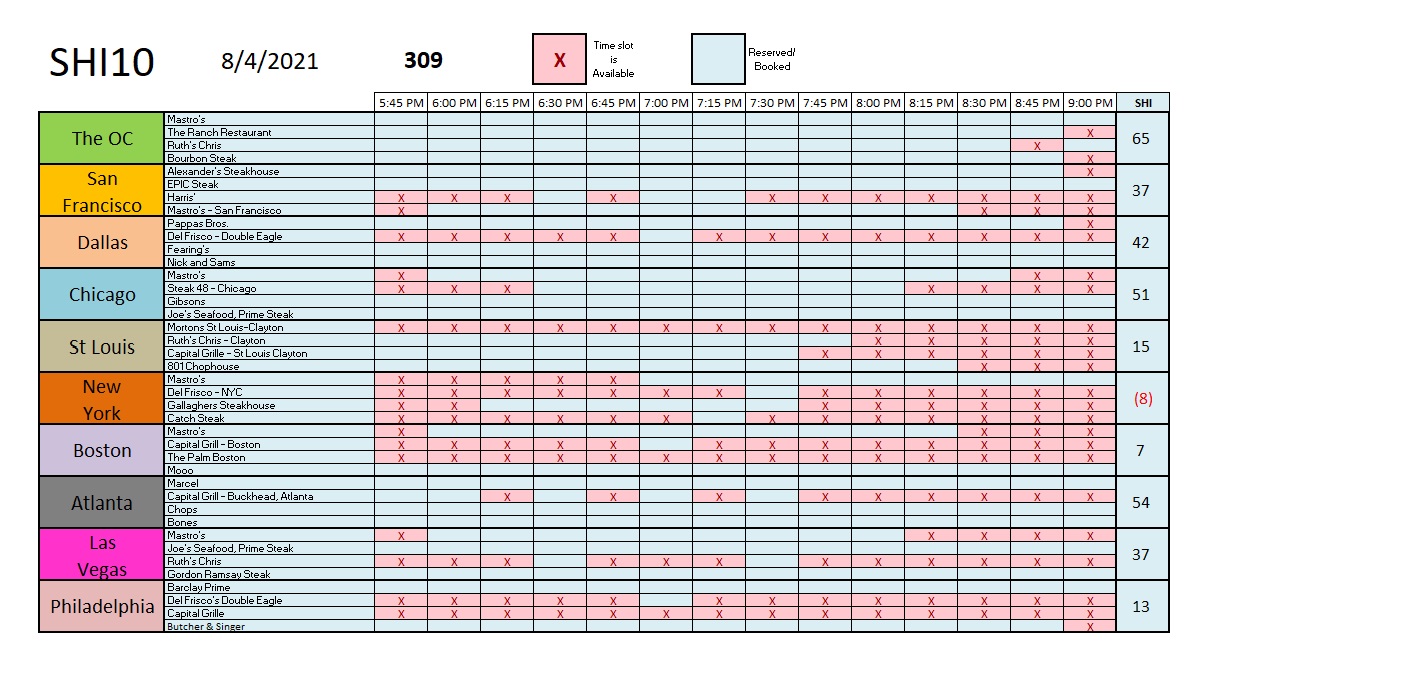

Many counties in San Francisco recently reinstated a ‘mask mandate’ for indoor activities … so, again, it will be interesting to see if this requirement adversely impacts pricey steak house reservation demand. For now, demand appears to remain strong. And, of course, here in the OC, expensive T-Bones are flying off the grill. Of the 56 reservation “slots” we track for the evening of Saturday the 7th, only 3 time slots remain open and available.

Have no doubt: The future is uncertain. As it always is. And the possible public policy responses to the delta surge might adversely affect economic growth. But I don’t think so. I think the world is significantly different today than it was 18 months ago. Today, I believe, businesses and governmental leaders will take a more individualized, more focused, response if infections surge. I expect to see the entire spectrum of choice outcomes. Unlike 18 months ago, however, I do not expect to see government mandated shut downs.

Time will tell. I’ve been wrong before … but we didn’t have 70.1% of the population partially- or fully-vaccinated before. For now, like that T-Bone at Mastros Ocean Club, it appears that the economy is sizzling. I believe this will continue.

<|> Terry Liebman